U.S. Review

Shock and Awful

- Daily life came to a screeching halt this week as governments, businesses and consumers took drastic steps to halt the COVID-19 pandemic.

- Financial markets seized up as it became clear just how much, and for how long, economic activity could be interrupted.

- The situation has rapidly progressed beyond being either a “demand shock” or a “supply shock”; it is an unprecedented interruption and reorganization of economic life.

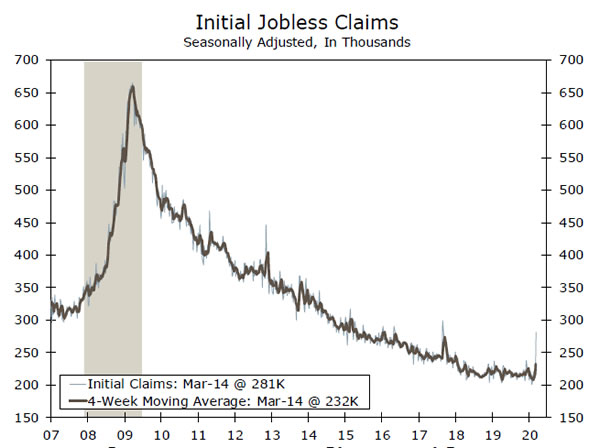

- We still have very few clues on how sharply spending will fall, but the incoming data will be unprecedented. Jobless claims will be in the millions next week.

Shock and Awful

Daily life came to a screeching halt this week as governments, businesses and consumers took drastic steps to halt the COVID-19 pandemic. U.S. equity markets fell 12% on Monday—the second worst daily loss in history—as it became clear just how much, and for how long, economic activity could be interrupted. Government-mandated closures of schools, bars, restaurants, gyms and movie theaters accelerated the shutdown and sent shockwaves through consumer-facing and discretionary industries. California, New York and parts of New Jersey went even further, ordering shelterin- place restrictions on non-essential movement. Thousands of retailers have closed and GM, Ford and Fiat Chrysler have shuttered their U.S. factories, with companies of all sizes and industries likely to follow. The situation has rapidly progressed beyond being either a “demand shock” or a “supply shock”; it is an unprecedented interruption and reorganization of economic life.

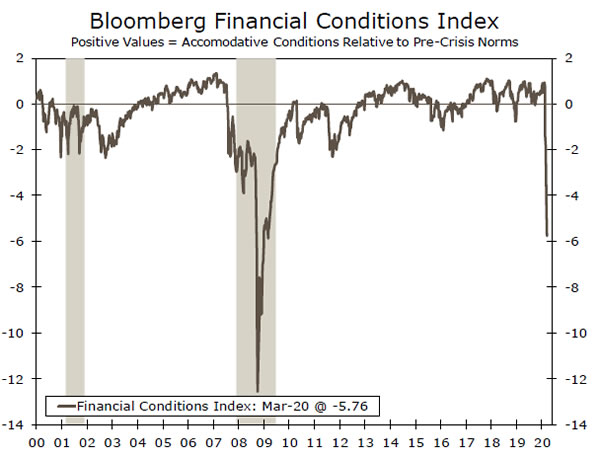

The abrupt suspension of the real economy threatens to morph into something much worse. In the words of Larry Summers, “economic time has stopped, but financial time has not been stopped.” Consumer rent, utility and credit card payments are still due, and corporations must meet payroll, rollover short-term liabilities and maintain working capital. Recognizing this risk, markets seized up this week, with assets selling off in unison and liquidity—even in typically very deep markets—evaporating. The Fed responded swiftly with a barrage of moves, including establishing a commercial paper funding facility (CPFF), primary dealer credit facility (PDCF), money market mutual fund liquidity facility (MMLF) and swap lines with foreign central banks to improve dollar liquidity. This is in addition to massive overnight repo operations, a minimum of $700 billion of Treasury and MBS purchases, a fed funds rate back at the zero lower bound, the elimination of reserve requirements and the encouragement of banks to use the discount window to “support the smooth flow of credit to household and businesses.” In short, the Fed wants to prevent what is fundamentally a health crisis from becoming a financial crisis, a credit crisis or a liquidity crisis, all of which appeared frighteningly possible this week, evoking memories of September 2008.

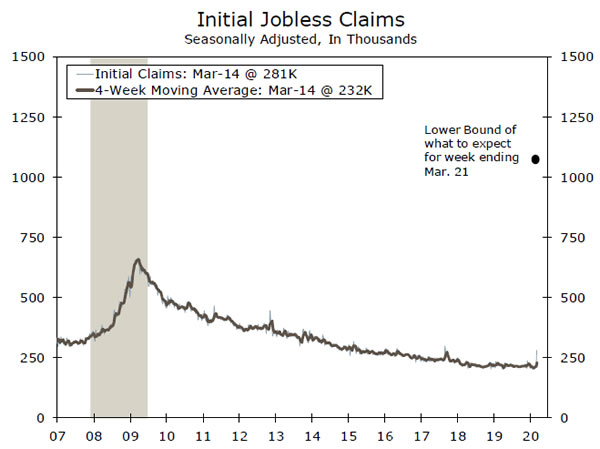

We still have very few clues on how sharply spending will fall, but the incoming data will be unprecedented. The New York and Philly Fed indices fell 34.4 and 49.4 points in March, respectively, while jobless claims rose to 281K. Next week, however, claims will likely be in the millions.

Unlike most economic data, financial markets are inherently forward-looking, and they are already telling us a lot, with the S&P 500 giving up almost a third of its value in the past few weeks. Yet no one has a clear view of how long the shutdowns and travel bans will last. The worst case scenario is truly ugly, but the Fed is not yet out of options and there are growing signs of a fairly robust fiscal response. The quality and quantity of stimulus will likely be the key to ensuring that the economy can get back on its feet once the public health crisis is resolved.

See a running tally of the policy responses here.

U.S. Outlook

Durable Goods Orders • Wednesday

COVID-19 has made the prior manufacturing outlook obsolete. Durable goods orders appear set to plummet in coming months, as uncertainty paralyzes capital investment and supply disruptions hit manufacturers. Initial purchasing manager’ indices available for March show a steep slowdown in activity—the Philadelphia Fed’s current activity index fell 49.4 points to -12.7, while the New York Fed’s index fell 34.4 points -21.5, easily the lowest reading since 2009.

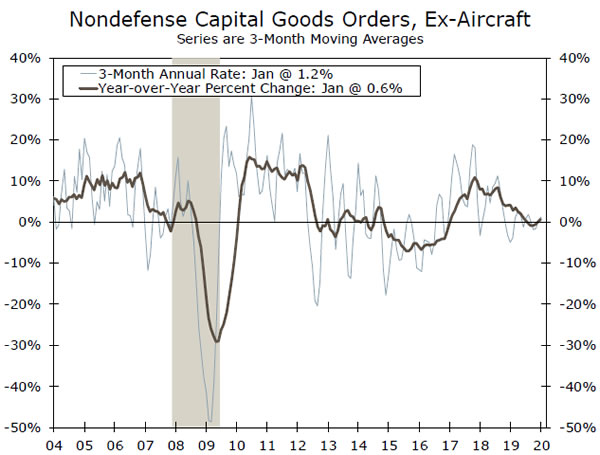

Next week’s durable goods report for February is likely too soon to see the hit, but it should be uninspiring nonetheless. Expect a big drawdown in the transportation line, again thanks to Boeing. Nondefense capital goods orders, excluding aircraft, may show further signs of stabilization, but it will not last.

Previous: -0.2% Wells Fargo: -1.4% Consensus: -0.8% (Month-over-Month)

Initial Jobless Claims • Thursday

Initial jobless claims are the highest frequency macro-indicator we have for the real-time impact of COVID-19 containment efforts, and its release has commanded much deserved attention. Initial claims jumped to 281K the week ended March 14. As you can see from the chart to the left, that is a significant pop, and puts claims at a level not seen in two years. But, that’s a drop in the bucket compared to what’s in store. Early state reports this week indicate initial claims for the week ended March 21 will rocket well over one million next week—and possibly as high as three million. That would surpass anything we saw during the financial crisis and could be upwards of three times the all-time high in claims set back in 1982. This will shock even the most bearish forecasters. As economic activity is grinding to a halt, the U.S. economy is quickly catapulting into a recession and in need of further policy intervention. For more see our recent report.

Previous: 281K Wells Fargo: 1-3M Consensus: 750K

Personal Income & Spending • Friday

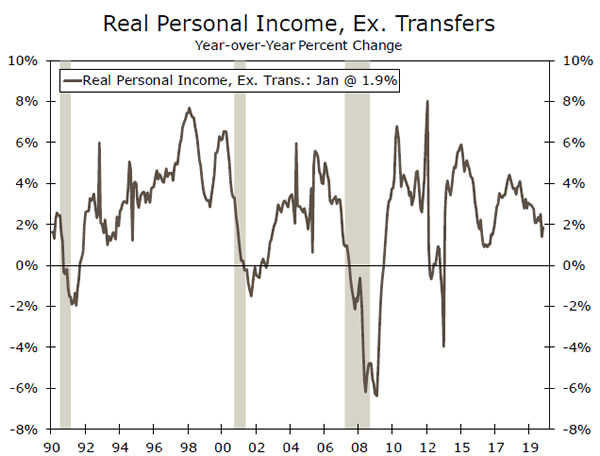

The personal income and spending report next week is for February, so it is unlikely to show any COVID-19-related slippage. In coming months, however, we will be paying particular attention to real personal income, excluding transfer payments. It is one of four primary monthly indicators used by the National Bureau of Economic Research to date recessions, and is a key indicator to watch to assess the extent of income lost from the mass layoffs.

We expect a wild couple of months of spending. Personal spending likely rose a trend-like 0.2% in February. But, there is perhaps big upside and downside for the March estimates. Anecdotal evidence suggests panic buying of food and personal items, but the closure of thousands of bars and restaurants across the country as well as travel bans suggest the service sector is getting whacked. Expect volatile consumption in the months ahead as consumers withdraw themselves from daily life.

Previous: 0.6%; 0.2% Wells Fargo: 0.3%; 0.2% Consensus: 0.4%; 0.3% (Month-over-Month, Inc; Spend)

Global Review

Easing Everywhere

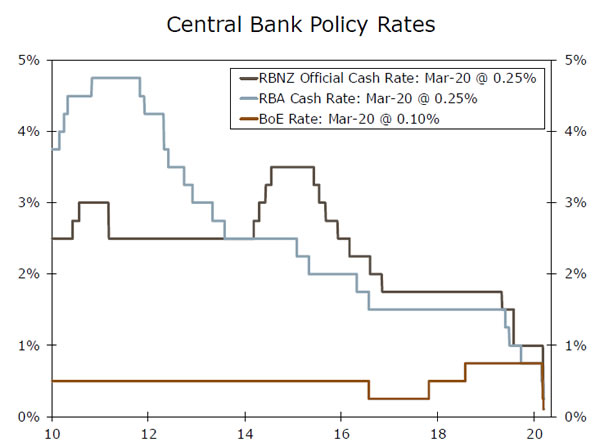

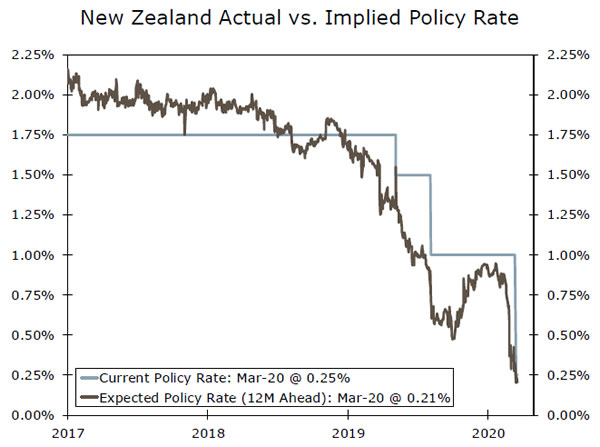

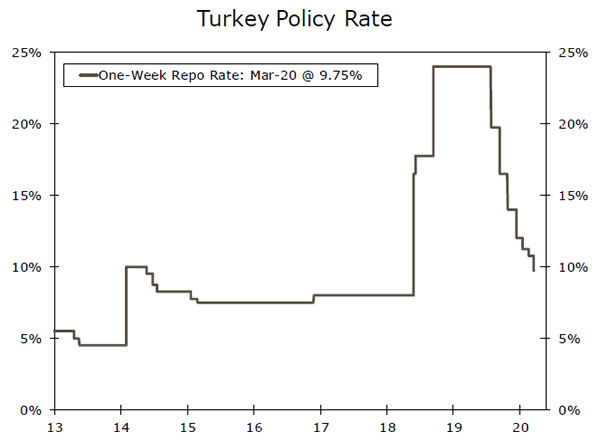

- It was a wild week for the global economy as concerns continued to mount surrounding the negative consequences of the coronavirus outbreak. Many central banks across the globe opted to cut interest rates this week, including the Reserve Bank of New Zealand. The central bank cut its policy rate 75 bps to 0.25%, while the Reserve Bank of Australia also cut interest rates 25 bps to 0.25%, and introduced quantitative easing measures. In a surprise move, the BoE cut rates 15 bps and increased its bond purchase program. Among other central banks to ease monetary policy include the central banks of Korea, Chile, Brazil, Turkey and Japan, as well as the ECB.

Easing Everywhere

Central banks remained in the spotlight this week. Broad fears that the spread of COVID-19 could bring a recession prompted central banks in numerous countries to ease monetary policy. To kick off the week, the Reserve Bank of New Zealand (RBNZ) surprised many market participants with its decision to cut its policy rate 75 bps to 0.25% after three meetings of holding rates steady, and stated rates will remains at this level for “at least the next 12 months.” The move follows many other G10 central banks that have eased monetary policy in an effort to cushion the economic impact from the COVID-19 outbreak. Similarly, the Reserve Bank of Australia cut its cash rate 25 bps to 0.25% and announced quantitative easing measures with plans to purchase government debt. Following the announcement, yields in Australia jumped, with the 10-year yield initially surging about 128 bps. Sticking with the G10, the Bank of Japan doubled its net purchases of exchangetraded funds to ¥12 trillion a year and introduced a new lending program to prevent further deterioration in confidence among households and businesses. In a surprise move, the BoE also cut rates 15 bps to 0.10% and increased its bond purchase program by £200B, while the European Central Bank (ECB) announced a package of asset purchases and other measures, known as the Pandemic Emergency Purchase Program (PEPP). The announcement included €750 billion in additional asset purchases through the end of the year, and additional flexibility in where it chooses to allocate its purchases, including Greek bonds. In addition, the ECB announced that it would be expanding its purchases under the corporate sector purchase program to include commercial paper, and eased collateral requirements for banks to access ECB liquidity operations.

With many G10 central banks cutting interest rates, emerging central banks have been under pressure to ease monetary policy as well. The Bank of Korea cut its policy interest rate 50 bps to 0.75% in an emergency meeting, and it also lowered the interest rate on the Bank Intermediated Lending Support Facility to alleviate some pressure on business owners and regional small-to-medium enterprises (SMEs). Elsewhere, India’s central bank announced liquidity-enhancing measures and hinted at a potential rate cut to mitigate any impact from the spread of the virus on its economy. As of now, other central banks including Chile, Indonesia, the Philippines and Brazil have also cut interest rates. The Turkish central bank was set to meet on Thursday, but moved the meeting to earlier in the week as fears regarding the coronavirus mounted. The central bank opted to cut its policy rate 100 bps to 9.75% from 10.75% on Tuesday.

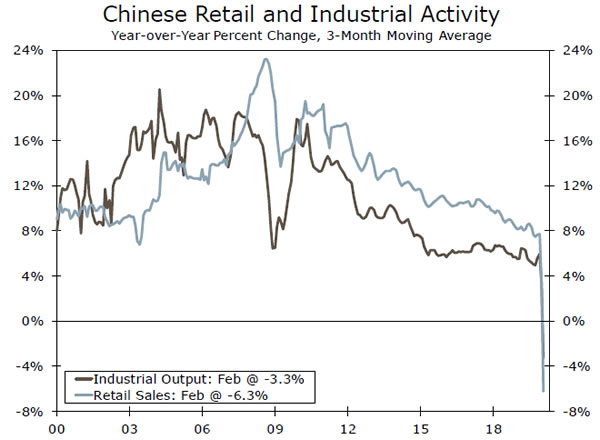

Among this week’s key economic data releases, China published some crucial economic figures for the months of January and February. Activity fell much more than expected as retail sales plunged 20.5% year-over-year, industrial output declined 13.5% year-over-year and fixed asset investment fell 24.5% yearover- year. The weaker-than-expected figures suggest that Q1 GDP growth could be even softer than we currently anticipate. As of now, we forecast the Chinese economy will contract on a sequential basis in the first quarter and grow only 3.0% for calendar year 2020, which would be the slowest rate of Chinese GDP growth in at least 40 years.

Global Outlook

Eurozone PMIs • Tuesday

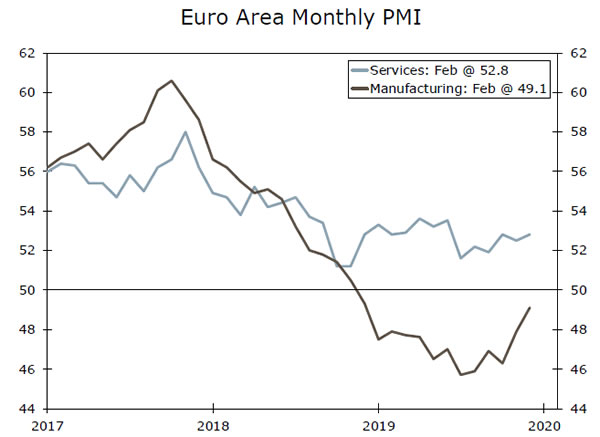

This week, in an emergency meeting, the ECB announced a €750B purchase program as credit risk among the region’s companies soars and the COVID-19 outbreak pummels the economy. The ECB said it is prepared to adjust the size and mix of its asset purchases to the extent necessary to implement an effective policy. Reinforcing the need for aggressive policy action from the ECB, the German March IFO business confidence index slumped to 87.7, the lowest level since 2009.

Next week’s release of the March Eurozone manufacturing and services PMIs will provide the first real insight into the extent to which the spread of the coronavirus is affecting the Eurozone economy. We will be focused mainly on the services sector as it has generally held up in recent months compared to the manufacturing sector. That said, we could expect to see some downside risks to both these figures given that the outbreak of the coronavirus across the Eurozone has weighed on sentiment and activity.

Previous: 49.2, 52.6 Consensus: 40.0, 40.0 (Manufacturing, Services)

United Kingdom PMIs • Tuesday

Earlier this month the Bank of England (BoE) delivered an unscheduled emergency rate cut of 50 bps. This week policymakers followed up its decision with its second emergency move, cutting rates 15 bps to 0.10% in an effort to cushion the U.K. economy from the negative economic effects of the coronavirus. In addition, the central bank announced that it would expand its government and corporate bond purchases by £200B.

Next week’s release of March PMI figures will be crucial, in the sense that it will provide some detail as to how the U.K. economy is holding up relative to the global shocks. We expect both the services and manufacturing PMIs will indicate sharp contractions stemming from the coronavirus outbreak. We look for the U.K. economy to contract 0.6% in 2020, the weakest year for the U.K. economy since the 2008- 2009 recession.

Previous: 51.7, 53.2 Consensus: 45.0, 45.0 (Manufacturing, Services)

Banxico Policy Decision • Thursday

The Bank of Mexico is scheduled to make a monetary policy announcement next week and is widely expected to lower its overnight rate another 50 bps to 6.50%, which is in line with our view as well. Before the coronavirus evolved, the Mexican economy was struggling to gain traction as it contracted in full-year 2019 for the first time since the 2008-2009 financial crisis. In response, the central bank began cutting interest rates. We still believe the central bank will ease monetary policy further, but the timing and magnitude of the cuts are somewhat uncertain.

On top of the coronavirus outbreak, the plunge in oil prices is also likely to depress growth in Mexico. We suspect the Mexican economy will continue to contract through Q3-2020 on a quarterly basis, and decline 0.4% year-over-year for the full calendar year 2020.

Previous: 7.00% Consensus: 6.50%

Point of View

Interest Rate Watch

Volatility Is a Sign of the Times

This was a momentous week for financial markets, beginning with the Fed’s full percentage point cut in the federal funds rate and announcement that it would purchase “at least” $500 billion of Treasuries and “at least” $200 billion of mortgage-backed securities (MBS). The open-ended commitment is notable, as is the Fed’s contention that this is not QE.

The Fed’s objective is to bring some order back to the credit markets by providing additional liquidity. Leaving the commitment open-ended was meant to assure the markets that the Fed would do whatever it takes to bring order back to markets. Order would be some tightening in the spread between most recent issued, or on-the-run, and previous issues, off-the-run bonds. The spread has widened as there has been an abrupt increase in demand for liquidity. The rush for liquidity is apparent in all asset markets, leading to highly synched trading. Almost everything is going up and down together.

The other takeaway from Jay Powell’s press conference last week is that the Fed is prepared to do much more. That became apparent over the course of the week, as the Fed rolled out its Commercial Paper Funding Facility (CPFF) and Money Market Mutual Fund Liquidity Facility (MMLF). Each new acronym the Fed rolls out is another piece of the puzzle that should serve to reduce some of the uncertainty in the financial markets. Nothing the Fed can do, however, can provide the answers the markets need most: How bad will the virus be, how long will it hang over the global economy and what will be needed to spark a rebound once the all clear signal has been given. Answers, either good or bad, should be coming in the next few weeks.

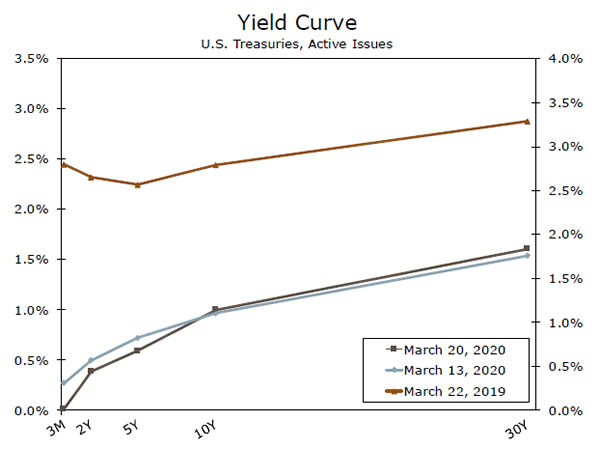

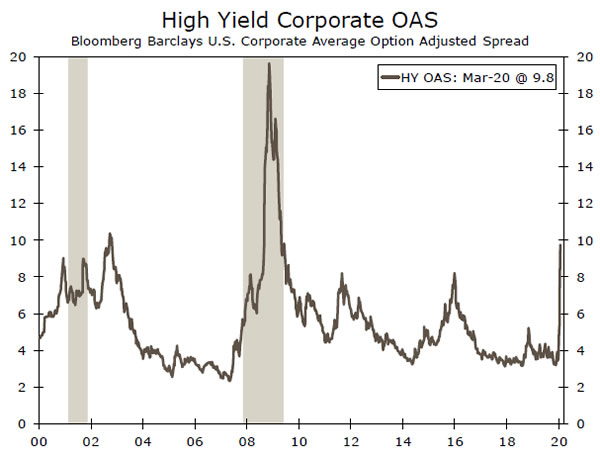

The bond market is ending the week with an upward sloping yield curve, albeit from an unusually low level. The spread between twos and tens is around 60 bps. The spread between Treasuries and High Yield Corporates remains wide and the Municipal market has been struggling not only with a rush for liquidity but a whole host of real and imagined fears about state and local governments’ ability to cope with the crisis.

Credit Market Insights

Debt in the Time of Corona

As businesses close and layoffs mount, it is clear the American economy is facing a potentially unprecedented drop in income over a short period of time. As we discussed in a report this week, it may be possible in some sense to replace this lost income, but deeper problems remain below the surface. For one, despite deleveraging over the past decade, households hold a large amount of debt. The bigger economic problems may begin if a loss of income starts to translate into debt defaults. Fortunately, policymakers are working across the board to develop solutions. Some proposed efforts have focused on the immediate problem, by supplanting the loss of income with checks to households, while others have focused on easing the immediate burden on debt. For example, last Friday the administration announced that it is waiving interest on all student loans held by federal government, bringing relief to some of the 43 million Americans with student loan debt. For mortgage debt, which makes up 68% of household debt, Fannie Mae, Freddie Mac and the FHA have announced moratoriums on foreclosures, along with payment forbearance for those directly affected by COVID-19. These measures are unlikely to bolster spending amid the broader tumult, but they could help prevent a cascade of defaults as many Americans see their incomes dry up. These efforts to shore up households will have important implications for the banking sector. For analysis on how the economic turbulence may impact business debt see Topic of the Week.

Topic of the Week

Public Health Crisis to Banking Crisis?

Last year, we wrote that the deteriorating financial health of the business sector made it more susceptible to shocks. That shock now appears to be upon us. Efforts to contain the spread of COVID-19 are bringing a significant portion of economic activity to a halt, along with a potential wave of defaults. While the spread of the virus and policymakers’ response will primarily determine how many businesses default, it is important to consider how the banking sector is positioned to handle the coming economic storm.

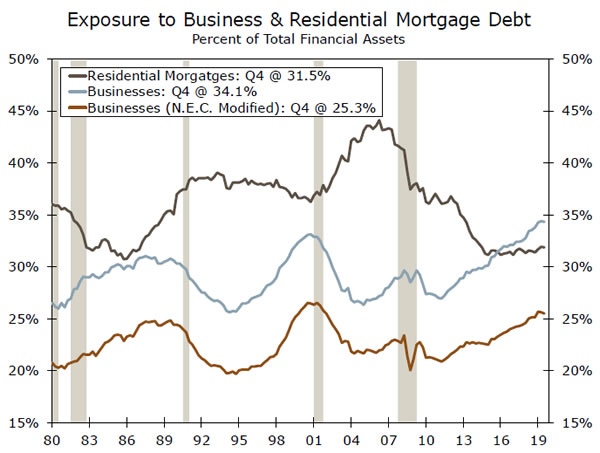

In a recent report, we estimated the exposure of U.S. banks to the non-financial business sector, based on banks’ loans to businesses as well as their holdings of corporate bonds, commercial mortgages and commercial mortgage-backed securities. In the top chart, the blue line represents an upper bound and the orange line represents a lower bound based on assumptions surrounding certain loan categories. For comparison, we also calculated banks’ exposure to the residential property sector, the primary catalyst for the previous financial crisis. While exposure to the business sector falls well below exposure to residential mortgages in the run up to the Great Recession, it currently stands at or near all-time highs.

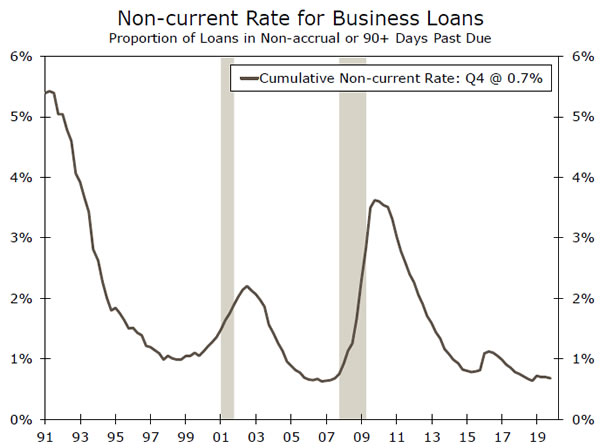

How many businesses will ultimately default is impossible to know. In prior cycles, the portion of commercial mortgages and C&I loans that reached 90+ days past due or non-accrual status depended on the depth and nature of the contraction in broader economic activity. For our time series, the non-current rate for business loans peaked at 5.4%, following the 1991 recession (bottom chart). Given today’s level of business loans outstanding, similar loan performance would imply $200 billion of delinquent loans on banks’ balance sheets. Fortunately, regulatory changes following the Great Recession have left banks with significantly more loss-absorbing capacity. The 25 largest banks hold roughly $1.1 trillion in common equity Tier 1 capital, suggesting they could withstand a doubling of the highest default rates seen since 1991 and still be considered wellcapitalized under the current regulatory definition.

{kind=link}