As a possible fiscal cliff looms in the United States, the August nonfarm payrolls report will be a crucial test for the strength of the economic recovery, making it the highlight of a relatively busier week as summer draws to an end. Canadian employment figures are also on the agenda, while the latest PMIs out of China will be important for market sentiment. But it is the Australian dollar that could see the most crossfire out of the major currencies as, apart from a policy meeting by the Reserve Bank of Australia, there will be a flurry of data releases.

A more dovish RBA?

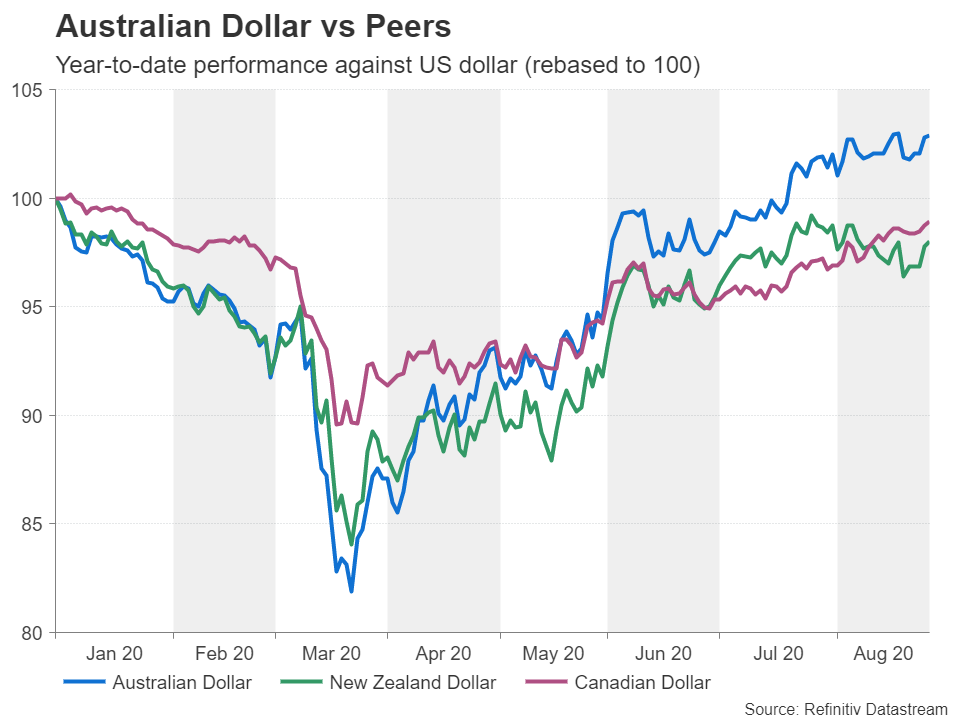

Just like stocks, the Australian dollar – a widely regarded barometer of risk appetite – continues to defy gravity, rallying sharply from the depths of the virus slump, even as the global pandemic shows no sign of abating. The aussie is up about 4% in the year-to-date versus its US counterpart, well ahead of its kiwi and loonie cousins. Those gains are thanks to Australia’s close trading ties with China, which has rebounded quickly from the coronavirus fallout, minimising the impact on crucial mining exports, as well as on the government’s strong initial response to contain the virus.

The comparatively mild hit to the Australian economy has meant the RBA hasn’t been required to do as much as other central banks to restore growth and doesn’t see a need for any further policy action for now. Thus, it’s almost certain the RBA will keep policy unchanged at its next meeting on Tuesday. However, the aussie may not necessarily be out of the woods as there is some evidence the second wave, which has put the country’s second most populous state back into lockdown, dented the recovery in August. Should policymakers display any fresh caution about the outlook, the aussie could face some selling pressure.

Aussie to likely shrug off domestic data

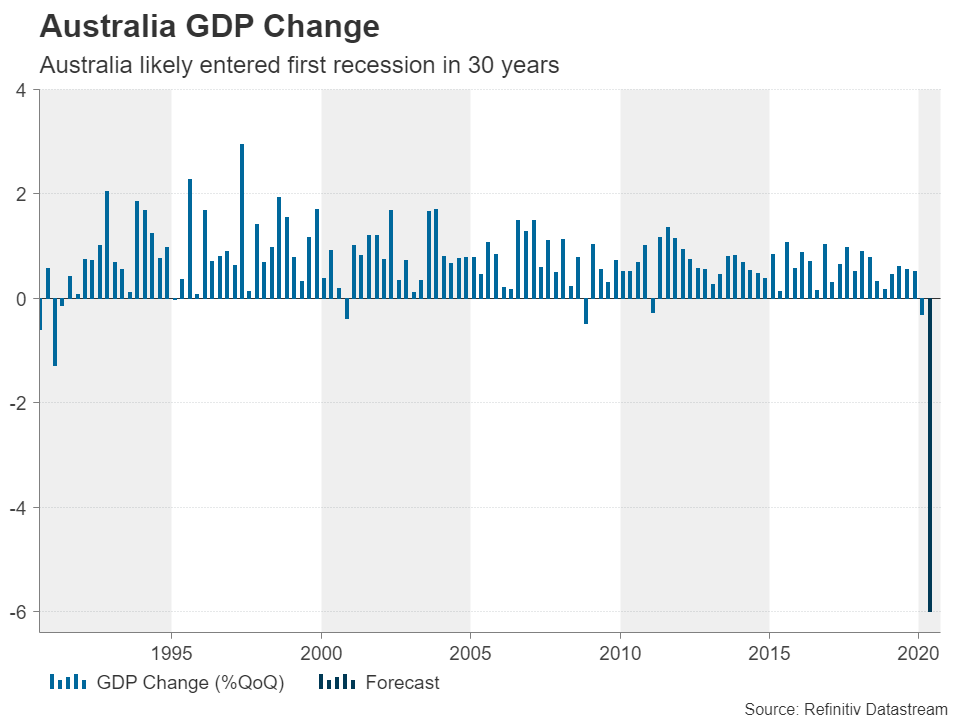

The recent deterioration in the Australian economy is not expected to show up in next week’s numbers, however. Kicking off the packed calendar are second quarter business inventories and July private sector credit figures on Monday, followed by Q2 net exports contribution and July building approvals on Tuesday. On Wednesday, the Q2 GDP estimate will be attracting headlines but may not be particularly market moving as a big surprise is unlikely. Lastly, retail sales for July are due on Friday.

With the above data considered to be somewhat out-of-date now, the latest PMIs out of China might provide bigger excitement for aussie traders. China’s official manufacturing and non-manufacturing PMIs for August are both out on Monday and will be followed by the Caixin/Markit equivalents on Tuesday (manufacturing) and Thursday (services). Any unexpected weakness in the Chinese PMIs could knock back risk appetite, though only temporarily as has been the case lately for nearly all negative news flow.

Dollar/yen’s downdrift may start to worry BoJ

Staying in the region, several key indicators are scheduled out of Japan in the coming days. They include preliminary industrial output and retail sales figures for July on Monday, and unemployment and Q2 capital expenditure numbers on Tuesday. The business spending gauge will be monitored for possible revisions to Japan’s Q2 GDP, but on the whole, the data are not anticipated to have a significant bearing on the yen.

Policymakers at the Bank of Japan on the other hand will be keeping an eye on both the data and the yen as a slow recovery combined with persistent US dollar weakness could spur them into action. The BoJ may have very limited tools left at its disposal but it is still capable of influencing policy by strengthening its dovish forward guidance. Ergo, the closer dollar/yen falls to the 100 mark, the higher the pressure will be on policymakers to do more.

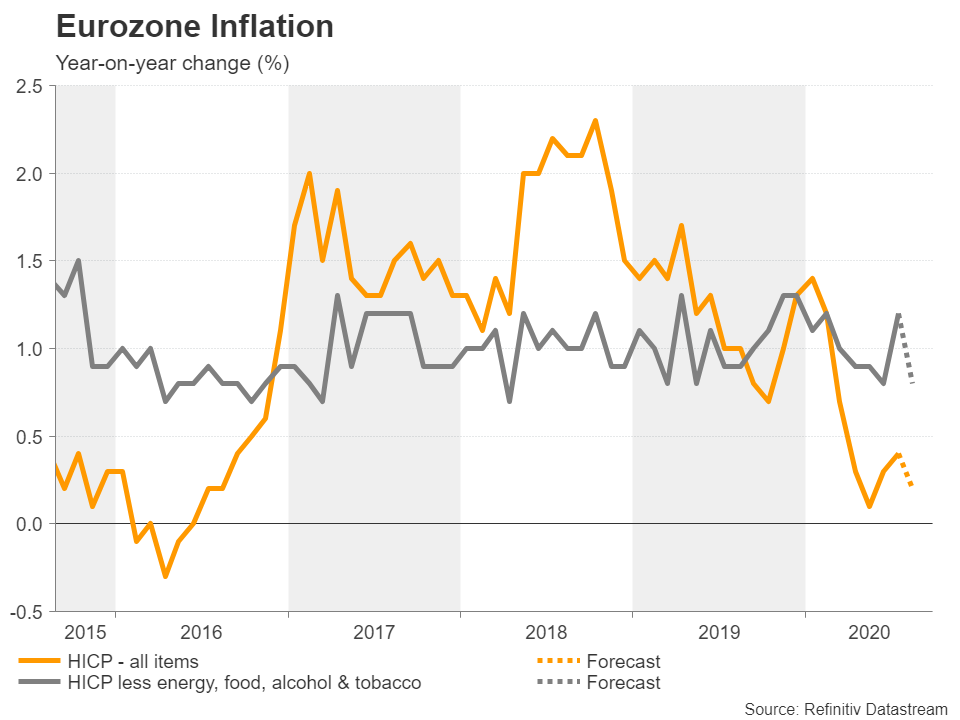

Eurozone inflation moving dangerously close to zero

Another central bank where the exchange rate could soon be causing it headaches is the European Central Bank. Although the euro’s rally has moderated lately, and euro/dollar might even be entering a consolidation phase amid signs the Eurozone recovery is stalling, further appreciation in the currency would amplify the downward pressure on prices. The pandemic shock has pushed annual inflation in the euro area back below 1% and is forecast to fall further, to 0.2%, in the flash estimate for August, which is due on Tuesday.

The headline as well as the underlying rates of inflation will be watched closely ahead of the ECB’s policy meeting in the following week. Other data out of the Eurozone that might attract interest next week are German industrial orders on Friday and the final August PMIs on Tuesday (manufacturing) and Thursday (services). After the surprise drop in the flash readings, any upward revisions to the final PMIs might help ease concerns about a slowing recovery, lifting the euro.

US jobs gains to slow further; will markets care?

Despite a major escalation in virus cases in the US over the summer that led to tightened restrictions across many states, the American economy has been chugging along, confounding dire predictions that the recovery would stutter. Yet the Fed remains unimpressed by the improving data and by just announcing its biggest policy shakeup in years, it’s given a very strong signal to the markets that interest rates will not be going up until unemployment has come down substantially from current high levels.

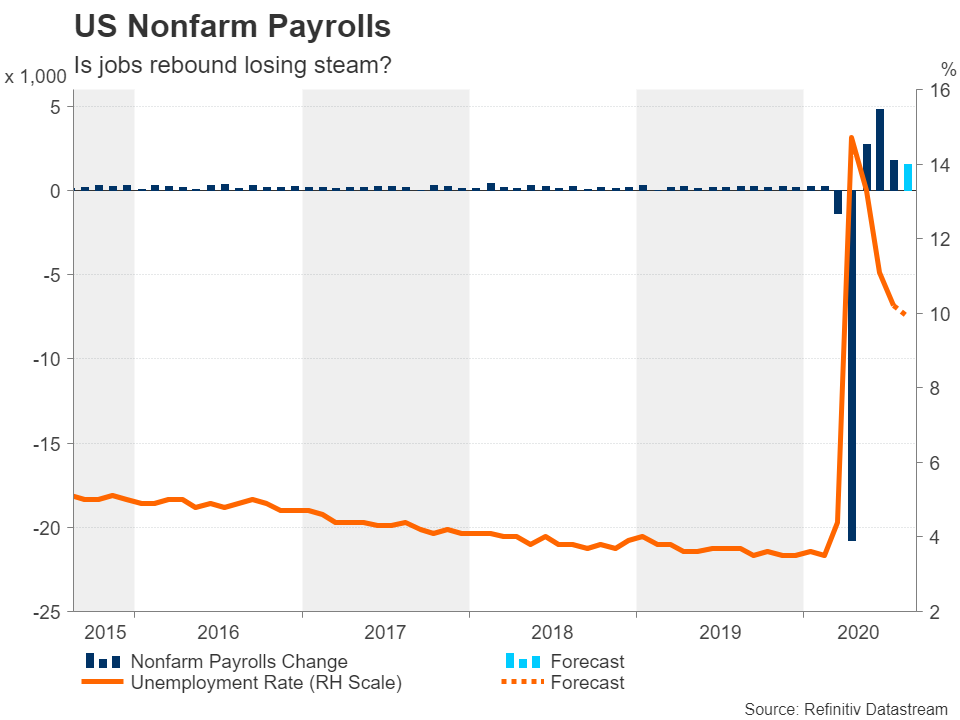

Looking at weekly jobless claims, it’s no wonder the Fed is worried. Initial claims for unemployment benefits have flatlined around 1 million in recent weeks. While this may be significantly down from the peak of 6.6 million in April, it’s still extremely high by historical standards. The slowing trend is likely to be reflected in the August nonfarm payrolls report out on Friday.

Analysts are projecting payrolls to rise by 1.55 million, which may seem like a large number but would only be enough to nudge the unemployment rate down from 10.2% to 9.9%. Compared to where the jobless rate was prior to the pandemic – at 3.5% – there is a long way to go before the Fed can say mission accomplished.

Markets do not appear too stressed about the lengthy road to recovery because they believe there will be an endless supply of monetary and fiscal stimulus to revive growth. But investors may be underestimating the lasting economic effects of demand, consumption and employment staying depressed for a protracted period. And if bond markets are correct in what they’re signalling, the Fed’s job of keeping rates low might get complicated by rising inflation.

However, as far as Wall Street is concerned, this is a problem for another day and even the dollar might struggle to find much direction from the jobs report. Instead, investors will probably take comfort from the ISM manufacturing and non-manufacturing PMIs, which are due on Tuesday and Thursday, respectively. Both PMIs are expected to edge slightly lower in August but remain comfortably above the 50 expansionary level.

Loonie seeks jobs boost

Employment figures will be doing the rounds in Canada too on Friday and unlike in the US, the report could have a stronger impact on the currency. The Canadian dollar is currently trading at 7-month highs versus the greenback, as investors turn more confident about the recovery prospects of Canada’s economy, both on the back of an improving domestic picture as well as receding fears about the recovery of its southern neighbour, which it relies on heavily for trade.

Any further improvement therefore in the labour market in August could lift the loonie to fresh highs.

{kind=link}