It’s an action-packed week, with three major central bank meetings, the election over who will become Japan’s next leader, and an overload of key economic data. The Fed decision will be crucial. Will the central bank reinforce its new inflation regime by signaling imminent stimulus, or will it sit back until the US election has passed? Neither the Bank of England nor the Bank of Japan is likely to act. Instead, those currencies may be driven mostly by how the Brexit saga and global risk sentiment evolve.

Fed: Snoozing until November

The past few weeks have been one wild ride for financial markets, with the Fed announcing it will change its inflation-targeting regime, the ECB talking down the euro, Boris Johnson making another ‘power play’ in the Brexit talks, and stock markets falling from their heights. Fortunately, things will stay exciting for a while longer.

The Federal Reserve will wrap up its policy meeting on Wednesday, and the question is whether policymakers will try to make their new ‘inflation overshooting’ framework more credible by hinting at new measures to boost inflation, or whether they think they have done enough for now.

Judging by some recent comments from policymakers and the minutes of the July meeting, the Fed is more likely to take the sidelines. The minutes implied there is no rush to strengthen the forward guidance, a view echoed by a few officials lately, who hinted they would like some more clarity on the economy’s path before committing to anything new.

Since economic data have remained encouraging, with consumption bouncing back nicely and the jobs market recovering at a healthy clip, there’s little pressure on policymakers to act immediately. After all, there is also an election approaching fast, so it makes sense to wait before taking any major decisions. The outlook for government spending will become clearer after the election, so Fed officials will have a better sense of how much more stimulus is needed.

All told, this meeting might serve mostly as a public relations exercise, where the Fed explains its newfound tolerance of higher inflation in more detail, rather than deliver new easing signals. That may come as a disappointment for those looking for dovish guidance, in turn lifting the dollar a little, especially if some policymakers pencil in rate hikes in the new ‘dot plot’ for 2023.

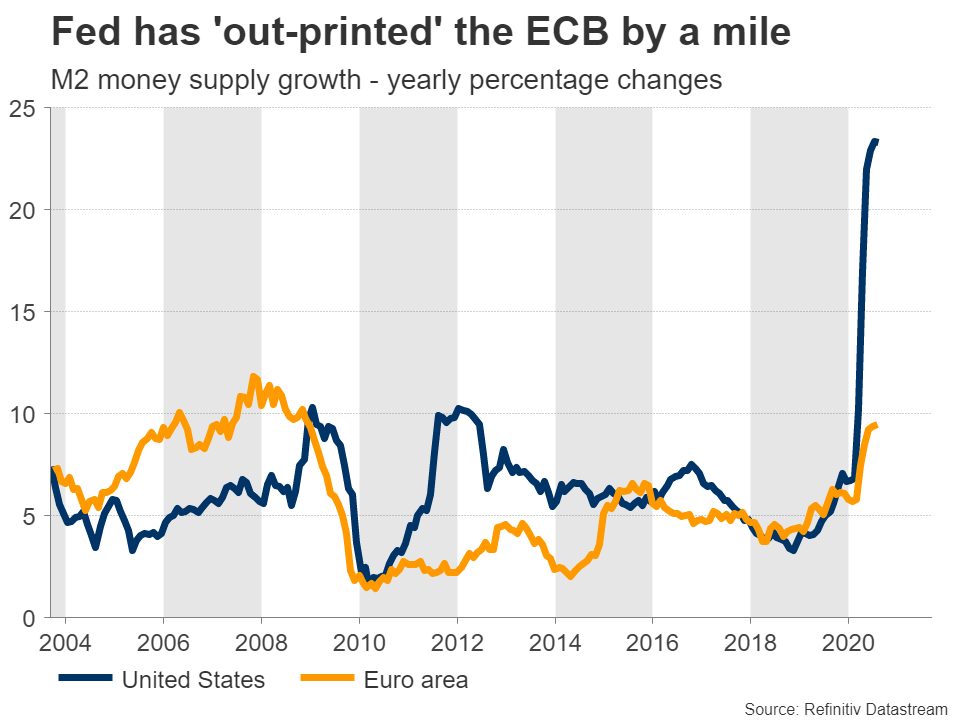

Having said that, it is difficult to envision any sustained dollar rally in an environment where the Fed is ‘out-printing’ the ECB, global inflation expectations are moving higher, Biden is ahead of Trump, and stock markets are near record highs.

The nation’s retail sales for August will hit the markets a few hours ahead of the Fed decision.

Yen: Prepare for turbulence

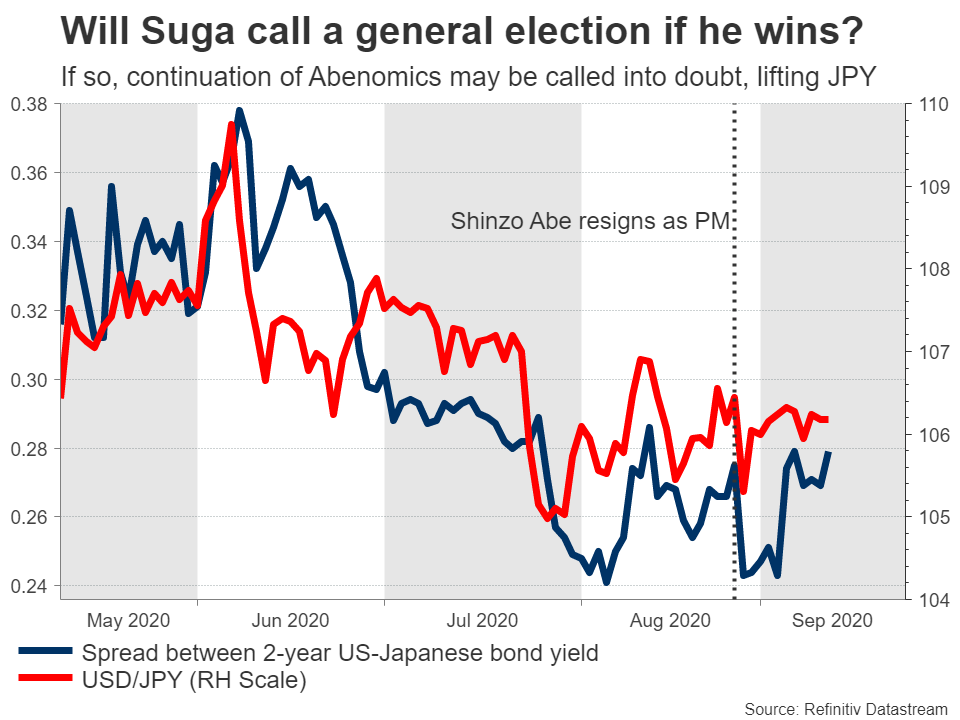

In the land of the rising sun, Monday will bring the leadership election of the Liberal Democratic Party to determine who will succeed outgoing Prime Minister Abe. The clear favorite to win is Yoshihide Suga, Abe’s Chief Cabinet Secretary, who has consolidated support within the party. Suga has vowed to continue ‘Abenomics’, so his victory would normally imply some downside in the yen, though this may be priced in already amid expectations of a landslide win.

That’s the expected part. What might catch markets by surprise is Suga calling a snap general election after he wins. The rest of Abe’s term would end in one year, so if Suga becomes Prime Minister, he may call an early general election now that he is riding high in opinion polls and his party is unified behind him, to improve his chances of winning a full term in office. If so, this might lift the yen, as a general election would present a risk to the continuity of ‘Abenomics’.

On Thursday, the spotlight will turn to the Bank of Japan’s meeting. No action is expected, though the latest reports suggest the BoJ may offer a slightly brighter view of the economy. Still, any market reaction might be minimal, with the yen likely to take its cue from politics and the global risk mood instead.

Pound haunted by Brexit, looks to BoE

The British pound came under heavy fire lately, after the UK tried to play hardball in the Brexit talks. Boris Johnson threatened to walk away from the negotiations if no deal is reached by mid-October, with his government also introducing legislation that would undermine the divorce pact the UK signed with the EU last year.

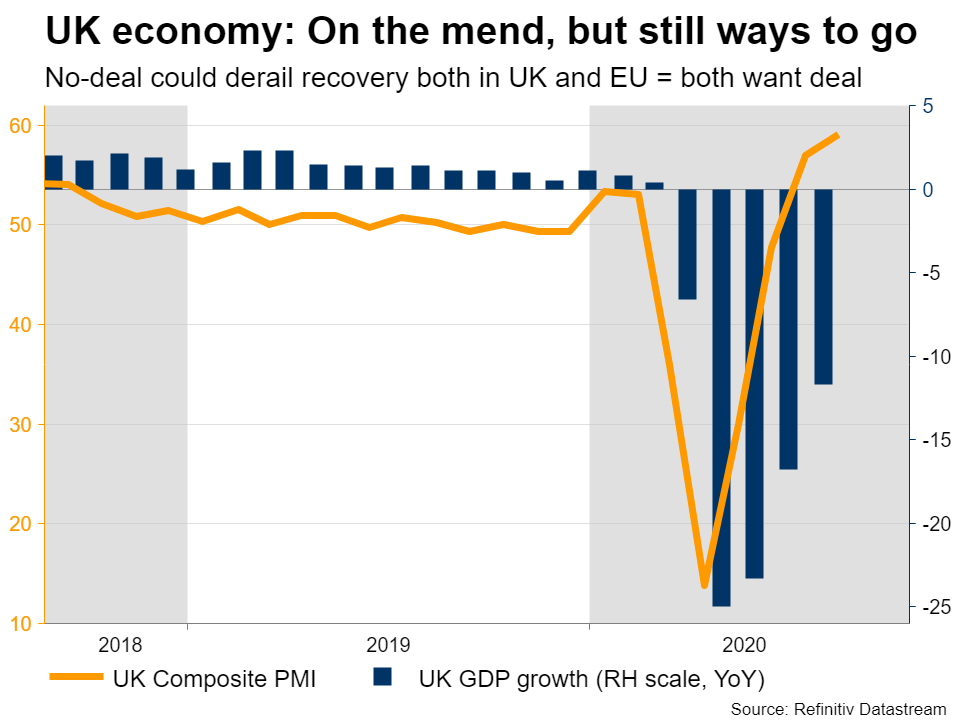

The bottom line is that tensions have escalated once more and the risk of a no-deal exit is on the rise, but this is not entirely surprising. Boris used the exact same tactic last year to extract concessions, and it worked.

Hence, the political posturing is likely to intensify over the coming weeks, spelling more pain for the battered pound. That said, an eleventh-hour deal still looks more likely than not, so while sterling may suffer for a while, it could stage a very powerful comeback once some concessions are made. Of course, that is unlikely to happen until the last possible moment, which might mean early-November.

The BoE meets on Thursday, but it might not be a major driver for the pound. Economic data have been improving, and it is too early for the Bank to react to the turbulence in the Brexit talks. With policymakers also downplaying the prospect of negative rates lately, markets will be on the lookout for any signals about the QE program being expanded in November.

Speaking of economic data, the British jobs numbers for July are out Tuesday, before inflation stats and retail sales for August hit the markets on Wednesday and Friday, respectively.

Commodity currencies brace for key data

There’s also an avalanche of data coming up in Australia, Canada, New Zealand, and China.

In Australia, the jobs report for August is due Thursday, with forecasts pointing to an increase in the unemployment rate. It seems the impact of Victoria’s lockdown is finally showing up. The RBA pays a lot of attention to employment, so a dire set of data may add credence to its own forecasts that the unemployment rate is headed to 10% by year-end, amplifying expectations for a 10 basis points rate cut.

Over in Canada, inflation numbers for July are out Wednesday, ahead of July retail sales on Friday.

In China, retail sales, industrial production, and fixed asset investment – all for August – will see the light on Wednesday.

Finally, New Zealand’s GDP numbers for Q2 are due on Thursday, but this is ancient history by now.

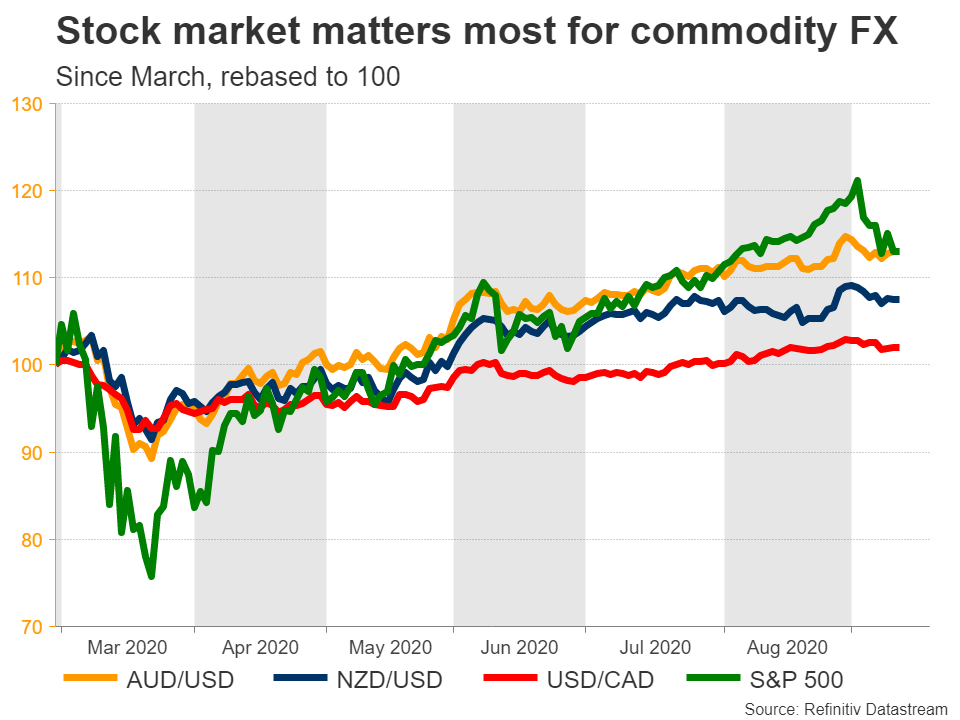

Instead of the data, the primary driver for all these currencies might be how global risk sentiment changes, and specifically whether the recent stock market selloff continues.

{kind=link}