It is probably the busiest week ever for markets. The US presidential election will eclipse everything else, but there are several other crucial events like a Fed meeting and nonfarm payrolls to follow the main dish. The Bank of England and the Reserve Bank of Australia will decide as well and both are ‘live’ meetings, where more easing is expected. Overall, the tone in the FX and stock markets will depend mostly on the election outcome, and whether we have a clear result on election night.

Markets on edge as election tightens

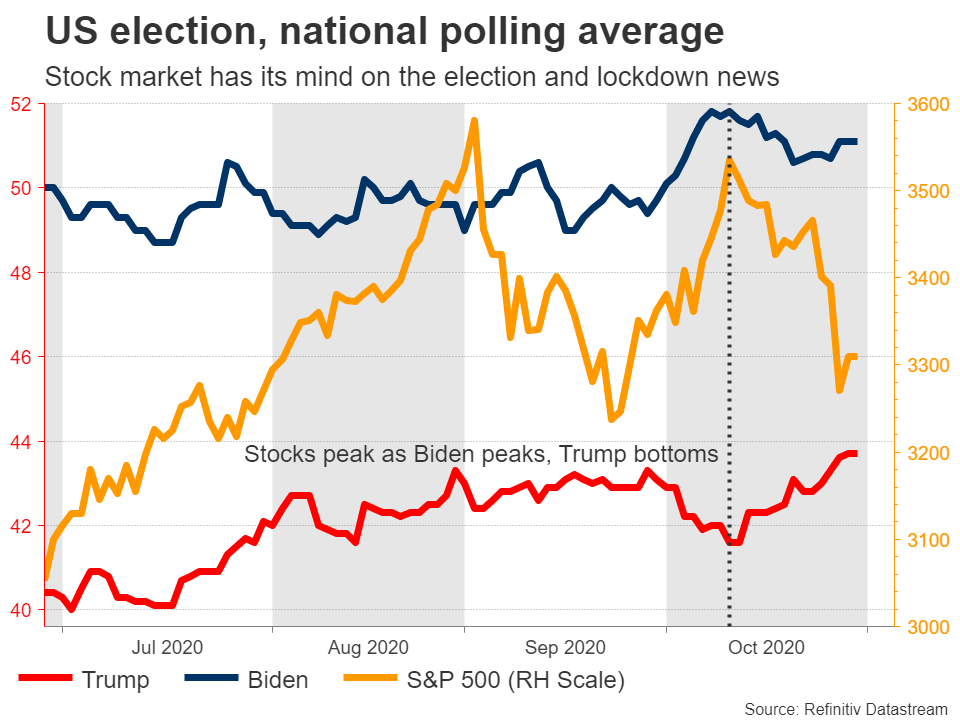

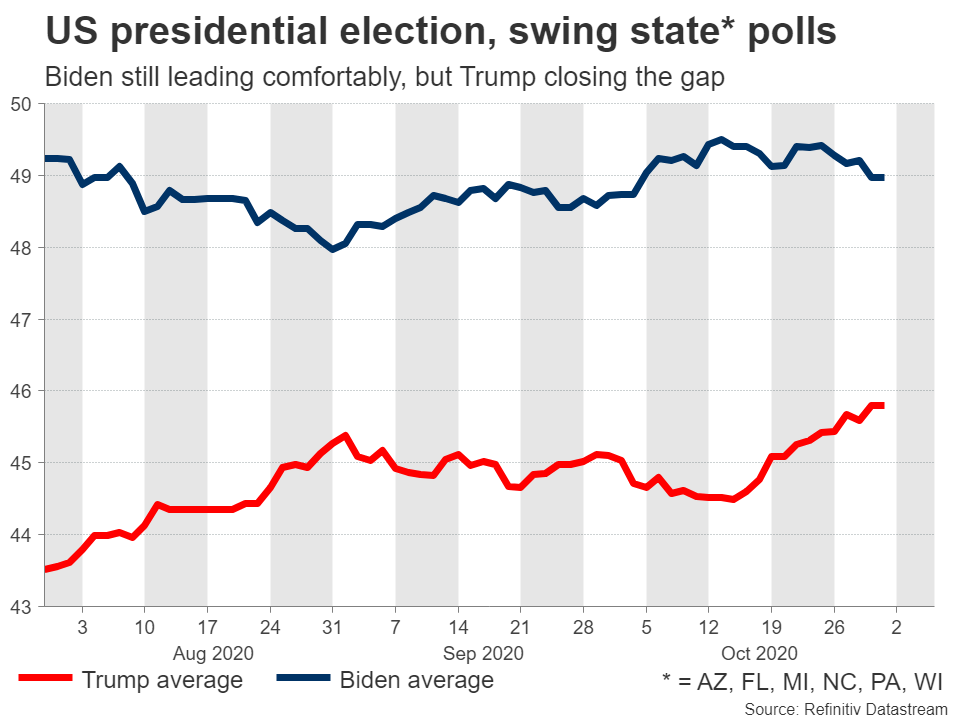

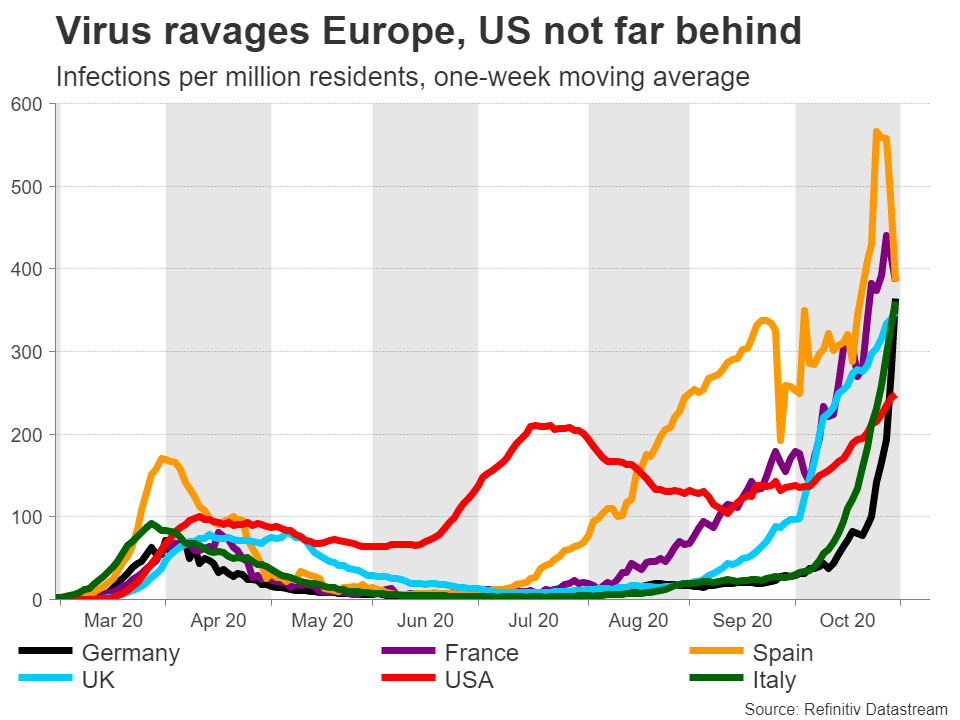

It has been a wild week, with stock markets tanking and the defensive yen soaring as Europe went back into partial lockdowns and the US election race tightened. Opinion polls still have Biden comfortably ahead, but Trump has narrowed the gap, and investors are reducing their risk exposure ahead of the event in fear of another upset.

According to betting markets, the most likely outcome is still a landslide Democratic victory, with the probability that the Democrats take full control of government resting at ~56%. This scenario is expected to deliver massive stimulus packages to heal the economy, so it could boost the wounded stock market but sink the US dollar on concerns of gargantuan deficits.

However, there is an equally good chance that we end up with a divided government, where no single party controls all of Congress and the White House. A lot will depend on the race for the Senate, which is too close to call. The market reaction would vary depending on who takes what. For instance, if Biden becomes President but the Republicans keep the Senate, they will likely veto most of his stimulus proposals and the result could be another wave of risk aversion.

But the most bearish outcome for the markets may be a contested election. If the numbers are close and Trump loses, he might dispute the result in the Supreme Court, leading to weeks of uncertainty. The initial reaction to that may be a sharp selloff, but it might not last long. Once the smoke clears, many players could see this as a buying opportunity.

Overall, Biden has a much bigger lead than Clinton did against Trump at this point, both nationwide and in most battleground states. Election polls were spectacularly wrong in 2016, but pollsters have since changed much of their methodology to adjust for that error, so the polls may prove more accurate this time. That said, if there was ever an election year that the polls would get wrong, it’s probably this one, and Trump has been doing a lot of rallies lately.

Fed meets ahead of NFP

In the aftermath of Tuesday’s election, traders will also have to digest a Fed policy meeting on Thursday and the latest US employment report on Friday. The overarching theme that will really drive markets is of course the electoral outcome, but these events could spark some volatility.

The Fed is unlikely to deliver any fireworks. Covid infections have spiked lately, which spells trouble for growth in the fourth quarter, but the situation is not dire either. The housing market is booming, the latest Markit PMIs point to continued recovery, and seekers of unemployment benefits have declined meaningfully.

Hence, the risks are clearly high, but the Fed can definitely afford to wait until December before taking any real decisions, at which point it will have a better sense of how much economic damage the latest wave of infections has inflicted on the economy and how much fiscal stimulus will be pumped by Congress.

On the data front, the main event will be the jobs numbers for October. Nonfarm payrolls are expected to have risen by 850k, pushing the unemployment rate down to 7.7% from 7.9% previously. Note though, that NFP reports tend to be only an intraday volatility event nowadays, not a trend-setter for markets. The initial market reaction is usually minor and fades within a few minutes. Beyond all this, the ISM manufacturing and non-manufacturing PMIs are also due on Monday and Wednesday respectively.

RBA: Cutting rates, but what about QE?

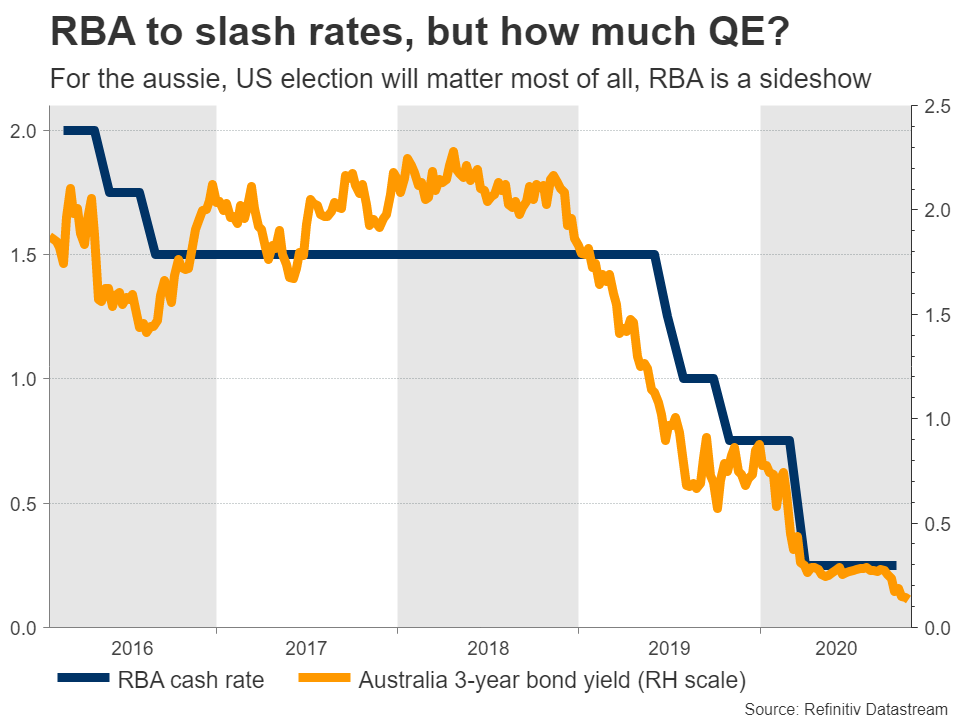

After a series of dovish communications lately, the Reserve Bank of Australia is expected to cut rates to 0.1% from 0.25% when it wraps up its meeting early on Tuesday, and also lower the yield target on 3-year Australian bonds by the same amount. The rate cut is almost fully priced in by now, so the reaction in the aussie may depend mostly on how the Bank calibrates its QE program.

Namely, will the RBA set a volume target about how big its QE program will be, say AUD 150bn, or will it simply signal that it will buy as many bonds as the situation demands to keep the yields on those bonds capped? Normally, the Bank would prefer to retain some flexibility and opt for the latter, but markets seem to expect a specific volume target.

Hence, if the RBA refrains from providing that volume target, markets could be left disappointed and the aussie may even spike higher. That said, FX markets typically front run these events much in advance, and the RBA has telegraphed its actions relatively well, so any impact is unlikely to be huge.

Instead, the most crucial variable for the aussie will be how the US election plays out. If Biden wins in a landslide, the aussie could get a double boost from both the risk-on atmosphere and expectations for calmer US-China relations. On the flipside, it may be the biggest underperformer in case of a Trump upset victory or a contested result.

In neighboring New Zealand, third-quarter employment stats are out on Tuesday and the all-important inflation expectations survey by the RBNZ is out Friday. But again, the kiwi will also pay more attention to US politics.

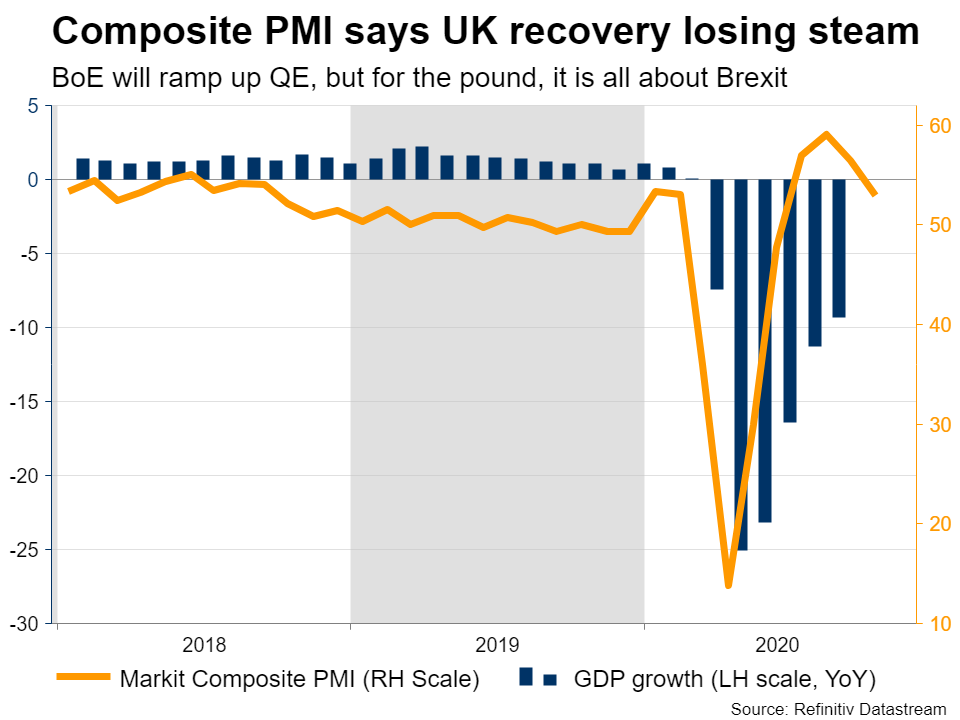

BoE: More QE, but it’s Brexit that matters

In the UK, the Bank of England is expected to ramp up its QE program on Thursday, increasing it by £100bn. As with the RBA, this move has been telegraphed well in advance and is probably priced in already, meaning that the reaction in sterling will depend mainly on whether the actual amount is smaller or bigger than expected. On balance, the BoE has more incentive to over-deliver, in which case the pound may spike a little lower.

In the bigger picture, it is all about Brexit. The latest is that the negotiations are making “good progress” according to EU chief von der Leyen. One final bout of drama cannot be ruled out, but at this stage, it seems increasingly likely that a deal will be hammered out over the coming weeks. Hence, any sterling selloff may remain short-lived, with an eventual deal likely to catapult the currency much higher in November.

Finally, Canada’s employment numbers for October are out Friday, alongside the US ones.

{kind=link}