We expect no major forecast changes in next week’s Bank of Canada rate decision and Monetary Policy Report. Indeed, the Canadian economic recovery is progressing largely in line with the central bank’s expectations, suggesting April GDP growth forecasts should be left mostly intact. We are tracking a 3.5% rise in Q2 GDP despite the spring virus wave—a projection in line with the BoC’s last published forecast. Vaccine distribution has accelerated as expected and early indicators are that household spending on hard hit travel and hospitality sectors showed signs of life in June as restrictions eased. With the economy performing largely as expected, we look for the BoC to lower the pace of asset purchases this month.

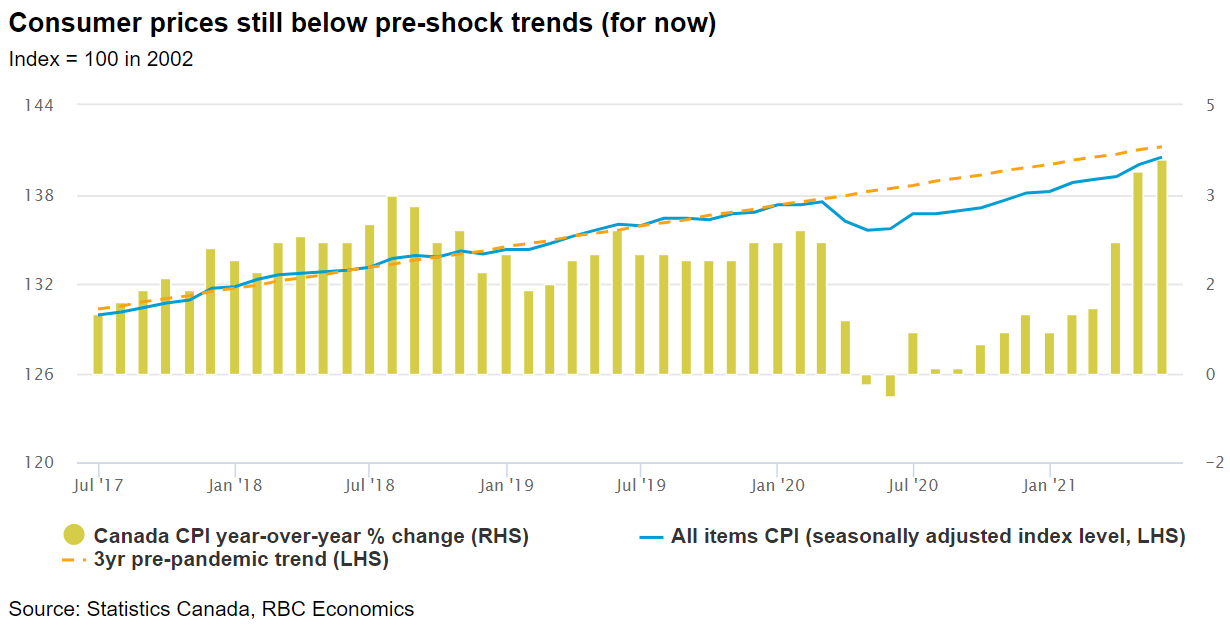

With a near-term bounce back in the economy looking increasingly assured, a more pressing concern is whether a consumer-led surge in demand over the second half of 2021 will stoke inflation pressures. Surging housing costs, and a retracing of price declines earlier in the pandemic (particularly for energy prices) already pushed headline CPI growth to 3.5% from year-ago levels in April and May. We expect the Q3 average to remain above the top-end of the central bank’s 1% to 3% target range. Although those readings have been higher than expected, BoC policymakers will likely continue to see the recent price surge as transitory. Up to this point, the increases have mainly pushed price levels back toward pre-pandemic trends. We expect no change to the policy rate or forward guidance timeline with the Bank expected to maintain exceptionally low policy rates until the second half of 2022.

Week ahead data watch:

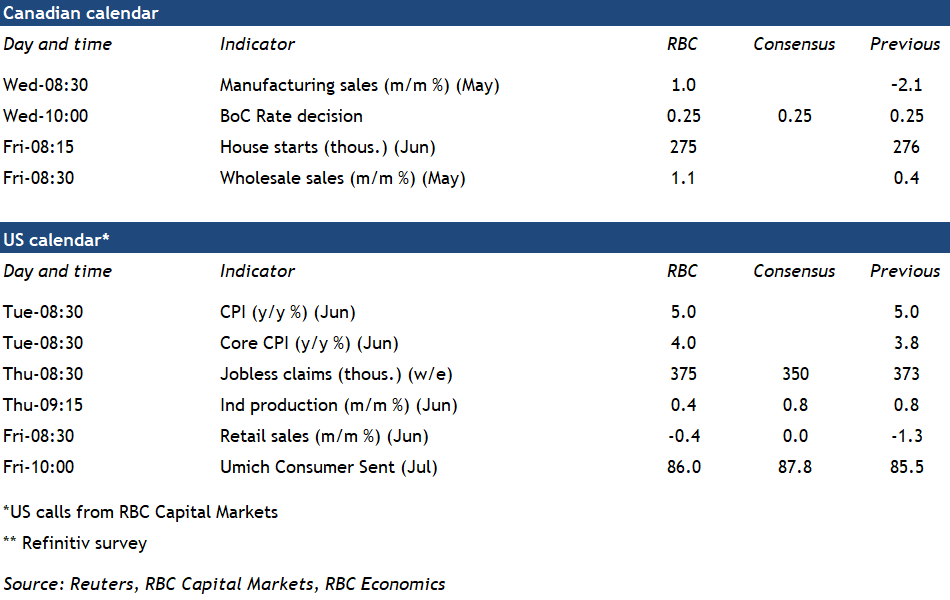

- Preliminary estimates for Canadian manufacturing and wholesale sales in May have already been released. Both indicators showed increases of ~1% despite the weak economic backdrop that was in place when many regions were under lockdowns.

- We expect Canadian June housing starts to have held at elevated levels—broadly in line with the strong permits issued in recent months.

- We expect US Inflation to jump 5.0% above year ago levels driven by pandemic base effects alongside firming price pressures. Central bankers will look past reopening bottlenecks for evidence of broad-based underlying price firming.

- US Retail Sales will likely show another decline in June as auto production disruptions limited new car sales.

- With over 50M vaccines in hand, Canada’s vaccination campaigain continues to thrive. Still, concerns about variants (delta) spread cannot be ignored. And the share of the eligible (12+) population receiving at least one dose has plateaued at still just short of 80%.

{kind=link}