Summary

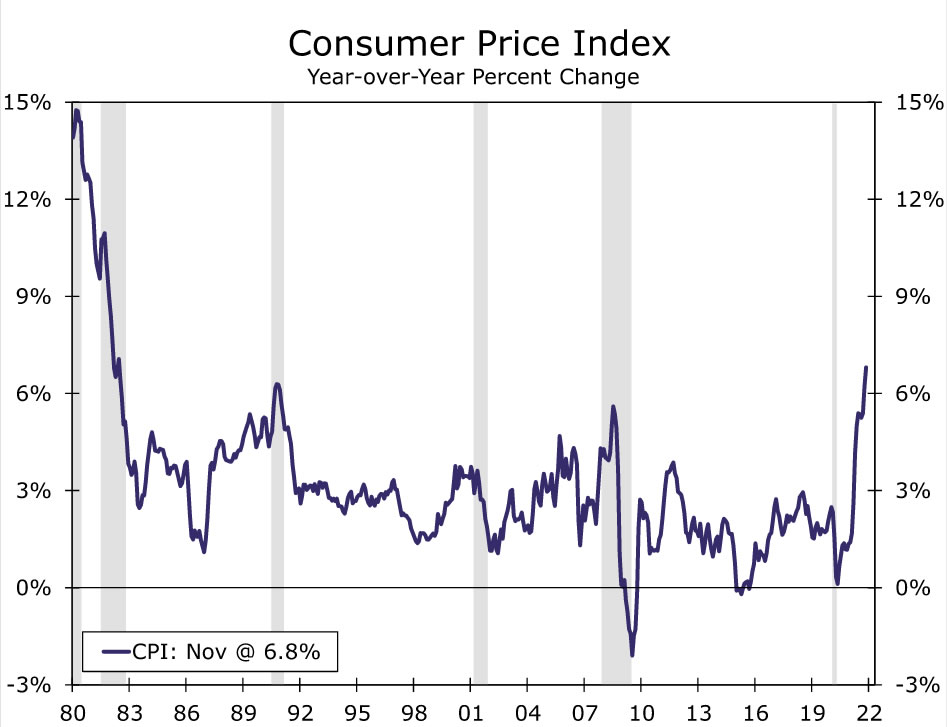

Another jump in prices in November propelled inflation up 6.8% from a year ago, the largest one year-increase since 1982. Pressures remain broad based, with supply chains still struggling to meet turbocharged demand for goods, and services inflation only recently beginning to reflect the pandemic’s effects on housing costs. We expect the monthly trend in price gains to moderate ahead, but there is a lot of daylight between the current pace of inflation and the Fed’s goal.

What Do November CPI, Eye of the Tiger, and E.T. Have in Common?

Inflation continues to feel extraterrestrial. The CPI rose 0.8% in November, pushing prices up 6.8% year-over-year. This 6.8% move is the biggest one-year change in the CPI since 1982. Once again strength was broad based. The goods side of the economy continues to adapt to the massive shift in spending on “things”, and services inflation pushed forward as travel-related prices rebounded and housing inflation climbed. While current strength continues to reflect the strains of the pandemic, that is likely to be little comfort to consumers seeing paychecks and savings stretch less.

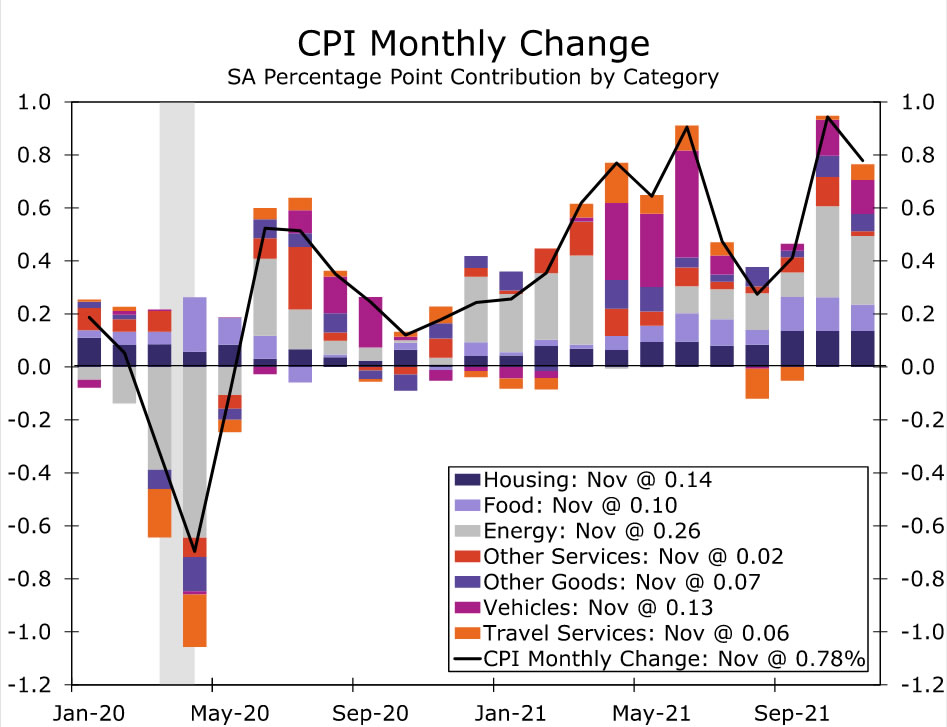

The dip in gasoline prices at the end of November was not enough to offset the earlier rise from October. Energy prices rose 3.5% and included another gain in energy services. We expect energy will offer some relief in the near term though, with gasoline prices and oil down 1.5% since the end of November, oil prices down about 15% from recent highs, and natural gas in storage more closely aligned with seasonal norms.

Beyond energy, however, we see little meaningful relief in sight. Price hikes remain widespread, meaning it will take more than a correction in one or two categories to return inflation to a more tepid pace. Food prices continue to sizzle, up another 0.7% in November. Food-related commodities are off from their recent highs, but continue to hover at a decade-high. And while November’s average hourly earnings numbers came in a touch light, wages were up another 0.8% in the leisure & hospitality sector.

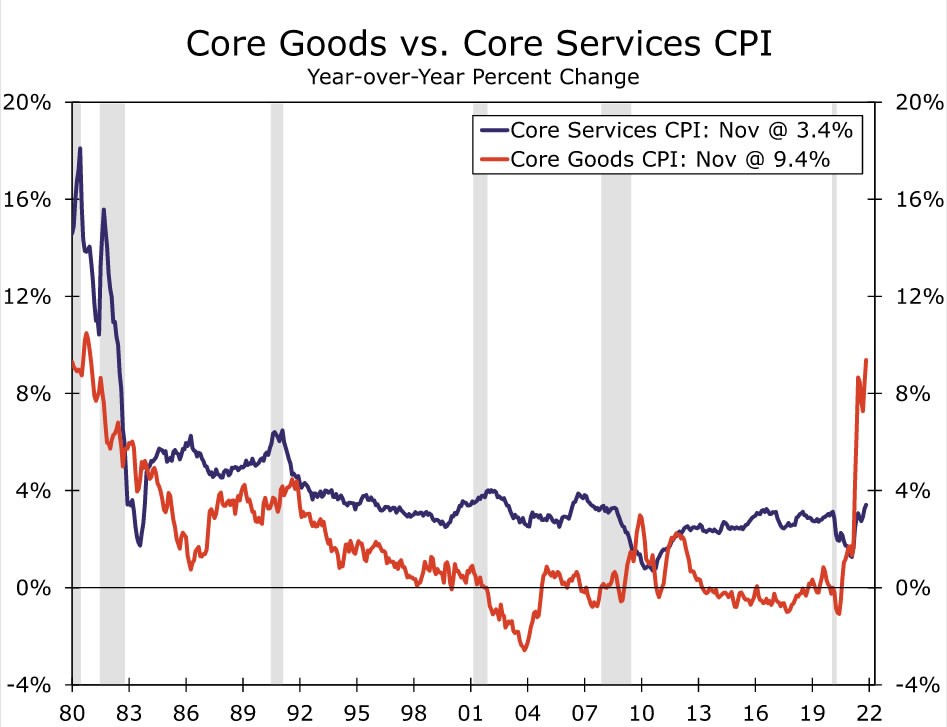

Excluding the volatile food and energy components, core CPI inflation slowed slightly from October but remained hot at 0.5% month-over-month. Core goods prices yet again led the way with a 0.9% month-over-month increase. As expected, motor vehicles once again pushed core goods prices higher. New vehicle prices rose 1.1% while used car and truck prices rose 2.5% for the second month in a row. Apparel prices also grew at a strong 1.3% pace in November, while prices for alcoholic beverages and medicine were roughly flat.

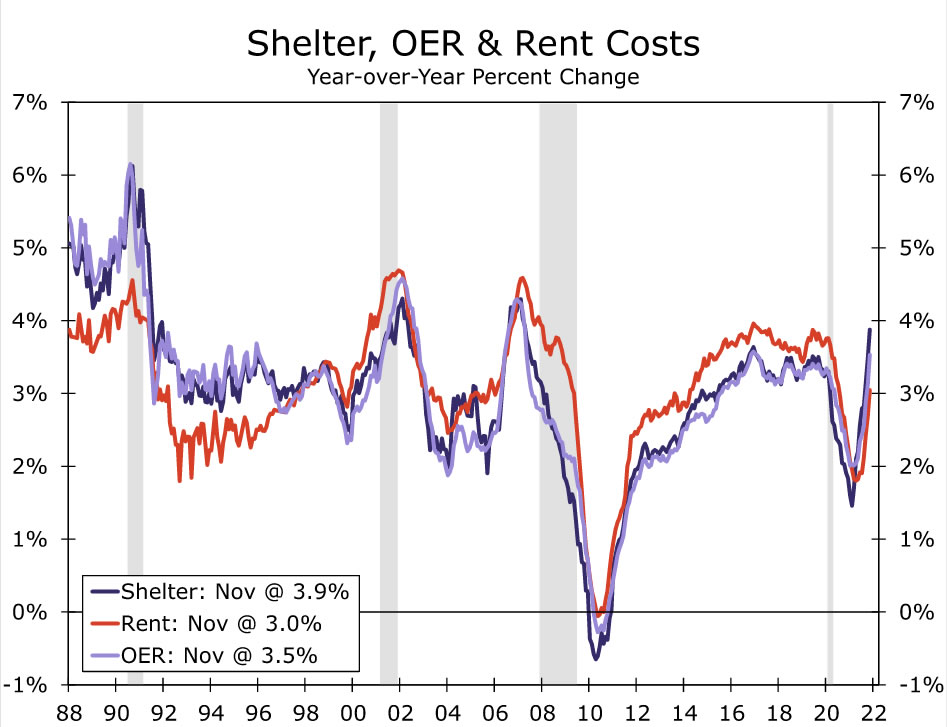

On the services side, shelter costs continued their steady climb higher. Shelter costs were led higher by another 0.4% increase in owners’ equivalent rent of residences and a 2.9% increase in prices for lodging away from home, such as hotels. Prices for car and truck rentals rose 1.1% in November and are up 37.2% year-over-year. Like lodging away from home, airfare price growth was also strong at 4.7% in the month. Higher service sector inflation is a phenomenon we have anticipated for quite some time now as the lagged effect from higher home prices and rents flow through to the CPI and as the pandemic-hit sectors of the economy normalize. However, goods price inflation remains stubbornly high and has yet to come back down to Earth, creating a double-barrelled inflation challenge for consumers and policymakers alike.

More Moderate Inflation Ahead, but the “All Clear” a Long Ways Off

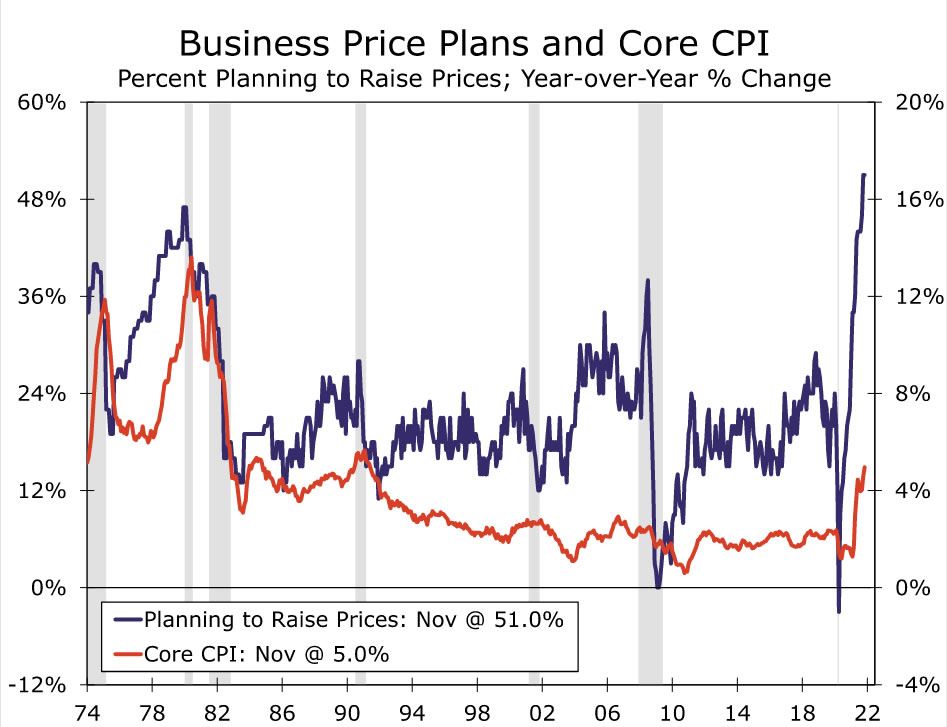

Inflation is set to remain a challenge for consumers and policymakers in the months ahead. The share of businesses planning to raise prices is the largest on record dating back to the mid-1970s. The breadth of price hikes raises the potential for current inflation to become self-reinforcing, particularly as employers’ desperation to hire is bidding up wages.

We expect headline CPI to peak on a year-ago basis at about 7% in the first quarter before base effects get tougher come spring. Monthly gains should continue to trend lower as the acute pressures from goods inflation begins to ease up and offsets the emerging momentum in services inflation. However, another big wave of COVID cases this winter could delay relief by keeping goods demand turbo-charged and global supply lines strained.

Even as the monthly trend in price hikes moderates ahead, there is a lot of daylight between November’s increase and the 0.2% monthly gains that would return inflation to a pace consistent with the Fed’s target. We estimate that headline and core CPI will still be above 3% year-over-year this time next year. We therefore look for the Fed to announce accelerating its wind-down of asset purchases at its meeting next week and to then raise the fed funds rate 50 bps in the second half of 2022. Slower inflation next year is not the same as benign inflation, and we think the Fed will need to respond accordingly.

{kind=link}