In 2021, optimism about the global economic recovery pressured gold to retreat from its 2020 highs but remain comfortably above its pre-pandemic levels. Next year, in an environment of higher interest rates, rising bond yields and a stronger US dollar, bullion’s prospects seem ominous. On the other hand, growth commodities like oil and industrial metals, whose fortunes are heavily dependent on global economic performance have appreciated in the current year. If the world continues to make progress in keeping the Covid-19 pandemic under control, strong demand will probably boost cyclical commodities further.

Fed policy might spell trouble for gold

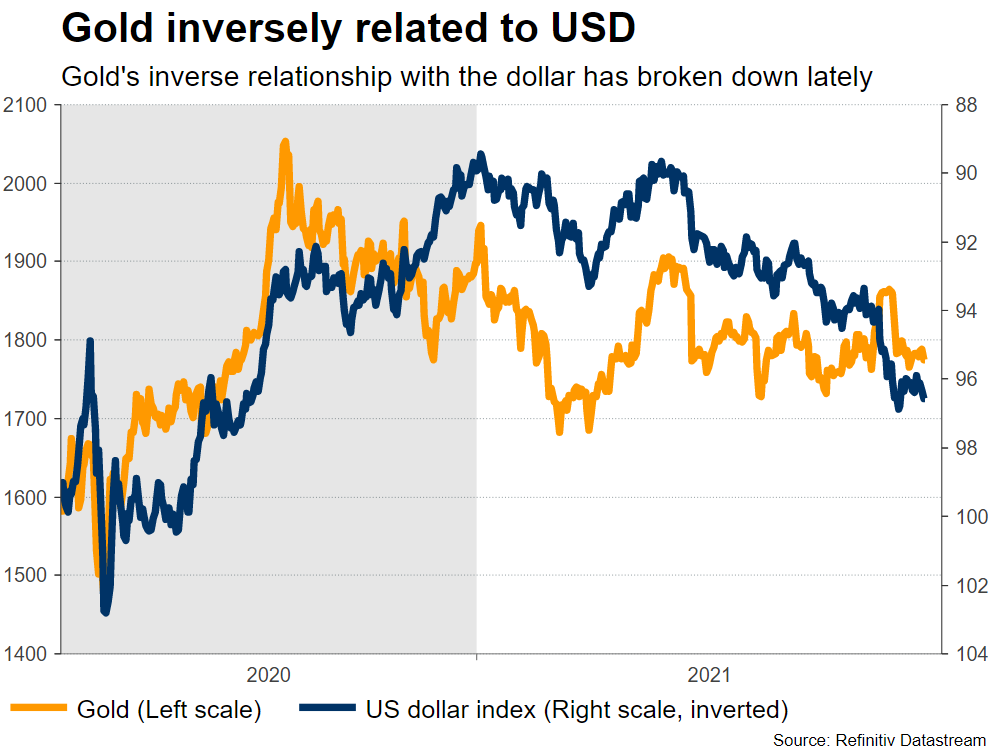

One of the most significant drivers for the price of gold in 2022 will be Fed policy, and primarily its impact on the US dollar. As the US jobs market has been recovering quite strongly in 2021 and surging inflation continues to haunt policymakers, the Fed has set the markets for a faster normalization of policy, accelerating its tapering program and flagging a more aggressive rate hike path.

Fed tightening would make the dollar more appealing relative to currencies bound to relatively looser monetary policies, such as the euro and yen. Since gold is mostly denominated in dollars, the roaring greenback could decrease the purchasing power of other currencies, further curtailing bullion demand.

Real yields remain a key driver

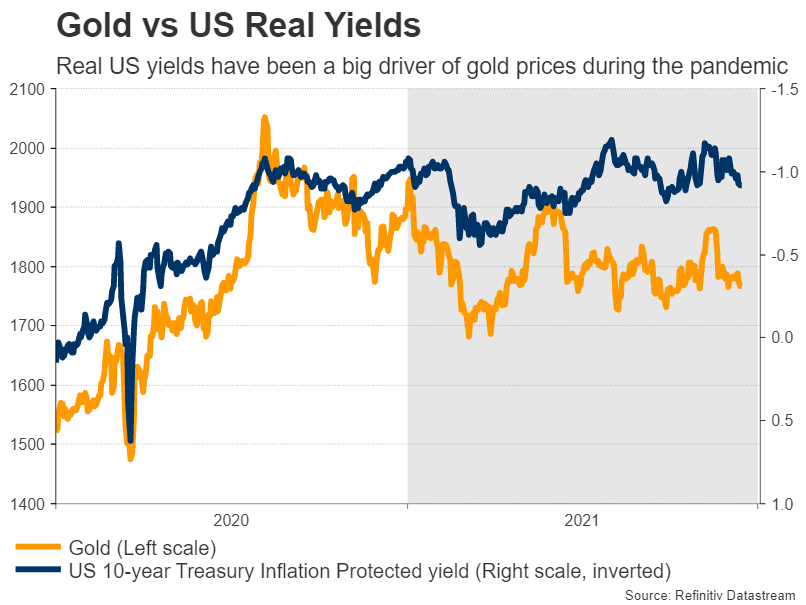

In 2021, government bonds failed to play the role of defensive assets as soaring inflation combined with low interest rates impeded their ability to generate income. However, gold did not manage to capitalize on its inflation hedging attributes in these conditions because investors shifted their focus to Treasury Inflation-Protected Securities (TIPS). In contrast to the yellow metal, TIPS not only provide protection against rising inflation but also pay a coupon that increases as inflation fires up.

In the upcoming year, inflationary pressures are expected to subside, while central banks are anticipated to raise interest rates that tend to push up sovereign bond yields. Should the Fed raise rates and inflation falls back as is being predicted, higher Treasury yields alongside lower inflation could push real yields back to the positive region. This would make government bonds more attractive than gold, which on top of generating zero interest also carries storage costs. Hence, positive or at least increasing real yields would probably cast a shadow over demand for gold.

Geopolitical risks and resurgence of Covid-19 might rescue gold

Geopolitical tensions can often spook global markets, triggering risk-off sentiment and boosting safe haven demand. Although gold has been somewhat unresponsive to geopolitical flare-ups lately, there are several lingering dangers that could explode into something bigger in 2022.

Military tensions are brewing in several hotspots. Russia is lining up troops on the Ukrainian border, with US officials fearing Moscow is preparing for an invasion. China, meanwhile, has been flexing its military muscles near Taiwan, while the US and Iran seem unable to find common ground in their negotiations over Tehran’s nuclear program.

On the virus front, the emergence of the Omicron variant has highlighted how the pandemic is far from over. If the existing vaccines prove ineffective against Omicron or other future variants, the global economic recovery might get derailed. Therefore, should governments impose new restrictions in 2022, risk aversion would soar again, increasing gold’s safe-haven appeal.

Gold levels to watch

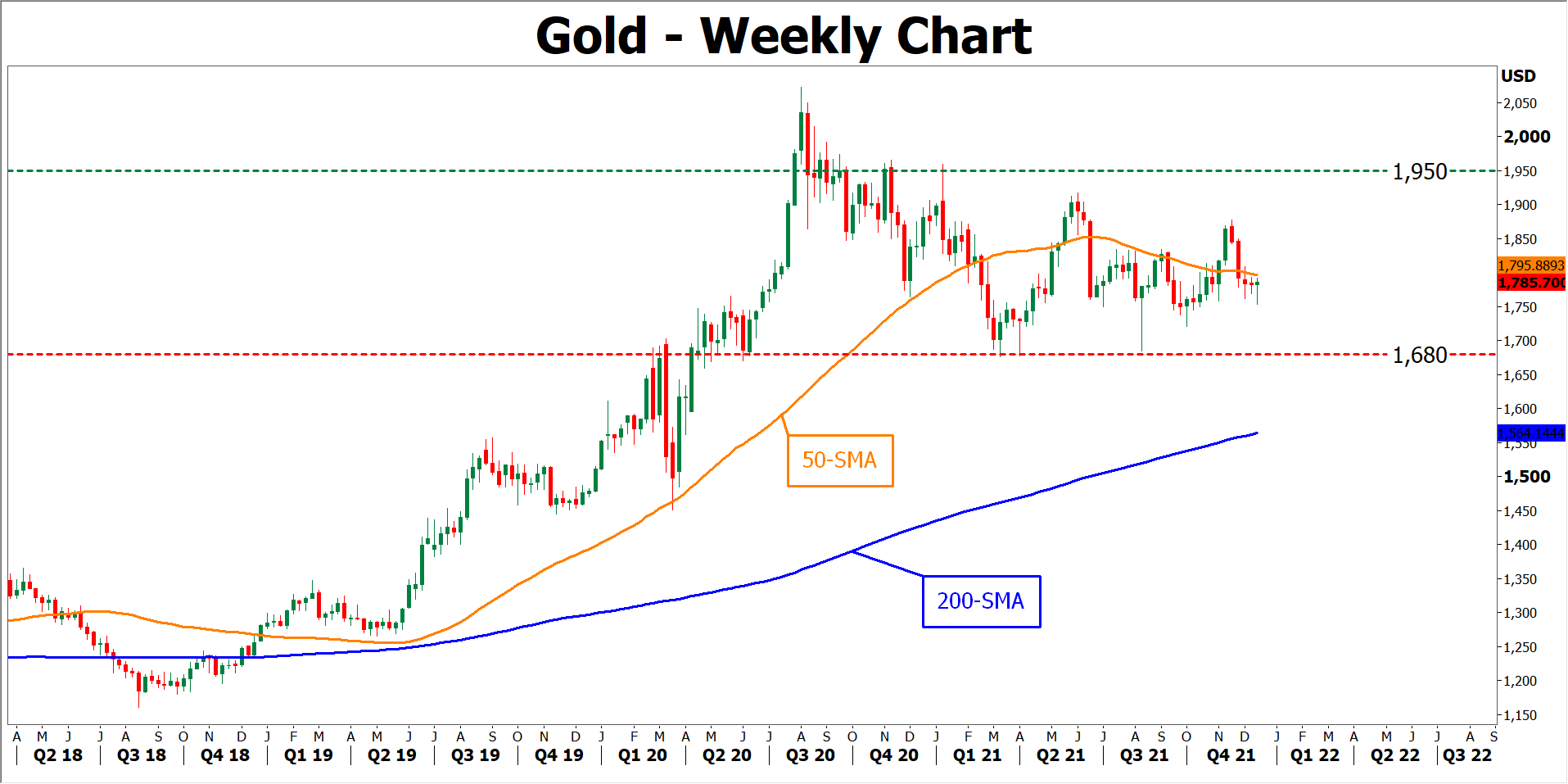

From a technical perspective, gold has been giving up ground in 2021, but the price appears to have adopted a more sideways pattern since June. In the positive scenario, an important upside target price for gold is $1,950. However, given the dollar’s persistent strength and the global trend in rising rates, the downside risks seem greater heading into 2022, putting the spotlight on the $1,680 region.

Oil to enter 2022 on a softer footing

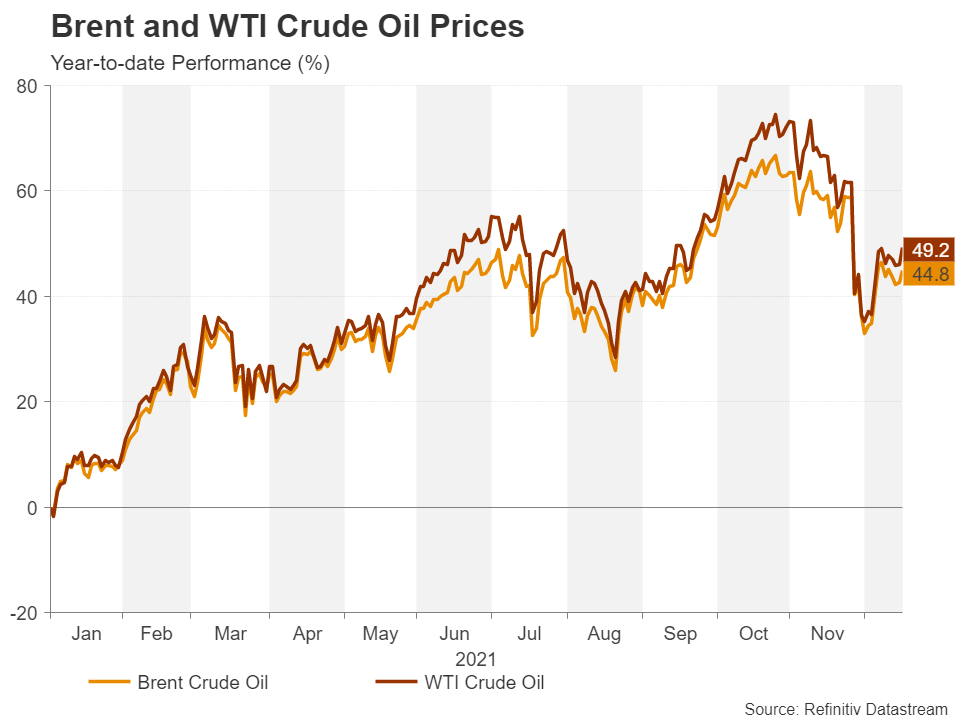

Oil prices rebounded from the pandemic induced lows of April 2020, starting 2021 on more ‘reasonable’ levels. Throughout the year, supply was unable to keep up with increasing demand due to the strong economic upturn that followed the economic shutdowns of the first coronavirus wave. This supply deficit, together with OPEC’s reluctance to increase output, caused oil prices to skyrocket, reaching a seven-year high in October.

In 2021, WTI crude oil surpassed $80 per barrel at a time when many Covid-19 restrictions were still in place. Heading into the new year, demand for oil is expected to rise further, reaching pre-pandemic levels in the first quarter. But the previously more bullish forecasts have been scaled back following the emergence of the Omicron variant, dimming hopes that 2022 can be another stellar year for ‘black gold’.

Oil prices staged a spectacular pullback in November after Omicron reignited fears of slowing economic growth. Some of the panic has since abated, but until there is more conclusive evidence that this new strain is not as severe as previous variants, the rally is likely to remain on pause.

In the interim, the diminishing prospect of an Iran nuclear deal is supporting the commodity. Talks between Western powers and Iran have not been progressing as well as hoped. Time will tell if the gap between the two sides will close in 2022, as the US piles pressure by tightening the enforcement of existing sanctions.

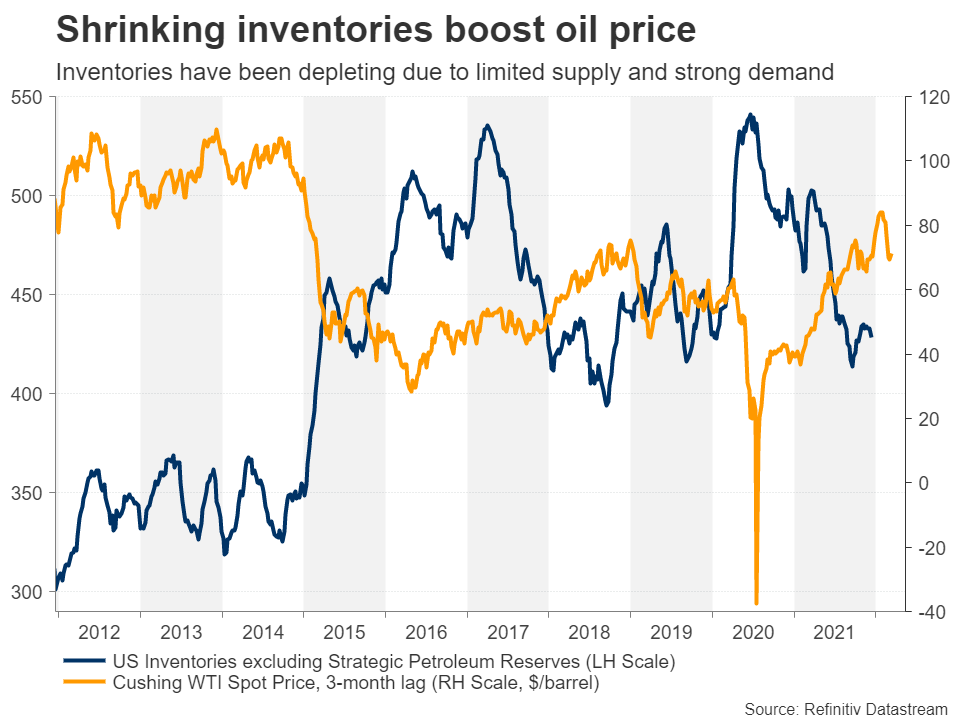

Depleting inventories to boost demand

Global oil inventories have fallen substantially in 2021, indicating an extremely under-supplied market, setting the stage for higher oil prices for the year to come. In Cushing, Oklahoma, the delivery point for WTI crude futures contracts, oil inventories are currently 50% lower than at the beginning of the year.

The depleting inventories are also mirrored by the higher price in near-term future contracts compared to longer dated ones, which also reflects market expectations that the shortages will subside within 2022. This difference in future contracts’ prices is known as backwardation, which was historically considered as a bullish sign for oil.

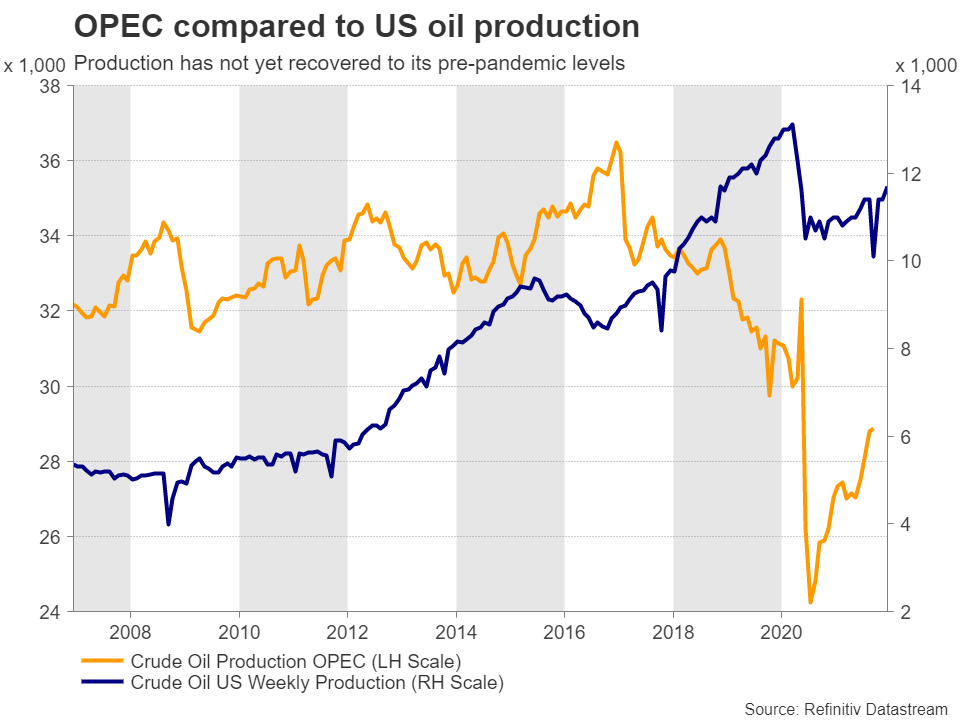

Despite the current deficit, forecasts expect a modest surplus for next year driven by increased production. At its December meeting, the OPEC alliance stuck to its agreement of increasing production by 400,000 barrels of oil per day for each month until September.

Non-OPEC supply in the spotlight

Next year’s surplus expectations are mainly driven by an anticipated increase in production from non-OPEC countries. But how realistic are these output forecasts when the oil industry is under attack due to the global shift towards green energy? The switch towards carbon neutrality by many governments has led to persistent underinvestment in new oil fields, especially in the US, amid fears about peak demand being reached soon, raising doubts about whether non-OPEC nations will be able to boost production sufficiently in 2022 even at current elevated prices.

Can industrial metal prices stage a new rally in 2022?

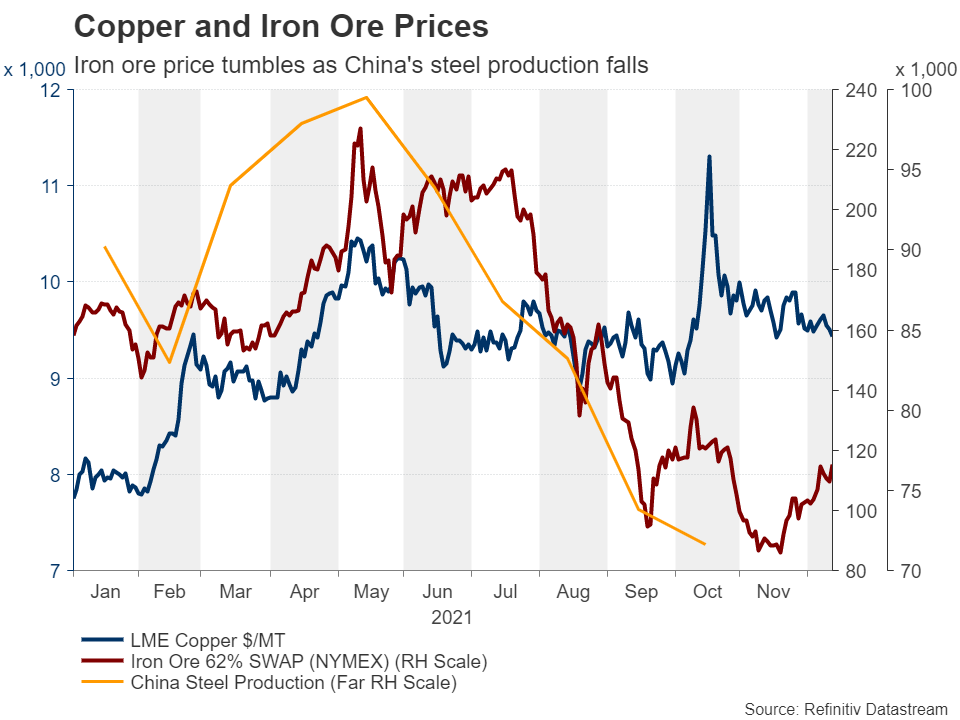

Industrial metals, led by copper and iron ore, entered 2021 firmly, as the prospects of strong economic growth and the global supply chain disruptions created an imbalance between supply and demand. This caused prices to soar, reaching historic highs during the first half of 2021. However, industrial metal prices headed south in August after the Chinese government cut down steel production amid energy crunches and a struggling property sector.

Copper is up about 20% so far this year, while iron ore is down by over 30%. The supply of the latter is expected to outpace demand in 2022 as the world’s largest iron ore miner, Vale, is anticipated to restore supply after the dam collapse in 2019 dented production. This together with weaker demand from China, could set the stage for lower iron ore prices in 2022. In contrast, copper’s outlook remains optimistic for next year amid expectations that demand will remain robust due to its usage in key components such as semiconductors and in renewable energy.

Clouded outlook

The worsening slowdown of the Chinese economy is potentially the biggest risk for industrial metals as well as for broader commodity prices in 2022. Moreover, souring diplomatic and trade relations between China and Australia, as well as persisting tensions with the United States, could generate further volatility in gold, metal and energy prices over the coming year, not to mention the threat of new virus mutations that can evade vaccines.

{kind=link}