U.S. Highlights

- A strong week for economic data as the ISM manufacturing index and the payrolls report surprised to the upside.

- The details of both reports showed improvements on the supply-side of the economy as falling manufacturer input

- prices and a strong improvement in the labor force shined through.

- The Fed still has its hands full taming inflation, but supply-side improvements could make the job much easier.

Canadian Highlights

- GDP missed expectations but is still running above trend as households continue to consume.

- Household savings came down in the second quarter but is still elevated compared to pre-pandemic levels.

- Based on the recent national accounts data, the Canadian economy is still in a period of excess demand and further rate hikes will be needed next week from the Bank of Canada.

U.S. – Good News on Aggregate Supply

Markets continued to sell off this week as better than expected data dimmed the hopes of a 50-basis point hike by the Fed at its upcoming September meeting. However, there were some reassuring signals in the ISM manufacturing report and the household employment survey that the supply-side of the economy continues to improve and may help moderate inflation. The Fed will continue its hiking cycle, but the supply-side improvements might just make the job of taming inflation a bit easier.

Tuesday’s solid job openings data from the JOLTS survey grabbed headlines. Private openings in July were north of 10 million. Though sky high job openings have become the norm, they are remarkable relative to history and represent the scale of the problem the Fed is looking to solve. To tame inflation, officials are hoping to lower the rate of job openings, without meaningfully raising the unemployment rate. There is little historical precedent for this, but there is also little modern historical precedent for what has transpired in the economy over the past two years. Nonetheless, with job openings still high, the labor market is signaling that employment demand remained robust in July despite rising interest rates.

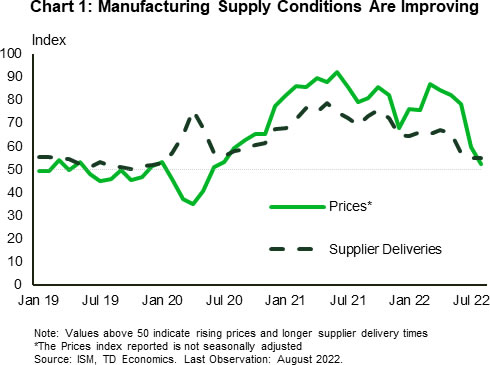

The good economic news continued yesterday as the ISM manufacturing index surprised to the upside in August, registering a healthy 52.8 print. Growth and production were notably slower than earlier in the recovery, but this was to be expected as the economy continues to operate in excess demand territory. The details in the report were also strong. New orders flipped back to growth and employment was up for the month. For the Fed, there was good news on supply chains as the supplier delivery index was unchanged and input price growth eased to its lowest rate since the summer of 2020 [Chart 1].

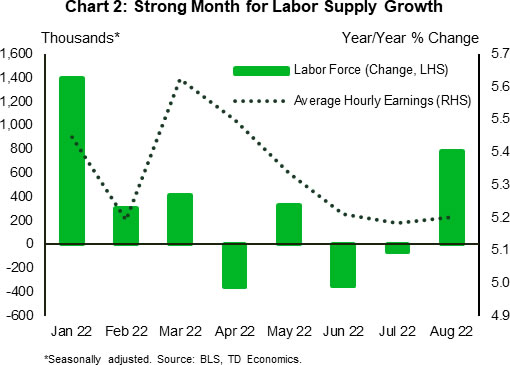

All of this was a buildup to today’s employment report. Consensus expectations were for nearly 300k new jobs, a print that would register as “good” during any expansion, let alone one that has featured so little bounce-back in the participation rate. Well, the data came in slightly better than expected, with payrolls adding 312k jobs, but it was the household report that had some positive elements. August showed that there was finally a large movement of people back into the labor force, 786k to be exact [Chart 2]. This helped lift the participation rate 0.3 percentage points, to 62.4% and brought some much-needed supply to the labor market. As the labor force expanded faster than employment, the unemployment rate rose to 3.7%. With just a bit more labor supply, average weekly wages moderated to 0.3% month-on-month, from 0.5% the month prior.

The Fed will see this report as good news. The drum-tight labor market is a key factor in setting wage expectations, and with more workers coming in off the sidelines, it means just a bit less wage pressure. That said, labor markets remain tight as wage growth is still at 5.2% year-on-year, and inflation is still persistently high. The Fed will continue to raise rates to fight inflation, but this week’s data suggest that some of the supply-side factors behind current price growth are finally starting to abate.

Canada – Full Steam Ahead to Hike Rates

All eyes were on GDP numbers this week ahead of the Bank of Canada’s interest rate announcement on September 7th. Canada’s second quarter GDP numbers came in at 3.3% quarter-on-quarter annualized growth (q/q), and although this was lower than expected, it is still running above trend and outperforming our global counterparts. Though there are signs of slowing ahead, this GDP report justifies the sentiment in the Bank of Canada’s most recent Monetary Policy Report that the economy is in excess demand and will require further interest rate hikes. Reflecting this expectation, bond yields rose with the Canada 2-year yield reaching a high of 3.7%, the highest level in 14 years.

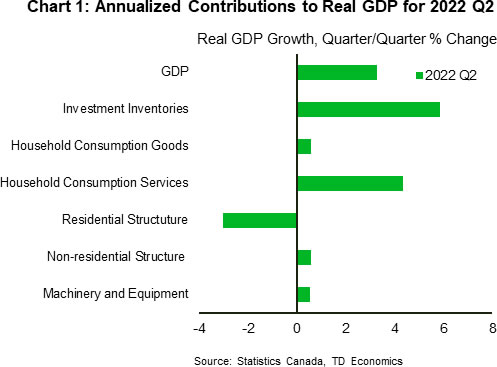

Second quarter Canadian growth was led by strong household consumption, non-residential investment, and inventories (Chart 1). Canadian consumers increased spending by 9.7% q/q, with consumption in services as the key driver (16.4% q/q). This reflected strength in the reopening of the economy post covid lockdowns and the pivot away from goods towards services. Also bolstering growth was non-residential investment in structures (11.1% q/q), as well as machinery and equipment (19.3% q/q). This was powered by the expansion of oil and gas sector companies in western provinces which are capitalizing on higher energy prices. On the flip side, growth in residential structures pulled back significantly (-27.6% q/q), reflecting the impact of the Bank of Canada’s aggressive rate hiking cycle. Indeed, in our latest Canadian Housing Outlook report we note that national Canadian home prices in the second quarter have declined by 9% q/q and have room to fall further. This is likely to weigh on residential investment, which will exert downward pressure on GDP growth going forward.

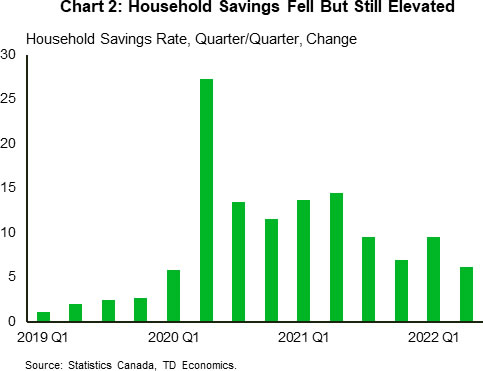

Though real GDP was lower than what most forecasters were expecting, growth in nominal GDP rose to 18% q/q, up from 16% q/q in the first quarter. This drove nominal household disposable income in the second quarter (3.9%), with wages and salaries rising 7.8%. With this income gain, combined with still elevated household consumption, the savings rate came down to 6.2% from 9.5% (Chart 2). With inflation likely to stay high and interest rates set to increase further, we expect that consumers are re-evaluating their spending patterns, which could cause a further fall in the savings rate next quarter.

With this GDP report in its back pocket, we expect the Bank of Canada to continue to raise rates next week, with 50 basis points being the floor, as markets are already pricing in a 75-basis points hike. It is clear that the economy is still operating well beyond excess capacity and is in need of higher interest rates in order to cool current inflationary pressures.

{kind=link}