U.S. Highlights

- The last jobs report before the Federal Reserve’s November meeting showed that 263k jobs were added in September, bringing the unemployment rate back down to 3.5%.

- ISM Manufacturing and Services PMIs indicate that demand for goods is slowing swiftly, while demand for services is slowing more gradually and has yet to yield substantial ground.

- Oil supply reductions signaled by OPEC+ this week will raise energy prices, creating another headache for the Federal Reserve.

Canadian Highlights

- The OPEC+ decision to scale back output jolted oil prices and supported the energy intensive TSX equity index. We still see limited upside for oil moving forward, amid a weakening global economy.

- In a speech this week, BoC Governor Macklem delivered a hawkish message. He noted that more work needs to be done to cool inflation, and that it’s still too soon to take a decision-by-decision approach to policy.

- This morning’s Labour Force Survey flashed some signs of cooling conditions (hours worked declined), but still reinforced that job markets are tight and wage growth is robust.

U.S. – More Jobs, Less Oil, No Pivot

The first week of the third quarter was largely centered around labor market conditions and their potential impact on the policy stance of the Federal Reserve at their November meeting in four weeks’ time. Lower job openings, higher jobless claims, and slowing job growth all provided some evidence of a softening labor market, but a lower unemployment rate and solid wage growth clouded the aggregate outlook. Equity markets rallied to start the week with hopes of a ‘Fed pivot’ before retreating on Friday as the jobs report drove yields higher and dampened the prospect of a less aggressive Fed. As of the time of writing, the S&P 500 is still up 2.5% for the week, while the ten-year treasury yield sits at 3.9% – 10bps higher than it was to start the day.

Non-farm payrolls capped the week, coming in slightly above market expectations with 263k jobs added in September. The unemployment rate ticked down by 0.2 percentage points, back to its July low of 3.5% as the labor force was virtually unchanged from its August level. Combined with steady growth in average hourly earnings of 0.3% month-over-month (m/m), it is clear that the labor market remains strong – a sentiment that is not lost on financial markets which are now pricing in a fourth 75bps hike by the Fed in November with 80% probability.

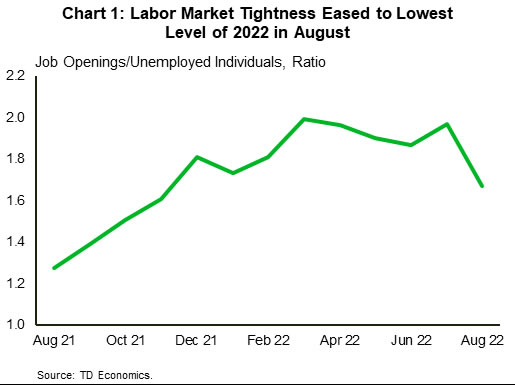

Earlier in the week, we saw job openings for August decline by 10% to reach their lowest level since June 2021. This brought the ratio of job openings to unemployed individuals down to 1.67 – its lowest level since November 2021 (Chart 1). This will be welcomed by Jerome Powell who noted that this ratio was exceptionally high in his September press conference. Jobless claims also displayed signs of softening with a 15.3% increase last week, although this only brings the level of claims back to where it was a month ago. On aggregate, the labor market will need to soften further in order for inflation to sustainably return to the Fed’s target range.

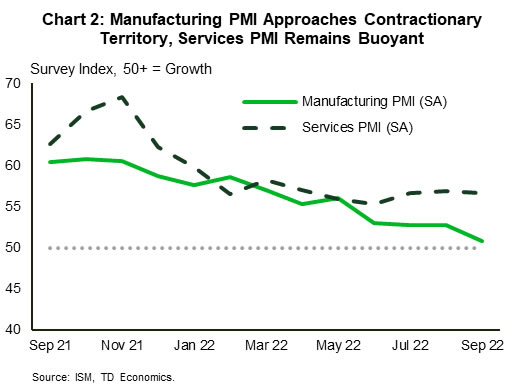

One sector which is showing clear signs of slowing is manufacturing, with the ISM Manufacturing PMI quickly approaching contractionary territory (Chart 2). The index dropped by 1.9 percentage points to 50.9 in September, reaching its lowest level since May 2020. Slowing demand was a leading contributor to the lower reading, with both new orders and new export orders contracting. Some of this demand has shifted into the service sectors, with the ISM Services PMI remaining well in expansionary territory, though it too is showing some signs of slowing. While the reading for September was slightly above expectations at 56.7, a slowdown in the backlog of orders as well as new orders could be indicative of the early signs of peak demand for services.

International events this week will serve to further complicate the Fed’s already difficult position, with OPEC+ signaling that it will curtail oil production by 2 million barrels-per-day (bpd). National gas prices, which have been rising for the past few weeks, will likely rise further and return to making positive contributions to headline inflation. Next week’s CPI data for September will provide a better picture of recent developments on the prices front, but as it stands now the Fed will likely remain resolute in its current hawkish stance.

Canada – More Work to be Done

Following another difficult month September, it was a turbulent week for Canadian equity markets. Bourses bounced higher to begin the week, with the TSX up 5% through Tuesday. Ironically, some weak economic data, and the recent rout in financial markets were big drivers for this brief turnaround. Investors figured that these signals would be enough for central banks around the globe to at least consider some adjustments to their aggressive tightening campaigns. However, this hope faded later in the week, as this morning’s employment report indicated that Canadian job markets remained tight, reinforcing hawkish messaging from BoC Governor Macklem earlier in the week.

The energy heavy TSX index was given another jolt by the steep climb in oil prices. WTI shot 15% higher this week (as of writing), buoyed by the OPEC+ decision to scale back global oil output by 2 million barrels per day in order to shore up prices after several weeks of declines. However, the actual reduction in output should work out to something closer to 900k barrels. Ultimately, even with this week’s rally, we see limited upside potential for WTI heading into 2023 as the global economic backdrop continues to soften.

Our assumption that oil prices will trend lower next year is a key factor underpinning our forecast for slowing inflation. This view is also cultivated by the additional 75 bps of tightening we think is in the cards for the Bank of Canada. In a speech this week, Governor Macklem reinforced that more tightening is on the way.

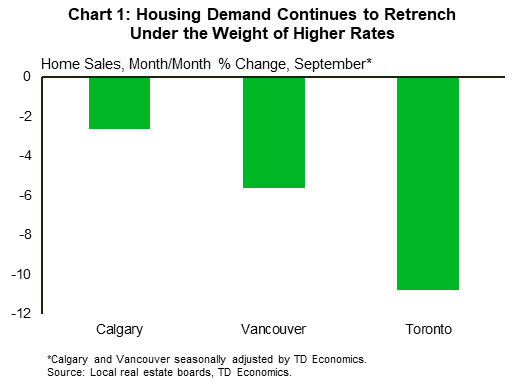

Additional rate hikes will erode housing affordability that’s already stretched-thin, further weighing on demand. In this vein, we’ve recently downgraded our forecasts for Canadian home sales and average home prices, and September data from local boards released this week reinforced our view. Most notably, home sales tumbled 11% m/m in Toronto, while prices were down nearly 3% m/m last month (Chart 1).

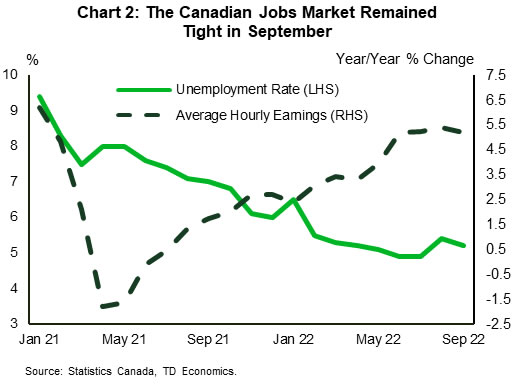

In his speech, Governor Macklem also remarked that it’s still too soon to take a “decision-by-decision” approach to policy. This latter remark could signal that the Bank is considering a higher endpoint for the policy rate than the 4% level we expect. However, this will depend on how the broader growth outlook evolves. This morning’s jobs report confirmed that the economy is cooling, but that labour markets remain tight and wage growth is robust (Chart 2). The Canadian economy added 21k jobs last month, bang on consensus. However, this was due to a rebound in the educational sector, which may have been “artificially” depressed by difficulties in seasonally adjusting the data in the month prior. Removing this sector yields a clearer picture – Canadian employment is softening, while hours worked also tumbled in September. However, the unemployment rate remains near a multi-decade low and wage growth is running at 5%. The latter is simply too high for a central bank hell-bent on returning inflation to its 2% target.

{kind=link}