Staying the course

- The RBNZ left the OCR at 5.5% as expected.

- The record of the meeting states that the risks to the outlook were viewed as “little changed” since the February Statement.

- The minutes noted the potential for a more flexible approach once inflation returns to the target range and when inflation expectations and pricing intentions are no longer elevated.

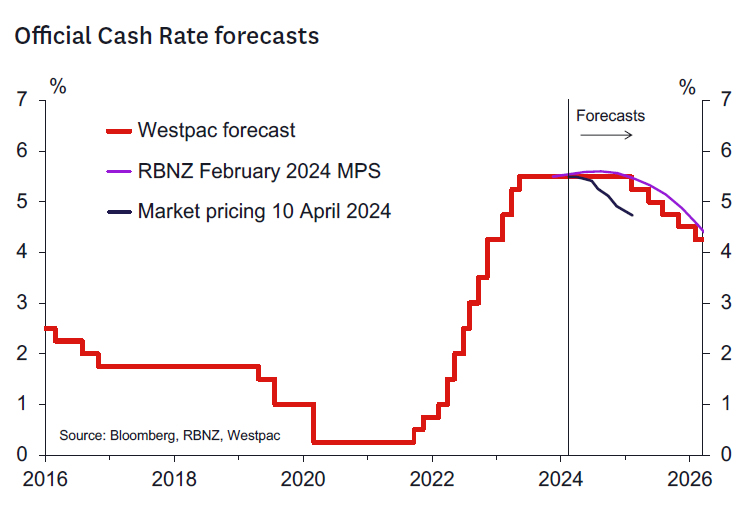

- The RBNZ’s monetary policy strategy looks unchanged, implying the OCR will remain at 5.5% until 2025 – in line with Westpac’s forecasts. The RBNZ is staying the course.

- We continue to forecast the OCR to remain at 5.5% in 2024 and be reduced from February 2025.

As we discussed in our Monetary Policy Review preview note, the data flow since the February Statement has not suggested a significant change in the outlook for inflation and the OCR. In general, data suggests:

- A modestly weaker demand picture than expected as the Q4 GDP data were a touch weaker than forecast while confidence indicators show the shine is coming off a bit such that a pickup in growth in H2 might be less certain.

- But the inflation picture looks less favourable than the RBNZ hoped. The near-term CPI outlook seems stronger than the RBNZ expected, as confirmed by the recent monthly price index data. In addition, the exchange rate is weaker, energy prices are a lot stronger, and pricing indicators in sentiment surveys point to lingering cost pressures.

The RBNZ picked up on many of these themes in their relatively short press statement (140 vs 309 words in February) and record of meeting. Key points were:

- Risks to the outlook for inflation were assessed as similar to the February Statement. Upside risks from services prices, local authority rates insurance and utility costs were noted as were downside risks coming from the long period of restrictive policy in a weak global growth environment.

- The global backdrop was assessed as similar to February. Labour markets remain tight but the potential lower policy rates offshore remains.

- The RBNZ still sees a need for the OCR to remain restrictive “for a sustained period”.

- The RBNZ’s focus remains on returning inflation to the mid-point of the 1-3% target range. However, the minutes noted the potential for more flexibility on this once inflation is back inside the target range and when inflation expectations and pricing intentions are no longer elevated.

We continue to see the OCR as remaining on hold through 2024 with a gradual reduction in the OCR coming from the February Statement. Key data to watch between now and the May Statement include:

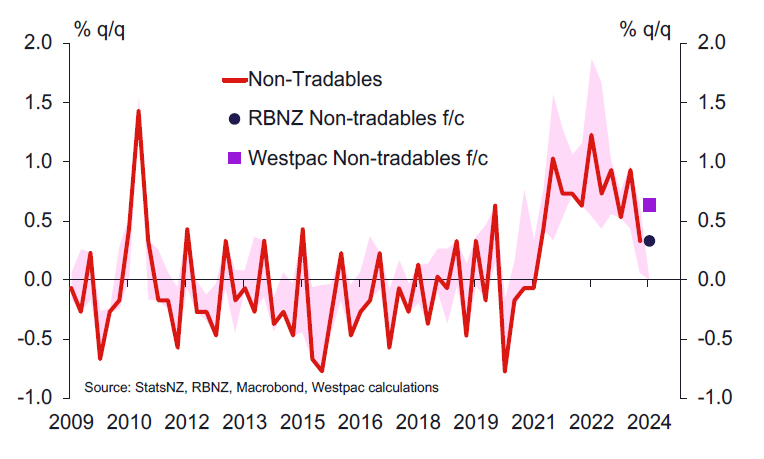

- The March quarter CPI (17 April) where the level of core inflation will be especially key (Headline CPI forecasts: RBNZ February 0.4% q/q, WBC 0.8% q/q, Nontradables CPI forecasts: RBNZ February 1.1% q/q, WBC 1.4% q/q).

- The March quarter labour market reports (1 May) where long awaited signs of labour market adjustment will be sought (Unemployment rate forecasts: RBNZ February 4.2%, WBC 4.3%, Private Sector LCI wages forecasts: RBNZ February 0.8% q/q, WBC 0.8% q/q). Global financial market developments will also be of relevance – especially the exchange rate and oil price developments as these will be crucial for determining the near-term CPI profile.

- As we anticipated, this unchanged outlook probably comes as a disappointment to those market participants looking for signs of an imminent RBNZ dovish pivot. However, there has been only a modest reaction to the statement in interest rate markets, which continue to price about 59bps of policy easing by the end of this year. The revised language around the potential flexibility the RBNZ might have around the timing of the return of inflation to the 2% mid-point is interesting and pragmatic. While inflation is likely to be within the target range by the end of the year, pricing intentions and inflation expectations indicators remain elevated and are only slowly falling. Watching that data as we progress through the year seems appropriate.

{kind=link}