Markets

Triggered by Fed chair Powell ruling out a hike, then reinforced by sub-consensus payrolls & ISM’s and by an in-line easing of CPI earlier this week, the US Treasury rally grinded to a halt yesterday. That happened despite a slew of (secondary) US data disappointing to the downside (jobless claims, housing data, IP and others). Given how a similar setting a day earlier triggered further UST gains, it suggests the correction lower may have run its course for now. Front end US yields took the lead. Markets on Wednesday fully priced in a rate cut in September and are unwilling to move this even closer in time. Focus is instead gradually shifting to what to expect in 2025 (currently three cuts priced in, following two this year) as the dominant driver of the front. The US 2-yr yield tested support between the May (post-payrolls) low of 4.70% and the 38.2% retracement on the 2024 upleg (4.689%) before rebounding throughout the session towards 4.8%. Longer maturities added between 1.2 and 3.5 bps with the 10-yr seeking to hold above 4.35-4.37% support. German Bunds outperformed. Yields rose 3.2-4.3 bps across the curve. Together with some fatigue hitting the stock markets (after hitting new intraday record highs in the US), the dollar bottomed as well. EUR/USD returned from 1.0884 to 1.0867.DXY recovered from the 104.08 low point to 104.46 in the close. Fed speak included Barkin, Mester and Bostic striking a cautious tone on inflation despite the “welcome tick down” (Mester) in the monthly CPI figures. They argue for patience with services and shelter still being inflationary. Bostic did add that it could be appropriate to reduce rates toward year end.

Apart from China’s monthly economic update (see below), there’s little to inspire markets today. The country also did its inaugural special bond sale to kickstart the economy/property market. We look out in core/US markets whether the aforementioned key technical levels in yields will hold into the weekly close. If they do, the dollar could show additional signs of bottoming out, especially if stock markets take some chips of the table ahead of the weekend. EUR/USD’s first meaningful support is located around the 1.08 big figure (1.0793, 50% USD recovery on the 2023Q4 decline).

News & Views

Chinese data published this morning showed a mixed, rather unconvincing picture on the country’s economic recovery. On the positive side, April industrial production accelerated to 6.7% Y/Y from 4.5%, better than the 5.5% expected (YtD growth 6.3%). The rise, amongst others, was driven by chip production and autos which suggests some positive impetus from foreign demand. However, more worrisome for the domestic growth story was another dismal performance of retail sales. Housing/property related data also showed ongoing weakness. Retail sales growth slowed more than expected from 3.1% Y/Y to 2.3% (vs 3.7% expected). Fixed asset investment growth (YTD Y/Y) also slowed from 4.5% Y/Y to 4.2% while a small further gain was expected. Property investment remains under pressure (-9.8% YTD) with residential property sales even slumping 31.1% YTD (from 30.7%). The data today confirm the picture of an very uneven recovery of the Chinese economy with especially the need to address factors that are weighing on domestic confidence/demand. In this respect China this morning successfully sold a first tranche of the special sovereign bonds program (CNY 40 bln) with a bid-cover ratio of 3.91. The funds of the program will be used to support infrastructure spending.

As the BOJ policy is entering a new phase, recently a debate is developing on how the BOJ should handle the big asset portfolio, including its holdings of exchange traded funds (ETF’s). The BOJ holds a portfolio of about 37 trillion yen of ETF’s which has an important latent profit. Unwinding portfolio in a broader policy normalization move, could realize a revenue that might be used to support spending when it would be returned to the government. However, on this topic, governor Ueda today indicated that the BOJ is in no rush to sell risky assets anytime soon. BOJ caution on selling assets amongst others is inspired by considerations that it might unsettle markets that are affected by the sales.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut which has broad backing. EMU disinflation continued in April and brought headline CPI closer to the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell left the door open for rate cuts later this year. Soft US ISM’s and weaker than expected payrolls supported markets’ hope on a first cut post summer, triggering a correction off YTD peak levels. Sticky inflation suggests any rate cut will be a tough balancing act. 4.37% (38% retracement Dec/April) already might prove strong support for the US 10-y yield.

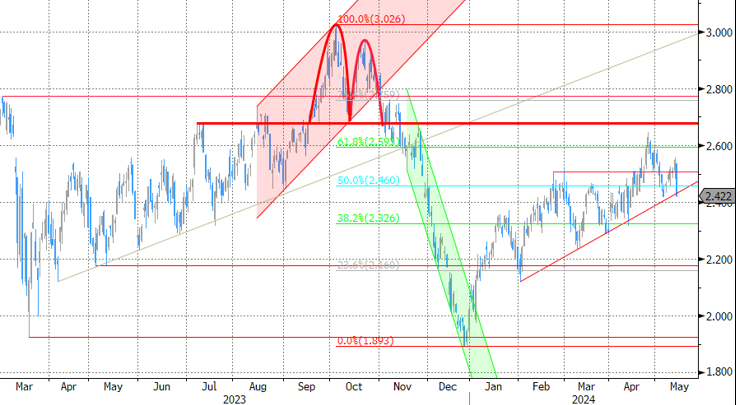

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 – 0.8768 trading range serving as the first real technical reference.

. The rise, amongst others, was driven by chip production and autos which suggests some positive impetus from foreign demand.){kind=link}