Week in review: Strictly risk-on Markets, Non-Farm Payrolls beat & US Deals

This week was heavily focused around the US with Indices hitting almost daily all-time highs in a stringent euphoric mood, with markets turning from War fears back to “TACO” trades, bullish on global economic outlook.

One thing to note is that asset managers are increasingly more bullish on stocks and market mood maybe a bit too euphoric, which may pull positioning too far on one side and lead to higher volatility in case of bad news – with some catalysts coming with the July 9th Trump deadline.

In terms of data, markets saw ECB inflation rates consolidating around 2% with some policymakers, the latest with Banque de France’s Villeroy commenting on the potential deflationary impact of a stronger Euro.

More directly market moving however was the streak of positive data releases for the United States, particularly as it comes to employment with NFP at +37K vs expectations and a beat on JOLTS.

One thing to be wary about in the solidity of that data point is the major rise in Government Jobs, providing a boost to the data without generating direct contribution to GDP.

Only ADP Private Employment missed, and and the miss was not a small one: -33K vs 97K expected.

This point of data tends to be less market moving than NFP, however Jerome Powell had previously mentioned private employment as a reason for the last year’s one-off 50 Bps cut from the FED.

The Week ahead: RBA and RBNZ rate decisions, July 9th Trump deadline, FOMC Minutes and BRICS Meeting

The week ahead will shift the market’s focus back to central banks and geopolitics, as participants brace for a series of global catalysts that could reintroduce uncertainty after several weeks of sustained positive sentiment.

Asia-Pacific Markets

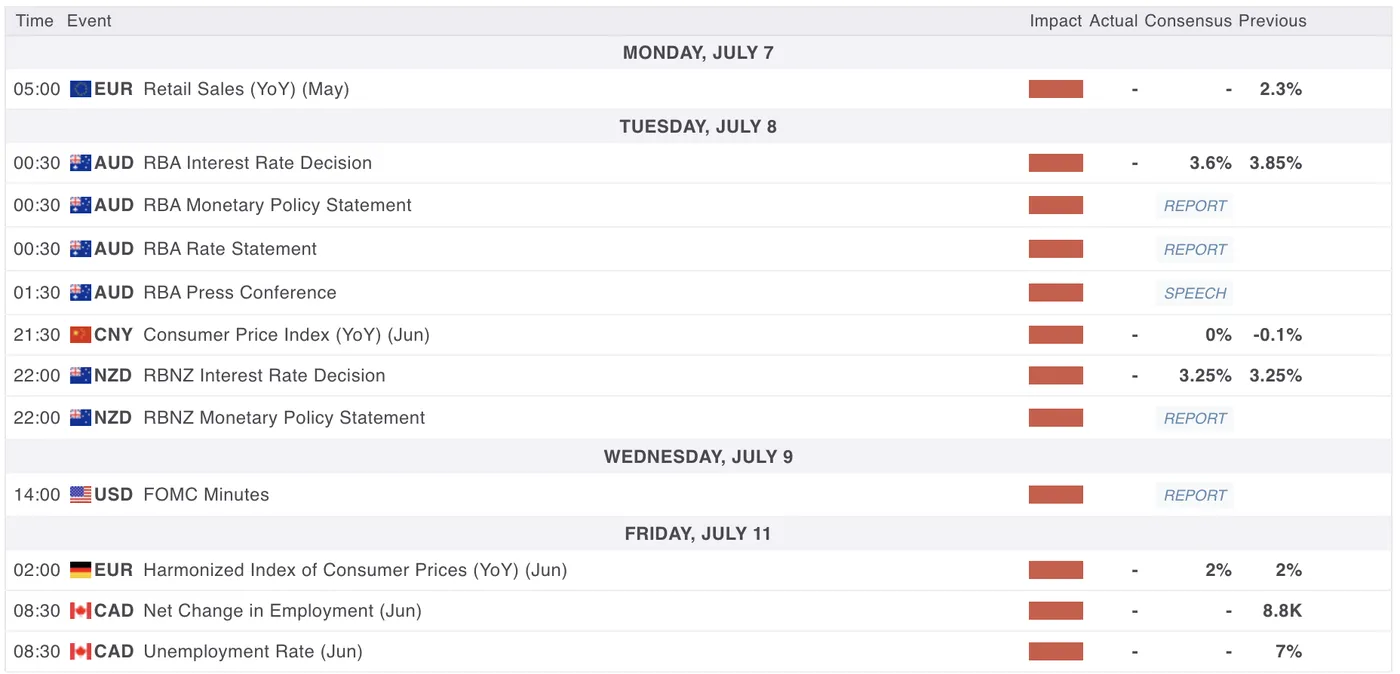

Reserve Bank of Australia Rate Decision

The Reserve Bank of Australia, after cutting its cash rate by 25 bps to 3.85 % in May (its first trim since January), is widely expected to shave another 25 bps to around 3.60 % at its upcoming meeting as inflation cools but global headwinds linger.

The decision will be released in the July 7th to 8th overnight session at 00:30 A.M. (8/07).

Reserve Bank of New Zealand Rate Decision

The Reserve Bank of New Zealand—having lowered its OCR by 25 bps to 3.25 % in May—is forecast to hold rates at 3.25 % on Tuesday July 8th at 10:00 PM, though markets see further easing into early 2026 amid a still‑negative output gap.

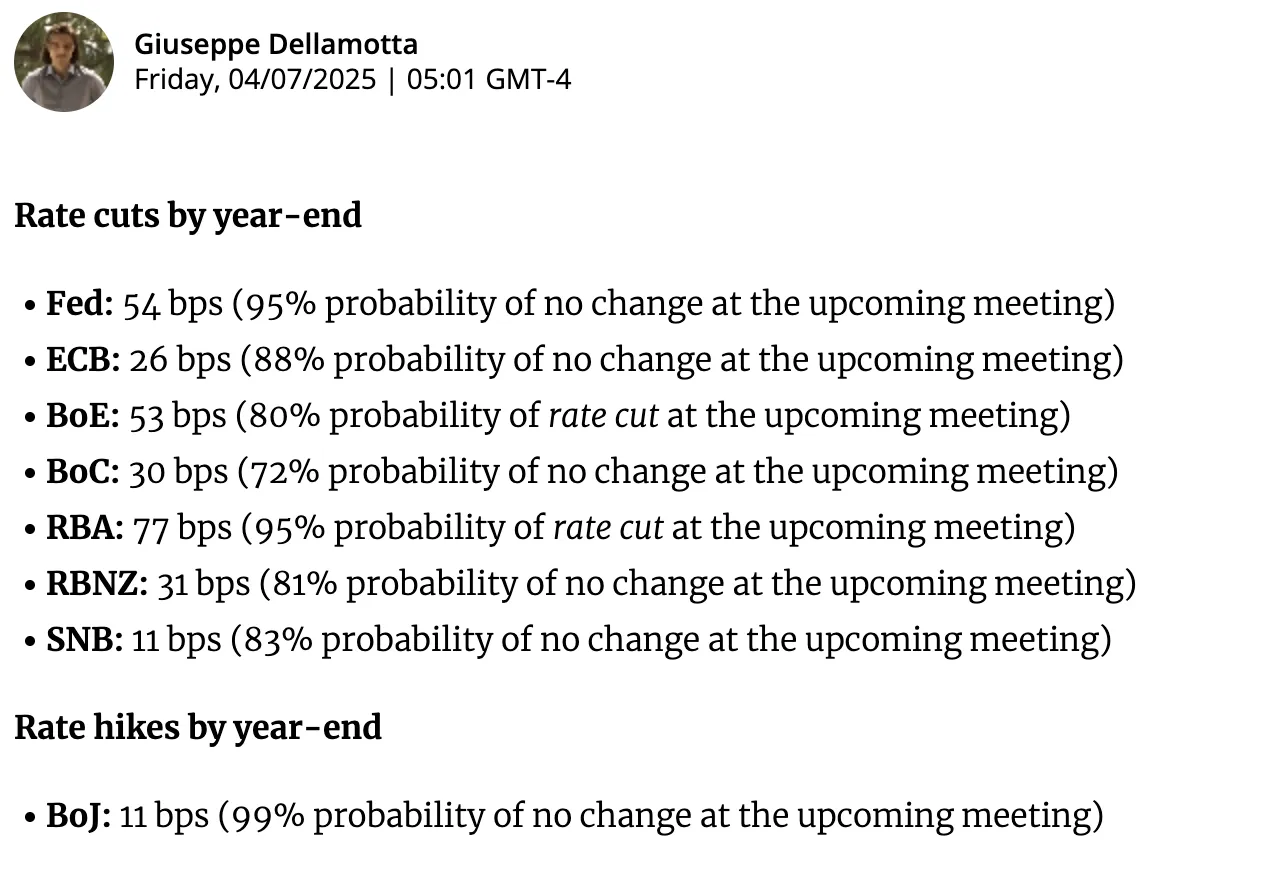

Central Bank Cut/Hike Market Pricing

Central Bank Cut/Hike market pricing – Source: Forexlive.com

Central Bank Cut/Hike market pricing – Source: Forexlive.com

BRICS Meeting in Rio De Janeiro

Brazil, Russia, India, China, and South Africa will convene this week in Rio de Janeiro, July 6 and 7 to discuss current geopolitical issues, including US tariffs, recent Middle East developments and other habitual subjects (expansion, climate action, commodity demand, development goals, …).

Economic Data from Europe, UK and North America

North America will mostly be concerned with the July 9th deadline from the Trump Administration to start imposing tariffs, which even though it had been priced in severely in the beginning of this year, has been broadly downplayed in the “TACO” trade trend.

Don’t forget the few bouts of CAD moving data with Ivey PMI on Tuesday at 10:00 A.M. and Canadian Employment on Friday at 8:30 ET.

In European markets, economic releases will mostly focus on the Eurozone Retail Sales and some ECB Speakers – the rest will be lower-tier data.

Key Events coming up next week (Hier-Tier Data only) – MarketPulse Economic Calendar

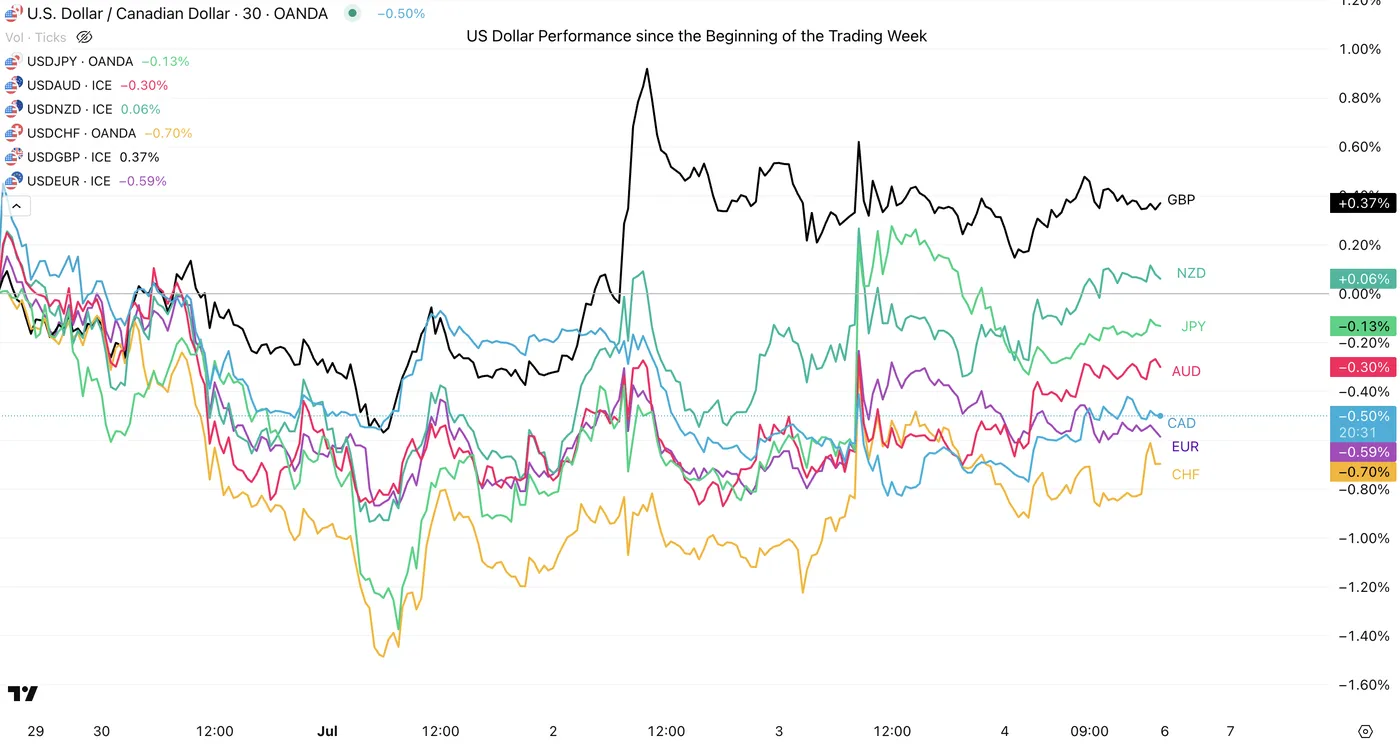

US Dollar performance versus other Forex Major counterparts

US Dollar Performance since the Beginning of the Trading Week, July 4, 2025 – Source: TradingView

The US Dollar has seen a decent rebound in the latter part of this week but still finishes down against most of its major counterparts – The CAD has however held particularly strong against the USD in the end of the week, something to check in the upcoming week.

CHF and the EUR have also had a consistent decent performance in the beginning of the week particularly but have started to show signs of potential tops – This will depend heavily on an upcoming potential US Dollar rebound, scenario explored in our latest Dollar Index analysis.

Weekly Asset Performance

Cross-Asset Weekly Performance, July 4, 2025 – Source: TradingView

Gold has bulls have seen some newfound strength but Ethereum takes the crown for this week’s cross asset performance.

The US Dollar and 30Y Bonds have on the other hand been the laggers of the week, again. Let’s see if the Dollar regains some ground after the positive NFP report from Thursday.

Safe Trades in the upcoming week!

{kind=link}