Sterling came under heavy pressure today, tumbling sharply alongside a selloff in UK government bonds. The 10-year gilt yield surged above 4.65%, up 20 basis points from levels seen just two days ago. The moves came after Prime Minister Keir Starmer’s government backtracked on key parts of its welfare bill to avoid a major Labour rebellion. The retreat may have salvaged the vote, but came at the cost of credibility. More importantly. uncertainty is also swirling around Finance Minister Rachel Reeves, after Starmer failed to affirm her job security during a heated parliamentary exchange today.

Meanwhile, from the US came a shock downturn in ADP employment, which posted a -33k print for June — the first monthly contraction since early 2022. The data has cast a shadow over Thursday’s non-farm payrolls, with markets now bracing for possible downside risks to the labor market. While July remains unlikely for Fed to resume cutting rates, further downside surprises in job creation or wage growth would likely make the FOMC’s decision a much tighter call.

Overall in the currency markets today, Sterling is by far the weakest major while Kiwi and Aussie are also under pressure, pointing to a broader risk-off tilt in markets. Euro and Yen are trading in the middle of the pack. Dollar is currently the strongest, recovery from its near term losses. Loonie and Swiss Franc follow.

Technically, with the strong break through 61.8% retracement of 1.0610 to 1.1200 at 1.0835 today, GBP/CHF is now on track to retest 1.0610 low. Further downside acceleration would raise the chance that it’s actually resuming whole down trend from 1.1675 (2024 high). In any case, near term outlook will now stay bearish as long as 1.0930 support turned resistance holds.

In Europe, at the time of writing, FTSE is down -0.45%. DAX is down -0.05%. CAC is up 0.79%. UK 10-year yield is up 0.189 at 4.647. Germany 10-year yield is up 0.039 at 2.614. Earlier in Asia, Nikkei fell -0.56%. Hong Kong HSI rose 0.62%. China Shanghai SSE fell -0.09%. Singapore Strait Times rose 0.53%. Japan 10-year JGB yield rose 0.04 to 1.432.

US ADP shock, private payrolls drop -33k in June

US private sector employment unexpectedly declined by -33k in June, according to ADP data, far below expectations for a 105k gain.

The weakness was concentrated in service-providing industries, which shed -66k jobs, while goods-producing sectors added 32k. Small businesses were hit the hardest, cutting -47k positions, while medium companies lost -15k, large firms added 30,000.

ADP Chief Economist Nela Richardson noted that while layoffs remain rare, firms are increasingly hesitant to hire or replace departing staff. “A hesitancy to hire and a reluctance to replace departing workers led to job losses last month,” she said.

Despite the hiring slowdown, wage growth remained relatively stable. Job-stayers saw annual pay increases of 4.4% yoy in June, just slightly below May’s 4.5% yoy. For job-changers, pay growth slipped to 6.8% yoy from 7.0% yoy, suggesting firms are still offering premiums for switching jobs, though at a moderating pace.

BoE’s Taylor backs steeper rate cuts as outlook deteriorates

BoE MPC member Alan Taylor warned today that the UK economy faces mounting risks to a soft landing, citing growing demand weakness and trade disruptions. In a speech, Taylor said his earlier forecast for a gradual disinflation and stable growth path is now at risk of being derailed in 2026.

“My reading of the deteriorating outlook suggested to me that we needed to be on a lower rate path, needing five cuts in 2025 rather than the market-implied quarterly pace of four,” Taylor said, citing recent shocks and global uncertainty that clouded his earlier view.

Taylor, who has consistently pushed for more aggressive easing, has voted for cuts in five of seven MPC meetings since joining last September—including a 50bps move in May followed by 25bps in June.

ECB’s Rehn warns of inflation undershoot risk, urges vigilance

Finnish ECB Governing Council member Olli Rehn warned that the Eurozone faces renewed risks of inflation falling below the 2% target as global uncertainties intensify. While acknowledging that risks to the outlook exist on both sides, Rehn said the downside appears more pressing. “The risk of staying below target is greater in my view, especially as our projections see price growth under target for 18 months,” he noted.

Rehn pointed to a trio of disinflationary forces — a strong Euro, lower energy prices, and rising tariffs — which he argued are weighing on both inflation and growth. “We need to be mindful of the risk of inflation staying persistently below 2%,” he said.

ECB’s Wunsch sees case for mild supportive stance as downside risks dominate

Belgian ECB Governing Council member Pierre Wunsch said the central bank may need a “mildly supportive” stance, especially if Eurozone recovery continues to lag. In an interview with Reuters, Wunsch noted “If the recovery is delayed — and it has been delayed a few times — and output is below potential, then being supportive is rational,” he said.

Wunsch highlighted several disinflationary forces at play, including lower energy prices, the strength of Euro, subdued wage growth, and the lack of tariff retaliation. He also flagged cheap Chinese imports as a contributing factor to weakening price pressures. “All these factors combined suggest that the upside risk is limited and the overall risk is to the downside,” he added.

With markets pricing in one final 25 basis point cut later this year, bringing the deposit rate to 1.75%, Wunsch said he was not uncomfortable with that view. “I don’t disagree with market pricing for interest rates,” he noted.

ECB’s Centeno: Must wait for more data before next move

Portuguese ECB Governing Council member Mario Centeno welcomed the return of Eurozone inflation to the 2% target, calling it “very good news.” However, he also stressed that the ECB remains focused on assessing incoming data.

Centeno told Bloomberg TV that the ECB is “monitoring all possible numbers” and assessing various aspects of the Eurozone’s 20-member economy. “The current situation doesn’t mean that we need to rush into more interest-rate reductions,” he said. “We need to see data, we need to see the developments.”

Eurozone unemployment unexpectedly rises to 6.3% in May

Eurozone unemployment rate edged higher to 6.3% in May, missing expectations for an unchanged reading at 6.2%. Eurostat data showed 10.83m people unemployed in the Eurozone, part of a total 13.05m across the EU.

The broader EU jobless rate held steady at 5.9%, but the number of unemployed rose by 54k in the Eurozone and by 48k in the EU compared to April.

Aussie retail sales underwhelm with 0.2% mom growth in May

Australia’s retail sales rose just 0.2% mom in May, falling short of expectations for a 0.3% rise. The modest increase was largely due to a rebound in clothing purchases, while spending on food fell and household goods remained flat.

Robert Ewing, ABS head of business statistics, noted that aside from the lift in clothing, retail spending was generally “restrained”.

He also noted that this dataset is nearing its conclusion, with July’s release set to be the last edition of Retail Trade. Going forward, the Monthly Household Spending Indicator (MHSI), which leverages administrative data, will replace it as a more comprehensive tool for tracking household consumption trends.

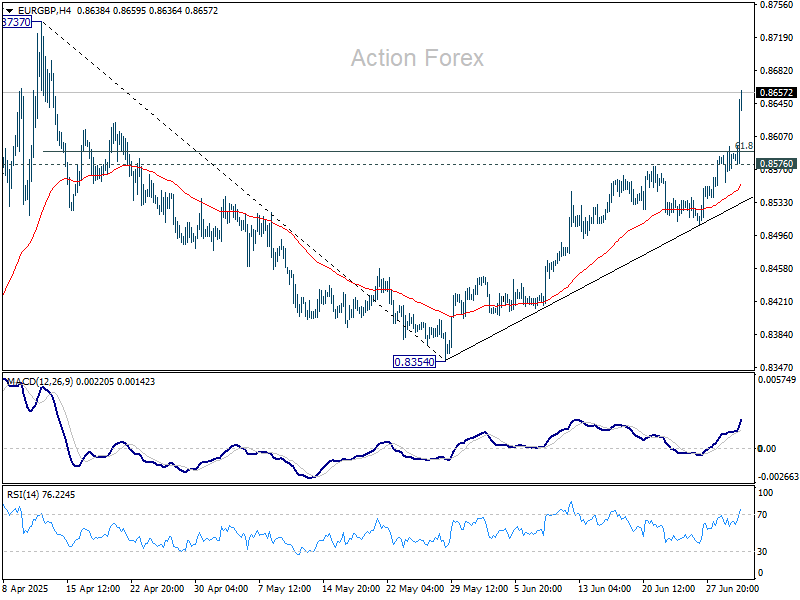

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8565; (P) 0.8581; (R1) 0.8605; More…

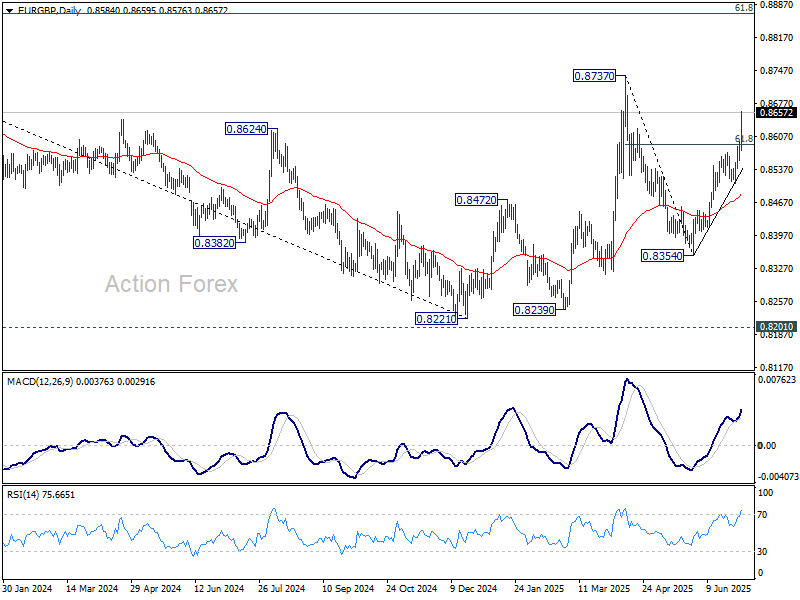

EUR/GBP’s rally from 0.8354 accelerated higher today and powered through 61.8% retracement of 0.8737 to 0.8354 at 0.8591. Intraday bias stays on the upside for retest 0.8737 high. Decisive break there will resume the whole rise from 0.8221 low. On the downside, below 0.8576 minor support will turn intraday bias neutral first.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it’s reversing the downside from 0.9267 (2022 high). But even if it’s a correction, firm break of 0.8737 will still pave the way to 61.8% retracement of 0.9267 to 0.8221 at 0.8867.

{kind=link}