- China to gain more airtime this week

- The ailing housing sector and the bond rally in focus

- RBA remains hawkish, but consumer appetite is critical

- Aussie benefits from dollar weakness

Market’s focus could turn to China this week

The post non-farm payrolls week tends to be a quiet one as the market digests the latest developments and prepares for the next risk events. Accordingly, the calendar is less impressive this week apart from Fed Chairman Powell’s testimony on Tuesday and Thursday’s US CPI release. This means that the market could have time to focus on countries away from the spotlight, for example China.

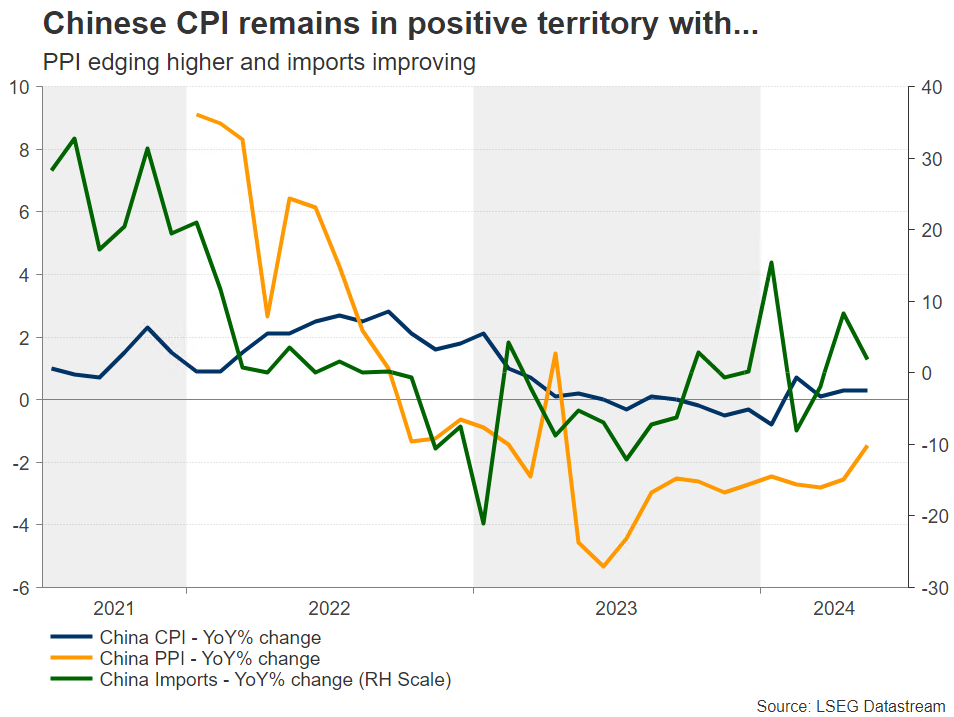

China’s main issue remains the housing sector. Supply destocking is progressing very slowly with the housing price index dropping to the lowest level since July 2015. The strong set of measures announced in May 2024 has yet to make an impact, which raises the possibility for further action from the Chinese authorities.

Communist Party’s plenary session on July 15-18 could hold surprises

Actually, the third plenary session of the 20th Communist Party of China (CPC) Central Committee will be held on July 15-18, with the usual issues being on the agenda. Boosting domestic demand appears to be the primary target of this session with developments in the housing sector also to be discussed. The market is speculating that further support measures could be announced during the plenary.

In the meantime, there appears to be a storm brewing in the bond market. Sovereign bond yields have been dropping aggressively as demand for safe assets has been increasing from (a) investors preparing for another stock market crash, and (b) commercial banks trying to safely invest their spare reserves as borrowing slows down. The PBoC has announced its willingness to intervene forcefully in the market, but the real solution would probably be to act upon China’s underlying economic issues. This makes the upcoming plenary session even more important.

Amidst these developments and following a rather mixed set of public and private PMI surveys, the inflation report for June will be published on Wednesday with the key trade balance data following towards the end of the week. CPI has been edging higher lately, and combined with the recent uptick demand for imports, one could argue that there are some tentative signs of improving domestic demand.

Amidst these developments and following a rather mixed set of public and private PMI surveys, the inflation report for June will be published on Wednesday with the key trade balance data following towards the end of the week. CPI has been edging higher lately, and combined with the recent uptick demand for imports, one could argue that there are some tentative signs of improving domestic demand.

RBA remains hawkish

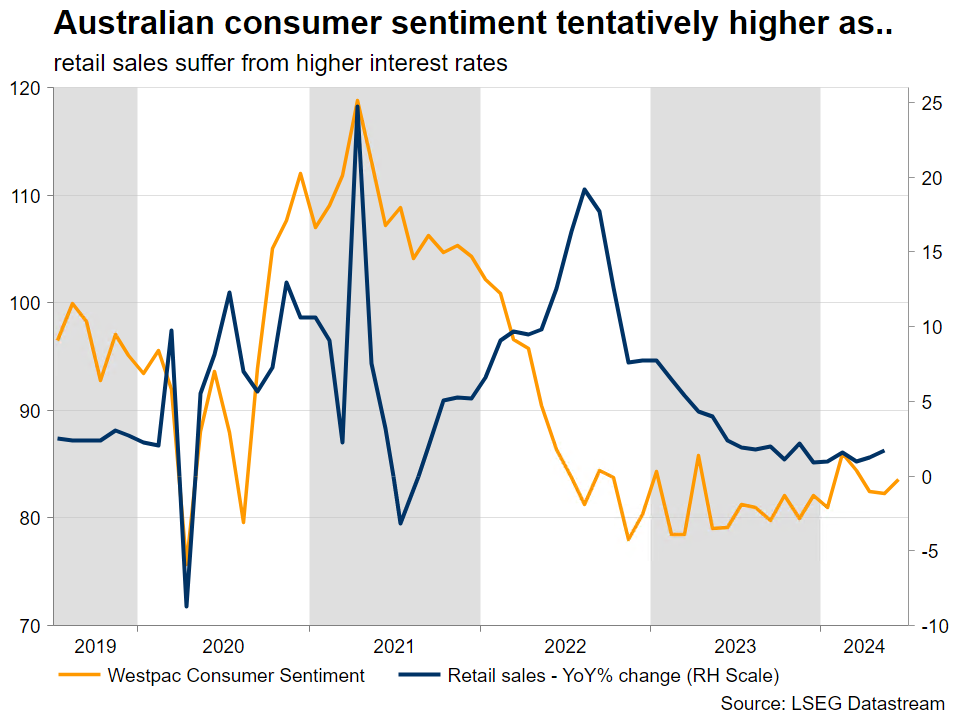

Not far from the Chinese shores, the RBA remains one of the most hawkish central banks. The June 19 meeting kept the door open to a rate cut down the line if data supports it. And considering the data released since then, the door remains firmly open as the labour market remains tight and the May CPI jumped to 4%. However, consumer appetite remains the big question mark going forward, especially as the housing market continues to show signs of weakness on the back of heightened interest rates.

Focus on inflation-related prints ahead of end-July official CPI report

Following the recently disappointing PMI surveys, there are some interesting data releases this week such as the Westpac consumer confidence indicator and the consumer inflation expectations index. The latter is especially critical for the RBA as it jumped to 4.4% in June and, despite the downward trend that has been in place since June 2022, progress has been very slow lately.

This mirrors the inflation stickiness seen across the developed countries, which is the main reason for the Fed postponing its much-expected rate cuts. The market understands that the crucial number for the RBA is the July inflation report for the second quarter of 2024 released at the end of July. Considering the various inflation indicators, predominantly the May and June monthly inflation prints, there is a strong possibility for an upside surprise on July 31. Confirmation of such an outcome could unlock the rate hike for the RBA, making the August 6 meeting live.

Aussie/dollar tests 2024 highs

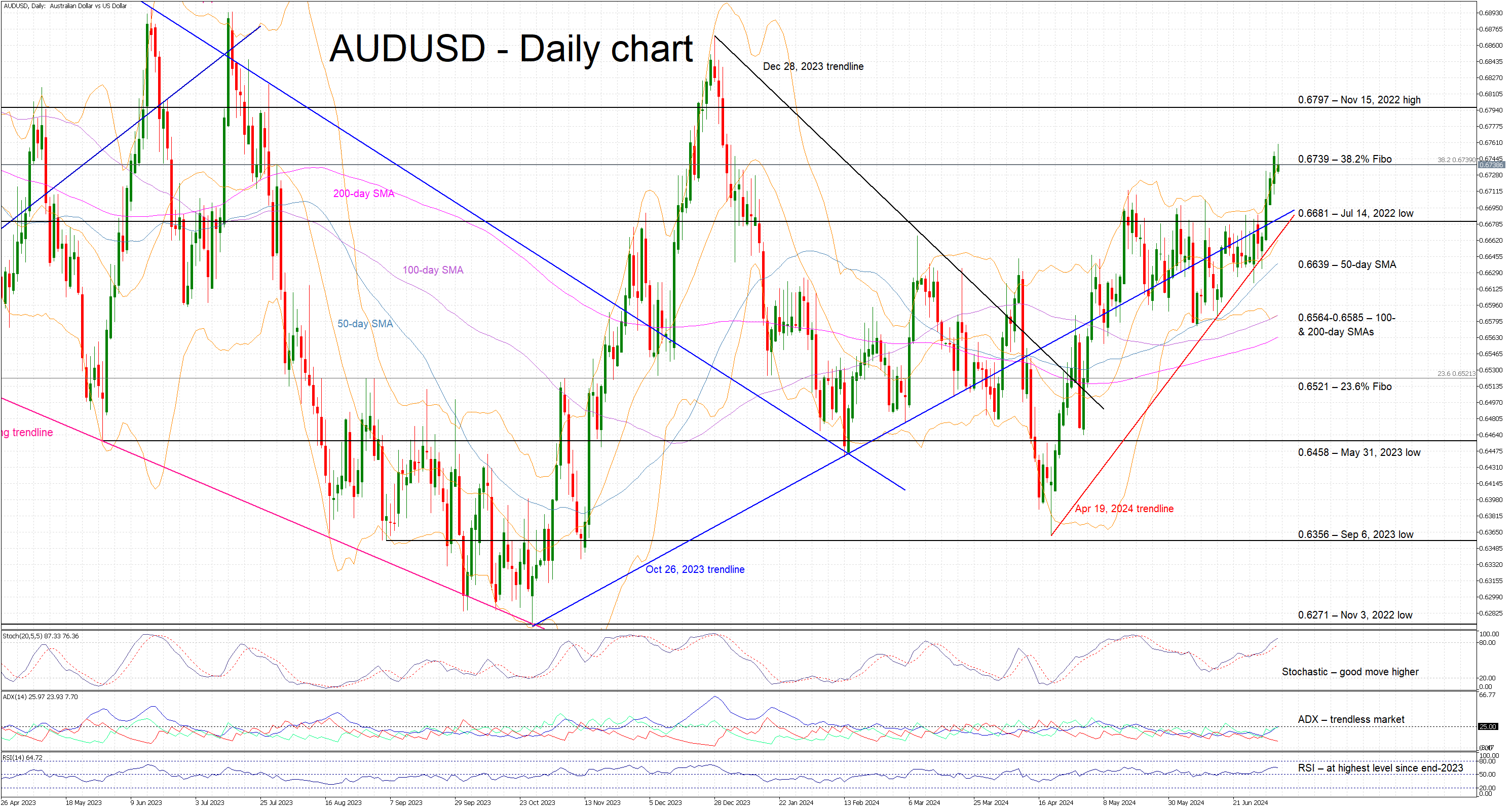

The aussie/US dollar pair has managed to forcefully break above the 0.6681 level, which has been acting as strong resistance over the past two months. Last week’s weak US labour market data, the revitalized expectations for a September Fed rate cut and the continued hawkishness of the RBA has allowed the aussie to take advantage of widespread dollar weakness. A strong set of Chinese and Australian data could boost the pair further, but only a dovish appearance from Chairman Powell and a weak US CPI print could unlock a rally towards the end-2023 highs.

{kind=link}