Sunrise Market Commentary

- Rates: Bearish sentiment on bond market remains in place

Today’s eco calendar heats up, but (US) eco data might be overshadowed by tomorrow’s CPI and retail sales. A speech by Atlanta Fed Bostic will be closely monitored. He’s relatively new on the Fed, but votes on policy next year. If he indicates willingness to hike rate 3 times next year, we might get more repositioning (bear flattening US yield curve). - Currencies: Euro holds the lead as risk rally slows

USD/JPY again held up well yesterday even as risk sentiment turned less buoyant. EUR/USD kept a cautious upward bias. Today’s eco calendar heats up. Especially US PPI might move the dollar, but the focus remains on tomorrow’s US CPI and retail sales. Sterling traders will keep a close eye at UK CPI and at the debate on the Brexit withdrawal bill

The Sunrise Headlines

- US stock markets closed with small gains after a weak opening. Overnight, Asian stock markets trade mixed with Japan slightly outperforming this time.

- Theresa May bowed to pressure from pro-European Conservatives by offering the British parliament a full vote on a final divorce deal, the latest sign of how political turmoil within her government is taking a toll on her Brexit plans.

- China’s economy cooled further last month, with industrial output, fixed asset investment and retail sales missing expectations as the government extended a crackdown on debt risks and factory pollution.

- Venezuela was declared in default by S&P Global Ratings after missing two interest payments on its debt. The nation owed investors about $200 million and failed to pay by the end of a 30-day grace period.

- Treasury Secretary Mnuchin said the Trump administration wouldn’t support tax legislation with a corporate tax rate of more than 20% as part of any future compromise between the House and the Senate.

- The number of banks deemed systemically important and subjected to extra regulation in the US would drop by two-thirds under plans to roll back Obama-era reforms (Dodd-Frank) that have attracted bipartisan support.

- Today’s eco calendar heats up with UK inflation data , EMU Q3 GDP, EMU industrial production, German ZEW investor sentiment and US NFIB small business sentiment and US PPI. Several central bankers speak including ECB Draghi, Fed Yellen, BoE Carney and BoJ Kuroda in Frankfurt

Currencies: Euro Holds The Lead As Risk Rally Slows

Dollar holds tight ranges ahead of key US data

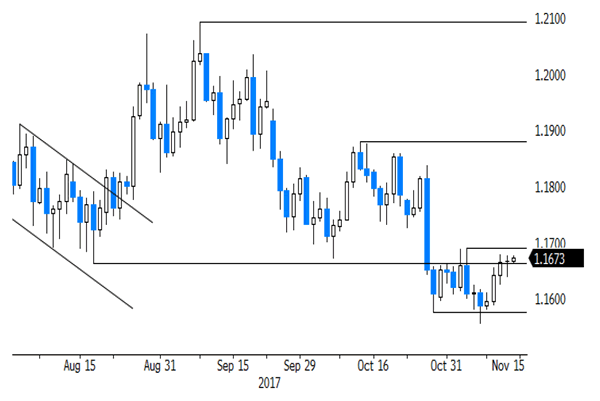

Yesterday, EUR/USD and USD/JPY trading was similar to what happened at the end of last week. Core yields hardly declined in European risk aversion. EUR/USD traded with a slightly positive bias intraday. High core yields prevented any substantial losses in USD/JPY. Risk sentiment improved in US dealings. It supported USD/JPY, but the dollar remained in the defensive against the euro. EUR/USD finished the day little changed at 1.1667. USD/JPY closed the session off the intraday lows at 113.62.

Asian equities are mostly trading in negative territory. Japan this time is the exception to the rule. Chinese retail sales and production data were a touch softer than expected. USD/JPY is holding in the 113.60 area after yesterday’s intraday rebound, but the pair is still locked in tight ranges. Changes in EUR/USD (1.1675) also remain small, but the pair nears 1.1690 resistance.

German ZEW investor sentiment and the details/composition of the EMU Q3 GDP will be published today. We don’t expect a big impact on the euro. US PPI is expected to rise 0.1% M/M and 2.5% Y/Y after a bigger rise last month (0.4% M/M and 2.6% Y/Y). The focus remains on tomorrow’s US CPI and retail sales, but interest rates and the dollar might react to the PPI’s, especially in case of a negative surprise. There were will be many headlines from the ECB conference on Central Bank communication, attended by ECB president Draghi, Fed Chair Yellen, BoE governor Carney and BoJ governor Kuroda. The meeting might yield interesting ‘theoretical’ insights, but we don’t expect CB heads to address actual monetary policy. The US tax bill also remains a wildcard for global trading. Basically, we expect more technical, sentiment-driven trading. A soft US PPI or a more pronounced risk-off sentiment might tilt the balance slightly against the dollar. Tomorrow’s US retail sales and CPI have most potential to move interest rates and FX markets this week. We started the week with a cautious bias on the dollar as the US currency recently was more vulnerable to negative news than the euro. We maintain that USD caution. That said, we don’t expect any USD setback to go very far though.

From a technical point of view, EUR/USD dropped below 1.1670/62 support, but subsequent follow-through price action occurred very slowly. The pair dropped to a new post-ECB low on Tuesday last week. A sustained break would confirm that the recent EUR/USD uptrend is broken. EUR/USD 1.1423 (38% retracement of 2017 rise) is the next downside target on the charts. A return north of 1.1690, would question recent downside momentum. Next resistance stands at 1.1837/80. USD/JPY’s momentum was positive in past months. The pair regained 110.67/95 resistance and tested the 114.49 MT range top. The attempt failed. A sustained break would improve the technical picture. We remain cautious to preposition for further USD/JPY gains. Last week’s price action was unconvincing despite a solid interest rate support.

EUR/USD: rebound off recent low. 1.1690 resistance under test ahead of key US eco data

EUR/GBP

UK CPI to rise north of 3%?

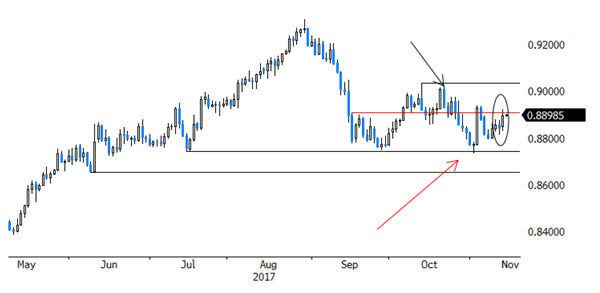

Sterling came again under pressure yesterday as press articles indicated that a growing number of Conservative MP’s wants a vote on PM’s May leadership, illustrating the deep division within the Conservative party. Several sterling selling waves pushed EUR/GBP to the 0.8920 area. Cable dropped to the 1.3062 area, but the ST range bottom (1.3040/27) was left intact. Later, UK Brexit minister Davis said that Parliament will have a final say on a Brexit deal. The pressure on sterling eased slightly. EUR/GBP finished the session at 0.8896 (from 0.8841).

The October UK price data will be published today. Headline CPI is expected at 0.2% M/M and 3.1% Y/Y. A rise above 3% was anticipated by the BoE. The BoE expects it to be temporary as price rises due to sterling’s decline will gradually ease. If inflation prints above 3%, Governor Carney has to write an explanation to the Chancellor of the Exchequer. Carney will probably argue that the peak in inflation is (almost) reached. Sterling might be slightly supported if Carney stresses that some modest further tightening is still possible. Markets will also keep a close eye at the debate on the ‘EU Withdrawal Bill’ in Parliament. This debate will probably create plenty of political noise. Fortunes for sterling probably won’t improve as long as political uncertainty stays as high as it is now.

MT technical: Sterling rebounded in September as the BoE prepared markets for a rate hike. This rebound ran into resistance as markets anticipated that any rate hikes would be very gradual and limited. This view was confirmed at this month’s BoE policy meeting. EUR/GBP currently trades in a 0.8733/0.9033 consolidation range. A downside test of this range was rejected. We assume that the 0.8733-0.8652 support will be tough to break. A EUR/GBP buy-on-dips approach for return action to the EUR/GBP 0.9023/33 ST range top is favoured

EUR/GBP: CPI and Brexit bill to guide GBP trading today