The U.S. Federal Reserve will be closely watching January inflation data on Wednesday after foregoing an interest rate cut last month for the first time in the last four meetings.

A resilient U.S. economy isn’t signalling an urgency to cut interest rates further. Retail sales likely ticked lower in January, given a pullback in auto sales after a string of upside surprises. That leaves any additional interest rate reductions in the near term more contingent on price growth continuing to slow towards a 2% rate.

We expect some signs of gradual easing in core price growth in January, but with the total consumer price index growth holding at 2.9% year-over-year, and the risk of a round of tariff hikes on imports from China threatening to stall further progress later this year.

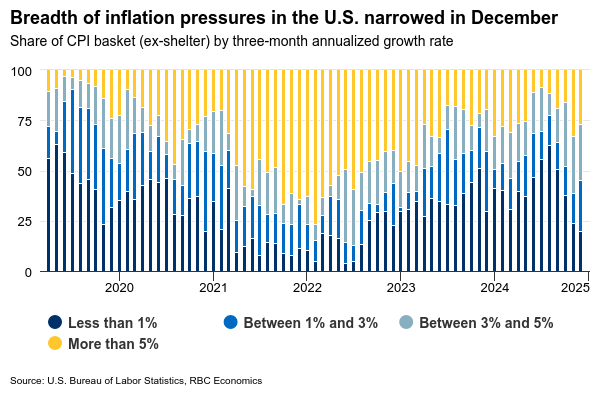

We expect core prices edged up by 0.2% for a second straight month, excluding volatile food and energy components. Growth in home rent prices has continued to slow as expected from an earlier slowdown in market rent costs filtering gradually through to lease renewals. Growth in core goods prices slowed in December after a larger rise in November. By our count, the breadth of inflationary pressures narrowed in December, and we will watch our diffusion measure closely for further signs of broader easing in price pressures.

We don’t expect that progress on inflation will be enough to prompt additional interest rate cuts from the Fed this year.

Week ahead data watch

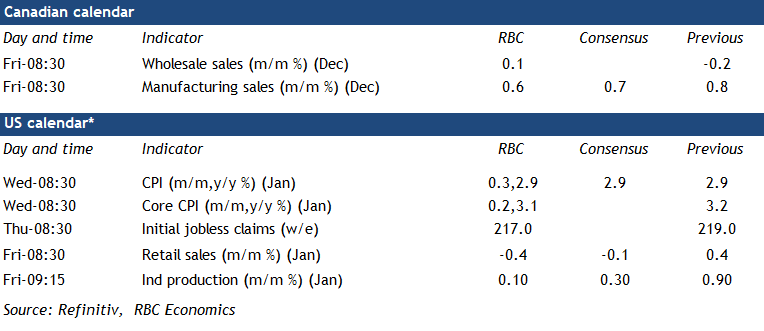

We expect manufacturing sales to edge 0.6% higher in December, in line with Statistics Canada’s preliminary estimate. Most of the increases were driven by higher sales in petroleum and coal products, and food subsectors.

Canadian wholesale trade likely grew 0.1% in December, according to StatsCan’s early indicator, given sales were up in the motor vehicles, parts and accessories subsector.

We look for 0.4% growth in January U.S. retail sales, slowing from the 0.5% increase in December. Auto sales dropped sharply during the month. Sales at gas stations saw price increases, but not enough to offset the pullback from the auto sector.

U.S. industrial production likely slowed from 0.9% to 0.1% in January, given hours worked in mining and manufacturing sectors both declined during that month.

{kind=link}