Global markets showed signs of stabilization today, but conviction remained notably absent as investors positioned cautiously ahead of Wednesday’s pivotal US CPI report. Technology shares rebounded strongly across Japan and South Korea, oil prices eased, and Dollar softened. Yet the moves appeared driven more by profit-taking and position adjustment than by a decisive shift in sentiment.

The recovery in technology stocks was particularly notable given last week’s sharp AI-driven selloff. However, the rebound may not be as reassuring as headline price action suggests. Market flow data indicate that while technology shares have rallied for two consecutive sessions, institutional investors continue to build net short positions across US and Asian technology sectors. That pattern points more toward short covering and profit-taking rather than the return of meaningful long-term buying interest.

Part of the improvement in sentiment also came from softer oil prices. Brent crude extended its retreat as US President Donald Trump again suggested that a deal to end the conflict with Iran could be reached within “two or three days.” Markets welcomed the possibility of progress, but the reaction remained measured. Traders appear reluctant to fully embrace a de-escalation narrative given the repeated delays and setbacks that have characterized negotiations in recent months.

The result is a market that is neither fully risk-on nor risk-off. Instead, investors appear content to reduce exposure and wait for clearer signals from inflation data. Following last week’s stronger-than-expected US nonfarm payrolls report, attention has shifted almost entirely toward inflation and whether rising energy costs are beginning to feed more broadly into consumer prices. A stronger CPI reading would likely reinforce expectations of additional Fed tightening, with implications for yields, Dollar and risk assets.

One notable exception to the generally cautious tone was Sterling. The Pound gained support after the BRC Retail Sales Monitor delivered a major upside surprise. UK retail sales rose 3.7% year-on-year in May, far exceeding expectations for a 0.6% increase and sharply reversing April’s -3.4% decline. While favorable weather and holiday spending contributed to the rebound, the data also suggested consumers remain more resilient than many had expected despite elevated borrowing costs and energy prices.

That resilience carries important policy implications. If consumer demand remains firm while inflation pressures persist, the case for another Bank of England rate hike later this year could strengthen considerably. For now, Sterling’s outperformance reflects growing confidence that the UK economy may be proving more resistant to higher rates than previously assumed.

In currency markets, New Zealand Dollar led gains for the week, followed by Sterling and Euro. Dollar is the weakest performer, with Yen and Swiss Franc also under pressure. The mixed ranking underscores the broader theme of selective positioning rather than a unified market view, a dynamic that could change rapidly once the US inflation data are released.

Oil Traders Are Betting on Peace; The Clock Is Betting on $150 Crude

Oil prices suggest traders still expect diplomacy to prevail. But beneath the surface, governments and businesses have been relying on strategic reserves and inventory drawdowns to offset supply disruptions from the Strait of Hormuz. Those buffers are finite, and the next few weeks could determine whether Brent continues falling—or begins a march toward $150. Read More.

Silver’s $70 Breakdown May Have Changed Everything

Silver’s slide below $70 may be more important than the selloff itself. A level viewed as a structural floor supported by supply deficits and industrial demand has now broken, raising the possibility that $70 could become a new ceiling. The next rebound may reveal whether investors are buying the dip—or using rallies to exit positions. Read More.

China Exports Surge 19.4% as US Trade Truce and Tech Demand Fuel Growth

China’s trade sector delivered another upside surprise in May. Exports surged nearly 20%, led by booming technology shipments, rising vehicle exports and a sharp rebound in trade with the US. Strong import growth and record purchases from South Korea also point to resilient manufacturing activity across Asia. Read More.

Australian Consumer Sentiment Falls Back Near Record Lows as Cost-of-Living Pressures Intensify

The pressure on Australian households is intensifying. Consumer confidence fell back near historic lows in June as cost-of-living concerns returned “with a vengeance”, highlighting the growing economic toll of higher prices and interest rates. Read More.

Australia NAB Business Confidence Lifts From Deep Lows as RBA Tightening Bites

The worst fears about the energy shock have not materialized. Australia’s latest NAB survey showed improving business confidence, steady activity and a sharp slowdown in cost and price growth, offering signs that RBA tightening is having the desired effect. Read More.

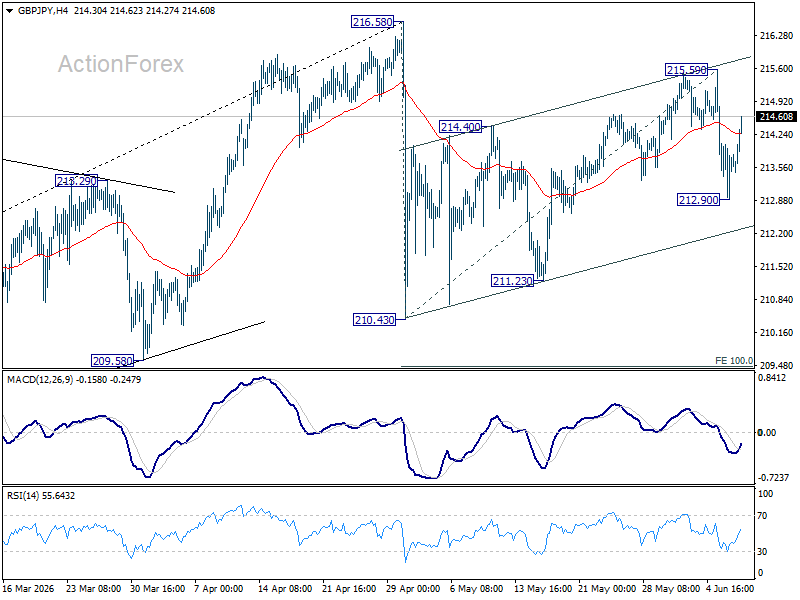

GBP/JPY Daily Outlook

Intraday bias in GBP/JPY is turned neutral with current recovery. Risk will stay mildly on the downside as long as 215.59 resistance holds. Below 212.90 will target 210.43/211.23 support zone. However, firm break of 215.59 will resume the rebound from 210.43 to retest 216.58 high instead.

In the bigger picture, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 206.77) will argue that it’s already in medium term down trend for 184.35 support.

{kind=link}