US-China trade talks over the weekend developed more positively than both we and consensus expected. Below we give a short overview of what happened and the implications in US and China, respectively.

What it means for the US

While both US and Chinese officials had signalled a positive outcome from the Geneva negotiations already on Sunday, the cuts to tariff rates were larger than we had anticipated. Treasury Secretary Scott Bessent announced a 115%-point reduction to the previous rate of 145%, which would take the rate close to pre-Liberation Day level of 30%. Previously, our baseline scenario included a cut down to 60%. The cuts are initially in effect for 90 days, as was the case with the delay of other reciprocal tariffs as well.

Before Trump entered the office, the average tariff rate on Chinese goods imports was around 10-12%. And already before the Liberation Day, the rate was increased twice by 10%-points at a time as part of the so-called ‘Fentanyl tariffs’.

For estimating the economic impact, we are going to assume a tariff rate of 30%. It is not immediately clear for us if the 10% universal tariff also applies on top of the pre-Trump rates and the Fentanyl tariffs. This means the rate could be slightly higher around 40-42%.

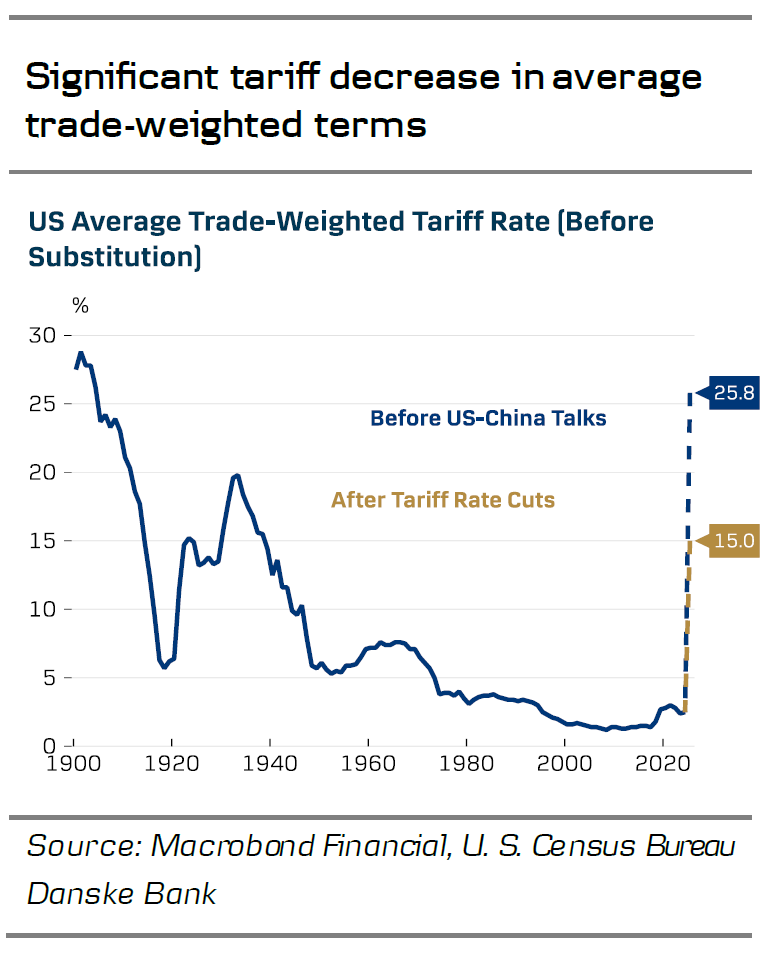

Before today’s announcements, the average tariff rate on all US imports was around 25.8%. Cutting the Chinese rate to 30% reduces the average rate by more than 10%-points to around 15%. The Tax Foundation estimated earlier, that without reductions, the tariffs would weigh on US GDP by around 0.8% or 1.0% including retaliation. After today’s announcements, the expected negative impact on US GDP could be nearly halved to only around 0.5%.

It is worth noting that consensus forecast for US GDP growth in 2025 had already been downgraded from 2.2% to 1.4% after the Liberation Day, reflecting a negative impact of 0.8%. Hence, if made permanent, today’s tariff announcements could pose upside risks to current consensus growth outlook. While the easing does not naturally alleviate all of the negative consequences already seen in international trade and consumer/business sentiment, in our view today’s announcement significantly reduces the risk of an outright recession down the line.

What it means for China

From a Chinese perspective the talks were also a success. China had several goals met:

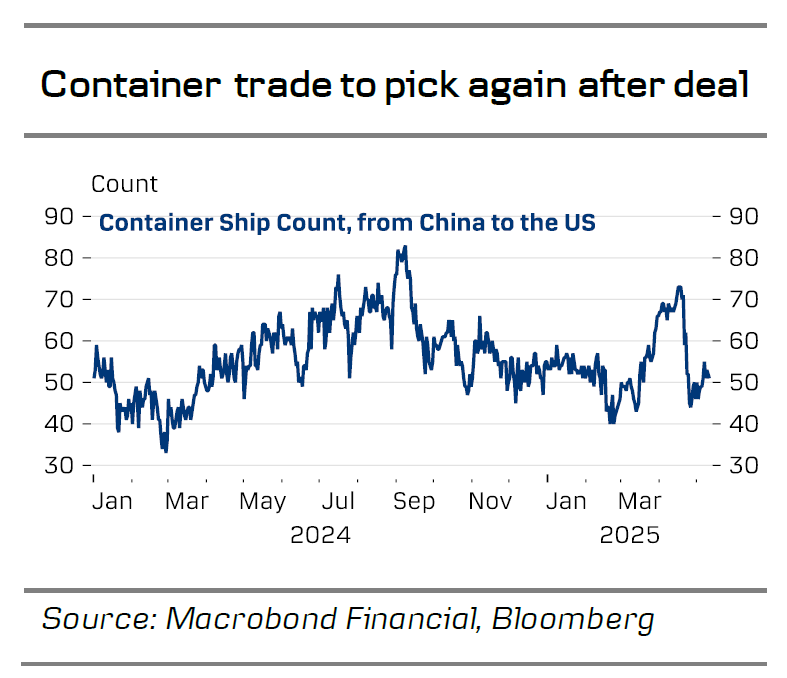

First and foremost, tariff rates have been significantly reduced, which means trade can resume and Chinese companies exporting goods for Halloween, Christmas, Black Friday etc. can ship their goods at tariff rates that are manageable. China could soon see tariff rates reduced by a further 20% if they strike a deal on Fentanyl, which seems likely based on positive comments from Bessent on China’s efforts to meet the US on this point.

With tariff rates significantly lower, the Chinese growth outlook for the coming quarters looks a lot better.

Second, negotiations according to the Chinese delegation happened in a good atmosphere with mutual respect, sincerity and understanding for the other side. These are key points for China and often underestimated. And in China it vindicates that the initial strong retaliation has paid off with the US showing more respect now instead of bullying. People matter in diplomacy and Bessent and Greer seem to be the right people at the table. You can disagree and have demands but if you show respect and understanding, it is much easier to get results when dealing with China.

Second, negotiations according to the Chinese delegation happened in a good atmosphere with mutual respect, sincerity and understanding for the other side. These are key points for China and often underestimated. And in China it vindicates that the initial strong retaliation has paid off with the US showing more respect now instead of bullying. People matter in diplomacy and Bessent and Greer seem to be the right people at the table. You can disagree and have demands but if you show respect and understanding, it is much easier to get results when dealing with China.

Where to go from here?

US-China talks are set to continue over the coming months. One of the tracks are related to Fentanyl and could very well lead to a further reduction in US tariffs on China by 20%- points. In the medium to longer term, trade talks will likely take time and could easily face bumps on the road due to disagreements on industrial policy, Chinese purchases of US goods etc.

It is worth keeping in mind that achieving significant reductions in US trade deficit with China, which remains a high priority for the US side according to Greer, appears unlikely without a significant reduction in US demand. During Trump’s 1st term, China failed to reach the levels of US goods purchases outlined in the so-called ‘Phase One’ trade deal agreed in 2019, and achieving a deal that satisfies all demands for both sides will be difficult to reach this time around as well – especially within the timeframe of only 90 days. However, it now seems more likely we could end up close to our original baseline scenario where US tariff rates on China are ultimately around 40%. A headwind but manageable for both sides.

Market implications

The agreement has fuelled a rally in global stocks, higher yields and a decline in EUR/USD and USD/CNY. The move reflects lower perceived risk of a US-driven growth slowdown, and was also evident in oil prices ticking higher. In the short-end of the USD curve, markets now price in only a 10% chance of the Fed cutting rates in June, and the next 25bp rate cut is fully priced in only by the September meeting. With trade talks on a better footing, macro data will likely start to matter more for market developments in the coming months – not least US data.

{kind=link}