- As widely expected and priced, today the RBNZ reduced the OCR by a further 25bps to 3.25%.

- The decision was reached following a 5 – 1 vote, with one MPC member voting for no change in policy.

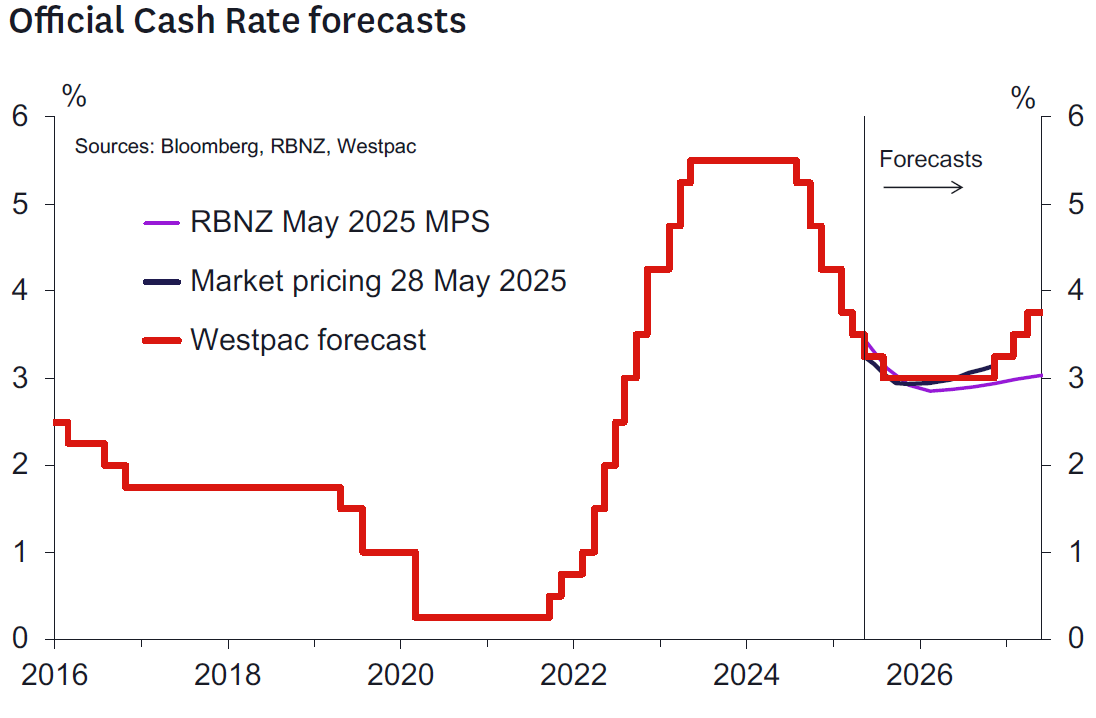

- The revised projection indicates a baseline expectation of 1-2 further OCR cuts by the end of this cycle, with 1 of those 2 cuts to occur in the September quarter.

- The RBNZ noted that is well placed to respond to both domestic and international developments to maintain price stability over the medium term.

- The Governor noted that the MPC has “no clear bias” for the July decision.

- Westpac now sees the next 25bp cut to 3% at the August MPS (previously July). But they could easily be done if the downside risks don’t crystalise.

Key messages from the RBNZ today.

As was widely expected and fully priced by the market, today the RBNZ announced a further 25bps reduction in the OCR to 3.25%. Given the unanimity of financial market opinion regarding this decision, the focus today was always going to be on the RBNZ’s revised projections and commentary and what this might imply regarding the outlook for policy at future meetings. In our opinion the following are the key take-outs:

- The RBNZ’s projection for the OCR now bottoms at 2.85% in the March 2026 quarter, compared to 3.1% in the February MPS.

- This was largely as expected and implies 1-2 further 25bp easings by cycle end.

- More surprisingly, the decision was reached by a 5-1 vote. One member voted for the OCR to remain unchanged, seeking to consolidate inflation expectations near the target midpoint and allowing more time to judge the impact of US policy uncertainty on household and business behaviour.

- During the press conference, Governor Hawkesby said that there was consensus regarding the medium-term OCR projection, but differences in view regarding the timing of how to get there.

- The RBNZ’s near-term OCR projection implies a further easing in the September quarter. In the press conference, Governor Hawkesby said the RBNZ would enter the next meeting with “no bias” regarding the outcome, which would depend on information over the intervening period.

- Mathematically, the RBNZ’s forecast of a 3.12% average OCR in the September quarter implies that this is more likely to occur at the August meeting, rather than the July meeting.

- CPI inflation is forecast to peak at 2.7%y/y in the September quarter, before declining to 1.9%y/y by early next year.

- The RBNZ’s near-term GDP growth forecasts are weaker than in February, although the unemployment rate is still expected to nudge higher to a peak of 5.2% before beginning to edge lower.

- The RBNZ notes that the risks surrounding the economic outlook are “heightened”, reflecting some uncertainty about whether the global trade shock will ultimately prove to be a net negative demand shock (thus disinflationary) or net negative supply shock (thus inflationary).

- To illustrate these risks, the RBNZ published two alternative scenarios. The downside demand scenario portrays a decline in the OCR to 2.55%. The supply shock scenario continues to forecast a decline in the OCR to 2.9%, but then a lift in the OCR to 3.5% later in the forecast period.

- Notably, these are both negative shock scenarios. The RBNZ did not explore scenarios where the impact of tariffs is less than in their central forecasts, though they acknowledge that this also a possibility.

- The RBNZ regards Budget 2025 as a wash for the economic outlook, with lower government spending (compared with the HYEFU) offset by an assumed lift in private capex in response to the “Investment Boost” policy.

Westpac’s view on policy outlook.

There was more division in the ranks of the MPC than expected. We expected increasing debate on the outlook for the OCR and the amount of weight to put on a higher near-term inflation profile, versus a lower medium-term profile as excess capacity and the weaker global outlook drag inflation down to the middle of the 1-3% target range. A vote on the merits of today’s 25bp cut hence signals more debate than that and suggests a raised bar for OCR cuts at each meeting going forward.

The RBNZ has reduced its near-term growth forecasts quite noticeably. The profile implies a pause in the recovery in place in recent quarters with quarterly growth expected in the range of 0.2-0.4% a quarter over Q1-Q3 2025. Our expectations are stronger – in the range of 0.4- 0.7% in the same period. The noticeably weaker trading partner growth profile is consistent with this mark down. That this weaker short term growth profile only argues for one more cut in Q3 seems telling.

The focus of the MPC on inflation expectations is noticeable and appropriate. Evidence these are falling back will likely be important in making the MPC hawks more comfortable with getting back on the easing track. The Q2 CPI on 18 July may well be pivotal in that regard.

We think this is an MPC that wants to slow down. Governor Hawkesby noted the MPC has no bias regarding the outcome of the next meeting. We previously expected the final cut to 3% to occur in July, although we were agnostic on whether this might also end up occurring in August. August looks a better bet now – hence we are moving our call.

There’s plenty of water to go under the bridge both domestically and internationally. We suspect that it will be easier to make the case for another easing in August than July given the pending negotiation dates set by the US authorities on trade agreements. The Q2 CPI will also be quite important. But equally uncertainty is high and a range of events both positive and negative could occur. So, we will watch the data like the RBNZ.

It’s too early to call time on the easing cycle. But you never know its ended when it ends. Policy is well placed to respond to whatever happens now the OCR is in the middle of the long- and short-term estimates of the neutral OCR (these range between 2.9 and 3.6%). Policy is “neutralish”.

If nothing overtly negative happens to the economy or medium-term inflation outlook between now and August, then there could be no change in the OCR in August also. Let’s see.

Summary of RBNZ’s economic view.

The RBNZ has revised down its near-term forecasts for economic growth, which are softer than our own. Part of that reason for that downward revision was the updates to forecasts for government spending in Budget 2025.

More notable are the updates to the cyclical components of GDP, with softer outlooks for investment spending and export growth. A key reason for this is the weaker outlook for global growth as a result of increased trade protectionism. The RBNZ has revised down its forecasts for global GDP growth in 2025 by 0.5ppts (year total basis). The related reductions in demand and increases in economic uncertainty are expected to be a drag on investment appetites.

Looking to next year, we see a risk that the strength of the New Zealand consumer surprises the RBNZ on the upside. Despite assumed low interest rates and increasing employment, the RBNZ’s forecast for household spending growth is weak over 2026.

On the inflation front, the RBNZ’s overall forecasts are broadly similar to our own. However, we think that the details of the inflation outlook will surprise the RBNZ. In particular, we don’t expect domestic inflation pressures will be as weak as the RBNZ is expecting over the medium term. The RBNZ expects non-tradables inflation will fall as low as 2.8% next year. In contrast, we think that ongoing and sizeable increases in government charges and other administered costs will see non-tradables inflation tracking close to 3.5%. On the other side of the equation, we don’t expect the same lift in imported inflation that the RBNZ has assumed. However, it’s those domestic inflation pressures, which have consistently surprised the RBNZ on the upside in recent years, that will be the bigger concern.

Key data and events before the RBNZ’s 9 July meeting.

Looking ahead to the RBNZ’s next policy review on 9 July, the key domestic data and events will be:

- The May Selected Price Indexes (17 June): This will provide the last indication of the likely outcome of the Q2 CPI report, which will not be released until 21 July.

- The Q1 GDP report (20 June): The outcome of this report will be compared to the RBNZ’s estimate, with any deviation having implications for the RBNZ’s estimate of the output gap and perhaps also its view on near-term growth momentum.

- The Q1 QSBO survey (1 July): The focus in this report will be on indicators of Q2 activity and cost/inflation pressures. The survey will reveal how confidence, hiring and investment indicators are looking in light of uncertainty about the global outlook and in reaction to policy changes contained in Budget 2025.

In addition to the above, key monthly activity indicators such as the Business NZ manufacturing and services indexes (mid-June) and the ANZ Business Outlook survey (late June) will also be of interest, as will developments in retail spending and in the housing market. Developments in the labour market will likely be tracked especially closely. A lift in filled jobs and job advertising would provide some reassurance to the RBNZ that the recovery is strengthening and becoming self-sustaining. Meanwhile, the inflation expectations measures from the ANZ’s consumer and business surveys will also be of some importance, to see whether their recent lift has endured.

Outside of New Zealand, interest will clearly centre on any clarity that emerges regarding the final form of US tariff policy and its implications for New Zealand’s export sector and inflation. The RBNZ’s policy decision will be announced on the same day (in US time) that the pause on President Trump’s ‘reciprocal’ tariffs is due to expire (ex-China). However, recent comments from Trump suggest that final decisions are likely to be taken sooner, at least regarding tariffs on some countries. Both the Fed and RBA will conduct policy reviews in the lead-up to the RBNZ’s meeting (the RBA just the day before the RBNZ’s decision is announced).

{kind=link}