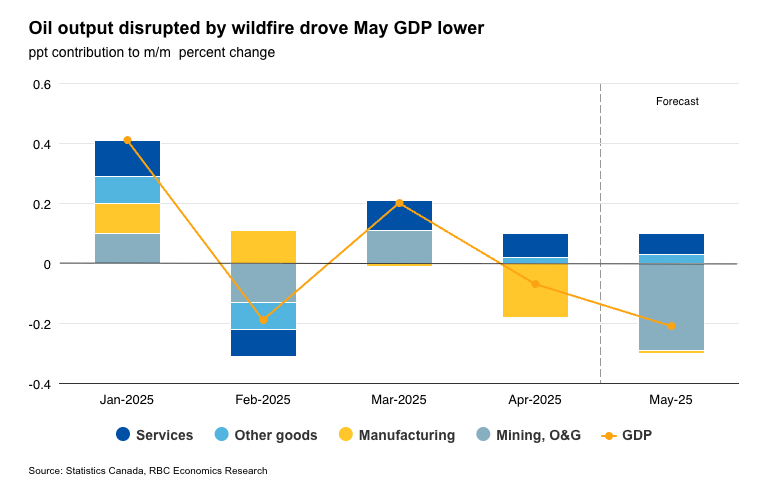

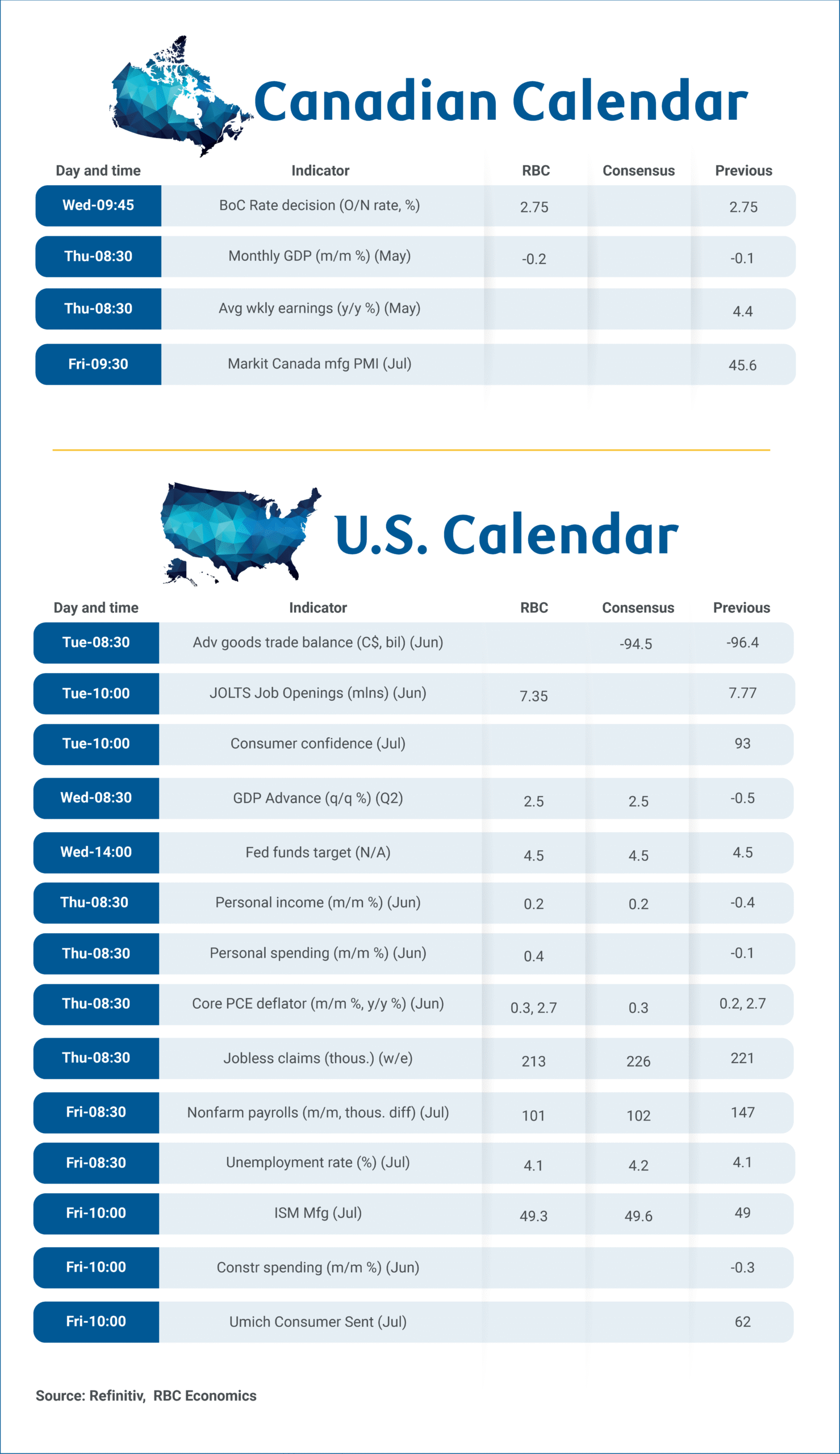

We’re expecting the Bank of Canada to leave the overnight rate unchanged again on Wednesday, while Thursday’s May’s gross domestic product (GDP) report for Canada will likely show a larger 0.2% decline, though most of it is expected to have reversed in June.

Manufacturing activity likely remains soft from ongoing trade disruptions, but we expect the bulk of May’s GDP decline could be attributed to a sharp decline in oil production, as wildfires in Alberta significantly disrupted operations.

Retail activity was also soft, dragged down by lower auto sales that reversed earlier gains in March and April when consumers pulled purchases forward to front-run tariffs.

Losses from both factors – lower retail purchases and oil production – are expected to have at least partially recovered in June. Statistics Canada’s preliminary estimate was for a 1.6% increase in nominal retail sales in June following the 1.1% May decline. Additionally, rebuilding efforts following natural disasters could also have supported GDP growth in other sectors.

On a quarterly basis, Q2 GDP growth is tracking close to flat— aligning with the more optimistic of the two scenarios the BoC projected in its April forecast. In its last Monetary Policy Report, the central bank took the unusual step of not providing a base case growth forecast but scenario analysis, given the enormous uncertainty tied to international trade at the time.

We’ll be watching Wednesday’s MPR closely for new projections but don’t expect any surprises regarding the decision to hold the overnight rate steady. The BoC has remained on the sidelines for the past two meetings after cutting the overnight rate by 225 basis points since June 2024.

What’s holding the BoC back?

Trade tensions remain heightened and economic data is still soft. However, the Canadian labour market showed signs of bottoming out in June, and sentiment indicators, which took a nosedive in March, have also partially recovered.

Critically for Canada, CUSMA exemptions are allowing the vast majority of Canadian goods exports to enter the U.S. duty-free. Echoing business reports from the latest BoC outlook survey, we continue to consider the most severe economic scenarios as less probable than earlier in spring, and expect the economy will remain soft over the second half of this year but won’t contract.

More unnerving for the BoC are recent inflation reports that have surprised broadly to the upside. Its preferred core measures have edged higher in 2025, driven mostly by building pressures among domestic services components. This contradicts earlier expectations that softening in domestic demand would lead to further disinflation and easing in core inflation.

Overall, sticky inflation readings, a weakening but relatively resilient economic backdrop and prospects for larger fiscal spending are reasons why we do not expect the BoC will cut again in this cycle.

Week ahead data watch:

Job vacancies in May’s Canadian Survey of Employment, Payrolls, and Hours (SEPH) data on Thursday will be analyzed for signs of softening in the labour market. Alternative job openings data from Indeed.com have stabilized in the summer after declines earlier in the year.

The U.S. data calendar is also crowded next week. U.S. Q2 GDP On Wednesday is expected to show an annualized increase of 2.5%, reflecting in part the reversal of a statistical quirk that distorted trade and inventory figures in Q1. The Fed meeting that afternoon is expected to maintain current rates and otherwise uneventful Friday’s July payrolls data is forecast to show a moderately slower but still robust pace of job growth. The unemployment rate from the separate Household Survey is expected to have remained unchanged at 4.1%.

report for Canada will likely show a larger 0.2% decline, though most of it is expected to have reversed in June.){kind=link}