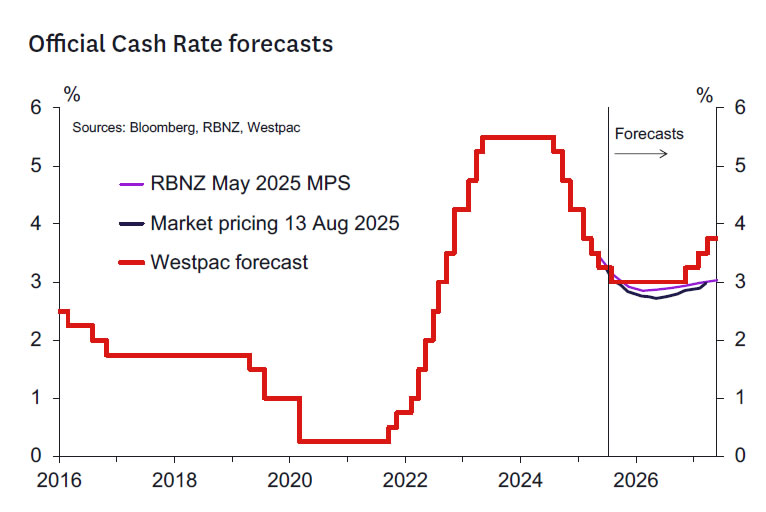

- We expect the RBNZ to cut the OCR by 25bp to 3%.

- We don’t expect a significant change in the RBNZ’s OCR profile, which is still likely to indicate a chance of a further cut in November.

- Beyond this meeting a data-dependent easing bias seems likely. A higher bar seems likely for an easing in October.

- We don’t expect a split vote, but we do expect to see evidence of debate among MPC members around the weight placed on high near-term inflation and rising expectations versus lower medium-term forecasts.

RBNZ decision and communication.

In its July review the RBNZ clearly indicated an easing to 3% was on the cards at the next meeting, assuming the dataflow between May and August went as expected. There’s nothing in the recent dataflow that should deter them from this course of action – even though there may be more debate on the outlook from August. The MPC member who voted for a pause in May had a different view on the timing of cuts and not the quantum in general. Hence, we anticipate a consensus decision this time around.

The focus will be on the forward outlook. In May, the view was a chance of easing in November – but not a full chance. Something like a 50:50 probability seemed to be in the tea leaves back then. There didn’t seem like a high chance of an October cut barring significantly adverse surprises. The view was that the OCR was on a glide path within the “neutral-ish” zone. There wasn’t much consideration of a move into stimulatory territory – even in the adverse scenario canvassed in the forecasts.

We don’t think that view will have changed much. Some domestic data has surpassed expectations (GDP, firmer CPI indicators) while other indicators may have disappointed (consumer spending, housing market indicators, PMI indices). In aggregate these don’t seem to have amounted to much. Hence if the forward track changes we expect it will be at the absolute margin – and such changes carry no policy information at all.

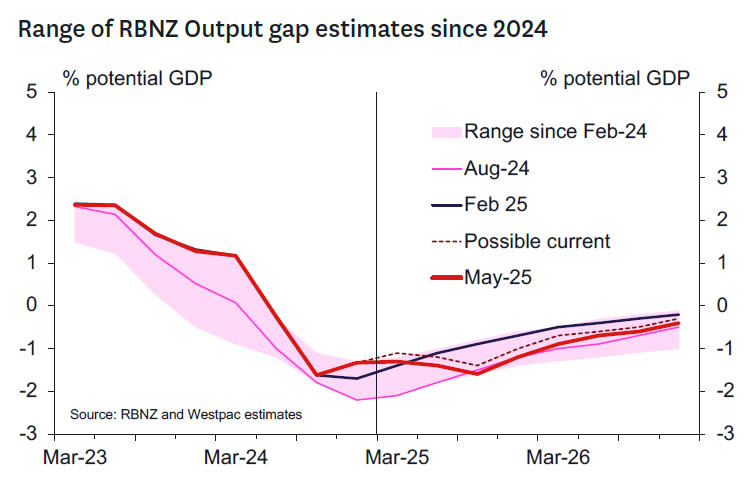

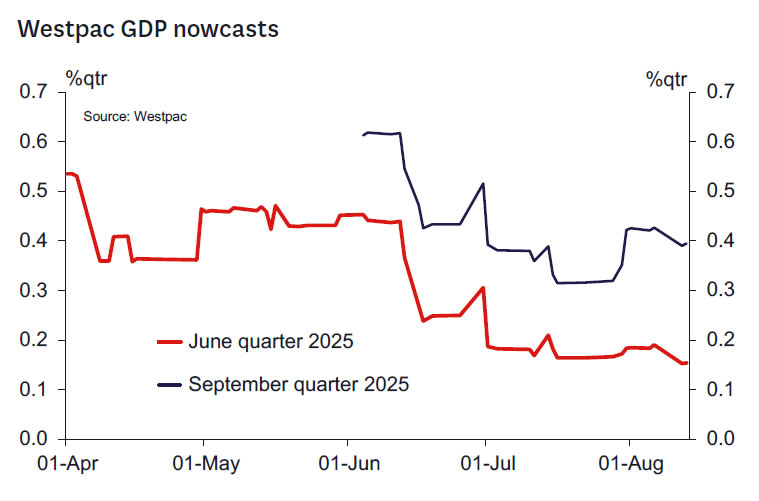

It’s useful to keep in mind that the RBNZ included a lot of weakness in their near-term output profile in their May forecasts. The weaker indicators seem to suggest that these adjustments were appropriate. We might see some adjustments at the margin to the timing of GDP growth. The RBNZ’s GDP Nowcast for the June quarter is lower than their previous forecast for 0.4% growth. So that might be revised down closer to our 0% q/q forecast for that quarter – incorporating the full impact of the residual seasonality that weighs down June quarters and boosts December quarters. The RBNZ’s forecast for the September quarter could be revised up from the 0.2% currently forecast. Hence, we might just see some subtle shifting in the profile as opposed to an aggregate marking down of 2024 growth (which at 1.8% y/y is low considering the 0.4% upside surprise the RBNZ got for March quarter GDP). We suspect the RBNZ’s output gap and short-term profile will be no weaker than presented in May and should be a touch less negative, implying less disinflation pressure in the medium term at the very margin.

The commentary on the labour market will be interesting but likely inconsequential. The RBNZ’s tendency is to start with their activity forecasts and develop an output gap estimate. The unemployment rate follows from that using an Okun’s law type relationship. Notwithstanding the substantial heat in the discourse around the Q2 labour market reports a week or so ago, it won’t change much for the RBNZ. We expect them to tweak the peak unemployment rate to reflect a higher peak than the optimistic 5.2% peak published in May. And we think they might push out the time over which the unemployment rate remains at the peak, so it lines up better with the output gap, assuming the expected lag between a pickup in quarterly growth and falling unemployment. None of this should impact the policy decision or OCR path at all. It’s all fine-tuning.

The commentary on the global outlook and tariffs will likely remain cautious and negative. The forecasts will reflect the increase in Consensus Forecasts since May. But we suspect the MPC will retain concerns that US trade policy has some twists and turns to go before the woods are formally cleared. We don’t expect the RBNZ to increase the indirect impacts of the external situation. Export prices have remained firm, and the global outlook isn’t weaker. NZ did end up with a larger tariff than was known in May. But the direct impacts of this were always likely to be negligible in aggregate. And hopefully the RBNZ’s business visits will have confirmed the view we have received from customers than it’s been generally OK to pass these direct costs through to US importers. And certainly, in aggregate the US import price data shows this seems to have been the case. Hence, we don’t expect much impact on the forecasts in the end.

The RBNZ expended a reasonable amount of capital in May shaping market expectations towards expecting OCR cuts at Monetary Policy Statements instead of at every meeting. In July, RBNZ Chief Economist Conway suggested that not much had changed for them since May. Hence, we think the strategy will remain the same. This will be to point markets to the data between now and November to support that last OCR cut. We don’t expect the RBNZ to reignite expectations of off-Monetary Policy Statement OCR changes unless something very untoward happens. And we haven’t seen that yet. That implies that the December 2025 OCR number of 2.92% looks about right. That’s about a 50:50 chance of a further cut in November. We don’t think the chances of a further cut are that high.

Could we get commentary raising the risks of a need to move the OCR into clearly stimulatory territory? We don’t think so, as to do so would invite markets to price such moves in quite soon and box the RBNZ in. Such a change in strategy would need to be supported by more substantive changes in the forecasts and risks. The global outlook might be such a pretext. But more likely would be an assessment that we need to see a decidedly stimulatory OCR relative to where the RBNZ thinks neutral is (currently RBNZ estimates range between 2.9-3.6%). Typical OCR cycles in non-crisis times often see the OCR bottom perhaps 50-125bp below neutral. Getting to that point might require knocking a substantial amount off the 2025 and 2026 growth forecast, presumably on the view that interest rate-sensitive segments of the economy won’t respond until an OCR in the 2-2.5% range is delivered. There’s been little evidence in support of that view emerging since May. There’s certainly plenty of exasperation as to how long it’s taking for the economy and labour market to pick up, hence the theme of our recent Economic Overview: “Are we there yet?” But central bankers know the lags are long and variable, so we doubt they will be too fazed yet. Especially with inflation knocking at the door of 3% for the next 5 months.

On inflation, we think they will boost their short-term forecasts such that annual inflation is forecast to be close to 3% for the remainder of this year (in the May MPS inflation was projected to be 2.7% and 2.4% respectively for the September and December quarters). That December quarter forecast looks particularly low and is a likely candidate for an upward revision, as it otherwise implies a sudden drop in quarterly inflation quite soon. We don’t think the medium-term forecasts will change much. Hence the mantra will be repeated where the MPC will retain confidence that inflation will head back towards 2% in the medium term.

Some alternative scenarios for the outcome of this meeting include:

- Hawkish scenario (10% probability) – a 25bp cut with a clear intent to pause. The RBNZ would note an intent to review things again in November but indicate a high hurdle for further cuts. This could happen if the RBNZ is losing confidence in where the CPI will peak, and how fast it will realistically fall in 2026. Rising inflation expectations would fuel that fire.

- Dovish scenario (10% probability)- a 25bp cut with a presumption of a further cut to 2.75% by November. The possibilities of a move lower still in the OCR towards 2-2.5% might also be discussed as a risk scenario. The RBNZ would be putting more weight on the downside growth and inflation scenario, with less regard for the short-term inflation picture.

Key developments since the May Monetary Policy Statement.

Activity: High-frequency economic data has generally been softer compared to the March quarter, though it’s more of a mixed tone rather than the broad-based downturn that we saw in mid-2024. The manufacturing PMI has dropped below the 50 mark again, and the comparable services index has remained soft. Retail card spending has lost some ground since the start of the year, although it recorded modest gains in the last two months. Westpac’s GDP Nowcast suggests an underlying growth pace of 0.1-0.2% for the June quarter. The actual GDP print is likely to come out lower than this, due to a seasonal distortion that has affected the figures recently, but the RBNZ had already made an allowance for this effect in its May forecasts.

Sentiment indicators: Forward-looking business confidence measures have generally held up at high levels, although the measures of current performance remain soft. The monthly ANZBO survey has picked up again after the initial shock of the ‘Liberation Day’ tariff announcement in April.

Global developments: Trump’s tariff announcements have been coming thick and fast in recent months, but as it currently stands, the weighted average US tariff rate is basically where it was at the time of the May MPS. There seems to be a growing acceptance of tariffs as the ‘new normal’, and Consensus forecasts of GDP growth for our main trading partners have been revised slightly higher again after the initial fall.

Inflation: June quarter inflation was close to the RBNZ’s forecast: annual inflation rose to 2.7% compared to their May forecast of 2.6%. The small upside surprise was likely due to the large increase in food prices. Swings in the prices of volatile items like food aren’t the focus for monetary policy. However, higher food prices and continued increases in administered costs (like rates) mean that inflation is likely to rise to around 3% before the end of this year – higher than the RBNZ had previously forecast. The RBNZ had noted this risk in their July policy review. Under the surface, core inflation remains within the target range and prices for more interest ratesensitive items have moderated.

Inflation expectations: We have seen a lift in some measures of expected inflation in surveys of households from both the RBNZ and ANZ. However, businesses’ expectations for inflation have remained well contained, as seen in both the RBNZ’s Survey of Expectations and in the ANZBO. Surveys of businesses’ plans for pricing from the ANZ and NZIER have been mixed.

Labour market: The unemployment rate rose to 5.2% in the June quarter, in line with the RBNZ’s forecast, although the 0.1% fall in employment was weaker than expected. The monthly filled jobs and vacancies data show that the current momentum remains weak, suggesting that the RBNZ will need to revise up its May forecast that the unemployment rate will peak at its current level.

Housing market: House sales and loan applications are running well ahead of year-ago levels. However, amidst a plentiful supply of dwellings, house prices have effectively been flat (and on the low side of the RBNZ’s forecast).

Commodity prices: Export commodity prices have generally held up over the last few months, with dairy prices coming off their recent highs while meat prices have made further gains. World oil prices have risen about 6% since May, against the RBNZ’s assumption of a slight fall.

Exchange rate: The current trade-weighted index (TWI) is only marginally below the 69.0 that the RBNZ assumed in its May Statement.

Kelly’s take.

There’s a decent case to remain on hold at this meeting and see how the economy progresses over the rest of the year. The building blocks of recovery are in place in the form of 225bp of interest rate cuts and very strong export returns that are not being meaningfully dented by the trade war.

A large part of the case for easier conditions in April and May was predicated on the global situation seriously spilling over to New Zealand. There might have been some of that in business and consumer sentiment in recent months. But mostly this hasn’t happened. Uncertainty will pass while the impact of commodity prices and interest rates will be more enduring. Market expectations of further OCR cuts increased the most recently when rate cut expectations in the US increased. This doesn’t seem like a good reason to ease more in New Zealand.

Given that view, what’s the case for cutting rates further when inflation is nearly 3% and forecasts suggest it might get to 2% but more likely somewhere between 2-2.5%? The policy lags are long and variable – that’s what we are seeing now. Raising expectations for 2-2.75% interest rates seems risky given where inflation is now. There’s plenty of scope to ease more down the road should low inflation rates become a more tangible reality. And it is an inflation mandate in the end.

{kind=link}