{kind=link}

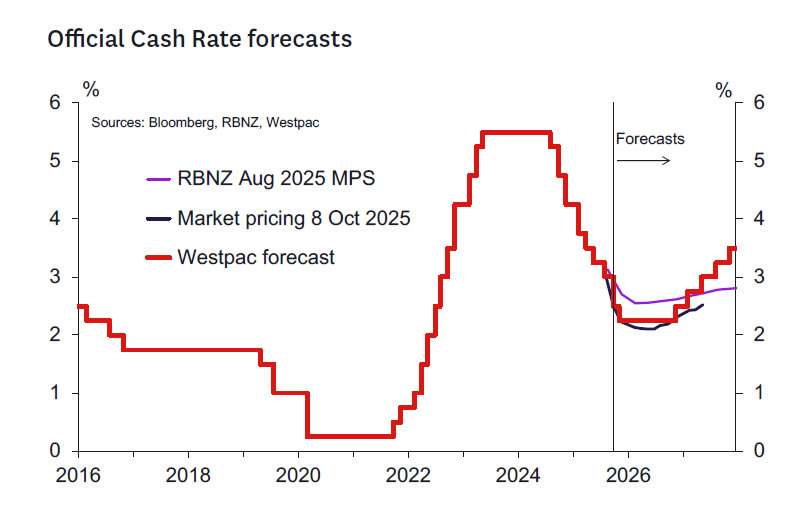

- As we expected, the RBNZ cut the OCR by 50bps to 2.50%.

- The decision was reached by consensus, with no vote required.

- The Bank’s commentary suggests further easing is likely in November reflecting significant excess capacity pushing down medium-term inflation.

- Westpac expects a 25bp cut at the 26 November MPS meeting. Further cuts beyond November remain a possibility but not our base case.

- Ahead of the 26 November meeting, the focus will be on the Q3 CPI and labour market reports, and high frequency indicators covering spending, activity and the housing market.

Today the RBNZ’s MPC announced that it had decided to lower the OCR by 50bps to 2.5%. The decision was made by consensus, so no vote was required. This means that the members who voted for a 25bp cut in August shifted to the 50bp camp this time while the new MPC member also shared their view. The MPC’s discussion canvassed two options: a 25bp cut and the 50bp cut.

The RBNZ emphasised signs of significant excess capacity in the economy that give them comfort that medium-term inflation will be well under control. The RBNZ marginally increased their estimate of the degree of excess capacity considering the weak Q2 GDP data but emphasised that a number of one-off or supplydriven factors also drove that weak result. Nevertheless, in line with their message from August, the MPC has little appetite for increased excess capacity – hence the relatively dovish reaction here – especially considering that the RBNZ’s appears to only expect that “…economic activity recovered modestly in the September quarter.”

The RBNZ was notably more positive on the global economic outlook than they have been in recent meetings. This makes sense given the run of more positive data and the general dialling down of concerns around the impact that US tariffs will have on global economic activity. Nevertheless, the RBNZ remains cautious about the global growth outlook next year.

Guidance for the future indicates that further easing seems likely in November – and perhaps beyond given the reference to future “reductions” in the OCR. The degree of guidance is equivocal, and hence further easing will be data dependent. But the language in the final sentence of the Media Release tells us a November easing is more likely than not.

“The Committee remains open to further reductions [our emphasis] in the OCR as required for inflation to settle sustainably near the 2 percent target mid-point in the medium term.”

With the market less than 50% priced for a 50bp easing today, and the RBNZ’s commentary also leaning dovish, the front end of the interest rate curve has rallied (1Y swap falling 12bps; 2Y swap falling 7bps). The NZ dollar has fallen about 1% to 0.5740 and NZD/AUD have fallen around 0.8% to 0.8750. At the time of writing, the market is pricing 27bps of easing for the 26 November meeting.

Westpac expects a 25bp rate cut at the 26 November meeting.

Given our expectations for the data flow over the coming weeks (see below) a further 25bp reduction in the OCR seems more likely than not at the 26 November meeting. This is consistent with our existing forecast.

It is possible that a case could be made for both no change or a 50bp cut in November, depending on the data flow between now and then. The no-change option would come into play should the short-term indicators improve markedly between now and late November. The RBNZ noted in the statement of record that they see the transmission mechanism as still working but needing time. They also noted that indicators of activity recovered “modestly” in the September quarter, which tells us that they would need to see a lot more stronger data before thinking about no change in the OCR in November. A much higher than expected Q3 CPI reading might also prompt a reassessment.

The 50bp option looks more interesting and seems a higher probability should data disappoint. There will be the issue of the long gap between the November and February meetings. If there remains some doubt about the economy’s forward momentum, it is possible that the MPC will elect to insure against the possibility of continued below-trend growth performance over the summer trading period.

Key quotes from the RBNZ’s commentary.

The press statement and record of meeting contained the following notable remarks:

- “The Committee remains open to further reductions in the OCR as required for inflation to settle sustainably near the 2 percent target midpoint in the medium term.”

- “While inflation is currently near the top of the band, spare capacity is consistent with headline inflation returning towards the target mid-point in the first half of 2026.”

- “There are upside and downside risks to the inflation outlook in New Zealand. Cautious behaviour by households and businesses could slow the economic recovery, reducing mediumterm inflation pressure. Alternatively, higher nearterm inflation could prove to be more persistent.”

- “…the Committee has revised its assessment of current spare capacity only marginally in response to new GDP and activity data, but note that the new data imply some downside risk.”

- “More timely indicators suggest that economic activity recovered modestly in the September quarter, but there remains significant spare capacity in the New Zealand economy.”

- “Slow growth in disposable incomes and house prices continue to weigh on economic activity, but lower interest rates are supporting a recovery in consumption.”

- “Aggregate global trade volumes and economic activity have so far proven resilient… However, growth expectations for 2026 have recovered to a lesser extent, with trading-partner growth expected to slow.”

Things to watch ahead of the 26 November meeting.

Looking ahead to the 26 November MPS, the key domestic economic indicators to watch are:

- The Q3 CPI (released 20 October) and October Selected Prices (17 November). We currently expect CPI inflation to rise to 3.1%y/y in Q3, compared to the RBNZ’s August forecast of 3.0%y/y. The October Selected Prices data will cast light on whether this is likely to be the peak.

- The Q3 labour market surveys (released 5 November). We currently forecast a broadly flat quarter for employment, leading the unemployment rate to nudge up to 5.3%. Our forecast is in line with the RBNZ’s August MPS forecast.

- The Q4 RBNZ Survey of Expectations (released 11 November), Q4 RBNZ Survey of Household Expectations (17 November) and the Q4 RBNZ Survey of Business Expectations (released 18 November). The particular emphasis will be on how inflation expectations are evolving with actual inflation close to 3%y/y.

In addition to these major quarterly releases, we expect the RBNZ will pay close attention to the developments in the BusinessNZ PMIs, consumer spending, the housing market and migration (out in mid-October and mid- November). The various activity and inflation indicators contained in the ANZ business and consumer confidence surveys (released late October) will also be of interest. Aside from domestic economic data, developments in US tariff policy and any clarity regarding how this is impacting the outlook for trading partner growth and inflation will also have an impact on the RBNZ’s deliberations at the November meeting. Movements in world prices for New Zealand’s key commodity exports, alongside movements in the exchange rate, will be important in gauging the extent to which international conditions are impacting the New Zealand economy.