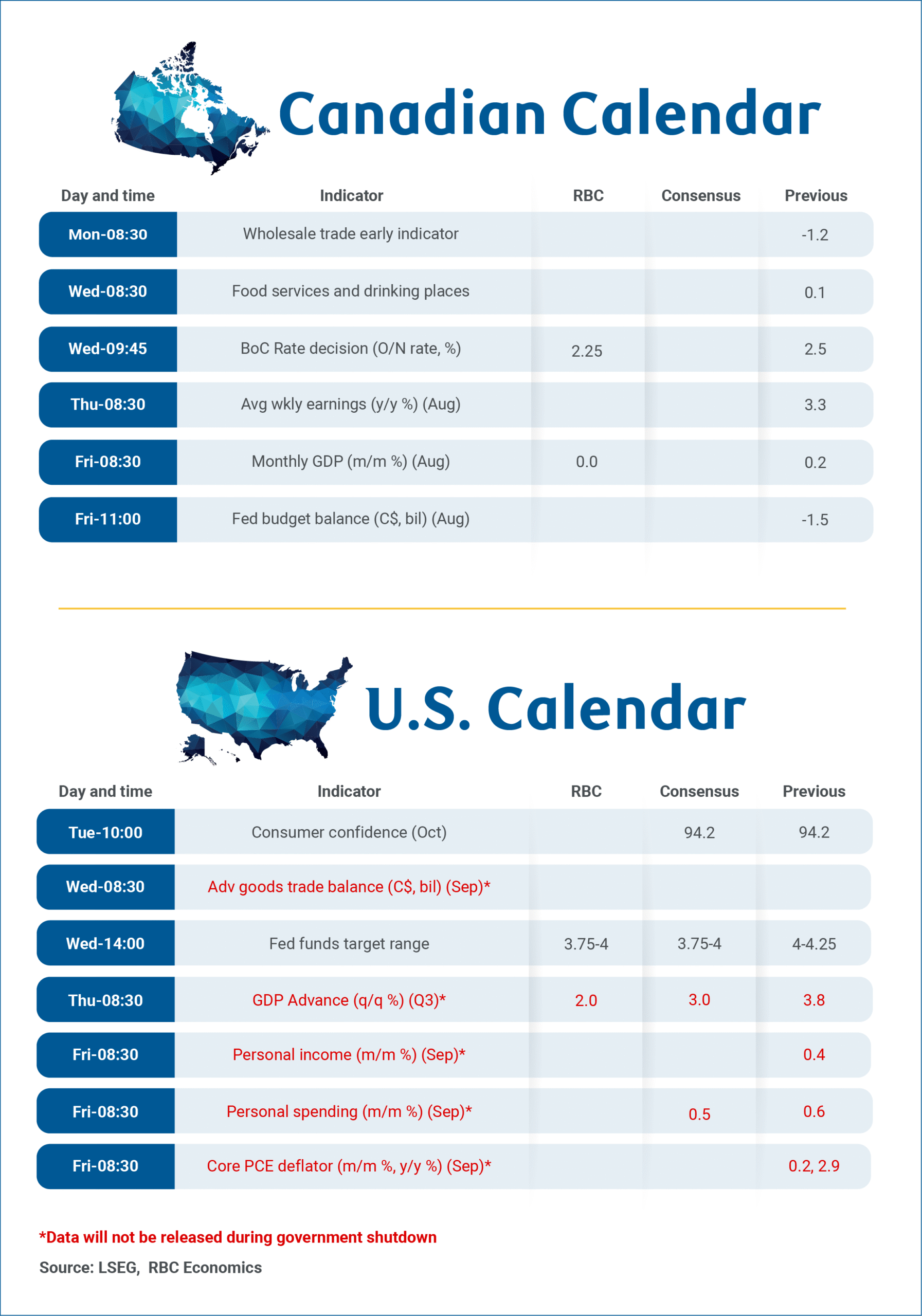

The U.S. Federal Reserve and Bank of Canada are both expected to cut policy rates on Wednesday, adding to 25 basis point reductions from each in September.

Another reduction from the U.S. Federal Reserve is widely expected – the Fed’s policy rate is starting from a higher, more restrictive, level than other central banks after cutting less since 2024, making it easier to justify additional reductions. And U.S. labour markets have been softening. The U.S. unemployment rate has edged higher with employment growth slowing to a stand-still since April – and soft alternative private sector data released during the U.S. government shutdown has been consistent with hiring demand remaining low.

The decision from the BoC is less straightforward. The Canadian central bank has already cut interest rates significantly more than the U.S. Fed in recent years and inflation is still running above the 2% inflation target.

Still, another 25 basis point rate reduction would leave the overnight rate at the bottom end, but not below, the BoC’s 2.25% to 3.25% estimated neutral range – in other words still at levels that would not be expected to significantly add to inflation pressures over time.

And we think it’s unlikely the BoC expected the one 25 basis point cut in September (the first reduction since March) would be enough to make a significant difference in the economy. The reduction last month came amid elevated trade uncertainty, “a weaker economy, and less upside risk to inflation,” according to the central bank.

Since September, data on growth and inflation have not surprised enough on the upside to derail another reduction this month. The unemployment rate at 7.1% in September was still elevated despite a rebound in employment counts. And, lower inflation expectations in the latest Business Outlook Survey are consistent with the BoC’s assessment of fading upside inflation risks.

This essentially means more room and flexibility for the central bank to have looser monetary policy. Still, we continue to expect that further cuts to the overnight rate to more stimulative levels would be increasingly difficult to justify when core inflation is running persistently above target, barring a significant further deterioration in growth that is not in our base case forecast.

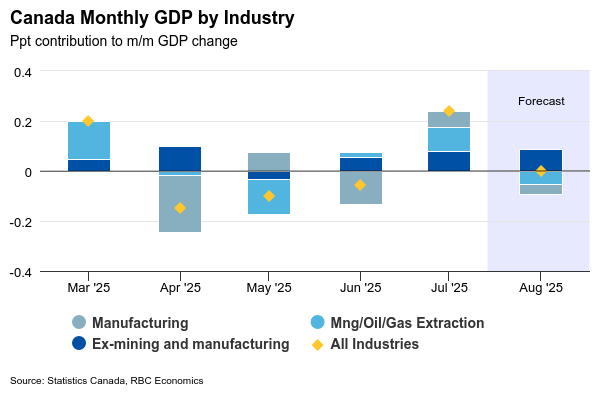

To be sure, U.S. tariffs are still hurting targeted sectors. We look for manufacturing and wholesale production to both contract in August gross domestic product data next Friday. Weakness in those sectors warrants a supportive policy response, but fiscal policy is more suited to respond to weakness in targeted sectors than blanket interest rate cuts . And the federal budget on Nov. 4 is expected to contain significant deficit spending to support growth in 2026 and beyond.

Week ahead data watch:

We expect August GDP held steady in Canada. Wholesale and manufacturing sales both declined after rising in July, and we expect a pullback in the mining sector to partially reverse a 1.4% jump in July. Other services industries likely posted growth, led by an 1.0% increase in retail sales. Early indicators for the advance GDP estimate for September are limited. Hours worked contracted 0.2% and the advance stimate of September retail sales was down 0.7%. But the advance manufacturing sales estimate bounced back 2.8%, which (if confirmed) would be the largest one month increase since February 2022.

{kind=link}