- Fed rate cut widely expected; dot plot and overall meeting rhetoric also matter.

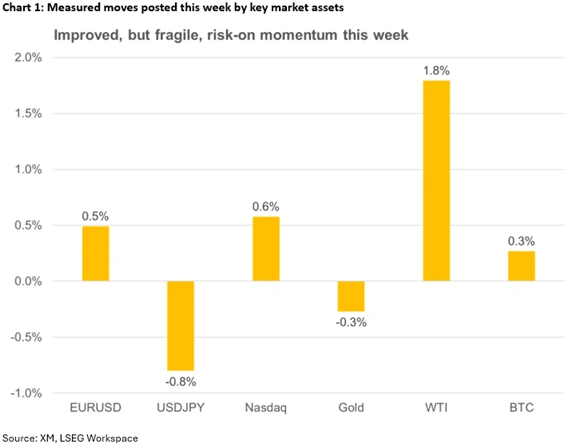

- Risk appetite is supported by Fed rate cut expectations; cryptos show signs of life.

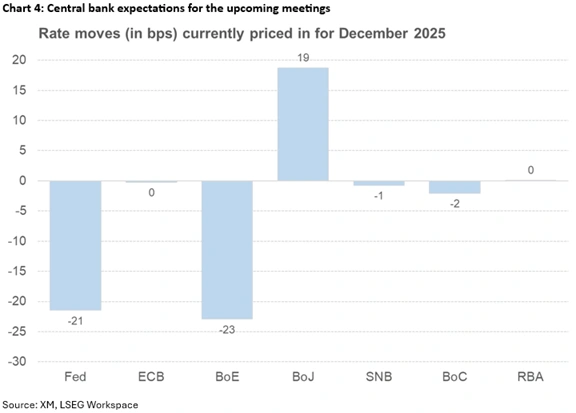

- RBA, BoC and SNB also meet; chances of surprises are relatively low.

- Dollar weakness could linger; both the aussie and the yen best positioned to gain further.

- Gold and oil eye Ukraine-Russia developments; a peace deal remains elusive.

Fed meeting in focus

With risk assets, including the ailing cryptocurrencies, remaining bid this week, mostly on the back of ballooning Fed rate cut expectations, the countdown to the most critical event until year-end is almost over. On Wednesday, at 19:00 GMT, the Fed will announce its rate decision, with the market appearing confident about another 25bps rate cut.

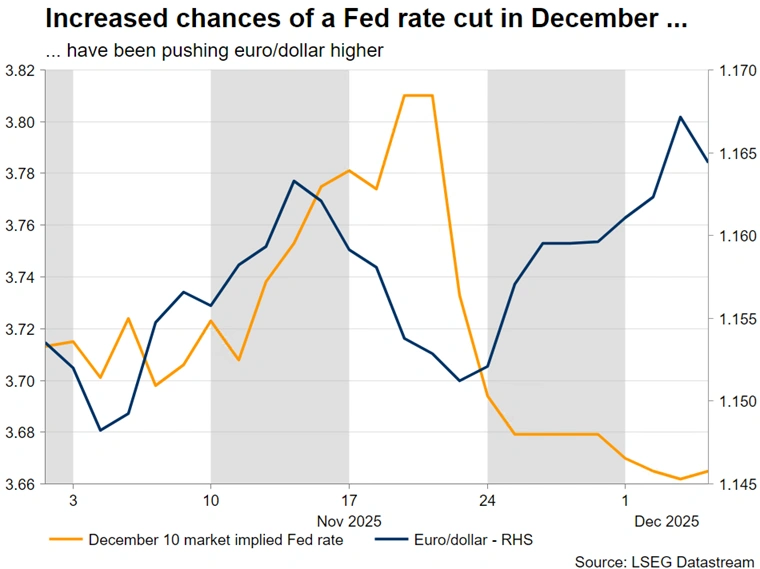

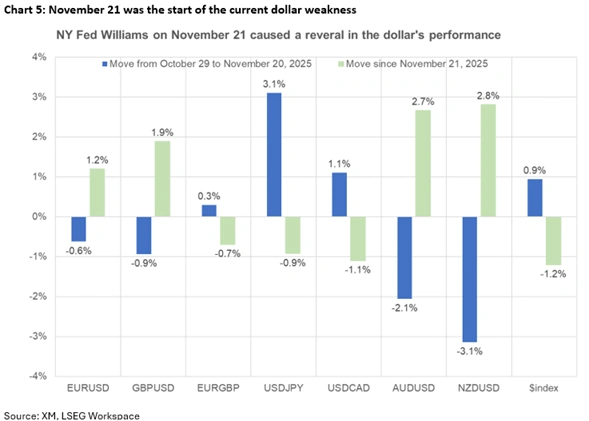

Aggressively hawkish Fedspeak, the minutes of the October meeting revealing a strong barrier to another cut, and the absence of clean data due to the federal government shutdown made the Fed rate cut look extremely unlikely during November. Everything changed, though, after New York Fed President Williams’ remarks on November 21, supported by the few data releases for November – particularly Wednesday’s weak ADP report – with the probability of the rate cut jumping to 86%.

On Wednesday, the focus will also be on the dot plot and overall meeting rhetoric. In September, the dot plot projected three rate cuts by the end of 2026, one more cut than in June. With the market currently pricing in 63bps of easing during 2026, there is a decent chance of the three rate cuts penciled for next year, making it the baseline scenario for the Fed.

While any dot plot adjustments might be easy to justify, Chair Powell will have some serious explaining to do if a rate cut is indeed announced, after stating in the October press conference that one should slow down when driving in the fog. Using the “weaker labour market” argument will probably be seen as a shallow justification, once again damaging the Fed’s low credibility.

Notably, these two factors – the dot plot and the meeting’s overall rhetoric – might prove less important for the 2026 policy outlook than usual, since Trump has probably picked Powell’s replacement. NEC Director Hassett appears to be the chosen one to lead the Fed into the future (of lower rates).

Markets have been preparing for the Fed meeting

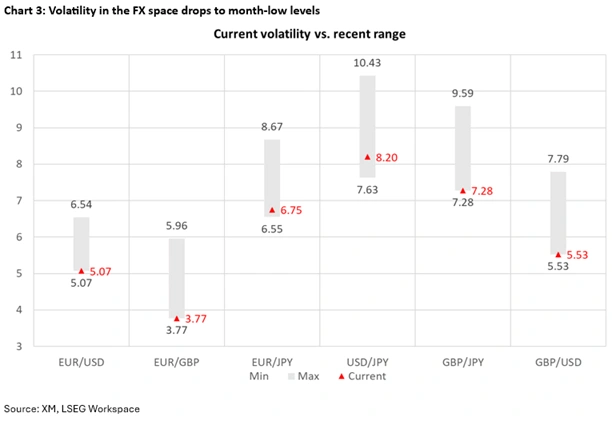

It has been a relatively quiet period, with one-month volatility easing across the board, but this could change dramatically next week. Confirmation of Fed rate cut expectations, along with balanced-to-dovish rhetoric and the dot plot pointing to three rate cuts, would support the current prevailing, but fragile, risk-on sentiment. Both equities and gold are expected to rally, with the dollar finding it difficult to reverse the current weakness. A strong move above 1.1700 in euro/dollar, resulting in a fresh higher high, would confirm the current short-term bullish trend.

The most acute market moves will probably take place in the unlikely scenario of the Fed keeping rates unchanged, a major upset to the current expectations. The initial aggressive risk-off reaction, with stocks tumbling and the US dollar strengthening, might only be tempered by an overly dovish Powell press conference and the dot plot projecting four rate cuts in 2026. Even then, markets might still feel betrayed, maintaining the bearish momentum. A drop below 1.1572 in euro/dollar would be important, but only a move below the key 1.1500 zone would negate the current short-term bullish trend.

Gold and oil also eye geopolitical developments

The Fed meeting is not the only game in town next week, as both gold and oil await developments on the Ukraine-Russia front. While the first round of meetings with Trump’s representatives was characterized as fruitful, sticky points – particularly the frozen Russian assets and the occupied eastern Ukraine regions – could derail the current effort.

Gold continues to hover near $4,200, with a dovish Fed meeting and a high-profile breakdown in the Ukraine-Russia negotiations creating a dual tailwind that could drive the precious metal towards the all-time high of $4,381.

Similarly, despite the confirmation of the current production quotas until end-March 2026 by the OPEC+ alliance, oil has been unable to rally meaningfully above a key downward sloping trendline. Positive progress, in the form of preparations for a trilateral meeting between US, Russian and Ukrainian leaders, could push oil towards the October trough of $56.36, close to the four-year low of $55.60.

How hawkish could the RBA sound?

Following three rate cuts during 2025, the chances of a dovish surprise on Tuesday are almost zero. Inflation has been stubbornly high, with the October CPI edging higher to 3.8%, and the trimmed mean following suit. Despite the weaker Q3 GDP report, partly due to softer consumption, RBA Governor Bullock is focused on the elevated inflationary pressures and the tightness in the labour market.

Externally, despite the numerous support programmes and the upbeat GDP projections for 2026, the world’s second largest economy continues to face deflation. Improved economic momentum in China would benefit Australia, potentially adding pressure for a more restrictive stance ahead.

The divergence in rhetoric between the Fed and RBA has been playing a pivotal role in the aussie/US dollar rally towards the 0.6610 zone. Confirmation of this central bank divergence next week could fuel a move towards the 0.6680 region, particularly if Fed Chair Powell opens the door to a January 2026 rate cut. That said, a more balanced message from Bullock et al. might result in a decline towards the 0.6550 area.

The BoC is expected to keep it powder dry

Following 100bps of easing so far in 2025, the BoC is expected to stand pat on Wednesday. However, excluding the surprisingly strong Q3 GDP report, the positive news is scarce, as seen in this week’s S&P Global PMI surveys. But the main headwind for the Canadian economy remains the stalled negotiations with the US over tariffs, mostly regarding products currently not covered by the USMCA agreement.

With additional tariffs hanging over their heads like Damocles’ sword, Governor Macklem et al. will probably remain slightly dovish and repeat their readiness to respond if the outlook changes dramatically. Unsurprisingly, dollar/loonie has been trading sideways, mostly due to the greenback’s weakness. The combination of a dovish Fed meeting and a more balanced BoC rhetoric could open the door to a decline towards the late-October low of 1.3887.

Unchanged SNB set to remain vigilant

The SNB is treading on thin ice as consumer price inflation continues to flirt with negative territory. The negative annual growth in PPI, following an especially weak Q3 GDP report, is seriously clouding the outlook, increasing the pressure for a dovish tilt on Thursday.

That said, not everything is bleak, as the recent PMI surveys and October retail sales managed to produce upside surprises. More importantly, the US and Switzerland have reached a trade agreement, with the US rate dropping from 39% to 15% and Switzerland committing to a $200bn investment until end-2028.

SNB President Schleger has recently repeated the high bar for negative rates, hoping that the SNB’s projection for inflation acceleration in 2026 will be confirmed. Notably, markets have not been indifferent to the negative rate remarks, with the Swiss franc stabilizing lately against both the euro and the dollar. Pending a dovish tilt on Thursday, the Franc’s short-term reaction will mostly depend on the dollar’s performance. Interestingly, the convergence of simple moving averages in dollar/franc are pointing to increased volatility ahead.

Is the BoJ on the cusp of the much-anticipated rate hike?

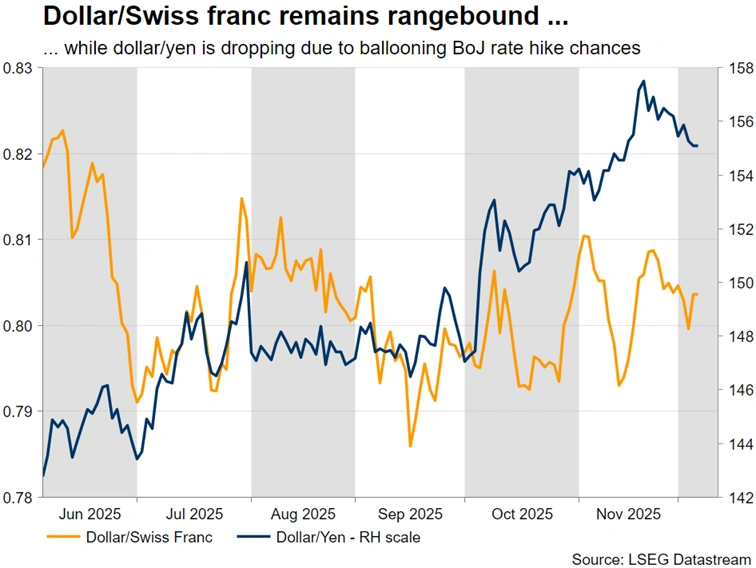

Since mid-November, there has been a hawkish tilt in BoJ commentary, with the latest reports suggesting that the government has agreed to the BoJ rise. Armed with elevated inflation and some initial positive wage growth demands, the BoJ is ready to take a leap of faith, hoping that this move won’t backfire down the line. Dollar/yen continues to decline, also taking advantage of the greenback’s weakness, with the first support expected in the 153.20-154.50 area.

{kind=link}