- US CPI and PCE inflation reports both due as Fed cut bets scaled back.

- Geopolitical turmoil keeps investors on edge as energy prices spike.

- Canadian employment, UK GDP and Japanese data also on the agenda.

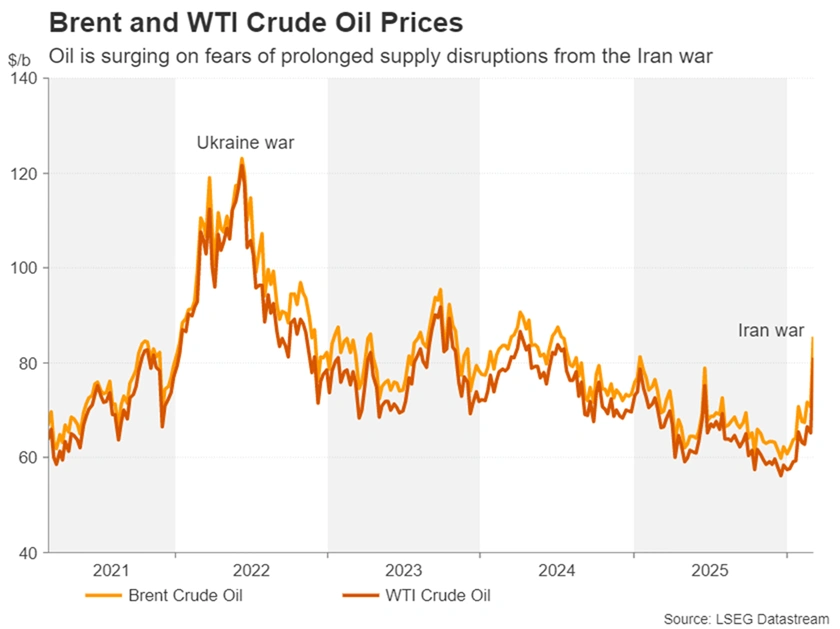

World grapples with new energy threat

Four years into the Ukraine war and still reeling from the ensuing shock to energy prices, major economies are facing the real threat of a fresh energy crisis, as the war in the Middle East roils markets. For the US economy, which is showing renewed signs of momentum and where inflation has been moderating only slowly, Fed rate-cut expectations had already been pared back before the war broke out.

Following the escalation, which has not only embroiled neighbouring countries, inflicting damage on their energy facilities or forcing their closure, but has also effectively shut the Strait of Hormuz to vessels, potentially disrupting about 20% of the world’s oil and gas supply.

All this cannot be good for the inflation outlook, as oil futures have soared by around 20% and European gas futures have skyrocketed by more than 50%. The United States is somewhat more immune to a direct energy shock from the Middle East turmoil, but the situation nonetheless creates a fresh headache for the Fed, which is unhappy about the slow progress of inflation returning to its 2% target.

Year-end rate-cut expectations have fallen to around 40 basis points from 60 bps a few weeks ago, while the next move is not fully priced in until September.

Spotlight on US inflation as Fed cut bets recede

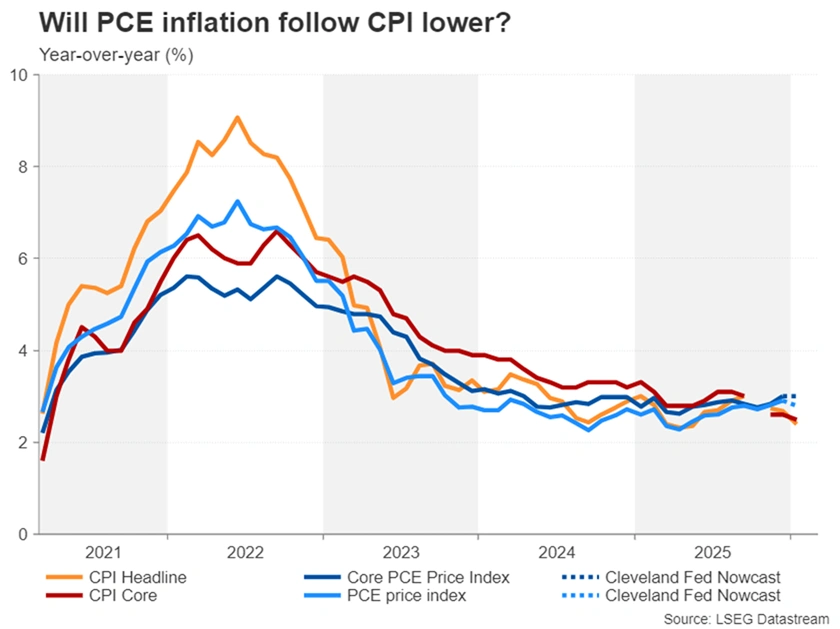

Next week’s data will be crucial in further shaping Fed easing expectations, as both the CPI (Wednesday) and PCE (Friday) reports are incoming. Although some policymakers appear comfortable with the idea of a long pause, less hawkish FOMC members could be persuaded to back a rate cut as early as June, if not sooner.

Headline CPI fell to 2.4% y/y in January, while the core rate moderated to 2.5%. Both are expected to have stayed unchanged in February. What might prove more market-moving, however, is the PCE data, as it’s watched more closely by the Fed, and unlike the CPI numbers, it remains stuck near 3.0%.

After edging up to 2.9% in December, headline PCE is estimated to have dropped to 2.8% in January according to the Cleveland Fed’s Nowcast model. But the more important core PCE price index is forecast to have held steady at 3.0%.

Whilst the PCE figures may not be as up to date as the CPI ones, any upside surprises during the current backdrop of elevated inflation risks could deal a further blow to Fed rate cut bets, increasing the US dollar’s short-term bullishness.

Investors will also be keeping an eye on the other releases included in the PCE report, namely, the personal income and consumption stats. Moreover, the week as a whole will be a data-heavy one, with a batch of housing market indicators on Tuesday and Thursday, as well as durable goods orders, the JOLTS job openings and the University of Michigan’s preliminary consumer sentiment survey, all due on Friday.

Yen loses out to Dollar and Franc

The Japanese yen has seen a mixed response to the major geopolitical flare-up, appreciating against most major currencies but falling against some, like the US dollar. Investors have favoured the dollar over other safe havens during the Iran crisis, even gold. The Swiss franc was also initially a strong beneficiary of safe-haven flows but it got knocked back when the Swiss National Bank issued a rate intervention warning.

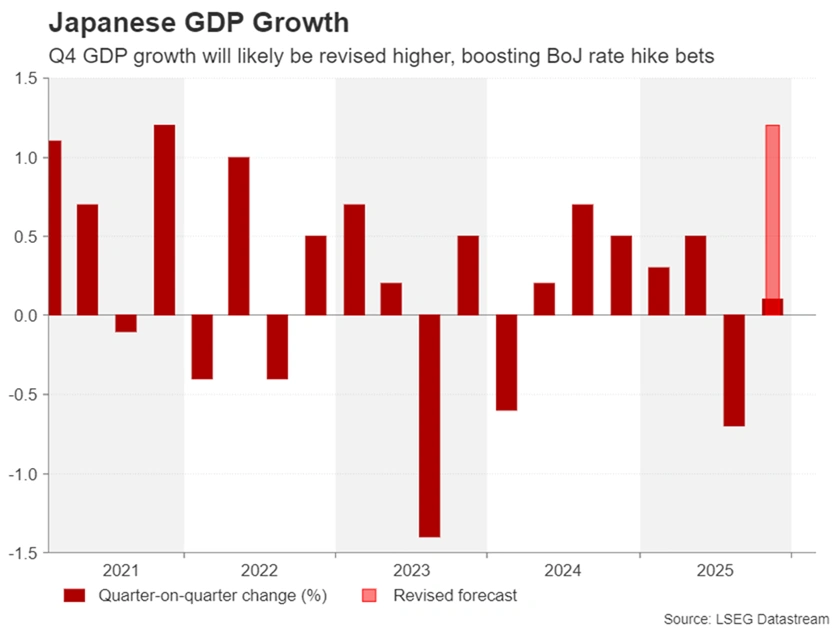

However, this doesn’t appear to have redirected any safety flows to the yen, as traders struggle to make sense of Bank of Japan communication, with the Middle East conflict complicating the policy direction even more, as it raises the prospect of stagflation. Governor Ueda remains uncommitted to a timeline for raising interest rates, while the government continues to question the need for further tightening.

Still, the BoJ has a history of catching markets off guard, and although investors see little chance of a hike before the June meeting, an earlier move cannot be ruled out, particularly if the wage and consumption data surprise to the upside.

Hence, next week’s releases on wage growth (Monday), household spending (Tuesday), revised GDP estimates (Tuesday) and corporate goods prices (Wednesday), will be monitored. A more imminent risk, though, for the yen, is a possible intervention by Japanese authorities, as the dollar hovers near the 158–160-yen intervention zone.

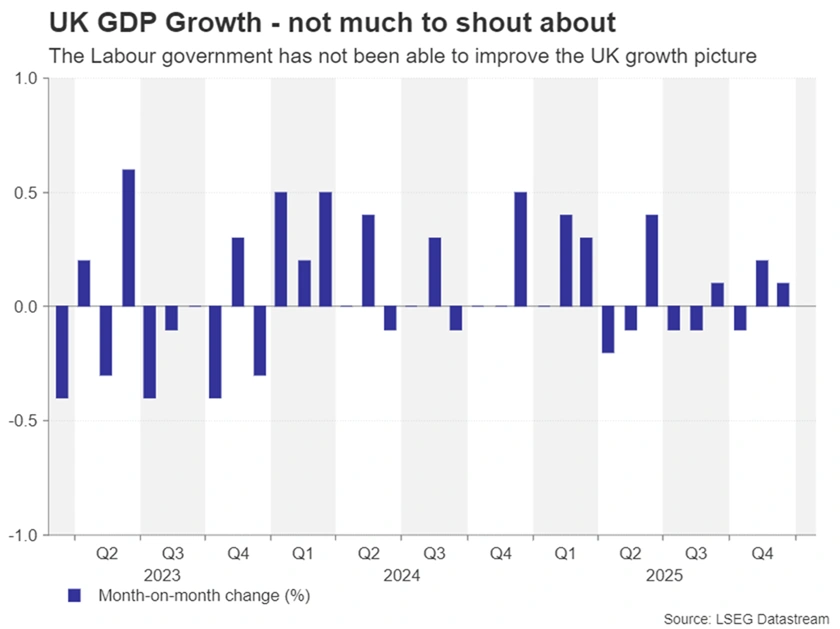

Pound subdued even as BoE rate cut priced out

The UK economy has barely grown since last summer as the government’s tax increases on businesses and the uncertainty generated by Chancellor Rachel Reeves’ chaotic budget has hit hiring and investment. The sluggish performance has kept the Bank of England on an easing path even as inflation re-accelerated during 2025.

The BoE’s main concern is the upward trending unemployment rate, which hit a five-year high in December. Nevertheless, with inflation decelerating only slowly and at 3.0%, still well above the BoE’s 2.0% target, the current developments in the Middle East could easily blow any rate cut plans off course.

Investors have already sharply lowered their expectations of a 25-bps reduction at the next meeting to less than 15% from over 80% and simultaneously priced out a second 25-bps cut.

However, if the upcoming releases, all due on Friday, disappoint, easing expectations would likely be bolstered, adding to sterling’s woes amid a resurgent dollar. The slew of data will include monthly GDP readings for January, as well as industrial production and trade figures.

Loonie eyes jobs data amid Oil boost

In Canada, employment numbers will likely attract some attention on Friday for the Canadian dollar, which has been lifted from the jump in oil prices amid fears of a prolonged disruption to supply from Iran’s counter attacks to the US- and Israel-led strikes.

Canada’s labour market shed jobs in January so a rebound in February would add more fuel to the loonie’s engines against other currencies apart from the dollar. However, a weak jobs report could prompt a pullback.

On the whole, though, geopolitical events will likely remain in the driver’s seat for the loonie as the Bank of Canada is not expected to tweak its policy settings anytime soon.

Aussie rally loses steam, might find support in China data

The Australian dollar is headed for its first weekly loss in seven weeks against the greenback, as risk sentiment ebbs on the back of the Iran conflict. However, Australia also faces fresh tariff uncertainty following the US Supreme Court ruling that President Trump’s reciprocal levies were illegal. Australian exports to the US look set to be charged 15% duties instead of 10%.

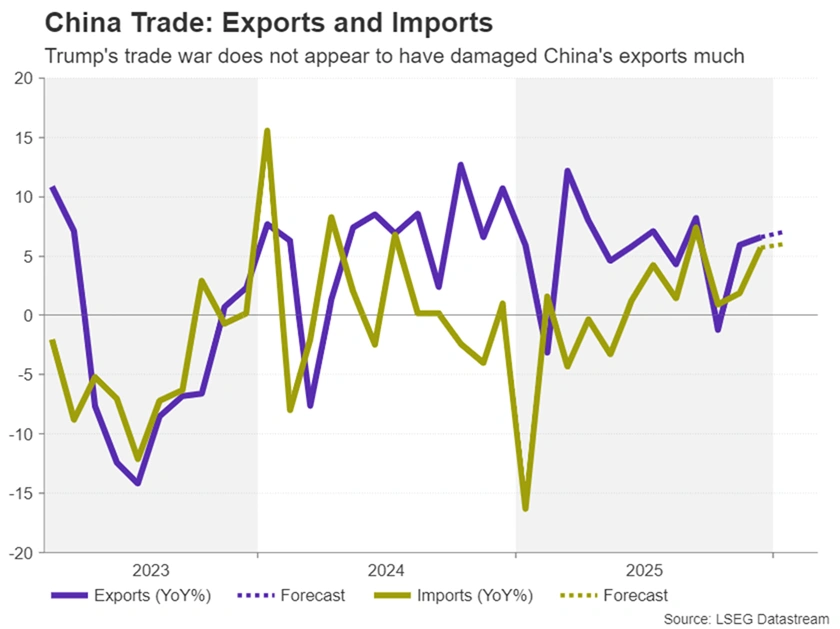

Yet, the Reserve Bank of Australia is still expected to hike rates again later this year, especially if higher energy prices push up inflation. But in the short term, the aussie might need a boost from other sources, which may come in the form of Chinese indicators.

Trade data out on Tuesday will show whether or not the rise in exports to non-US countries continues to outstrip the decline in shipments to America in February. Moreover, China potentially stands to gain from the Supreme Court decision, with its effective tariff level falling from 20% to the new global rate of 15%.

A day earlier, the consumer and producer price indices for February will also be watched. Stronger-than-forecast readings could lend some support to the Aussie.

{kind=link}