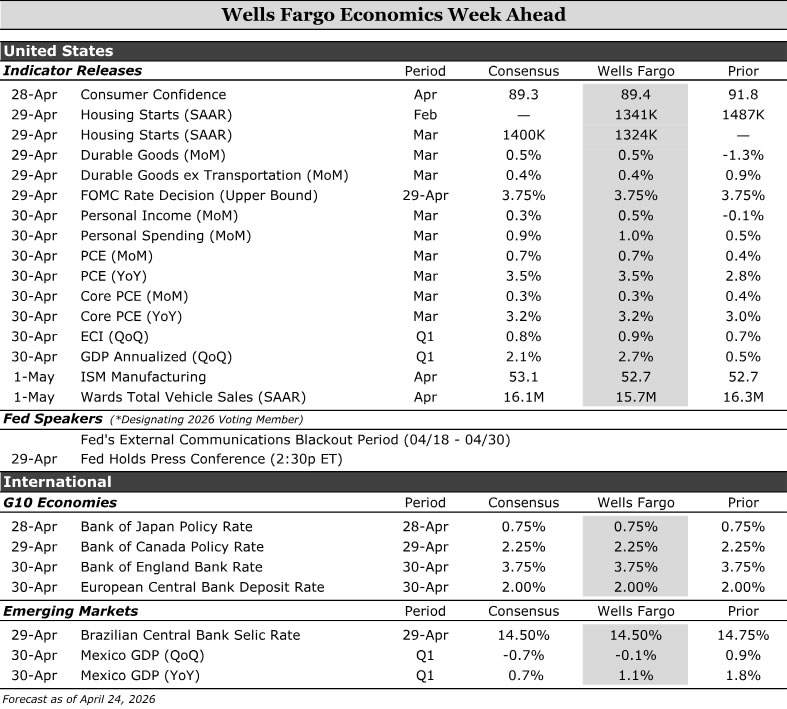

United States:

- FOMC (Wednesday), Personal Income & Spending (Thursday)

G10 Economies:

- Bank of Japan (Tuesday), Bank of Canada (Wednesday), Bank of England (Thursday), European Central Bank (Thursday)

Emerging Markets:

- Brazilian Central Bank (Wednesday), Mexico GDP (Thursday)

U.S. Week Ahead

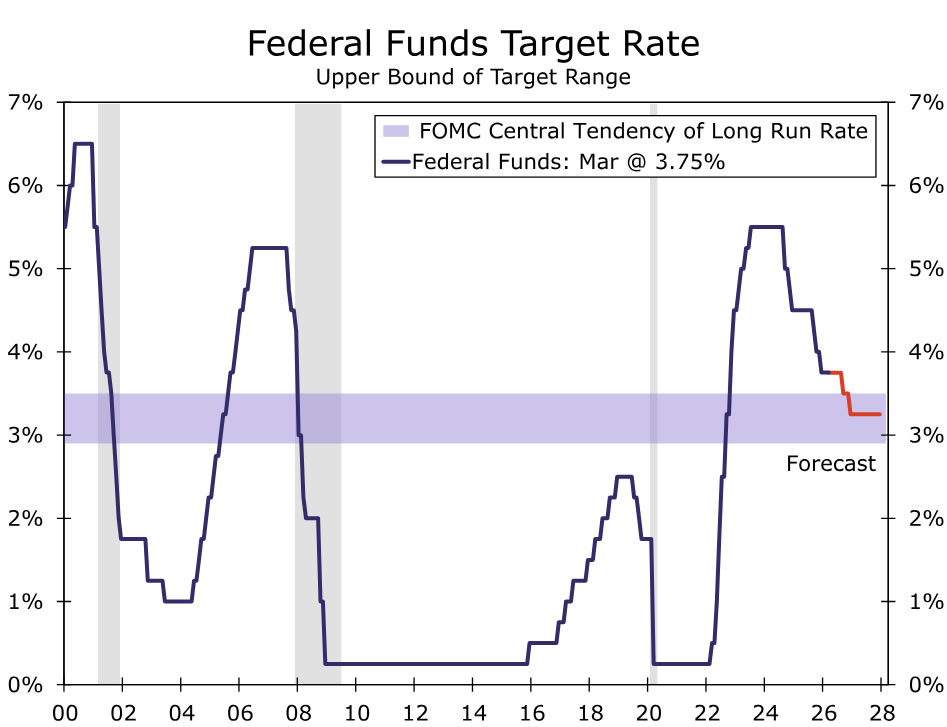

FOMC • Wednesday

The Fed’s dual mandate remains in tension. Recent data point to PCE inflation remaining stuck around 3%, with the energy shock from the conflict in the Middle East expected to strengthen headline inflation in the near term. Meanwhile, the labor market continues to lose momentum. First‑quarter job growth was distorted by strikes and volatile weather, and we expect hiring to slow further in coming months as renewed geopolitical uncertainty restrains labor demand. Against this backdrop, we expect the Fed to remain patient and hold the federal funds target rate steady at next week’s meeting.

The Committee is likely to emphasize optionality in its statement. We expect it to note that higher energy costs are keeping inflation elevated and to soften forward guidance, replacing language around “the extent and timing of additional adjustments” with more open‑ended phrasing that references “future adjustments” to the policy rate.

Chair Powell is also likely to stress in his press conference that policy is well positioned to await further data. We expect him to highlight heightened uncertainty stemming from the Iran conflict and its implications for both sides of the dual mandate, while reiterating that the Committee is prepared to adjust policy as needed to balance these risks. Our forecast continues to call for two 25 bps rate cuts this year, in September and December.

Personal Income & Spending • Thursday

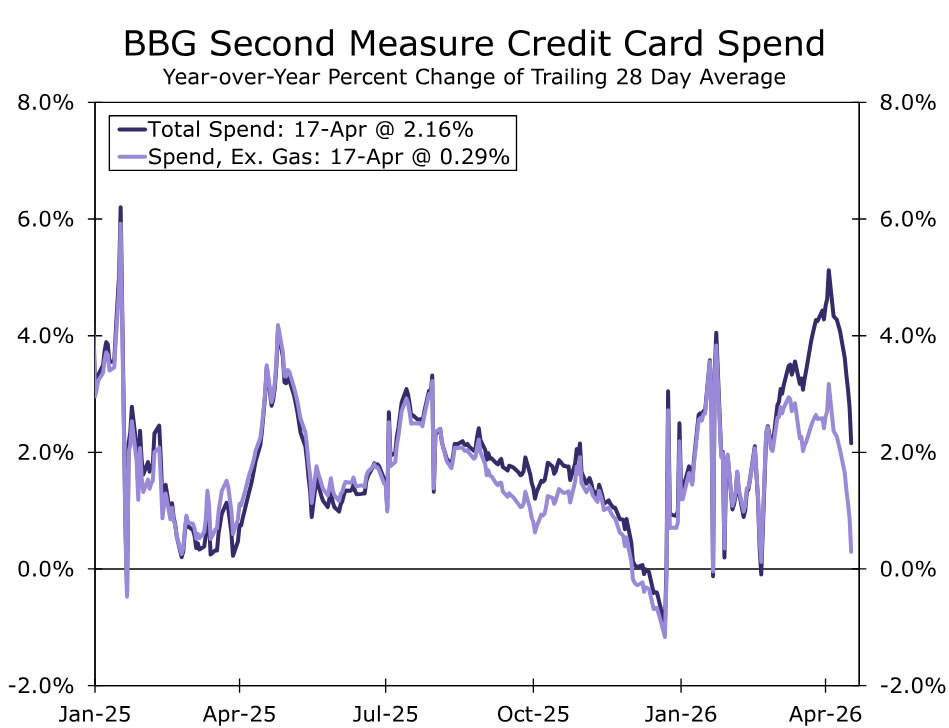

Consumer spending has remained broadly resilient in the immediate aftermath of the Iran conflict, though early signs suggest higher gas prices are beginning to weigh on demand. Higher energy costs will drive a 0.7% gain in the March PCE deflator, lifting nominal spending in the near term. On a real basis, we estimate consumption rose a more modest 0.3% last month. Core retail sales held up in March, and high‑frequency Bloomberg credit card data point to continued spending into early April. More recent estimates, however, suggest a pullback in spending outside of gasoline (chart).

That resilience is increasingly being sustained by offsets rather than improving fundamentals. We expect personal income rose just 0.5% in March, with elevated inflation eroding household purchasing power amid a cooling labor market. While households have so far absorbed higher fuel costs, the mid‑April slowdown in credit card spending may signal early trade‑down behavior. As we parse the broader March spending data, we will be watching closely for additional softening in discretionary categories. Overall, we expect spending to continue, but at a slower pace, as higher tax refunds and after‑tax income have largely offset—but not eliminated—the initial hit from higher prices.

G10 Week Ahead

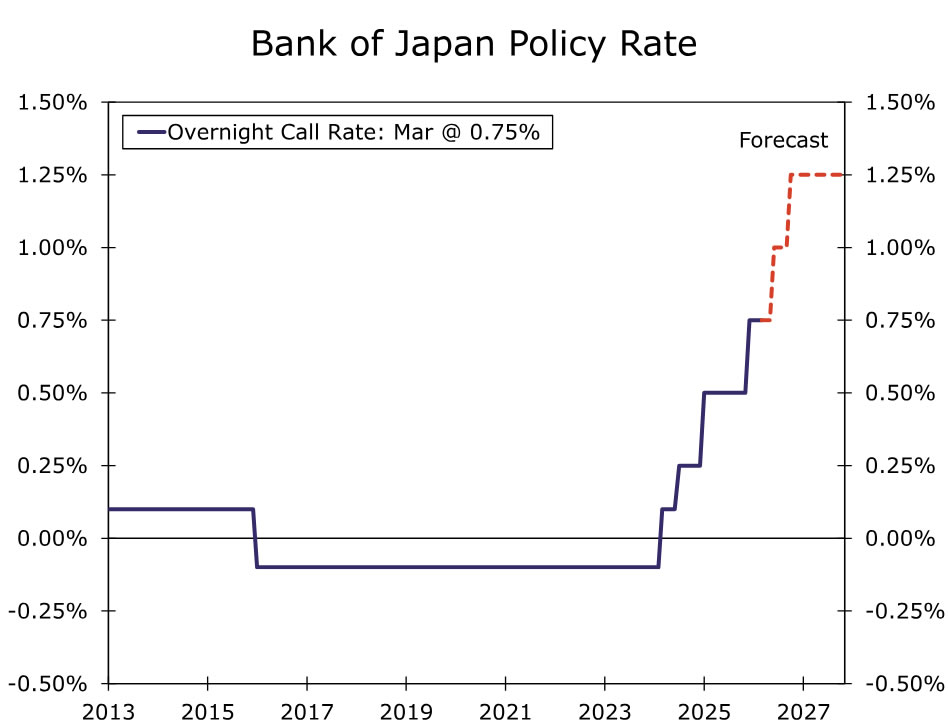

Bank of Japan Policy Rate • Tuesday

The Bank of Japan (BoJ) enters the April 27-28 meeting with a tightening bias intact, even as growth risks have risen. Headline CPI softness reflects energy subsidies and base effects, while underlying “core‑core” inflation remains above target and inflation expectations have firmed. Wage dynamics are the decisive input, with another year of 5%+ Shunto outcomes reinforcing the credibility of a wage‑price cycle. The macro tension is clear: growth momentum is increasingly fragile and exposed to the energy shock, but not weak enough to restrain policy on its own. As a result, although the April meeting is technically live, a hold with hawkish‑leaning guidance remains the cleanest outcome if policymakers prefer additional confirmation on oil prices, FX and financial conditions.

The policy direction rather than timing is the key signal, in our view. The BoJ’s revised reaction function explicitly tolerates weaker growth so long as inflation persistence and wage gains remain intact. Our base case remains for a Q2 hike (June), followed by at least one additional increase later in 2026, taking the policy rate to around 1.25% by year‑end. Even at that level, policy would remain only mildly restrictive relative to estimates of neutral. Risks to the outlook are skewed toward higher rates if yen weakness persists or energy prices remain elevated, while a durable de‑escalation in the Middle East represents the main downside risk to the tightening path.

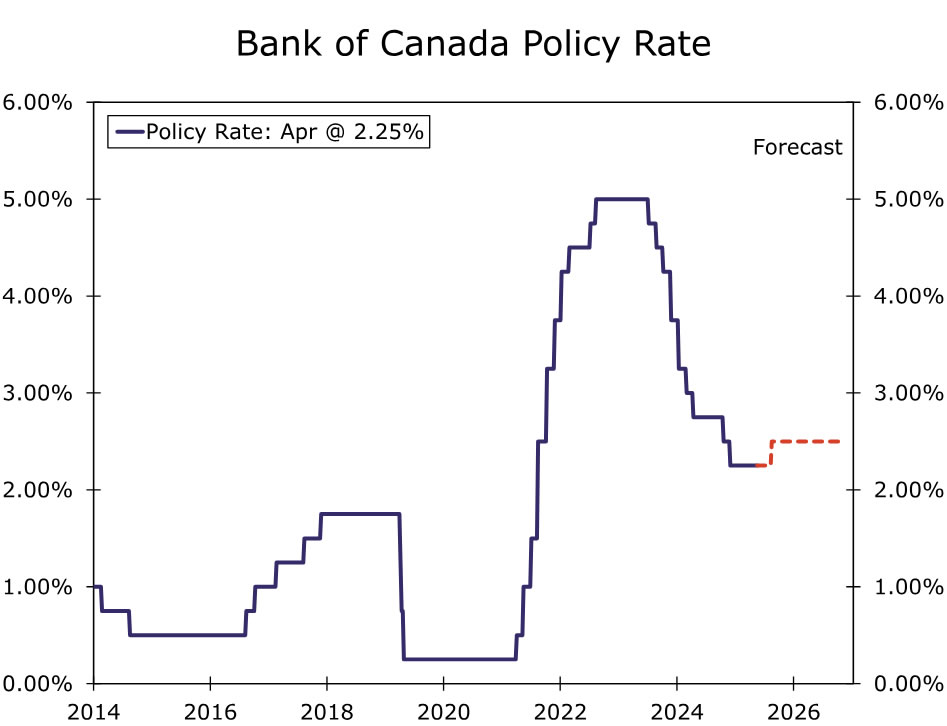

Bank of Canada Policy Rate • Wednesday

We expect the Bank of Canada (BoC) to hold rates at 2.25% in April, with the meeting serving as a reaction function update rather than a decision point. Growth remains soft but resilient, with labor markets stabilizing rather than deteriorating and higher energy prices improving the nominal growth mix despite ongoing trade and USMCA uncertainty. April communications should be less dovish, emphasizing two‑sided risks while making clear that the bar for renewed rate cuts has risen materially.

The dominant shift is on inflation, not growth. The energy shock has reintroduced risks around headline persistence and expectations, even as the Bank avoids overreacting to what may still be a relative price shock. Our baseline is for rates to remain on hold through mid‑year, with a 25 bps hike in July. By that time, the BoC would have received better data on how the shock is propagating through the economy, the passing of the USMCA July 1 deadline and another update to its Monetary Policy Report. We continue to believe that further rate hikes may be entertained in H2 if energy prices stay elevated for longer, inflation expectations firm and price pressures broaden.

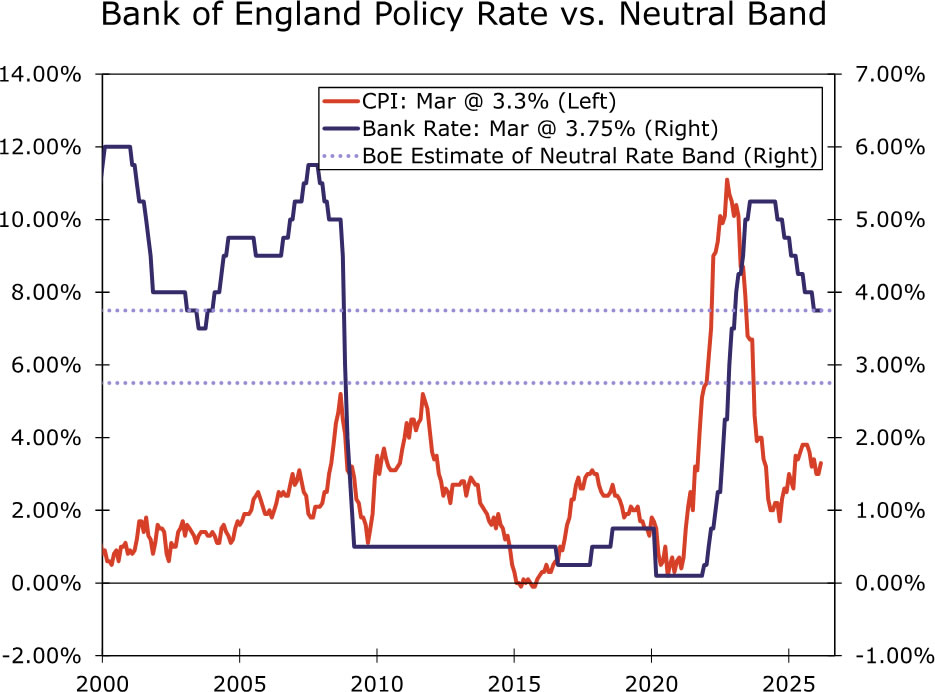

Bank of England Bank Rate • Thursday

When Bank of England (BoE) policymakers meet next week, we expect that they will keep the Bank Rate on hold at 3.75%. The Monetary Policy Committee’s guidance is likely to continue emphasis on optionality and data dependence, particularly if second-round effects become more pronounced. We expect growth projections to be revised lower and near-term inflation forecasts higher as the energy supply shock reintroduces upside risks to headline persistence, with longer-horizon forecasts largely unchanged. It would take a notably sharp upgrade to the growth outlook or medium-term inflation forecasts well above the 2% target to shift our view toward a tightening cycle this year.

For now, the bar for a rate hike remains high. Wages are still soft, and while the unemployment rate surprised to the downside at 4.9% (vs 5.2%), the drop largely reflected lower participation rather than a meaningful pickup in employment. March inflation came in high but reflected the direct shock of higher fuel prices rather than anything out of the ordinary. And even though April PMIs surprised to the upside, anecdotal evidence suggests the stronger pace of expansion partly reflects a short-term boost from firms and households pulling purchases forward amid feared price rises and war-related supply shortages. This pace is unlikely to be sustained if price levels remain high. We therefore see the BoE on hold in 2026, particularly with the policy rate already restrictive and at the top of the bank’s estimated 2.75%-3.75% neutral range. That said, risks are skewed to the hikes, especially if services inflation continues to accelerate and feed through into wages.

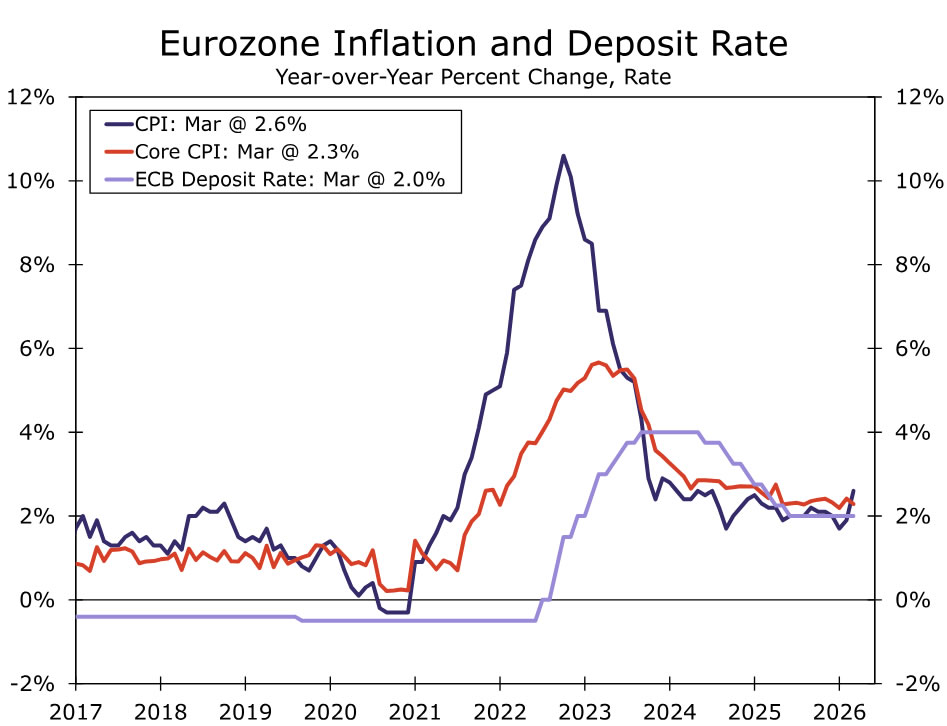

European Central Bank Deposit Rate • Thursday

The European Central Bank (ECB) is expected to hold rates at 2.00% at its meeting next week, but the policy debate has turned meaningfully more hawkish against a deteriorating macro mix. Euro area growth momentum has softened materially since the start of the year, with activity indicators now consistent with near stall speed and services increasingly bearing the brunt of the slowdown. At the same time, the energy shock linked to the Middle East conflict has reintroduced persistent inflation risks, with higher oil and gas prices pushing up headline inflation, tightening supply conditions and raising the risk of second round effects through services prices, wages and FX pass‑through. This has shifted the ECB’s characterization of the outlook toward a clearly stagflationary configuration, weaker growth but firmer and more uncertain inflation dynamics.

Against this backdrop, the ECB has moved away from any easing bias and is operating with a lower bar to tightening. March projections marked a clear regime change, with 2026 inflation revised sharply higher, core inflation expected to remain above target through the forecast horizon and policymakers explicitly emphasizing upside inflation asymmetry and credibility risks. While April is likely to be a holding and signaling meeting rather than a decision point, the tone should continue to validate that hikes are live as early as June. Our base case remains for two 25 bps rate hikes this year, beginning in Q2 and taking the deposit rate to 2.50% by end‑2026, with risks skewed toward earlier or additional tightening if energy prices stay elevated or inflation expectations show signs of drifting higher.

EM Week Ahead

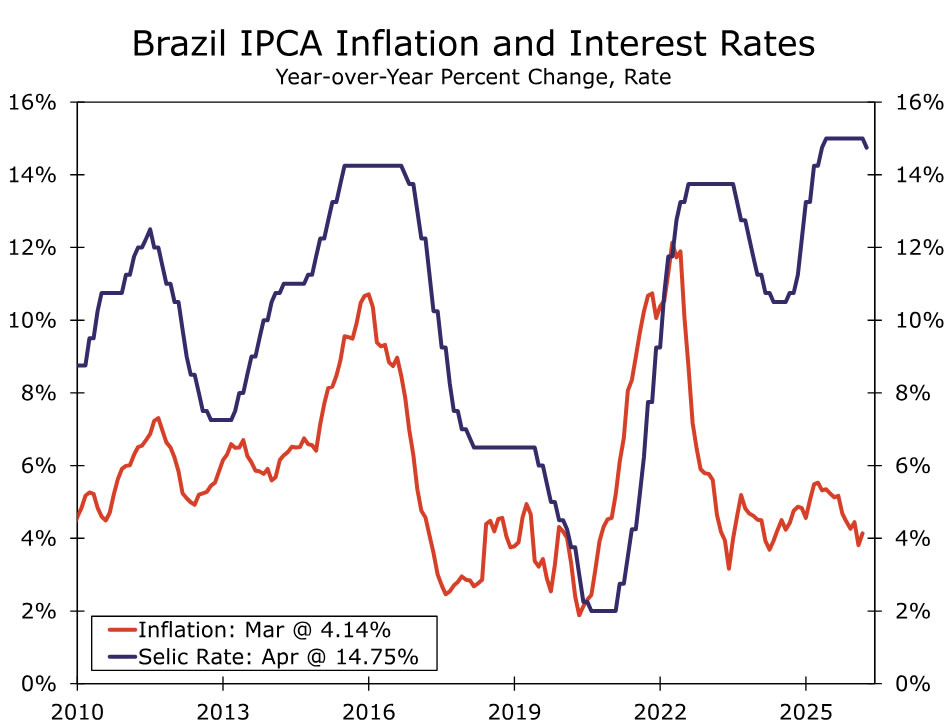

Brazilian Central Bank Selic Rate • Wednesday

The Banco Central do Brasil (BCB) is likely to cut the Selic by 25 bps next week to 14.50% under our baseline. A strong IPCA‑15 inflation print on Tuesday (Apr 28) could still keep the BCB on hold. Either way, the easing cycle has become shallower, more intermittent, and more data-dependent than it appeared back in February.

Our baseline remains for the BCB to deliver 25 bp cuts at each remaining meeting in 2026, bringing the policy rate to 13.25% by year‑end. That said, the risk is clearly skewed toward fewer cuts, as the BCB assesses elevated external and domestic inflation risks. June stands out as a likely pause point, giving policymakers time to evaluate fuel price pass‑through, indirect effects and the stability of inflation expectations. Political risk also rises into Q3, with the pre‑election cycle likely to weigh on expectations amid renewed populist pressures. As such, we see meaningful downside risk to the number of cuts delivered this year.

The macro backdrop argues for caution. March IPCA marked the first clear pass‑through from the energy shock, with fuel and food driving a broad‑based acceleration. Inflation expectations have de‑anchored further, with breakevens rising toward 6%. The inflation outlook for the remainder of 2026 remains highly dependent on the scale and duration of the supply shock. Our baseline has inflation rising to around 4.3% by year‑end, with upside risks as pressure broadens from energy into fertilizers and food. Government subsidies may dampen, but are unlikely to fully offset, pass‑through.

On activity, data have been resilient so far, with some support from higher net energy exports. However, the need to maintain elevated real rates to re‑anchor inflation expectations will continue to weigh on the growth outlook as the year progresses. On fiscal policy, fuel tax exemptions and subsidies add execution risk in an election year. While these measures are officially framed as fiscal neutral, their credibility depends heavily on oil prices and political discipline. Absent structural adjustment, ongoing expenditure pressures and political constraints imply persistent fiscal risk premia, which in turn limit the scope for sustained monetary easing.

Mexico GDP • Thursday

We expect Mexico’s preliminary Q1 GDP reading to print -0.1% quarter-over-quarter from 0.9% in Q4, as early-2026 momentum fades across key domestic drivers. The year-over-year GDP is expected to decline to around 1.1% from 1.8% in Q4. After a strong January, private consumption lost steam in February, with retail sales contracting on the month and slowing sharply year-over-year, led by weakness in fuel, automobiles and food categories. We expect this softening in consumer demand to persist in March in light of energy price shocks. Although industrial activity rebounded on a month-over-month basis in February, it remains in a clear year-over-year contraction amid broad-based manufacturing weakness and elevated trade-related uncertainty. Investment continues to be a material drag, with gross fixed investment still contracting in both month-over-month and year-over-year, reflecting a fragile business climate, policy uncertainty and delayed capex amid USMCA renegotiation risks. Overall, Q1 growth looks below trend and materially weaker than late 2025, with downside risks if March data fail to stabilize. We continue to expect Banxico to remain dovish given the sluggish growth outlook and take advantage of the narrow window on inflation to cut the policy rate one last time in Q2.

{kind=link}