Canadian Highlights

- March CPI came in a touch softer than expected, with headline inflation jumping to 2.4% on higher gasoline prices but shorter-term core measures are still, on average, running below 2%.

- The first quarter BoC Business Outlook Survey signaled improving pre-war sentiment, but noted rising input costs and some upward drift in inflation expectations since the onset of the conflict.

- With war-related uncertainty elevated and inflation expectations a key area of focus, the BoC is likely to remain on hold next week while reiterating its commitment to keeping expectations well anchored.

U.S. Highlights

- Iran signaled a reopening of the Strait of Hormuz amid a fragile ceasefire, easing oil prices and lifting markets, though evidence of a full normalization in shipping remained limited.

- Retail sales rose sharply in March, boosted by higher gasoline prices but also supported by solid underlying volumes, pointing to continued consumer resilience.

- Business surveys showed activity stabilizing even as war-related supply disruptions pushed price pressures higher, complicating the policy outlook.

Canada – Well Behaved Core Inflation Strengthens BoC Hold Case

The fluid Middle East situation continued to drive Canadian financial markets. Oil prices remain volatile, with WTI up this week amid limited progress on diplomatic efforts between Iran and the U.S. Canadian bond yields also edged higher (as of writing), with Middle East tensions keeping inflation risks in focus. Since the onset of the war, the 10-year bond yield is up about 35 bps.

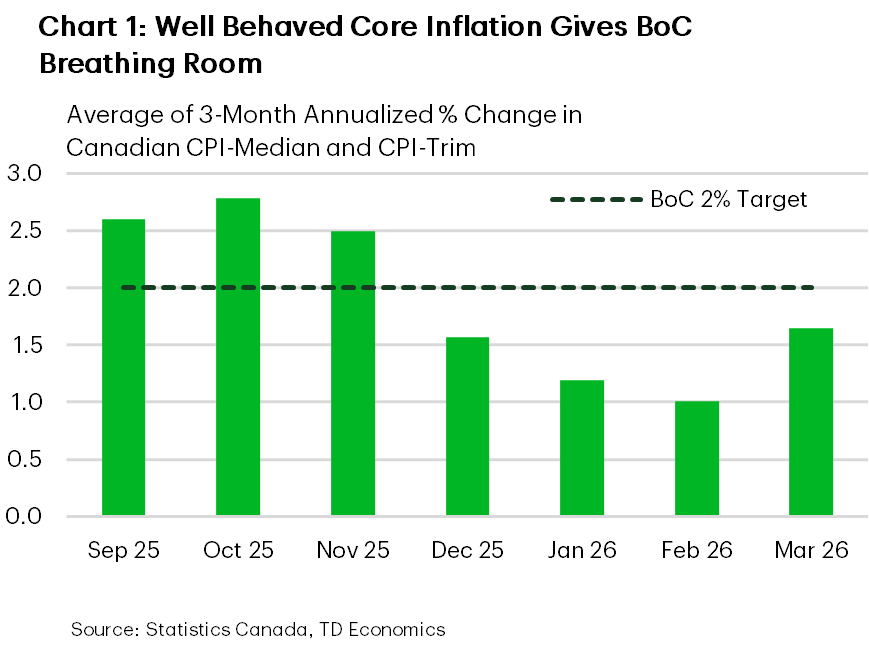

This week’s data offered a largely pre-war read on momentum and an early look at inflation spillovers. Retail sales rose in February and Statistics Canada’s flash estimate points to another gain in March. For the Bank of Canada, though, March CPI was the focal point. Headline inflation rose 0.6 ppts to 2.4%, driven by the recent jump in gasoline prices, but the details were modestly softer than expected. For instance, shorter-term core metrics firmed on the month, but remained below 2%, on average (Chart 1). Gasoline prices have been more contained through April, while the federal government has temporarily removed the excise tax on fuels. Still, year-over-year inflation should get a mechanical lift from base effects tied to the April 2025 carbon-tax cut.

The Bank of Canada’s Q1 Business Outlook Survey (BoS) was conducted largely before the war, with only a smaller share of responses collected afterward. Pre-war results showed sentiment improving as firms are adjusting to U.S.–Canada trade frictions. In the background, the CUSMA review is now underway. U.S. and Canadian officials flagged several irritants this week – including U.S. tariffs on Canadian aluminum/steel/autos/lumber and provincial restrictions on U.S. alcohol sales – that will shape negotiations. Multiple parties also suggested the original July 1 deadline is unlikely to be met.

Firms surveyed post-war in the BoS reported only modest impacts on activity measures so far, but flagged rising input costs. The ability of firms to pass through higher costs was mixed, constrained by lackluster demand and increased competition.

Next week brings the release of the federal government’s Spring Economic Update. Last November’s budget pegged the FY 2026/27 deficit at a lofty 2.0% of GDP. This shortfall would also be at the higher end compared to provincial expectations this budget season. However, this year’s outlook for nominal GDP (which drives government revenues) will likely be revised up relative to last November. The update may also be light on substantial net new measures, as several had already been announced, like the grocery rebate top-up.

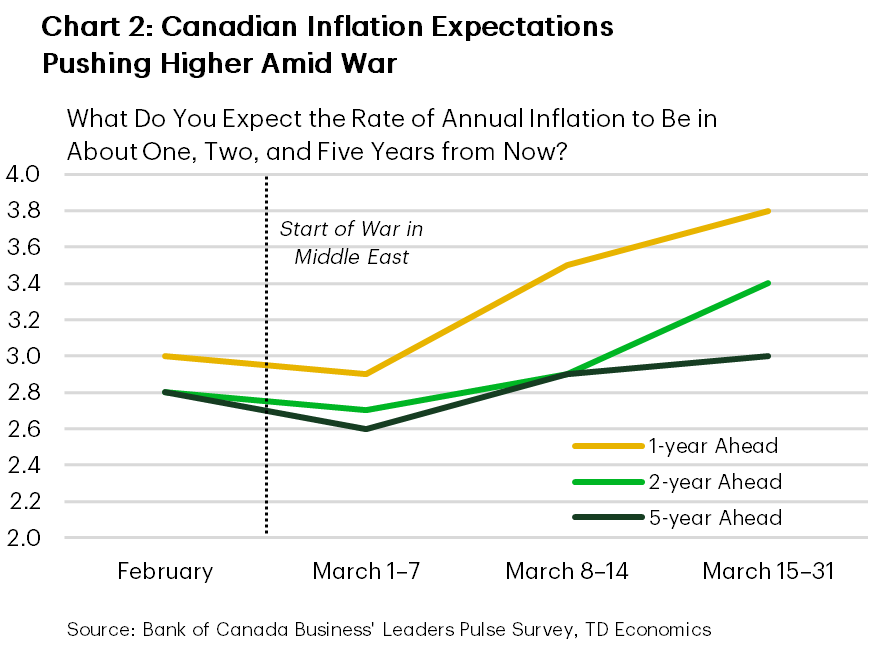

Attention turns to the Bank of Canada’s rate decision next week. The Bank is widely expected to stay on hold – our call as well. With the economic fallout from the war still highly uncertain, it would be premature to pivot from a hold, particularly with core inflation still well behaved. That said, the BoS points to some upward drift in shorter-term inflation expectations, though long-term measures remain well anchored (Chart 2). Expect the Bank to stress its willingness to act as needed to keep expectations anchored.

U.S. – Markets Jitter, Prices Bite

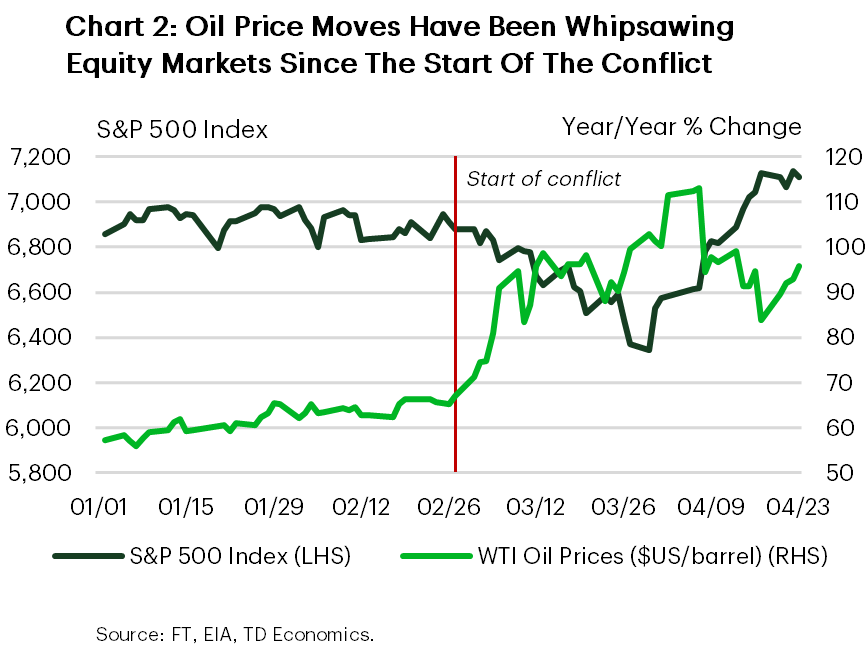

As the Iran conflict approaches the two month mark, financial markets remained highly sensitive to signals around energy supply risks. Early in the week, Iran announced that the Strait of Hormuz would be reopened to commercial shipping vessels during a newly brokered ceasefire, triggering a sharp pullback in oil prices and a relief rally in risk assets. WTI crude fell into the low $80s per barrel range, while U.S. equities moved to new highs as immediate worst case supply scenarios were priced out (Chart 1). That said, reporting around actual shipping flows suggested that conditions on the ground were uneven. As a result, while near term fears eased, geopolitical risks remain elevated and sentiment fragile, leaving markets vulnerable to renewed volatility should tensions re escalate.

U.S. economic data this week offered a reminder that domestic momentum has not yet broken down. Retail and food services sales rose 1.7% in March, driven largely by a surge in gasoline prices, but importantly, real (inflation adjusted) spending also increased a solid 0.8%. Core retail sales excluding gasoline, autos, and building materials posted broad-based gains, suggesting that households have not yet pulled back meaningfully on goods consumption. One area of softness was spending at restaurants, which was little changed on the month, highlighting some emerging price sensitivity among consumers.

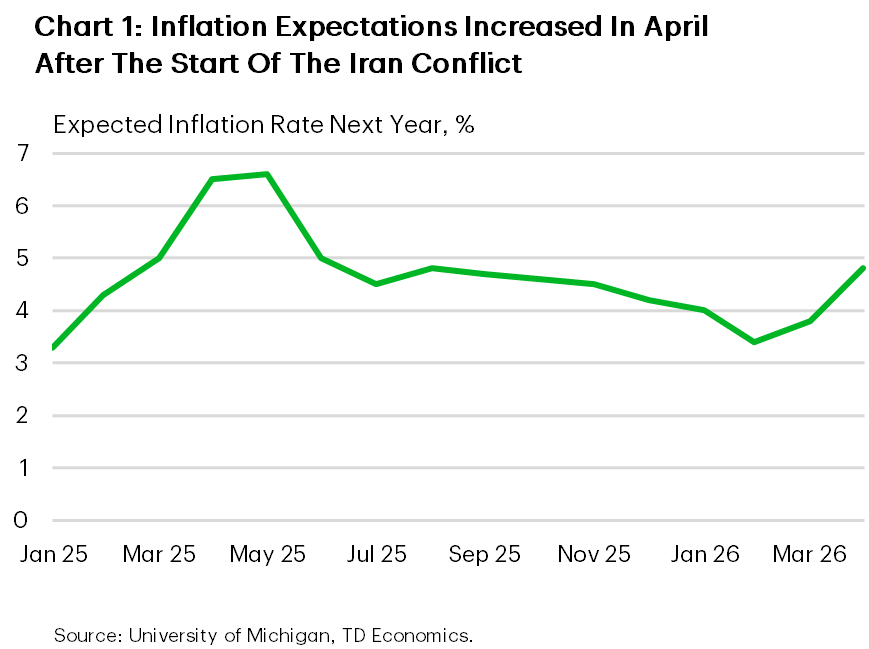

Forward-looking indicators painted a more mixed picture. The latest U.S. PMI readings showed business activity recovering modestly in April after stalling in March, with manufacturing rebounding more strongly than services. However, the rebound was accompanied by worsening delivery times and a sharp increase in input and output prices, reflecting ongoing supply disruptions tied to the conflict. Firms reported precautionary stock building and rising costs, reinforcing concerns that inflation pressures could re-intensify. The University of Michigan survey released today showed inflation expectations over the next year rising sharply, a key indicator energy-driven price worries are becoming more entrenched (Chart 2).

Markets are also increasingly focused on the Federal Reserve policy backdrop. Kevin Warsh’s confirmation hearing this week underscored uncertainty around the future policy framework, with investors parsing how shifts in leadership could influence the Fed’s reaction function at a time when inflation and growth risks are pulling in opposite directions. While Warsh’s confirmation by the Senate Banking Committee was uncertain amid the ongoing DOJ investigation of Chair Powell, headlines on Friday morning suggested the charges had been dropped. This clears a path for Warsh’s confirmation, which means next week’s interest rate announcement will likely be Jerome Powell’s last as chair. Looking ahead, next week’s data calendar is heavy, with personal income and PCE inflation, first quarter GDP, and ISM surveys all due. Together, these releases will help determine whether the economy is slowing enough to offset renewed price pressures.

, with Middle East tensions keeping inflation risks in focus. Since the onset of the war, the 10-year bond yield is up about 35 bps.){kind=link}