Markets received some welcome relief from US inflation data today, but the respite might prove short-lived as renewed geopolitical tensions quickly returned to the forefront. While headline CPI accelerated to its highest level in three years, the underlying details were slightly softer than feared, allowing investors to step back from the idea that the Federal Reserve may need to move rapidly toward rate hike.

US CPI rose from 3.8% yoy to 4.2% yoy in May, matching expectations and reflecting the continued impact of higher energy prices. However, core CPI edged up only from 2.8% yoy to 2.9% yoy, while monthly core inflation slowed from 0.4% mom to 0.2% mom. Markets had been particularly concerned about the possibility of a core inflation surprise above 3%, which could have significantly strengthened expectations for additional Fed tightening. Instead, the report suggested that the energy shock has not yet spread through the broader economy as aggressively as feared.

The data leave Fed in a relatively comfortable position. Inflation remains elevated and energy costs continue to pose risks, but policymakers have room to wait and assess whether current pressures become more persistent. Following last week’s strong nonfarm payrolls report, the combination of resilient employment and contained core inflation supports a patient approach rather than an immediate policy response.

Meanwhile, that inflation narrative was quickly overshadowed by developments in the Middle East. US President Donald Trump struck a much more confrontational tone toward Iran today, saying the country had taken too long to negotiate and would now have to “pay the price.” The comments marked a notable shift from just a day earlier, when Trump suggested a deal could be reached within “two or three days” and that the Strait of Hormuz could reopen shortly thereafter.

The tougher rhetoric followed Tuesday’s US strikes against Iranian targets, which US Central Command said were conducted in response to the downing of a US Army Apache helicopter. While Iran has not directly claimed responsibility for the incident and Iranian state media reported no offensive operations in the Strait over the past day, the latest exchange has reinforced concerns that diplomatic progress may be moving further away rather than closer.

US equity futures traded modestly lower as the session began. With the CPI hurdle now behind markets, investor attention is also returning to the AI sector, where heavy selling pressure has persisted since late last week. The rebound attempts seen earlier in the week have struggled to gain traction, leaving technology shares vulnerable to further volatility.

In currency markets, Sterling leads weekly performance, supported by stronger domestic data and expectations that Bank of England may need to maintain a tightening bias. New Zealand Dollar and Euro followed. Australian Dollar is the weakest performer as markets continued to unwind expectations for further RBA tightening. Swiss Franc and Yen also lagged, while Dollar and Canadian Dollar traded closer to the middle of the pack.

US Inflation Climbs to 4.2%, But Core CPI Offers Fed Some Relief

US inflation hit its highest level in three years in May, driven primarily by soaring energy costs. But while headline CPI rose to 4.2%, the closely watched core measure remained below 3% and monthly core inflation slowed, offering markets some relief from fears of a more aggressive Fed response. Read More.

AUD/USD Faces 0.70 Breakdown If US Core CPI Tops 3%

AUD/USD is approaching one of its most important levels of the year. With markets focused on whether US core CPI can stay below 3%, a hotter inflation reading could strengthen Fed hike expectations and trigger a decisive break below the 0.70 handle. Read More

Gold Approaches Make-or-Break $4,000 Zone as US-Iran Tensions Escalate

Gold is rapidly approaching the most important technical battleground of the 2026 correction. As fading US-Iran peace hopes keep inflation concerns elevated, prices are closing in on the critical $4,000 support zone. A brief break is possible, but the bigger question is whether buyers step in and defend the broader support cluster. Read More.

Japan Producer Inflation Jumps to 6.3% as Energy Shock Drives Costs Higher

The energy shock is increasingly showing up in Japan’s inflation data. Producer prices rose faster than expected in May, while import costs recorded their strongest increase since late 2022 as higher crude oil prices flowed through supply chains. Read More.

China CPI unchanged at 1.2%, PPI Climbs to Highest Since 2022

China’s inflation story is increasingly split in two. Consumer inflation remained subdued in May as falling food prices kept CPI below expectations, while producer inflation climbed to its highest level in nearly three years as energy and commodity costs surged. Read More.

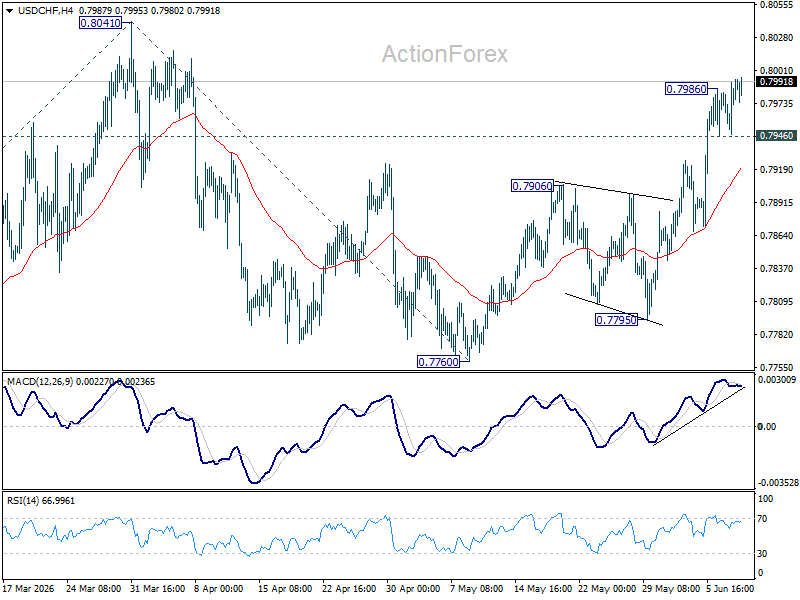

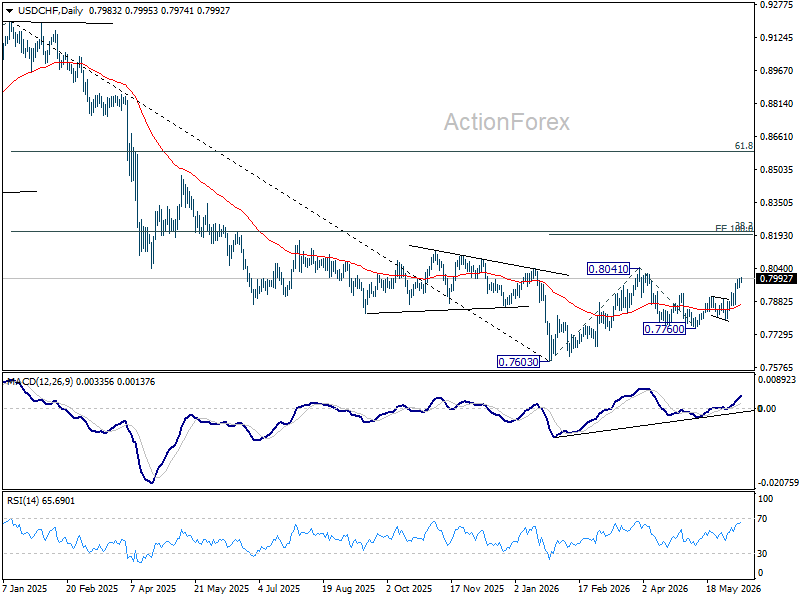

USD/CHF Daily Outlook

USD/CHF’s rally resumed after brief consolidations .intraday bias is back on the upside for retesting 0.8041 high. Firm break there will resume the rise form 0.7603 and target 100% projection 0.7603 to 0.841 from 0.7600 at 0.8198 next. On the downside, below 0.7946 minor support will turn intraday bias neutral again.

In the bigger picture, while a medium term bottom was formed at 0.7603, it’s still early to call for bullish trend reversal. As long as 38.2% retracement of 0.9200 (2025 high) to 0.7603 at 0.8213 holds, the larger down trend could still continue through 0.7603 at a later stage. However, firm break of 0.7603 will argue that the trend has reversed and turn focus to 0.8332 support turned resistance (2023 low) for confirmation.

{kind=link}