Labor market conditions remain stable, but the recent pace of hiring is unlikely to be sustained. We expect payroll growth to moderate to 120K in June and look for the unemployment rate to hold at 4.3%. Separately, Chair Warsh is expected to outline a more structural framework for central banking and limited forward guidance in his first major public remarks. In Canada, activity is expected to improve modestly following a soft Q1, with energy output providing support but partially offset by weakness elsewhere. In the Eurozone, inflation has heated up alongside temperatures, but we expect headline and core inflation to cool slightly with lower energy prices. In emerging markets, China’s June PMI is expected to point to continued softness, with sluggish activity and sentiment suggesting weak medium-term growth momentum.

United States

Warsh Speaking • Wednesday

FOMC Chair Kevin Warsh is set to deliver his first “Fed speak” at the ECB’s Sintra Forum alongside central bankers from across the globe. We doubt that Warsh will provide much insight on the near-term policy path and instead emphasize more structural views on the future of U.S. central banking in the years ahead.

We do not expect much forward guidance beyond limited remarks that center on price stability and patience. His comments on structural central banking topics will probably be similar to what he said at the most recent press conference as it relates to communication tools, the Fed’s balance sheet, alternative data, AI and productivity, and so forth. Although we don’t expect it, we will be listening closely for any guidance on where Warsh’s views lie as it relates to the near-term policy outlook as well as the longer-run neutral rate.

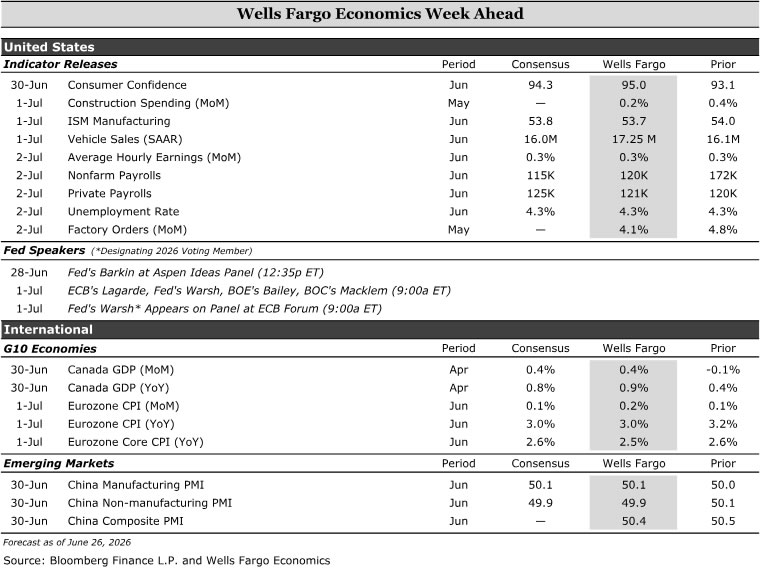

Our base case is for the FOMC to keep the fed funds rate steady at current levels through year-end 2027, with risks tilted towards a few rate hikes if the employment and inflation data come in hotter than expected over the next few months.

Employment • Thursday

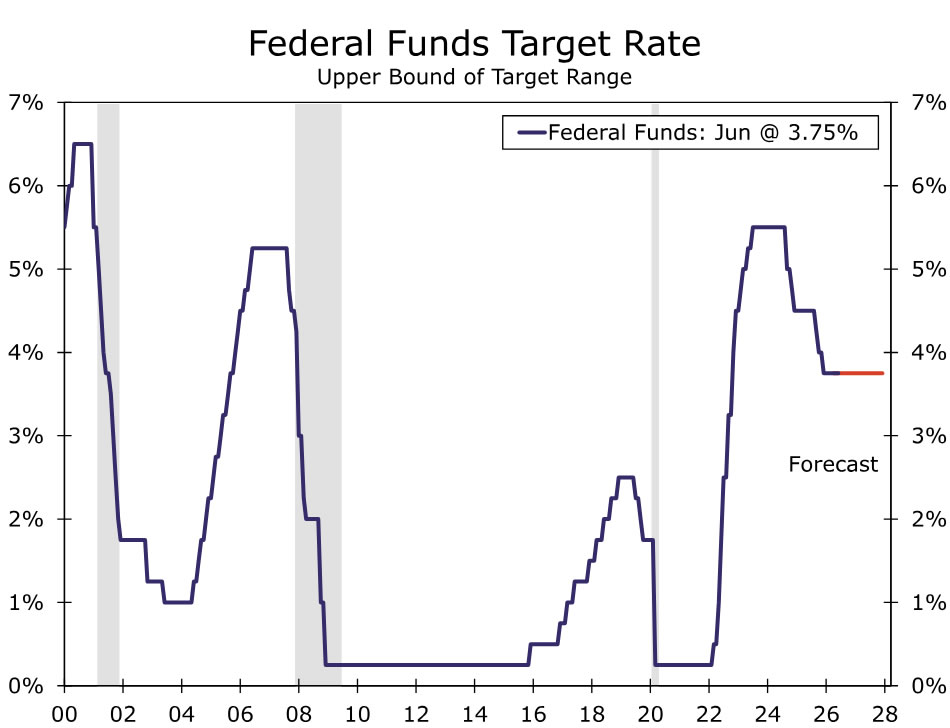

The labor market continues to stabilize after its swoon in 2025. Initial jobless claims are low and regional Fed employment PMIs point to some modest firming in hiring in June. That said, other indicators have softened recently. Indeed job postings and ADP’s weekly hiring measure have both turned down since the spring, while small business hiring plans fell to a fresh cycle low in May. Taken together, the data suggest labor demand is holding roughly steady rather than re-accelerating in a meaningful way.

We estimate nonfarm payrolls rose 120K in June, with private payrolls up a similar 121K. While job growth has averaged a 188K pace over the past three months, we suspect that overstates the underlying trend. May’s gain was underpinned by outsized gains in leisure & hospitality and local government ex-education, categories where the recent pace of hiring looks unlikely to be sustained and could ultimately be revised away.

We look for the unemployment rate to hold at 4.3%, though risks are tilted to the downside. A rebound in household employment appears likely, but could be accompanied by a pickup in labor force participation which would leave the jobless rate unchanged. Wage growth should remain contained, with average hourly earnings rising 0.3% on the month and 3.5% over the past year. Even with some recent firmness in headline payroll gains, the broader picture remains one of a labor market near balance, with neither labor demand nor wage pressures signaling a return to overheating.

G10 Week Ahead

Canada GDP • Tuesday

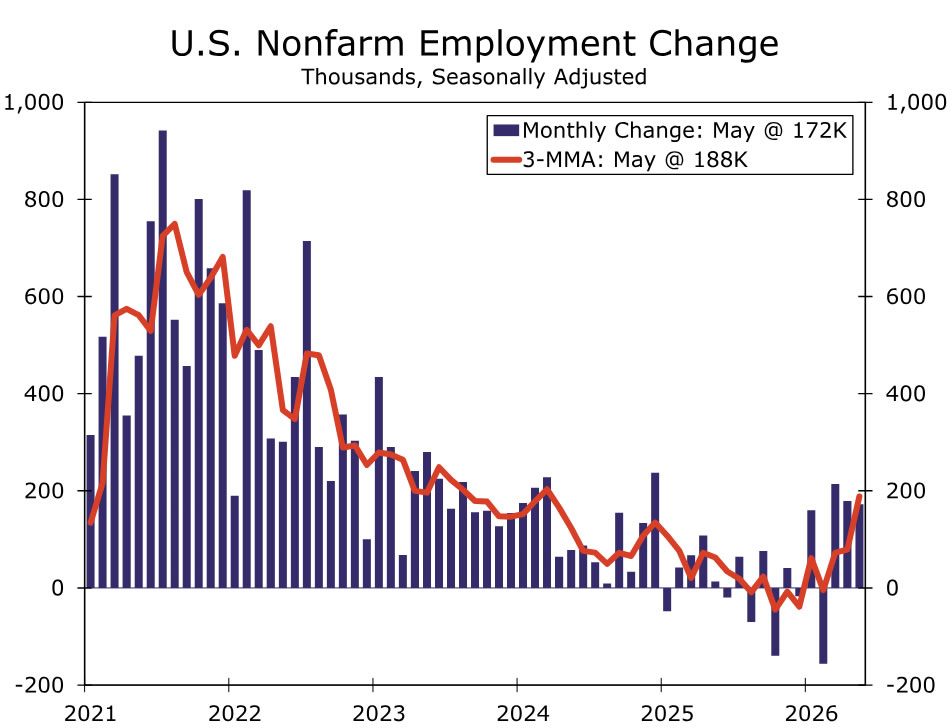

Canada’s April monthly GDP is likely to rise 0.4% month-over-month, in line with Statistics Canada’s advance estimate. Activity should modestly improve after a softer Q1, supported in part by stronger energy sector output, although declines in agriculture, forestry, fishing and hunting may provide a partial offset. While recent PMI surveys also point to some firmness in April, the strength appears tied to stock building amid higher prices and elevated uncertainty around the Middle East conflict rather than a sustained pickup in demand.

For the Bank of Canada (BoC), a stronger April GDP print may not be enough to shift the policy outlook toward tightening. But even as May CPI surprised to the upside, the increase was largely energy-driven, with the BoC’s preferred core measures remaining broadly stable, and wage pressures contained.

Against this backdrop, we now see a higher bar for tightening and expect the BoC to remain on hold through year-end. That said, the outlook remains highly contingent on whether the U.S.–Iran interim deal holds and on the trajectory of USMCA negotiations.

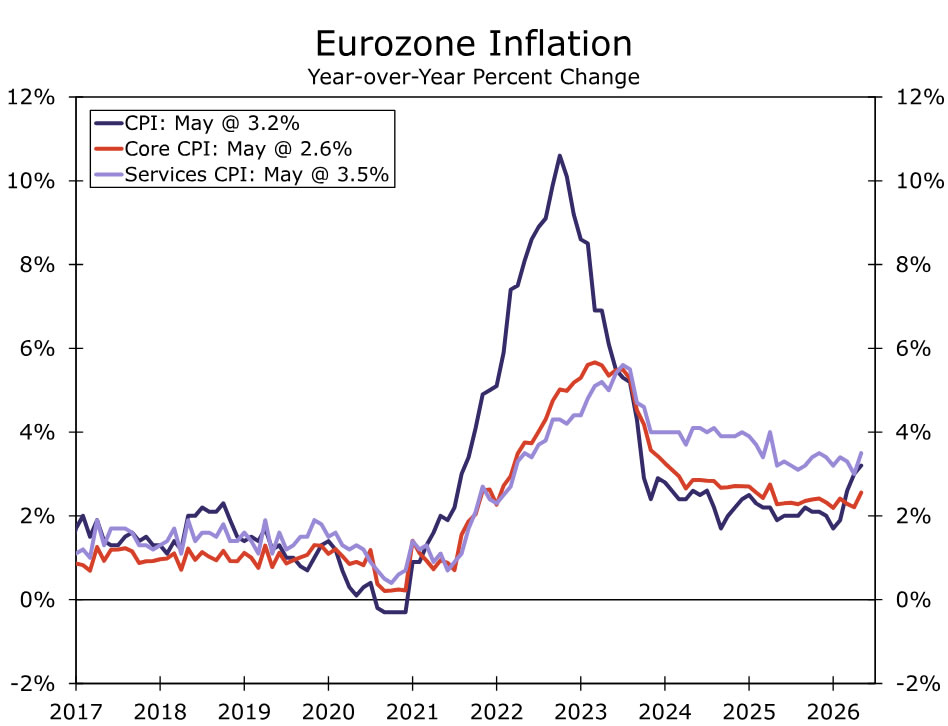

Eurozone CPI • Wednesday

We expect next week’s Eurozone CPI release for June to show headline inflation easing to 3.0% year-over-year (from 3.2%), with core inflation edging lower to 2.5% (from 2.6%). Lower retail energy prices should help contain headline pressures, with recent pump price data pointing to some relief. PMI data also suggest that lower energy prices are beginning to filter through to businesses, as input cost and selling price inflation eased in June.

Still, we do not expect the data to deter the European Central Bank (ECB) from another hike in Q3. Medium-term inflation expectations remain elevated relative to pre-war levels, even as one-year inflation expectations have moved lower. We expect the ECB to pause in July while policymakers assess developments in the Middle East, including whether the Strait of Hormuz remains open and safe for oil flows, before hiking in September and bringing the Deposit Rate to 2.50%. That said, risks are tilted toward a hold if growth momentum weakens, core inflation surprises to the downside, or price pressures remain narrow.

EM Week Ahead

China PMIs • Tuesday

China’s official June PMI figures are due next week and should provide an initial read on whether economic activity stabilized at the end of Q2. We expect the data to remain close to the 50 threshold separating expansion from contraction, with manufacturing PMIs edging up to 50.1 and nonmanufacturing PMI slipping to 49.9.

Momentum has been subdued so far in Q2, with recent data pointing to a soft and uneven backdrop. May PMI readings showed a similar pattern, with manufacturing easing to the neutral threshold while nonmanufacturing was supported by a boost to services around the early-May Labor Day holiday.

Looking ahead, we expect domestic demand to remain soft. External developments, including the potential for lower global oil prices if a U.S.-Iran interim agreement holds, are unlikely to materially alter that outlook, as households remain partly insulated by domestic energy price caps. As such, we continue to see GDP growth slowing to 4.5% in 2026 and 4.3% in 2027, with policy support likely to remain targeted rather than broad-based.

{kind=link}