- We expect the ECB to keep policy rates unchanged, with the deposit rate at 2.25%, on Thursday 23 July, in line with consensus and market pricing.

- We expect Lagarde to keep full optionality on the future policy rate path, leaving the door open to a September hike, but without pre-committing.

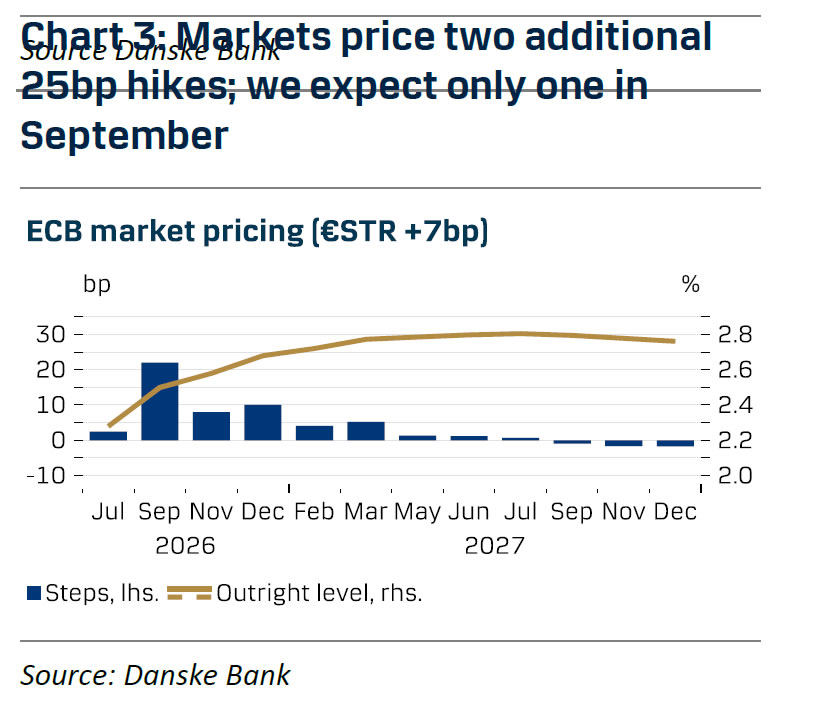

- We expect a final 25bp hike in September, bringing the deposit rate to 2.50%.

We expect the ECB to leave policy rates unchanged at the July meeting, in line with market pricing and consensus. Since the June meeting, inflation has surprised to the downside, including beyond energy, and near-term oil futures have declined even after the recent end to the ceasefire between the US and Iran. These developments, combined with broadly anchored medium-term inflation expectations, give the ECB the option to wait for new staff projections at the September meeting before potentially hiking policy rates again.

Focus during the meeting will be on signals about the future rate path. We will be particularly attentive to the risk assessment of the inflation and growth outlook. The ECB views inflation risks as tilted to the upside and growth risks as tilted to the downside, but Lagarde stated on 1 July that they are now “probably more balanced”. Yet, given the recent escalation of the war in Iran and the lack of new staff projections, we do not expect the risk assessment to be changed.

We expect Lagarde to keep full optionality on the future policy rate path, leaving the door open to a September hike, but without pre-committing. At the Sintra conference, she reiterated that the ECB has set aside forward guidance and instead provides “framework guidance” on its reaction function. With markets currently pricing in 22bp worth of ECB hikes at the September meeting, and given the high uncertainty around the future path of energy prices, we do not believe the ECB has an incentive to rock the boat.

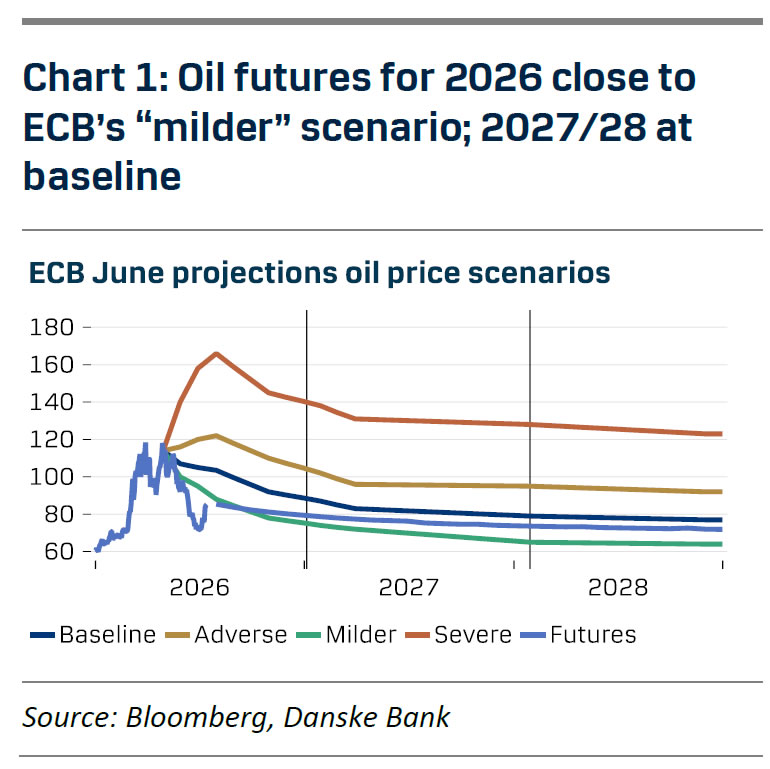

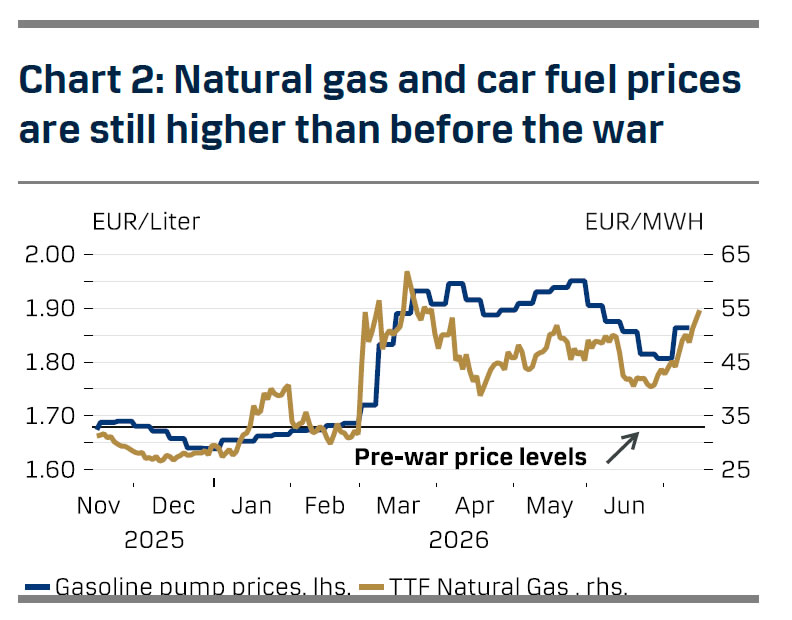

Our baseline remains that the ECB will deliver a final 25bp hike at the September meeting. The bias in the GC remains hawkish, even as it is slightly more balanced now compared to June. While crude oil futures have declined the prices of refined oil products and natural gas remain above pre-war levels, by 10% for gasoline and 170% for natural gas, respectively. Consumer inflation expectations also remain elevated, and markets are pricing inflation to average 3.25% y/y for the rest of 2026 and 2.65% y/y in 2027. Having said that, growth has been weaker than expected in Q2, and the June inflation print was soft, with no signs yet of indirect effects from the energy shock. At the same time, there are no signs of second-round effects, and the labour market is weakening, so we do not expect more than one additional hike and we then see the ECB cutting the deposit rate back to 2.00% next year.

{kind=link}