Here are the latest developments in global markets:

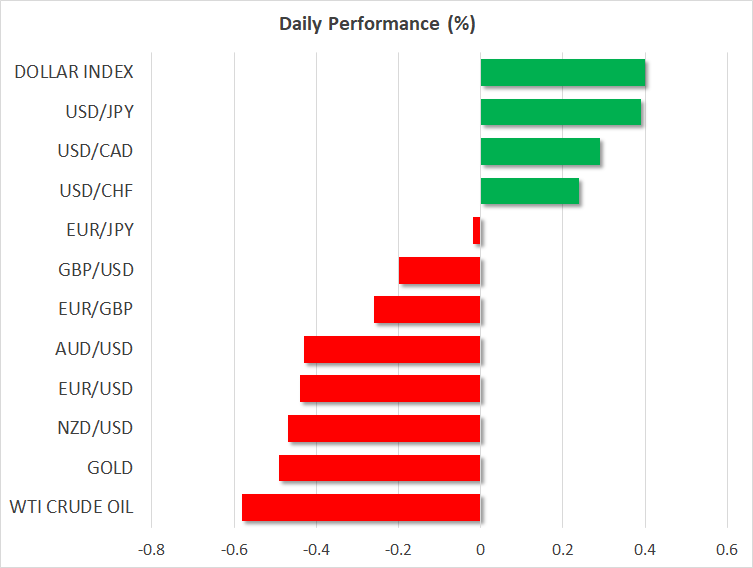

FOREX: The dollar picked up speed as the 10-year US Treasury yield continued to trend near 3.0%, the highest since early 2014, underpinned by concerns that increasing oil prices could spread inflationary pressures, while a rise in US debt issuance was also supportive for the jump in yields. Besides that, Saturday’s news out of North Korea increased appetite for riskier investments. The North Korean leader said that he would suspend nuclear and intercontinental ballistic missiles tests ahead of a crucial meeting with South Korea and the US in late May or early June. In response, the dollar index jumped to a near 2-month high of 90.64 (+0.37%) today, while dollar/yen crawled up to a 2 ½-month high of 108.03 (+0.34%). Euro/dollar tumbled to a two-week low of 1.2236 (-0.44%) on the face of a strengthening dollar, unable to gain from an encouraging composite PMI out of the Eurozone. Pound/dollar was also trading at two-week lows, last seen at 1.3975 (-0.22%) as traders remained cautious on whether the BoE will deliver a rate hike in May, following the BoE governor’s dovish comments on Thursday. Euro/pound was on the back foot after four days of rising, changing hands at 0.8756 (-0.24%). The antipodean currencies were among the worst performers, with aussie/dollar and kiwi/dollar extending declines towards 0.7635 (-0.47%) and 0.7171 (-0.50%) respectively. Dollar/loonie stretched its uptrend to 1.2796 (+0.31%).

STOCKS: European equities turned lower on Monday on the back of rising US Treasury yields, while disappointing statements by UBS, Switzerland’s biggest bank, weighed on equity market sentiment. The pan-European STOXX 600 was down by 0.27% at 0800 GMT, with all sectors except healthcare and energy being in the red. The German retailer Metro AG was leading the losses after the company cut its earnings projections for the 2017/2018 year, saying that earnings from its Russian operations could ease more than expected in the second half of the year. UBS also stood cautious about the coming quarter despite upbeat reports on Q1 2018 earnings, citing geopolitical and trade risks as threats to the outlook. The German DAX 30 fell by 0.28%, the Swiss SMI declined by 0.58% and the French CAC 40 dropped by 0.21%. The UK’s FTSE 100 was steady, supported by basic materials. Indices tracking US stock futures were flashing red, pointing to a negative open.

COMMODITIES: Oil prices weakened further on Monday despite the United Arab Emirates saying that the OPEC’s mission “is not complete” yet and supply cuts by OPEC and non-OPEC members including Russia will continue until the end of the year. WTI crude and Brent retreated to $67.95 (-0.66%) and $73.69 (-0.50%) per barrel respectively. In precious metals, gold declined to a two-week trough of $1,327.02 per ounce (-0.50%).

Day Ahead: US flash PMIs and existing home sales in the calendar; Australian CPI in focus

Monday will be a relatively quiet day ahead of a week featuring central bank meetings, important data releases, and possibly developments on the geopolitical front.

The day continues with the Canadian wholesale sales for the month of February scheduled for release at 1230 GMT.

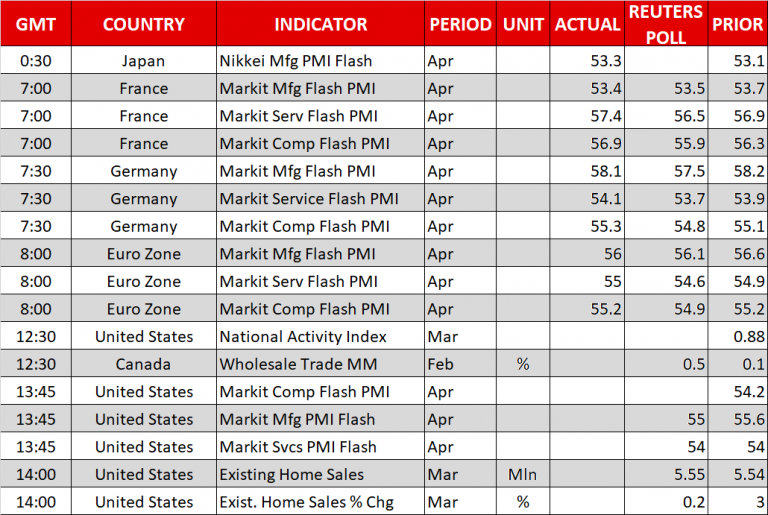

The US will see the release of April’s preliminary PMIs out of Markit at 1345 GMT, with analysts expecting the manufacturing PMI to tick marginally lower to 55.0 compared to 55.6 seen in March, while the composite index is anticipated to inch higher by 1.1 points to 55.3.

Remaining in the US, at 1400 GMT, existing home sales data for the month of March will be attracting interest. Growth in sales is said to have slowed down from 3.0% m/m to 0.2%.

Turning to today’s public appearances, European Central Bank Executive Board member Benoit Coeure will be speaking at a conference at 1400 GMT. Later at 1930 GMT, Bank of Canada Governor Stephen S. Poloz and Senior Deputy Governor Carolyn A. Wilkins will be making comments in front of the House of Commons Standing Committee on Finance, while at 2200 GMT a speech by RBA Assistant Governor Christopher Kent will be in focus.

During Tuesday’s early Asian session, the Australian Bureau of Statistics will deliver data on consumer prices (0130 GMT). Forecasts are for the headline CPI to rise by 2.0% y/y in the first quarter of 2018 from the 1.9% seen in the previous quarter, probably due to seasonal effects. The core measures however, which are closely watched by the RBA, are projected to remain on average slightly below the central bank’s inflation target range of 2-3.0%, signaling that a rate hike is not likely to happen anytime soon, as subdued wage growth and high debt levels continue to hang in the background.

Should inflation numbers surprise to the upside, bringing some relief to RBA policymakers, the Australian dollar could recoup losses made the past couple of days. On the other hand, disappointing prints could push the currency to fresh lows.

In stock markets, Google-parent Alphabet will be releasing quarterly results today after the US market close.

{kind=link}