RBNZ is widely expected to deliver another 25bps cut tomorrow, bringing the Official Cash Rate down to 3.50%. With the move largely priced in, traders will be focused on how the central bank interprets the rapidly evolving global environment.

As the first major central bank to meet since the US launched the sweeping reciprocal tariffs, RBNZ’s tone and guidance will not only be key for New Zealand, but will also offer insights for the broader Asia-Pacific region.

While there are speculative whispers about the possibility of a larger-than-expected rate cut to cushion the economy against the external shock, RBNZ will likely refrain from doing so just yet. The current level of uncertainty, both in terms of policy responses and economic impact, should see the central bank remain cautious, maintaining its easing bias without overcommitting.

With another cut already projected in May, RBNZ is expected to stay on its path of gradual policy accommodation while waiting for more concrete data on trade disruption effects. The question of whether the RBNZ will eventually push OCR below 3.00% remains open. Much will depend on how the trade war unfolds, how consumer and business sentiment hold up, and the extent of the ripple effects across Asia’s open economies.

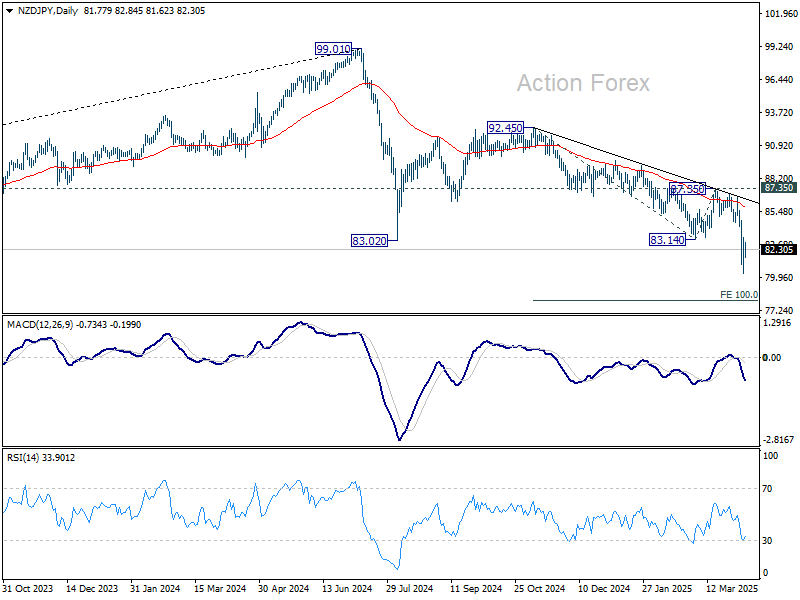

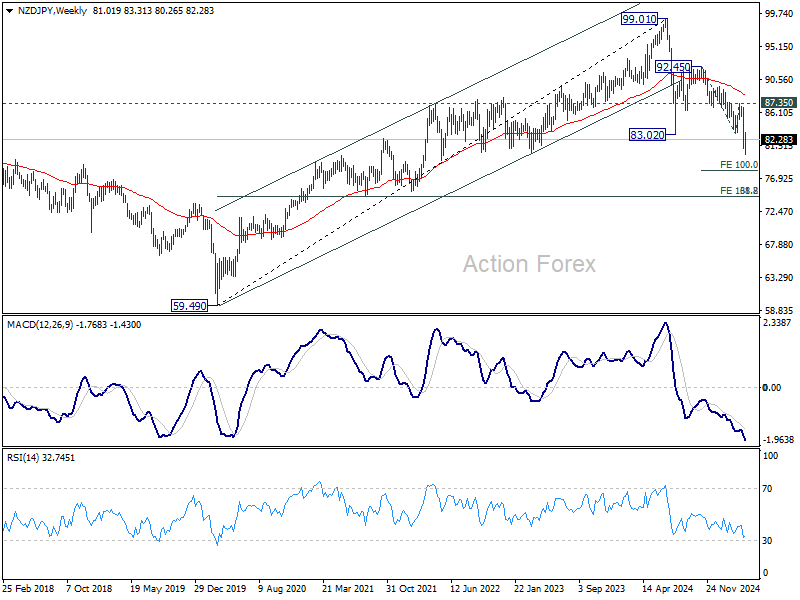

Technically, NZD/JPY’s down trend from 99.01 (2024 high) resumed by breaking through 83.02 low last week. Whether this is a correction of the multi-year uptrend from the 2020 low of 59.49, or a full reversal, is yet to be determined.

In either case, near term outlook will remain bearish as long as 87.35 resistance holds, in case of recovery. Next target is 100% projection of 92.45 to 83.14 from 87.35 at 78.04. Firm break there will target 138.2% projection at 74.48. This coincides with 61.8% retracement of 59.49 to 99.01 at 74.58.

{kind=link}