{kind=link}

AUD/USD is steady after RBA minutes reinforced tightening bias, though policymakers emphasized low confidence in outlining the next move. That cautious messaging capped immediate upside follow-through. Still, markets continue to price a solid chance of a May rate hike, despite growing talk that the currency’s recent surge could lessen the need for further tightening. As long as those expectations remain intact, any pullback in AUD/USD should be contained, leaving the broader uptrend undisturbed.

In recent days, arguments have surfaced that Aussie’s recent surge may act as a “shadow hike,” reducing need for additional tightening. Since early January, AUD has rallied roughly 5.8% against Dollar and 4.8% against Yuan. A stronger exchange rate lowers import prices, theoretically easing inflation pressure without further rate increases.

Given that China accounts for roughly 25–30% of Australia’s total trade and US around 11% of goods imports, the appreciation looks meaningful. Standard models suggest that a sustained 10% appreciation trims headline inflation by about 0.5–1.0% over a year.

However, relying on currency strength alone to anchor inflation is a risky strategy. The recent 5% move is helpful but limited, and its impact is concentrated in goods prices. Yet goods inflation is no longer the primary problem. December CPI showed headline at 3.8%, driven by domestic pressures. Rent inflation persists amid structural housing constraints. Services costs remain elevated due to wage dynamics. In short, exchange-rate strength does little to address core domestic drivers.

The logic for further tightening rests on three pillars a stronger AUD cannot directly weaken. First, labor market remains tight, and wage growth continues to support services inflation. Second, productivity gains remain modest. Without stronger output per worker, higher wages feed directly into higher prices. Third, fiscal policy still provides tailwinds, offsetting some monetary restraint.

Market pricing continues to assign high probability to another 25bps hike in May, pending Q1 CPI confirmation. Unless data show abrupt cooling in labor market or services pricing, the “shadow hike” narrative is unlikely to displace tightening bias.

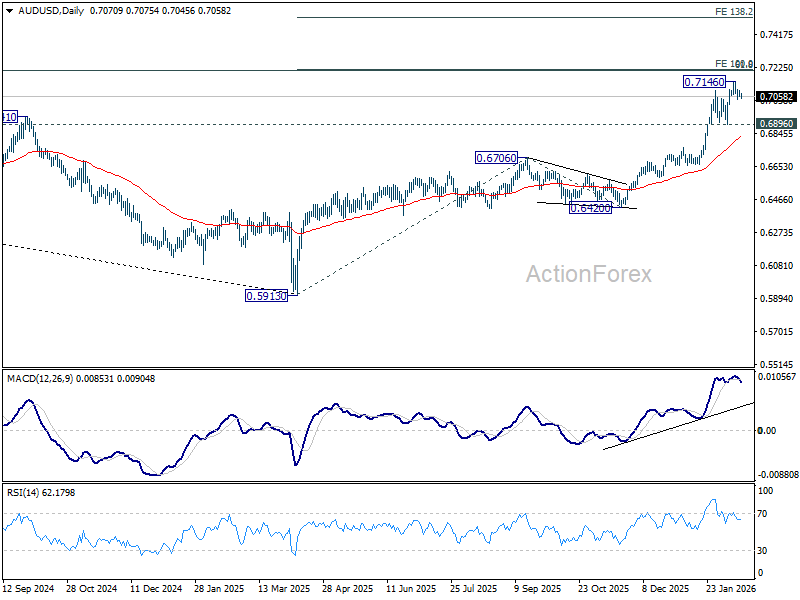

Technically, some more consolidations would likely be seen in AUD/USD below 0.7146 short term top. But downside should be contained above 0.6896 support to bring up trend resumption. The real test lies in 0.72 zone, with 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213. Decisive break there will pave the way to 138.2% projection at 0.7516. But that break through 0.72 might need either a shift in expectations for more than one RBA hike this year, or more Fed rate cuts.