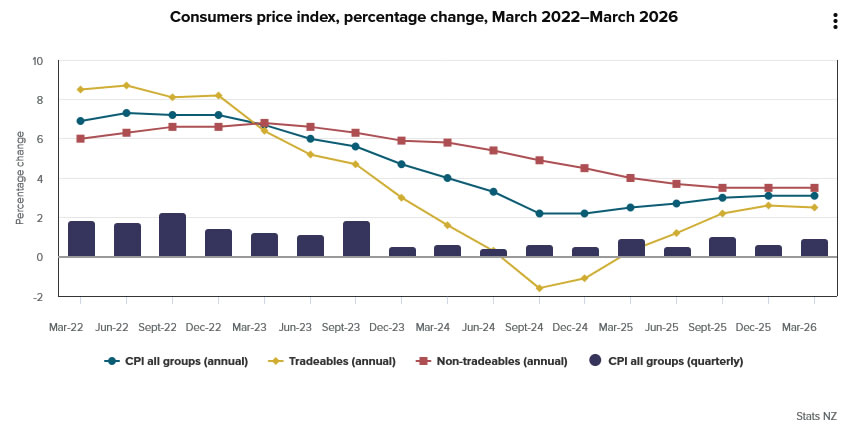

New Zealand’s CPI held steady at 3.1% yoy in Q1, above expectations of 2.9% and marking the highest level since Q2 2024, keeping it above the RBNZ’s 1–3% target band for a second straight quarter. On a quarterly basis, CPI rose 0.9% qoq, slightly above forecasts, suggesting underlying pressures remain persistent despite expectations for easing earlier in the year.

The breakdown highlights a clear divergence between external and domestic inflation. Tradable inflation edged lower from 2.6% yoy to 2.5% yoy, reflecting softer imported price pressures. In contrast, non-tradable inflation held firm at 3.5% yoy, with a 1.1% quarterly increase.

Energy played a key role in the latest pickup. Petrol prices rose 3.5% in the quarter, reversing earlier declines in January and February, while electricity prices surged 12.5% yoy, remaining the largest contributor to annual inflation for a third consecutive quarter. Even excluding petrol, CPI still rose 0.8% qoq, indicating that inflation pressures are not solely driven by energy.

For the RBNZ, the signal is uncomfortable. While core CPI remains relatively contained at 0.5% qoq and 2.6% yoy, the persistence in non-tradables and the continued influence of energy costs point to upside risks. With inflation still above target and domestic pressures holding firm, expectations for a July rate hike are likely to strengthen, particularly if second-round effects begin to emerge in coming months.

| Data | Latest |

|---|---|

| CPI (qoq) | +0.9% |

| CPI (yoy) | 3.1% |

| Tradable CPI (qoq) | +0.7% |

| Tradable CPI (yoy) | 2.5% |

| Non-tradable CPI (qoq) | +1.1% |

| Non-tradable CPI (yoy) | 3.5% |

| Core CPI (qoq) | +0.5% |

| Core CPI (yoy) | 2.6% |

| CPI ex-petrol (qoq) | +0.8% |

{kind=link}