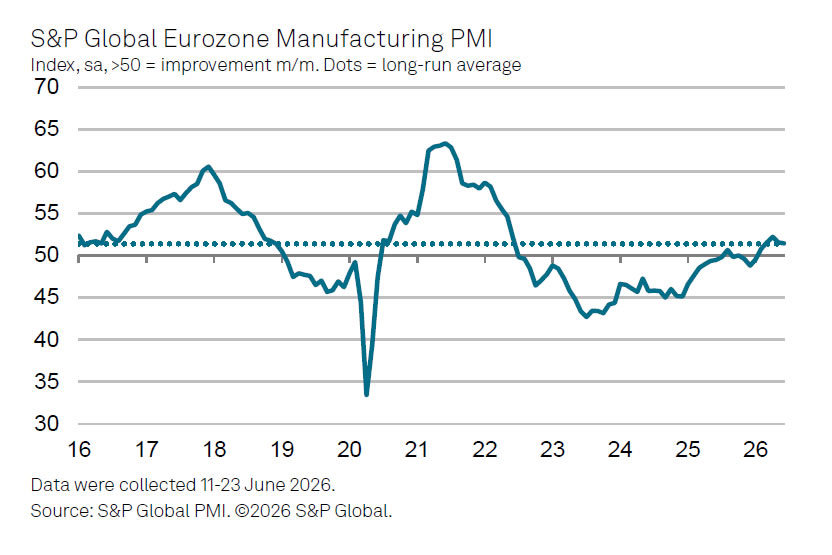

Eurozone manufacturing remained in expansion territory in June despite a modest slowdown in headline activity. The S&P Global Eurozone Manufacturing PMI eased from 51.6 to 51.4, a four-month low, while the Manufacturing Output Index rose from 51.3 to 51.7, its highest level in two months. The data suggest factory production continued to strengthen even as broader business conditions softened slightly.

According to S&P Global Chief Business Economist Chris Williamson, the latest survey capped the strongest calendar quarter for Eurozone manufacturing production since the first quarter of 2022. He noted that the expansion was accompanied by a welcome easing in inflationary pressures, with both input costs and output prices rising at their slowest pace since March, reflecting lower oil prices and improving supply conditions. Williamson said these developments should help reduce firms’ costs while supporting consumer demand through lower inflation.

Looking ahead, however, the outlook is less straightforward. Williamson cautioned that manufacturers have benefited in recent months from precautionary stockpiling linked to the Middle East conflict, a tailwind that is already beginning to fade. While lower energy prices and easing supply constraints provide a supportive backdrop, the unwinding of inventory building could weigh on production growth in the coming months, leaving the durability of the manufacturing recovery dependent on underlying demand rather than temporary stockpiling.

| Indicator | Previous | Latest |

|---|---|---|

| Eurozone Manufacturing PMI | 51.6 | 51.4 |

| Manufacturing Output Index | 51.3 | 51.7 |

| Input Cost Inflation | Slowest since March | |

| Output Price Inflation | Slowest since March | |

| Quarterly Manufacturing Output | Strongest since Q1 2022 | |

| Positive Drivers | Lower oil prices; easing supply concerns | |

| Key Risk | Precautionary stockpiling fading |

{kind=link}