Sample Category Title

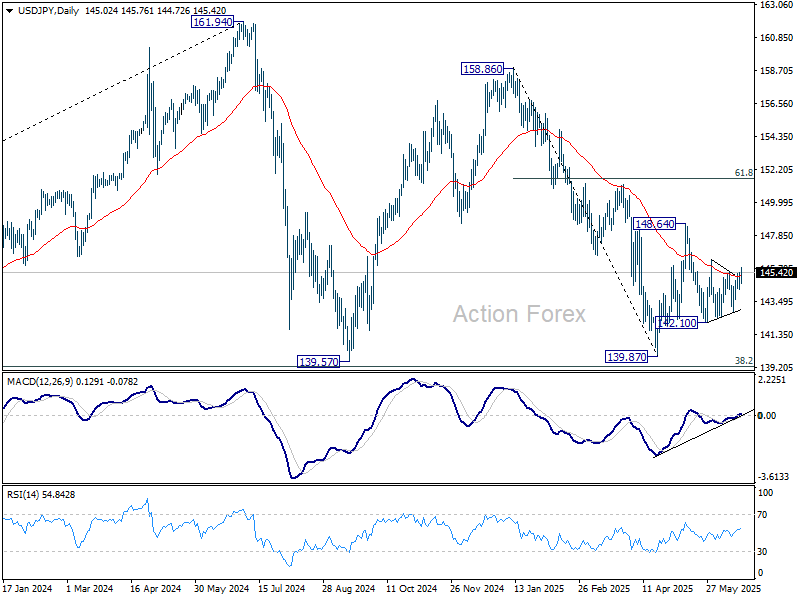

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.49; (P) 144.96; (R1) 145.60; More...

Intraday in USD/JPY is back on the upside with break of 145.46 resistance. Further rise should be seen to 146.27 first. Break there will target 148.64 next. On the downside, below 144.32 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

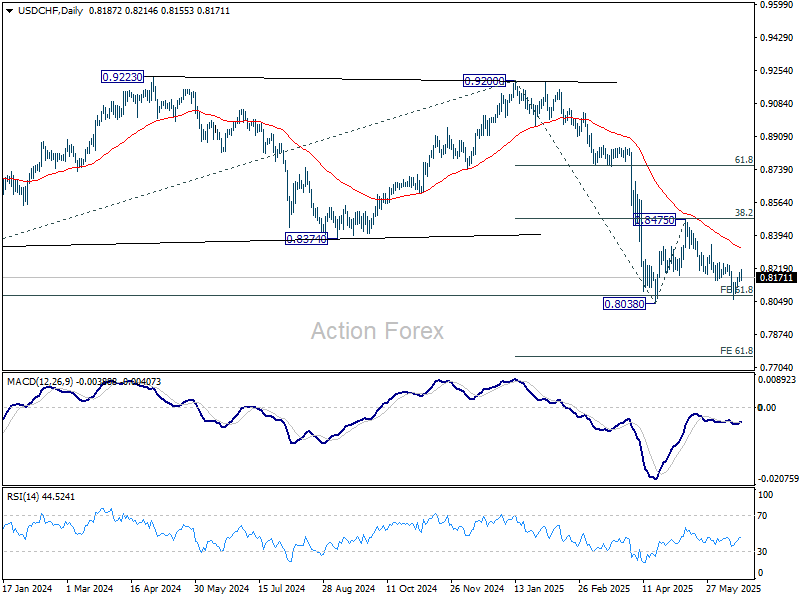

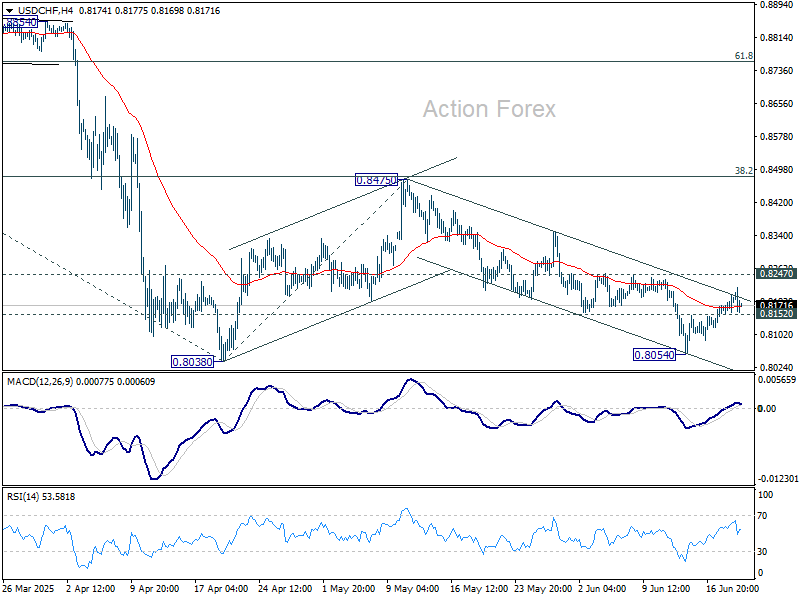

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8133; (P) 0.8153; (R1) 0.8184; More….

Intraday bias in USD/CHF stays neutral at this point. On the downside, break of 0.8152 minor support will argue that recovery from 0.8054 has completed after failing 0.8247 resistance. Deeper fall should be see to 0.8038/54 support zone. Firm break there will resume larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Nevertheless, break of 0.8247 resistance will argue that corrective pattern from 0.8038 is starting the third leg. Bias will be turned back to the upside for 0.8475 resistance again.

Swiss Franc Jumps After Measured SNB Cut, Sterling Recovers after BoE

Swiss Franc rebounded broadly on Thursday after SNB delivered a widely expected 25bps rate cut to 0.00%. Some trade had speculated on either a stronger dovish signal or even surprise action aimed at curbing Franc strength. Instead, SNB refrained from anything bold, and the post-meeting move in Franc reflected such disappointment. Also, in a global environment marked by elevated uncertainty, particularly with ongoing Middle East tensions, the safe-haven demand for the Swiss Franc remains intact.

Meanwhile, Sterling also found some footing after BoE held rates steady at 4.25%. The 6-3 split on the Monetary Policy Committee leaned dovish, with three members voting for a cut. Still, the overall tone remains consistent with its “gradual and careful” easing stance. There was no sense of urgency in the statement, and policymakers continue to stress flexibility in the face of heightened geopolitical and inflation uncertainty.

For the day so far, Swiss Franc is the strongest performer, followed by Sterling and Dollar. At the other end of the spectrum, Kiwi and Aussie lag, followed by Yen. Euro and Loonie are positioning in the middle.

Technically, one focus is AUD/USD's reaction to 0.6455 support as selloff pick up momentum after weaker than expected job data. Sustained break there will confirm short term topping at 0.6551. That would open up deeper fall to 38.2% retracement of 0.5913 to 0.6551 at 0.6307, even as a correction.

In Europe, at the time of writing, FTSE is down -0.15%. DAX is down -0.68%. CAC is down -0.81%. UK 10-year yield is up 0.005 at 4.503. Germany 10-year yield is down -0.007 at 2.507. Earlier in Asia, Nikkei fell -1.02%. Hong Kong HSI fell -1.99%. China Shanghai SSE fell -0.79%. Singapore Strait Times fell -0.68%. Japan 10-year JGB yield fell -0.045 to 1.411.

BoE on hold, dovish undercurrent builds with 3 votes for cut

BoE left its policy rate unchanged at 4.25% today, as expected. The vote came in at 6–3, with Swati Dhingra, Dave Ramsden, and Alan Taylor opting for a 25bps cut. Known doves Dhingra and Taylor had pushed for a larger 50bps cut at last meeting. A surprise was that Ramsden who aligned with the majority last time and supported the 25bps cut. The voting marked a slight shift toward a more dovish stance.

In its accompanying statement, BoE acknowledged that underlying UK GDP growth has remained weak, and that labor market slack is becoming more evident. Inflation jumped to 3.4% in May, largely as expected. BoE expects inflation to hover around current levels through year-end before gradually falling toward the 2% target in 2026.

The statement also pointed to heightened geopolitical risks, particularly from the Middle East, as a complicating factor for inflation and energy costs. In light of this backdrop, the BoE reaffirmed that its next moves will be “gradual and careful” and emphasized that monetary policy decisions are “not on a pre-set path”.

SNB cuts to zero, sees subdued growth as tariff front-loading fades

SNB lowered its policy rate by 25 bps to 0.00%, as widely expected. The move came as inflation pressures continue to ease and growth momentum slows following a front-loaded export boost in Q1. SNB noted that its conditional inflation forecast has been revised downward for 2025 and 2026, but still sees average inflation staying well within its price stability range through the forecast horizon.

The new projections put inflation at just 0.2% in 2025 (down from 0.4%), 0.5% in 2026 (down from 0.8%) and 0.7% in 2027 (down slightly from 0.8%). These figures assume that the policy rate remains at zero throughout the period. SNB said that without today’s cut, the forecast would have been even lower.

On the growth side, SNB acknowledged that the strength in Q1 GDP was driven largely by a pull-forward of US-bound exports — a pattern mirrored in other economies. When adjusted for these front-loaded flows, underlying momentum was "more moderate".. As a result, growth is expected to slow again and remain "rather subdued" over the remainder of the year. SNB projected GDP to rise just 1% to 1.5% this year and next.

ECB's Nagel: Monetary policy is on the right track

German ECB Governing Council member Joachim Nagel remarked today that with inflation nearing 2% on average this year, ECB is “more or less mission accomplished” on the price stability front. He added that rates are now in “neutral territory,” and monetary policy is "on the right track.

At the same conference, Vice President Luis de Guindos reiterated that the path forward will be data-dependent and decided on a meeting-by-meeting basis. He warned of elevated geopolitical risks, including trade tensions and Middle East conflict, which could alter both inflation and economic outlook.

ECB's Villeroy: Next move could be a cut amid sub-2% inflation risks

French ECB Governing Council member Francois Villeroy de Galhau further easing could be on the table if inflation continues to drift below target.

“Barring a major exogenous shock, including possible new military developments in the Middle East, if monetary policy were to move in the next six months, it could be more in the direction of accommodation,” Villeroy said in a speech.

He highlighted that investors are increasingly concerned inflation could settle below ECB’s 2% target, not above it.

Australia jobs fall -2.5k in May, but full-time hiring and hours worked offer Support

May’s Australian employment data surprised to the downside, with a -2.5k decline compared to expectations of a 19.9k gain. Yet beneath the weak headline, the composition was stronger than it appears: full-time jobs surged 38.7k while part-time jobs plunged by -41.1k.

Unemployment rate was unchanged at 4.1%, and the participation rate edged down from 67.1%to 67.0%, both suggesting a labor market that’s cooling slightly, but not cracking.

A sharp 1.3% mom rebound in total hours worked provides further reassurance, marking a recovery from recent holiday and weather-driven softness.

NZ GDP tops forecasts with 0.8% growth in Q1

New Zealand’s GDP grew 0.8% qoq in Q1, slightly ahead of expectations of 0.7% qoq. On a per capita basis, output rose 0.5% qoq.

Gains were broad-based, with all major sectors contributing positively: goods-producing industries led the way at 1.3% qoq, followed by primary industries at 0.8% qoq, and services at 0.4% qoq. Manufacturing and business services were standout performers among the detailed industries, helping to drive the recovery.

Despite the quarterly uptick, GDP contracted by 1.1% over the year to March 2025.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8133; (P) 0.8153; (R1) 0.8184; More….

Intraday bias in USD/CHF stays neutral at this point. On the downside, break of 0.8152 minor support will argue that recovery from 0.8054 has completed after failing 0.8247 resistance. Deeper fall should be see to 0.8038/54 support zone. Firm break there will resume larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Nevertheless, break of 0.8247 resistance will argue that corrective pattern from 0.8038 is starting the third leg. Bias will be turned back to the upside for 0.8475 resistance again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8656) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

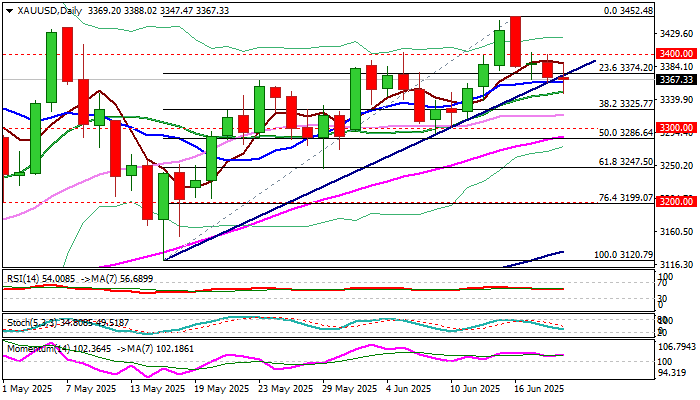

Gold Cracks Pivotal Support in Post-Fed Trading But Lacks Strength

Gold edged lower on Thursday following probe through pivotal supports at $3374/65 (Fibo 23.6% of $3120/$3452/trendline support/10DMA).

Near term sentiment weakened after Fed rate decision and comments from Chair Powell. Although Powell did not provide any new information regarding Fed’s policy outlook (Fed is likely to deliver two 0.25% rate cuts in 2025) but inflation outlook was upwardly revised, while predictions of economic growth were downgraded.

In addition, overheated geopolitical situation and continuous story about US tariffs, which also became key components, adds to uncertainty and hawkishly aligned overall message from Fed.

However, dips below pivotal supports were so far limited (contained by 20DMA at $3350) and struggling to verify break, keeping traders cautious and refraining from taking any stronger action.

Markets will look for today’s closing for fresh signals, although loss of $3374/65 zone might not be very harmful for larger bulls, as there is still plenty of space towards lower breakpoints at $3325/00 (Fibo 38.2% / psychological), where extended dips should find firm ground and still see pullback as a healthy correction.

High uncertainty over escalation of conflict in the Middle East is likely to continue to underpin the action and limit downside attempts, which would add to (still) preferred dip-buying scenario.

Technical picture on daily chart remains predominantly bullish as positive momentum is strong and MA’s are in almost full bullish configuration that contributes to scenario of healthy correction preceding fresh push higher.

Psychological $3400 level marks significant barrier, clear break of which to sideline downside risk and shift focus on target at $3452 (Jun 16 top) and key barrier at $3500 (new record high).

Res: 3388; 3400; 3437; 3452.

Sup: 3350; 3325; 3300; 3286.

ECB’s Villeroy: Next move could be a cut amid sub-2% inflation risks

French ECB Governing Council member Francois Villeroy de Galhau further easing could be on the table if inflation continues to drift below target.

“Barring a major exogenous shock, including possible new military developments in the Middle East, if monetary policy were to move in the next six months, it could be more in the direction of accommodation,” Villeroy said in a speech.

He highlighted that investors are increasingly concerned inflation could settle below ECB’s 2% target, not above it.

ECB’s Nagel: Monetary policy is on the right track

German ECB Governing Council member Joachim Nagel remarked today that with inflation nearing 2% on average this year, ECB is “more or less mission accomplished” on the price stability front. He added that rates are now in “neutral territory,” and monetary policy is "on the right track.

At the same conference, Vice President Luis de Guindos reiterated that the path forward will be data-dependent and decided on a meeting-by-meeting basis. He warned of elevated geopolitical risks, including trade tensions and Middle East conflict, which could alter both inflation and economic outlook.

BoE on hold, dovish undercurrent builds with 3 votes for cut

BoE left its policy rate unchanged at 4.25% today, as expected. The vote came in at 6–3, with Swati Dhingra, Dave Ramsden, and Alan Taylor opting for a 25bps cut. Known doves Dhingra and Taylor had pushed for a larger 50bps cut at last meeting. A surprise was that Ramsden who aligned with the majority last time and supported the 25bps cut. The voting marked a slight shift toward a more dovish stance.

In its accompanying statement, BoE acknowledged that underlying UK GDP growth has remained weak, and that labor market slack is becoming more evident. Inflation jumped to 3.4% in May, largely as expected. BoE expects inflation to hover around current levels through year-end before gradually falling toward the 2% target in 2026.

The statement also pointed to heightened geopolitical risks, particularly from the Middle East, as a complicating factor for inflation and energy costs. In light of this backdrop, the BoE reaffirmed that its next moves will be “gradual and careful” and emphasized that monetary policy decisions are “not on a pre-set path”.

(BOE) Bank Rate maintained at 4.25%

Monetary Policy Summary, June 2025

The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

At its meeting ending on 18 June 2025, the MPC voted by a majority of 6–3 to maintain Bank Rate at 4.25%. Three members preferred to reduce Bank Rate by 0.25 percentage points, to 4%.

There has been substantial disinflation over the past two years, as previous external shocks have receded, and as the restrictive stance of monetary policy has curbed second-round effects and stabilised longer-term inflation expectations. This has allowed the MPC to withdraw gradually some degree of policy restraint, while maintaining Bank Rate in restrictive territory so as to continue to squeeze out existing or emerging persistent inflationary pressures.

Underlying UK GDP growth appears to have remained weak, and the labour market has continued to loosen, leading to clearer signs that a margin of slack has opened up over time. Measures of pay growth have continued to moderate and, as in May, the Committee expects a significant slowing over the rest of the year. The Committee remains vigilant about the extent to which easing pay pressures will feed through to consumer price inflation.

Twelve-month CPI inflation increased to 3.4% in May from 2.6% in March, in line with expectations in the May Monetary Policy Report. The rise was largely due to a range of regulated prices and previous increases in energy prices. Consumer price inflation is expected to remain broadly at current rates throughout the remainder of the year before falling back towards target next year.

Furthermore, global uncertainty remains elevated. Energy prices have risen owing to an escalation of the conflict in the Middle East. The Committee will remain sensitive to heightened unpredictability in the economic and geopolitical environment, and will continue to update its assessment of risks to the economy.

There remain two-sided risks to inflation. Given the outlook, and continued disinflation, a gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate. Monetary policy is not on a pre-set path. At this meeting, the Committee voted to maintain Bank Rate at 4.25%.

The Committee will continue to monitor closely the risks of inflation persistence and what the evidence may reveal about the balance between aggregate supply and demand in the economy. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further. The Committee will decide the appropriate degree of monetary policy restrictiveness at each meeting.

Minutes of the Monetary Policy Committee meeting ending on 18 June 2025

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices.

The international economy

2: UK-weighted global GDP was estimated to have grown by 0.4% in 2025 Q1, in line with the projection in the May Monetary Policy Report. Since the MPC’s May meeting, the US administration had made progress in negotiating trade deals with the United Kingdom and China. The reduction in tariffs with China had reduced the US average effective tariff rate by just over a third. However, the future configuration of tariffs remained highly uncertain, with potential changes in tariff policy continuing to pose risks to global trade. Indices of trade policy uncertainty had also remained at elevated levels.

3: The impact of trade policies had been evident in activity data. For example, GDP and trade releases suggested that exports to the United States had been expedited ahead of tariffs taking effect. On the one hand, euro-area GDP had grown by a stronger-than-expected 0.6% in 2025 Q1, accounted for by strong exports and investment, and GDP in China had expanded by 1.2%, supported by net exports. On the other hand, US GDP had contracted by 0.1%, weaker than had been anticipated, as imports had significantly outstripped exports. There had also been some tentative evidence over recent months that goods from China destined for the United States were being shipped to other countries, including to Asia and Europe.

4: More timely PMI data had suggested some further front-loading of activity in the euro area with strong manufacturing PMIs but softer services PMIs in May, although front-loading was expected to unwind over the second quarter as a whole. In the United States, consumer confidence and investment intentions indicators had rebounded in May, although ISM manufacturing PMIs had been softer. The US House of Representatives had passed a fiscal bill with significant tax cuts. These were broadly in line with what had been incorporated in the May Report forecast. The bill had yet to be passed by the Senate.

5: The euro-area labour market had remained tight but had continued to gradually normalise, while the labour market in the United States had remained close to balance. Unemployment in these regions had remained low compared to historic averages. Indicators of pay growth had continued to moderate.

6: Annual headline consumer price inflation had continued to decrease in the euro area and in the United States. In the euro area, there was growing evidence that the 2021-2022 inflationary shock had been largely squeezed out of the system. Twelve-month HICP inflation had decreased to 1.9% in May, marginally below what had been expected in the May Report, while core inflation had also fallen to 2.3%. Lower services price inflation had accounted for the decrease in the headline figure. In the United States, CPI inflation had risen slightly to 2.4% in May, and core inflation had remained at 2.8%. There were few signs of tariffs impacting the latest US inflation data but some measures of short and medium-term household inflation expectations had continued to rise, possibly reflecting the anticipated impact of tariffs.

7: The Committee discussed cross-country trends in inflation. Both wage growth and consumer services price inflation had remained at more elevated levels in the United Kingdom than in the euro area or the United States. While in part reflecting greater persistence of inflation in the United Kingdom, for services, some of that difference could be accounted for by the greater contribution of regulated prices to UK inflation recently. Any such comparisons also needed to take account of differences in cyclical and structural factors.

8: The Brent oil spot price had increased by 26% to $79 per barrel since the MPC’s May meeting, in part reflecting an escalation of the conflict between Israel and Iran. European natural gas spot prices had also increased by 11%. Non-oil commodities prices were little changed.

Monetary and financial conditions

9: Some measures of global financial market volatility had fallen back since the MPC’s previous meeting, although they had remained elevated overall in light of continuing geopolitical and trade policy uncertainty. Across advanced economies, government bond yields had been little changed overall. At the short end of the curve, yields had initially risen following the May MPC meeting, accounted for partly by an easing in tariffs between the United States and China, although they had subsequently fallen back following data releases. At the long end of the curve, initial increases had been associated with an increase in term premia related to the fiscal outlook in a number of economies, before those yields had also fallen back.

10: Equity prices had recovered in these economies since their declines following the US administration’s tariff announcement in April. The US dollar effective exchange rate had depreciated further and was around 5% weaker than its level prior to the April tariff announcement, with some investors diversifying into, or hedging dollar exposures using, other currencies. This had contributed to the relative strength in the euro effective exchange rate.

11: At its meeting on 5 June, the ECB Governing Council had announced a 25 basis point reduction in its interest rates, in line with market expectations. At its May meeting, the Federal Reserve’s Federal Open Market Committee had maintained the target range for the federal funds rate at 4.25 to 4.5%.

12: Consistent with moves in other advanced economies, gilt yields had initially risen and then fallen back, while UK equity prices were slightly higher since the MPC’s previous meeting. There had been a small appreciation in the sterling effective exchange rate. In the Bank’s latest Market Participants Survey (MaPS), the median profile for CPI inflation implied a peak of 3.4% in the third quarter of this year, a slight increase relative to expectations in the previous survey. The median respondent had continued to expect inflation to be at the 2% target at the three-year horizon. There had been little change in medium-term UK financial market inflation compensation measures.

13: Market expectations were for Bank Rate to remain unchanged at this meeting. The median MaPS respondent was expecting 50 basis points of Bank Rate cuts this year, unchanged from the May survey and broadly in line with what was implied by market pricing. The distribution of Bank Rate expectations had shifted upwards relative to the May survey, consistent with the relatively shallower profile of cuts implied by market pricing, albeit with market contacts continuing to emphasise ongoing economic uncertainty.

14: Underlying trends in money and credit data had been consistent with the assessment set out in the May Monetary Policy Report, though with some recent and temporary volatility associated with the bringing forward of house purchases ahead of increases in the Stamp Duty Land Tax that had come into effect in April. Given market-implied expectations for a shallower profile of Bank Rate since the MPC's previous meeting, quoted rates on some mortgage rates had increased slightly, consistent with a pace of pass-through in line with historical experience.

Demand and output

15: UK GDP had increased by 0.7% in 2025 Q1, a little stronger than had been expected in the May Monetary Policy Report. Household consumption had risen by 0.2%, while business investment had increased by 5.9% following a weak 2024 Q4 outturn. Net trade excluding valuables was estimated to have made a positive contribution to quarterly growth, of 0.6 percentage points, while the change in inventories had contributed 0.2 percentage points to growth. Both of these components of GDP could have been affected by a front-loading of activity ahead of the imposition of new tariffs by the United States and related trade policy developments.

16: Monthly GDP had fallen by 0.3% in April, following fairly strong increases over previous months. The latest data appeared to have been affected by the front-loading of activity ahead of the increases in Stamp Duty Land Tax and in Vehicle Excise Duty in April. There had also been some evidence that the temporary boost to trade ahead of the imposition of new tariffs had unwound, with goods exports to the United States recording their largest ever monthly fall in April. Overall, the monthly path of output suggested that quarterly GDP growth was likely to fall back to around ¼% in 2025 Q2, slightly higher than had been expected at the time of the May Report.

17: Business surveys had continued to point to weak underlying GDP growth. For example, although the S&P Global UK composite PMI output index had risen to above 50 in May, it had remained some way below its historical average. Textual analysis of PMI responses by Bank staff suggested that global concerns had played a larger role in its weakness over recent months, relative to domestic factors. That said, most companies responding to the latest DMP Survey were not expecting tariffs to have a material impact on their sales and investment, and had judged that uncertainty around US tariffs fell between April and May. Agents’ intelligence suggested that business sentiment had continued to wane, with contacts not expecting to see a material recovery in demand until 2026. Taken together, the steer from surveys over recent months had remained consistent with a zero to slightly positive pace of underlying growth currently.

18: The Committee discussed the divergent signals on the strength of activity over recent months. Surveys had historically tended to give a less volatile steer on GDP growth, but they could also be affected excessively by swings in sentiment that were not ultimately reflected in firms’ output. Recent developments in output also needed to be considered in the wider context of the supply side of the economy, and the opening up of slack in the labour market and within companies. The Committee was continuing to monitor indicators of UK economic uncertainty and its impact on investment decisions.

19: Spending Review 2025 had agreed departmental settlements within the envelope for total government spending that had been confirmed at the Spring Statement in March. Budgets had now been set until 2028‑29 for day-to-day resource spending and until 2029-30 for capital spending.

Supply, costs and prices

20: Issues with the quality of the official data, including relating to the labour market, continued to be an area of concern for the MPC. The Committee therefore continued to draw on a wide range of information beyond the official data to inform its judgements on the conjuncture. These sources included business surveys and intelligence from the Bank’s Agents.

21: Several indicators of labour demand and firms’ hiring intentions had softened further in recent months. The ONS/HMRC PAYE estimate of payrolled employees had fallen by 0.4% in the three months to May, with a single-month decline of 109,000 in May that had been the largest monthly contraction since May 2020. Revisions to early vintages of the HMRC data could be large and, given the earlier timing of the data extraction for May, the latest HMRC data were more uncertain than usual. That said, survey-based measures of the labour market, such as the employment component of the S&P Global UK composite PMI, the permanent staff placements component of the KPMG/REC Report on Jobs and the latest Agents’ intelligence on recruitment difficulties, corroborated this pattern of ongoing loosening. A measure of underlying employment growth developed by Bank staff continued to suggest a subdued rate of near-zero employment growth.

22: The ratio of vacancies to unemployment had continued to fall below Bank staff’s estimate of its equilibrium level. The net additional hours desired by workers, as a percentage of average hours worked, had risen to its highest level since March 2015 in 2025 Q1. The overall weakening in these early-stage indicators of the tightness of the labour market suggested that some modest deterioration in late-stage indicators, such as the unemployment rate and the redundancy rate, should be expected over the coming months. Churn in the labour market had remained subdued, with outflows from unemployment gradually edging lower. Taken together, the analysis conducted by Bank staff implied that slack was continuing to emerge in the labour market but there were no strong signs, as yet, that a more abrupt loosening was underway.

23: A broad set of indicators suggested that underlying pay growth had eased further in recent months, albeit to a still elevated level and above what could be explained by economic fundamentals. Private sector regular average weekly earnings (AWE) growth had fallen to 5.1% in the three months to April, down from 5.5% in March. Annual pay growth in retail and hospitality had been 6.7% in April, in line with the increase in the National Living Wage. Higher-frequency estimates of AWE growth continued to indicate an annualised run-rate of around 5%. The timelier ONS/HMRC PAYE proxy for private sector pay had edged lower from 5.8% in April to 5.7% in May.

24: The latest data on pay settlements and pay expectations had remained on track with the May Monetary Policy Report projection for a significant decline in wage growth. Data from the Bank of England’s and Brightmine’s settlements databases suggested that the median rate of pay awards had remained at around 3 to 4% since the start of the year, although these estimates had continued to be based on incomplete samples. The latest intelligence from the Agents had continued to suggest average pay settlements for 2025 of 3.5 to 4%, consistent with the range reported in the Agents’ annual pay survey that had been conducted ahead of the February Report. The MPC continued to monitor closely the flow of pay settlements information and other data that would enhance the Committee’s visibility on the prospective path of pay growth.

25: Twelve-month CPI inflation had been 3.4% in May, following 2.6% in March and 3.5% in April. The rise since March had largely been due to a range of regulated prices and previous increases in energy prices. The April CPI release had triggered the exchange of open letters between the Governor and the Chancellor of the Exchequer that was being published alongside these minutes. The May outturn had been in line with expectations in the May Report. Core CPI inflation had been 3.5% in May, around 0.2 percentage points lower than expectations at the time of the May Report.

26: The ONS had announced in June that an error had been identified in an extract of the licensed vehicles data provided to the ONS by the Department for Transport. These data had been used to calculate the April 2025 Vehicle Excise Duty component of consumer price inflation. The error had resulted in an overstatement of the headline CPI by 0.1 percentage points for the published April 2025 figure only. The error had been corrected in the May data, such that going forward only the year-on-year rate of CPI inflation in April of next year would be distorted.

27: Core consumer goods price inflation had risen to 1.6% in May, alongside a material increase in food consumer price inflation, to 4.4%. Meat, chocolate and non-alcoholic drinks had exhibited the strongest inflation rates, consistent with higher wholesale prices for beef, cocoa beans and coffee. Agency intelligence had also highlighted the impact of labour and packaging regulation costs.

28: Consumer services price inflation had returned to 4.7% in May, having risen from that level in March to 5.4% in April. Underlying services price inflation had remained elevated across a broad range of measures, regardless of whether they were based on exclusionary, trimming or reweighting approaches. While these had been on a downward trajectory, there had been little change in the higher-frequency pace of underlying services price inflation since late 2024.

29: CPI inflation was expected to remain just under 3½% for the remainder of the year, with a brief increase to 3.7% in September. This profile was broadly unchanged from the projection made at the time of the May Report, although the pass-through to prices from National Insurance contributions, from regulatory changes and from some food input costs continued to require monitoring.

30: Some indicators of households’ short- and medium-term inflation expectations had fallen back in the latest data, but had remained at the upper end of the range of rates explicable by the path of consumer price inflation. The Citi/YouGov measure of median one-year ahead inflation expectations had declined to 4.0%, while the Bank/Ipsos measure had fallen to 3.2%. The increases in household expectations prior to the latest data could be explained by the response of households to actual inflation, in particular to increases in the prices of salient items such as food and energy prices. Nevertheless, this represented an upside risk to future pay and inflation dynamics. Medium-term measures of inflation expectations from these surveys had also remained elevated.

31: Measures of businesses’ inflation expectations had remained elevated but to a lesser extent than household measures. According to the DMP Survey, businesses’ year-ahead own-price expectations had fallen from 4.0% in the three months to February to 3.7% in the three months to May. Year-ahead CPI expectations had stood at 3.2%, up slightly from 3.1% in the three months to February.

The immediate policy decision

32: The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

33: The Committee considered the news since the previous MPC meeting, particularly the extent to which it was sufficient to change members’ views on domestic inflationary pressures and hence the required stance of monetary policy.

34: Underlying UK GDP growth appeared to have remained weak and the labour market had continued to loosen. While there remained uncertainties around the balance of supply and demand in the economy, there was clearer evidence that a margin of slack had opened up over time in the labour market as had been expected. Members noted the continuing weakness in job vacancies, in the ratio of vacancies to unemployment relative to its estimated equilibrium level, and in ONS/HMRC PAYE payrolls even with less weight placed on the most recent data point, alongside the increase in net additional hours desired by workers.

35: Measures of pay growth had continued to moderate and, as in May, the Committee expected a significant slowing over the rest of the year. This was consistent with the now-more-representative sample of recorded pay settlements this spring, and with the broadly unchanged signals from the DMP Survey and Agents’ intelligence. The growing margin of slack in the labour market pointed to limited pay drift going forward. The Committee remained vigilant about the extent to which easing pay pressures would feed through to consumer price inflation.

36: Twelve-month CPI inflation had increased to 3.4% in May from 2.6% in March, in line with expectations in the May Monetary Policy Report. The rise had been largely due to a range of regulated prices and previous increases in energy prices. Services price inflation had been unchanged from March, at 4.7%. Food price inflation had risen materially in May, which might prove salient for households’ formation of inflation expectations. There had been some signs of levelling off in indicators of household expectations, but both household and business inflation expectations remained elevated. Financial market measures of inflation compensation were in contrast more subdued.

37: Consumer price inflation was expected to remain broadly at current rates throughout the remainder of the year before falling back towards target next year. While base effects would start to work to bring inflation down in 2025 Q4 and 2026 Q1, more pronounced disinflation was needed to ensure CPI inflation declined back towards the 2% target consistent with the baseline projection in the May Report.

38: The Committee remained focused on returning inflation sustainably to the target. Alongside the baseline forecast, the May Report had set out two illustrative scenarios. In one scenario, there could be weaker supply and more persistence in domestic wages and prices, including from second-round effects related to the near-term increase in CPI inflation. In another scenario, inflationary pressures could ease more quickly owing to greater or longer-lasting weakness in demand relative to supply, in part reflecting uncertainties globally and domestically. The mechanisms underlying both scenarios remained relevant for the Committee’s deliberations, set alongside a broader assessment of risks.

39: Recent developments had highlighted a broad range of global risks, including but not restricted to trade policy. Global uncertainty remained elevated.

40: Based on the latest constellation of tariff announcements, provisional Bank staff analysis suggested that the direct impact of the trade shock on world GDP could be smaller than the Committee had expected in the May Report. Trade policy uncertainty would nevertheless continue to have an impact on the UK economy.

41: There had been rapid geopolitical developments in the lead up to this MPC meeting. Energy prices had risen owing to an escalation of the conflict in the Middle East. The Committee would remain vigilant about these developments and their potential impact on the UK economy.

42: Although monetary policy had been eased over the past year, the Committee had retained a restrictive stance in order to continue to squeeze out persistent inflationary pressures. There was a range of views among members on the remaining degree of restrictiveness.

43: All members stressed that monetary policy was not on a pre-set path. The Committee would remain sensitive to heightened unpredictability in the economic and geopolitical environment, and would continue to update its assessment of risks to the economy.

44: Six members preferred to maintain Bank Rate at 4.25%. Disinflationary progress had continued, but there was not a strong case for a further easing of monetary policy at this meeting. Inflation seemed likely to stay around 3½% over the second half of 2025 before falling back towards the target from next year. There had generally been some greater signs of disinflationary pressures from the labour market, both in terms of quantities and wages, than from developments in domestic prices. Recent global developments had not had a significant impact on this meeting’s policy decision.

45: The risks around the medium-term path of CPI inflation remained two-sided. Assessing the pace of disinflation would continue to be key for these members in reaching a view on how quickly to remove remaining policy restraint. That assessment was likely to include a number of elements. Signs of weak demand, for example as a result of continued high saving, could lead to a more rapid opening up of slack in the labour market. In contrast, supply side constraints, such as continued weakness in productivity, or structural change in goods and labour markets could contribute to inflationary pressures. Inflation persistence could also be generated by higher food prices raising inflation expectations, impacting wage and price setting behaviours.

46: Three members preferred a 0.25 percentage point reduction in Bank Rate at this meeting. The cumulative evidence from a range of labour market data pointed to a material further loosening in labour market conditions. Private sector regular wage growth had come in lower than expected, while incoming pay settlements data had continued to be close to the Agents’ annual pay survey figure for the end of 2025, and were approaching sustainable rates. Consumer spending and underlying growth had remained subdued, alongside ongoing risks to global growth. The disinflation process was continuing, with the most significant contributions to the pickup in headline inflation coming from one-off tax and administered prices, though with uncertainty from global developments that needed monitoring. In the medium term, a continued monetary policy stance that was too restrictive risked inflation deviating from the 2% target on a sustained basis and the opening up of an unduly large output gap. Given this balance of risks, a less restrictive policy path was warranted.

47: Given the outlook, and continued disinflation, a gradual and careful approach to the further withdrawal of monetary policy restraint remained appropriate. The Committee would continue to monitor closely the risks of inflation persistence and what the evidence might reveal about the balance between aggregate supply and demand in the economy. Monetary policy would need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term had dissipated further. The Committee would decide the appropriate degree of monetary policy restrictiveness at each meeting.

48: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be maintained at 4.25%.

49: Six members (Andrew Bailey, Sarah Breeden, Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) voted in favour of the proposition. Three members (Swati Dhingra, Dave Ramsden and Alan Taylor) voted against the proposition, preferring to reduce Bank Rate by 0.25 percentage points, to 4%.

Operational considerations

50: On 18 June, the stock of UK government bonds held for monetary policy purposes was £590 billion.

51: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Sam Beckett was present as the Treasury representative.

Jonathan Bewes was also present on 9 June, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank’s Court of Directors.

Silver Price Retreats from 2012 Highs

As shown on the XAG/USD chart, the price of silver climbed above $37 per ounce yesterday — a level not seen since 2012. However, this morning, the price has dropped by approximately 2.5% from yesterday’s peak.

The bullish driver behind the rally has been fears that the US could become involved in a military conflict between Israel and Iran. Concerns in financial markets intensified after media reports stated that US officials are preparing for a potential strike on Iran.

Another factor influencing silver's price was the Federal Reserve’s decision to keep interest rates unchanged and maintain a cautious policy stance. Yesterday, Jerome Powell warned that President Trump’s tariffs could fuel inflation (a bullish signal for silver) and complicate the economic outlook.

Technical Analysis of the XAG/USD Chart

In our previous analysis of the XAG/USD chart, we identified an upward channel. This channel remains relevant, though its configuration has shifted.

The price of silver remains in the upper part of the channel (a sign of strong demand). However, two signals suggest a potential correction may develop:

→ A bearish divergence on the RSI indicator;

→ A sharp decline from the channel’s upper boundary (marked with a red arrow), breaking through the local line that divides the upper half of the channel into quarters.

Nevertheless, given the scale of geopolitical risks, there is a chance that the bears may struggle to significantly shift the trend — especially with markets nearing the weekend closure.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Dow Futures (YM) Elliott Wave Outlook: Wave 4 Correction Underway

The rally in Dow Futures (YM) that began from the April 7, 2025 low remains intact. It is unfolding as a five-wave impulse pattern according to Elliott Wave analysis. Starting from that low, wave 1 peaked at 39,649. A corrective pullback in wave 2 followed which found support at 36,922. The Index then resumed its upward trajectory in wave 3, which itself subdivides into five smaller-degree waves. As shown on the 1-hour chart below, wave 3 reached its high at 43,316. The market is now experiencing a pullback in wave 4.

Wave 4 is taking shape as a double three structure, a corrective pattern characterized by multiple sub-waves. From the wave 3 high, wave (a) declined to 42,518, followed by a wave (b) rally that topped at 42,944. The subsequent wave (c) dropped to 42,223, completing the first leg of the double three, labeled wave ((w)). The Index then rallied in wave ((x)), peaking at 43,069. Then it turns lower in wave ((y)), which also unfolds as a double three. Within this structure, wave (w) ended at 42,424, and a corrective wave (x) rally concluded at 42,860. The Index is now expected to extend lower in wave (y) of ((y)), targeting the 41,297–41,972 range. This decline should finalize wave 4, setting the stage for a potential wave 5 rally to new highs.

Dow Futures (YM) 60-Minute Elliott Wave Technical Chart

YM Elliott Wave Technical Video

https://www.youtube.com/watch?v=AzQ9N0tT8U4