Sample Category Title

Japan’s trade deficit widens as imports surge, exports to China drop

Japan’s trade deficit expanded sharply in January, reaching JPY -2.759T, the largest shortfall in two years, as imports surged 16.7% yoy, far exceeding the expected 9.3% yoy gain.

Meanwhile, exports rose 7.2% yoy, falling slightly short of the 7.7% yoy forecast, with strong shipments to the U.S. (+18.1% yoy) offset by a -6.2% yoy decline in exports to China.

On a seasonally adjusted basis, exports declined -2.0% mom to JPY 9.253T, while imports climbed 4.7% mom to JPY 10.109T, leading to a JPY -857B trade deficit.

Gold (XAU/USD) Eyes Fresh Highs, US-Russia Talks Fail to Quell Haven Demand

- Geopolitical tensions continue to support gold prices despite talks between the US and Russia, and a potential phase two deal between Israel and Hamas.

- Gold has held above the $2900/oz level to start the week, but the RSI indicates it is in overbought territory.

- The article identifies key support levels for gold at 2924, 2913, and 2882, and resistance levels at 2937, 2942, and 2950.

Risk aversion persisted in the markets today, even as a U.S.-Russia meeting in Saudi Arabia sparked hopes for a potential decline in safe-haven demand. Additionally, reports emerged of a phase two agreement being reached between Israel and Hamas.

Both developments carried the expectation of easing the geopolitical tensions that have weighed on global sentiment over the past 12 to 18 months. However, these events have so far failed to significantly alleviate the sense of geopolitical risk, keeping haven demand firmly in place.

US-Russia Talks in Saudi Arabia

A US and Russian delegation met in Saudi Arabia today to discuss a potential end to the Ukraine conflict. Market participants may have been eyeing a drop in geopolitics which may lead to a drop in Gold prices as haven demand falls. However this failed to materialize despite reports that the talks were positive.

Key Quotes and Reports from the Meeting from Both US and Russian Officials:

- US, Russia Agree To Appoint Teams To End Ukraine Conflict – US Official

- US Spox Bruce: One Call One Meeting Not Enough For Enduring Peace

- Russia’s Dmitriev: Russian, US Officials Have Separate Discussion On Future Economic Cooperation, Including Global Energy Prices – RTRS

- US, Russia Peace Proposal Would Include Ukraine Elections – Fox

- US State Sec Rubio: US, Russia Agree To Restore Embassy Staffing -AP

- U.S. National Security Adviser Waltz: There Will Be Talks About Territory And Security Guarantees

- US Sec Of State Rubio: Everyone Involved In Conflict Has To Be Part Of Talks

- US Sec Of State Rubio: European Union Needs To Be Involved At Some Point

- US National Security Adviser Waltz: US Allies Are Being Consulted On Ukraine

- US National Security Adviser Waltz: US Is Glad Europe Is Talking About Contributing More Forcefully To Ukraine Security

- Russia’s ForMin Lavrov: We Agreed To Form Process For Ukraine Conflict Settlement

- Russia’s ForMin Lavrov: There Were Also High Interest To Lift Barriers For Economic Cooperation

- Russia’s ForMin Lavrov: European Troops In Ukraine Is Unacceptable For Russia

- Russia’s ForMin Lavrov: I Can Say That Today’s Talks Were Not Unsuccessful

Despite the comments by Russia’s Foreign Minister Lavrov that the talks were not unsuccessful, the road ahead may be a long and bumpy one. Ukrainian President Volodymyr Zelenskiy announced that his visit to Saudi Arabia has been rescheduled for March 10th, as he awaits the arrival of the U.S. delegation in Kyiv. This could explain why markets have not had any meaningful reaction as of yet.

Israel-Hamas Phase Two Deal Appears on Course

In another positive for risk sentiment, both sides appear ready to discuss phase two of the ceasefire. Israeli Foreign Minister Gideon Saar stated that negotiations for the second phase of the hostage deal will commence soon. This view was echoed by Hamas Gaza Chief Hayya, who announced that the group is prepared to begin immediate negotiations for the second phase of the Gaza ceasefire agreement.

Another potential positive for geopolitical risk. Israeli Foreign Minister meanwhile acknowledged he is aware that Arab states are coming up with a plan for Gaza as Egyptian President Sisi is set to travel to Saudi Arabia for discussions. On the flip side however, the Israeli Foreign Minister has said they are unwilling to accept or support a plan that would see civilian control of Gaza transferred from Hamas to the Palestinian Authority.

Tariff Developments and the Week Ahead

The Dollar has so far had a limited impact on Gold prices. We have seen spikes when key data has missed estimates but the precious metal quickly recovers. This is a sign that haven demand and risk sentiment remains skewed in favor of further gains for Gold prices.

Tariffs by the US have heated up as well which continues to support Gold prices. President Trump has said that tariffs on automobiles would come on April 2, while Chinese lithium company Jiangsu Jiuwu Hi-Tech halted exports of processing equipment per LSEG.

Signs that a global trade war remains a massive concern for market participants moving forward.

On the data front, the FOMC minutes will be out on Wednesday followed by S&P PMI data on Friday. Both of these events could lead to a spike in volatility but i do expect any moves to prove short-lived.

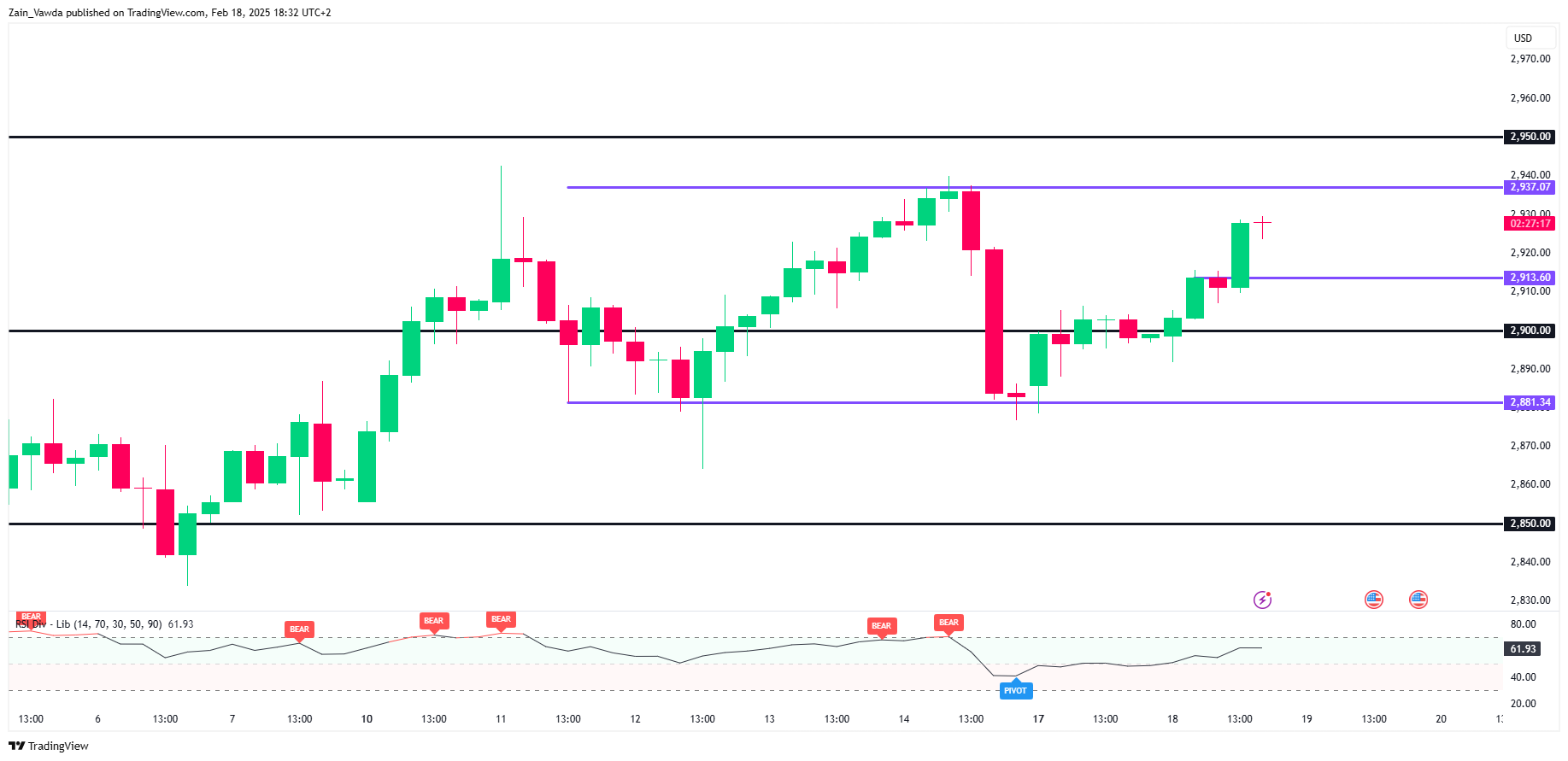

Technical Analysis – Gold (XAU/USD)

Gold prices did experience a pullback last week following hotter than expected inflation data from the US. However this proved short lived as prices retested its alltime highs around the 2942/0z handle.

On the daily timeframe the RSI period 14 is back in overbought territory. As we know though, an instrument can remain in overbought territory for extended periods of time.

Gold (XAU/USD) Daily Chart, February 18, 2025

Source: TradingView (click to enlarge)

Dropping down to a four-hour chart H4, markets are in a sort of range with highs around 2937 and lows around 2881.

A rejection at 3937 could lead to a retest of support at 2924 and 2913 before the 2900 comes into focus.

On the upside, a break of 2927 and the all-time high at 2942 will see focus shift toward the 2950 and 2975 resistance handles.

Gold (XAU/USD) Four-Hour H4 Chart, February 18, 2025

Source: TradingView (click to enlarge)

Support

- 2924

- 2013

- 2900

Resistance

- 2937

- 2942

- 2950

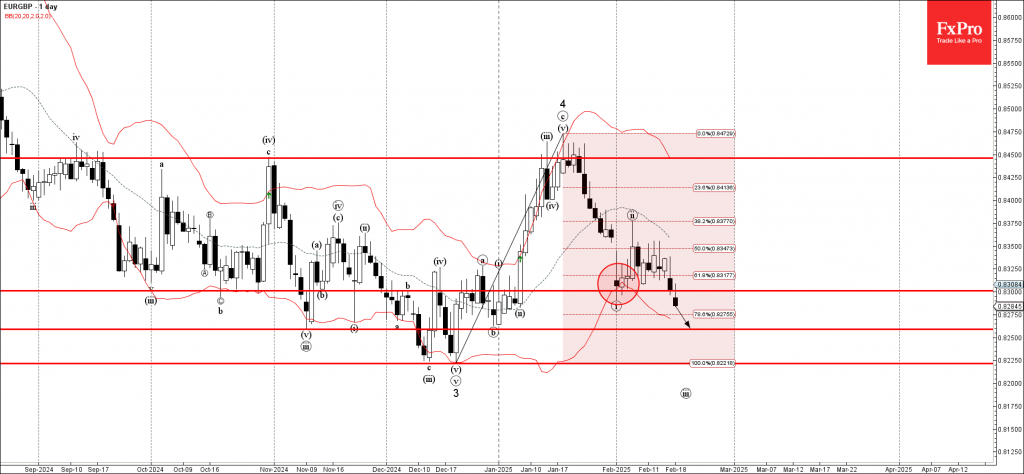

EURGBP Wave Analysis

- EURGBP broke the support zone

- Likely to fall to support level 0.8265

EURGBP currency pair recently broke the support zone between the support level 0.8300 (which stopped the previous impulse wave i at the end of January) and the 61.8% Fibonacci correction of the upward ABC correction 4 from December.

The breakout of this support zone accelerated the active short-term impulse wave iii of the higher order impulse wave 5 from January.

EURGBP currency pair can be expected to fall to the next support level 0.8265 (former low of the minor correction b from the end of December).

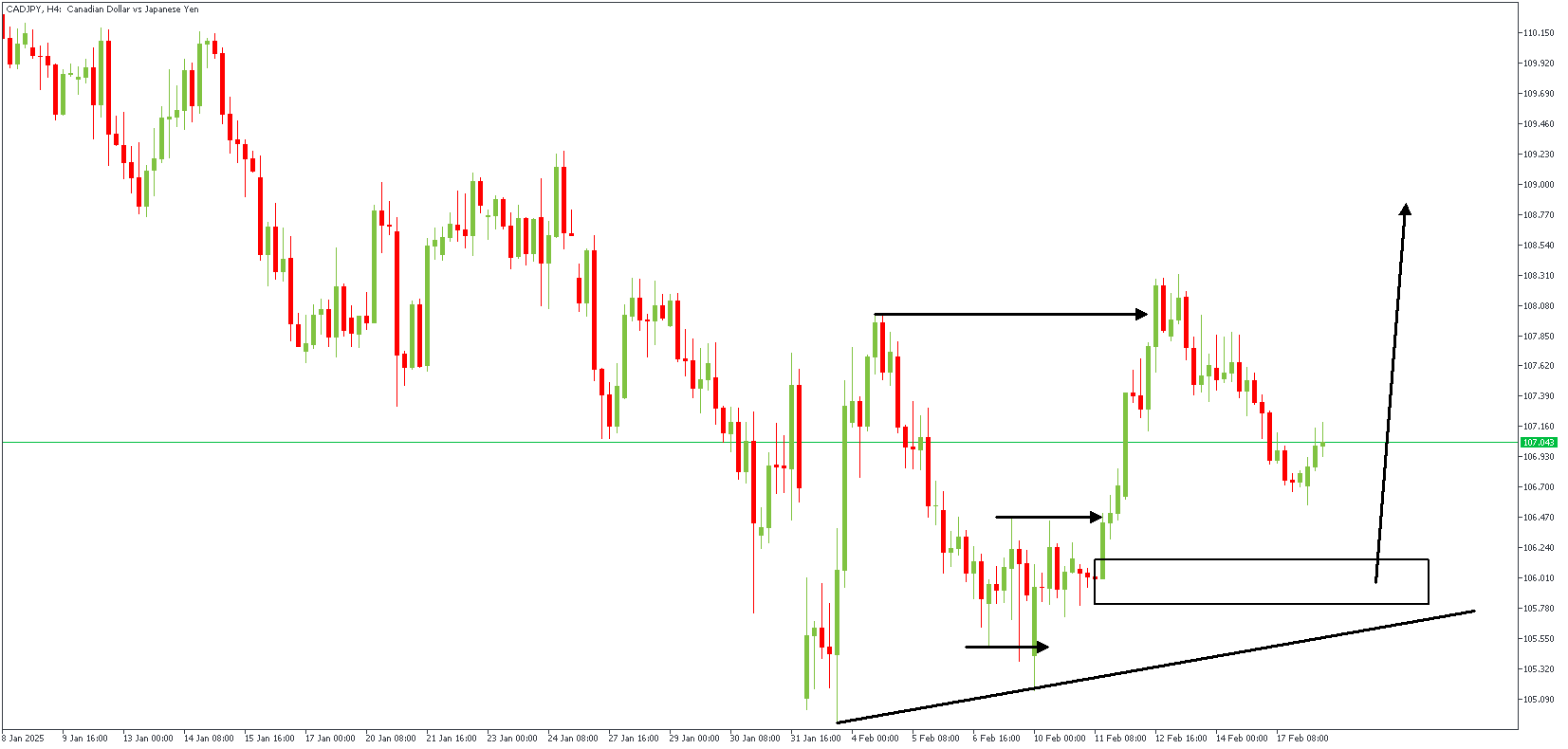

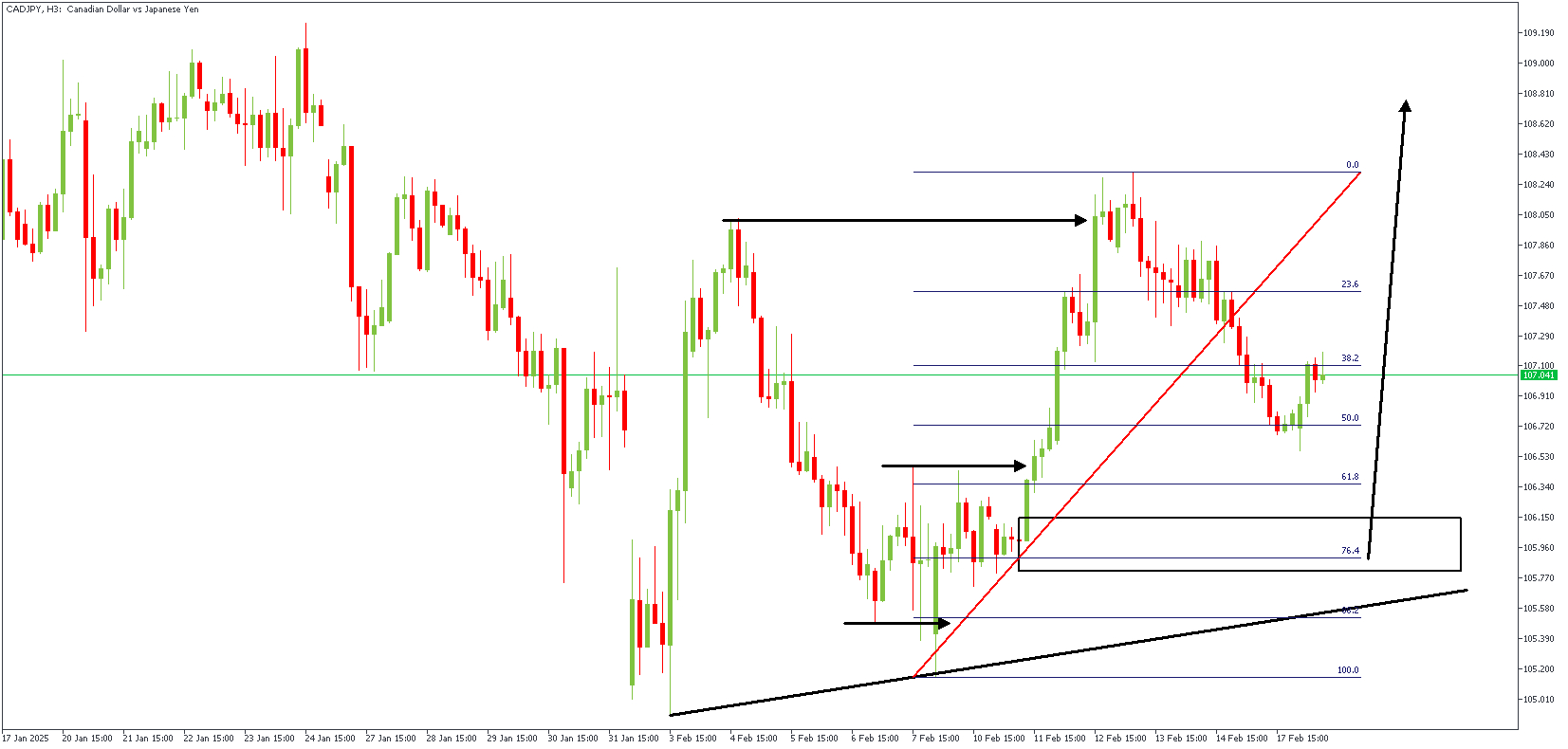

CADJPY Technical Analysis

The Japanese Yen (JPY) is trading weakly in the European session but is not falling sharply because many traders believe that the Bank of Japan (BoJ) will raise interest rates again. Additionally, the gap between Japanese and US bond yields is narrowing as investors expect the US Federal Reserve (Fed) to cut interest rates soon. This has helped to limit losses for the Yen.

On the other hand, positive news about a delay in US President Donald Trump's reciprocal tariffs and ongoing peace talks between Russia and Ukraine are reducing demand for the safe-haven JPY. At the same time, rising US Treasury bond yields support the US Dollar (USD), helping it recover from a three-day losing streak and keeping the USDJPY pair positive.

CADJPY – H4 Timeframe

CADJPY has recently broken above the previous high on the 4-hour timeframe chart, leaving an FVG (Fair Value Gap) and a drop-base-rally demand zone behind, near the origin of the bullish momentum. The presence of a trendline support further affirms the bullish sentiment.

CADJPY – H3 Timeframe

The 3-hour timeframe chart of CADJPY shows the price retracing towards the demand zone at the base of the bullish break. This demand also serves as the order block from the SBR (Sweep Break Retest) pattern and overlaps the 76% Fibonacci retracement level. Considering the trendline support's presence, the price is expected to bounce off the demand to resume the bullish impulse.

Analyst's Expectations:

- Direction: Bullish

- Target- 108.667

- Invalidation- 105.088

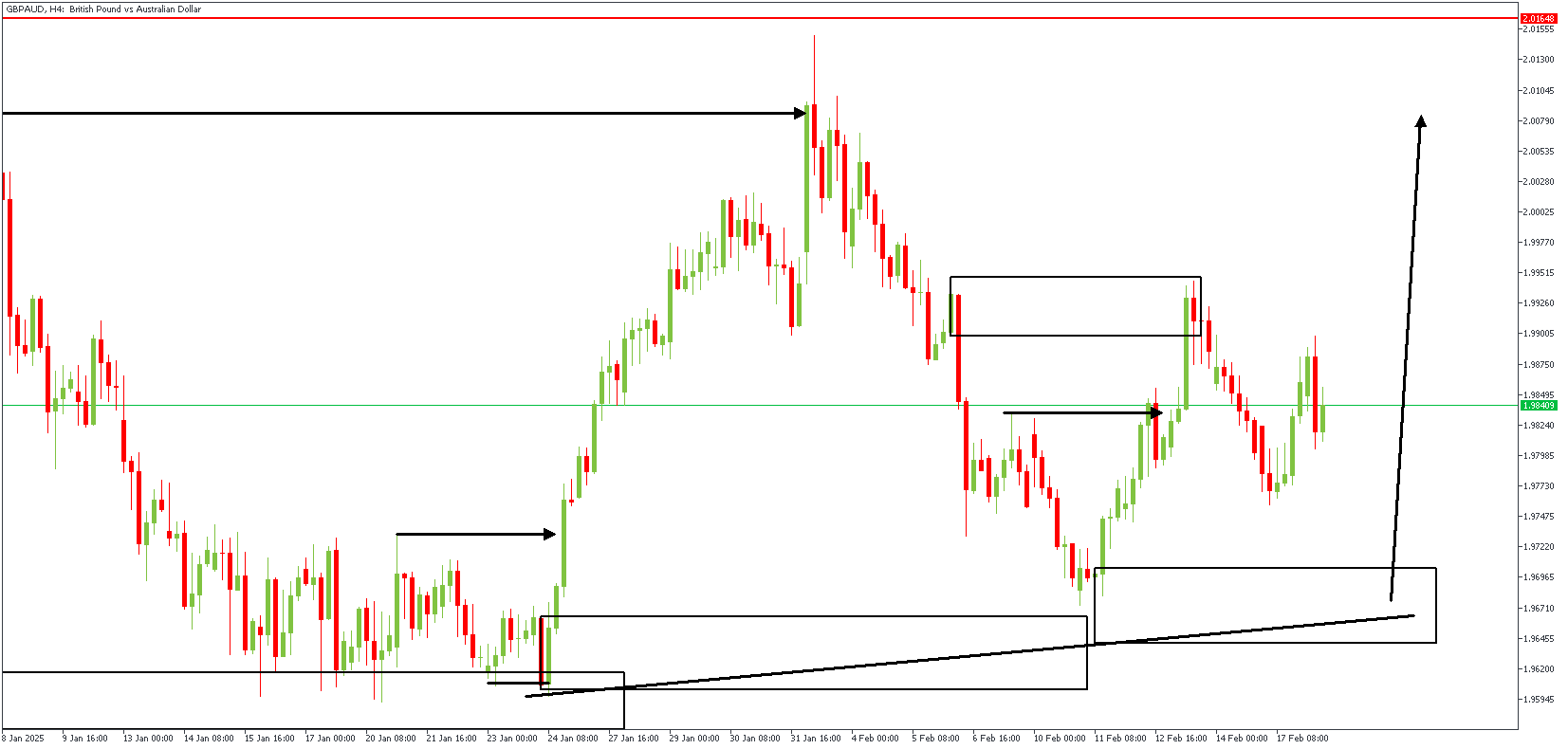

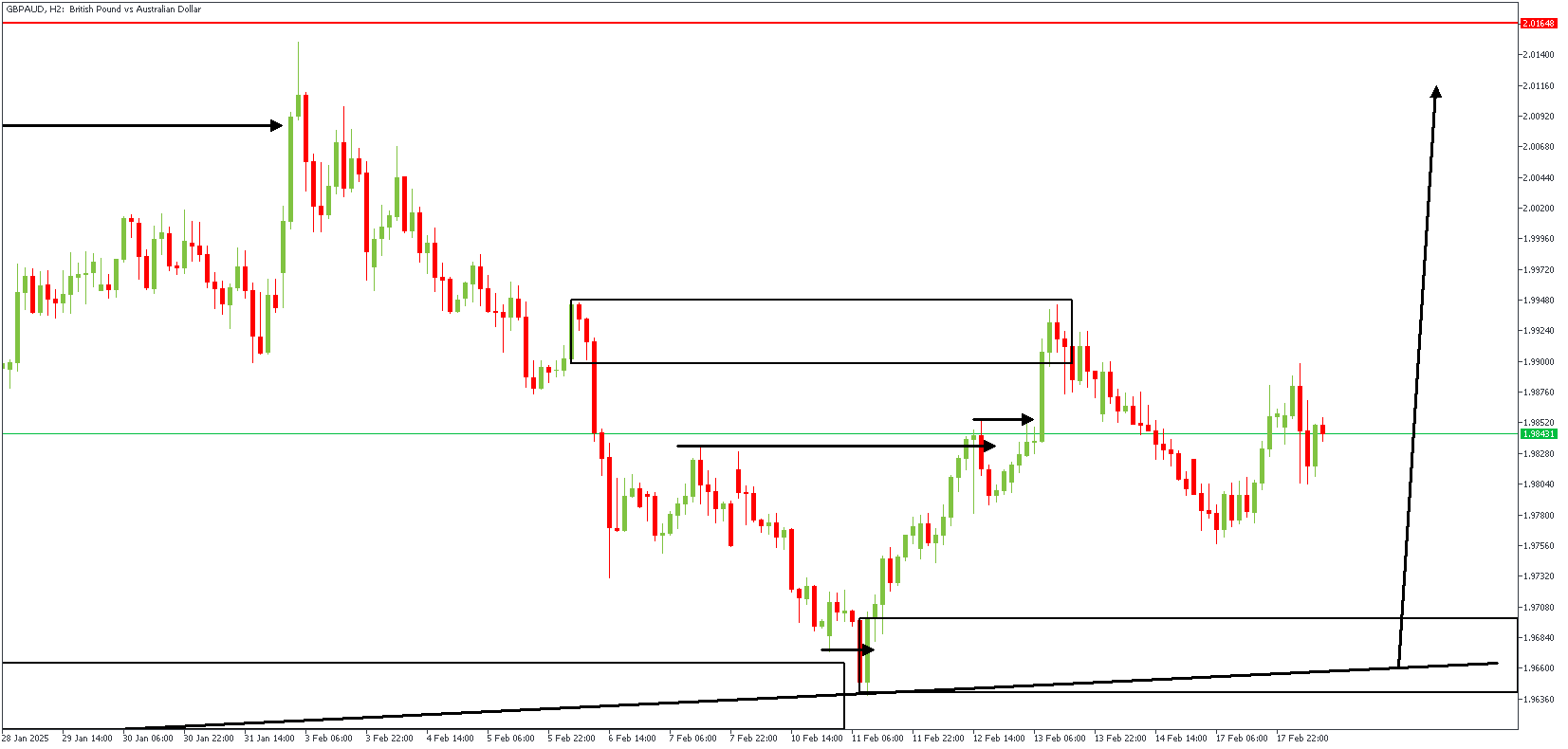

GBPAUD Technical Analysis

The British Pound (GBP) is slightly weaker than the US Dollar (USD), down by about 0.2%, while the USD remains strong. According to Shaun Osborne, Chief FX Strategist at Scotiabank, the Pound is struggling to keep its gains despite positive news about wages and jobs in the UK.

Recent data showed that wages in the UK grew by 6.0% for the three months ending in December, which was better than expected. Additionally, more people found jobs than analysts had predicted. This has reduced expectations of interest rate cuts from the Bank of England (BoE), aligning with the BoE’s cautious approach to lowering rates.

Even though the Pound gained some strength last week, it struggled to surpass the 1.2610 level against the USD, a key resistance point. The Pound has been moving around the 1.26 mark for the past two days without making significant progress. If it drops below 1.2580, it could fall further to the 1.2525/30 range.

GBPAUD – H4 Timeframe

The 4-hour timeframe chart of GBPAUD shows the price reacting off the confluence area of a trendline support and a drop-base-rally demand zone. The initial momentum has declined, allowing for a bearish retracement and a possible retest of the trendline support.

GBPAUD – H2 Timeframe

The 2-hour timeframe chart of GBPAUD further clarifies the original bullish sentiment on the higher timeframe. It presents an SBR (Sweep Break Retest) pattern with the demand zone lying around the 88% Fibonacci retracement level. The confluence from the trendline support confirms a bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 2.00705

- Invalidation: 1.95451

New Zealand Dollar Slips Ahead of Expected RBNZ Cut

The New Zealand dollar is sharply lower on Tuesday. NZD/USD is trading at 0.5700 in the North American session, down 0.62% on the day.

RBNZ expected to chop rates by 50 basis points

The Reserve Bank of New Zealand meets on Wednesday for the first time this year. The RBNZ lowered rates by a half-point at the last meeting on Nov. 27 and the markets have priced in another half-point cut on Wednesday at 90%, which would bring the cash rate down to 3.75%. The central bank held rates for over a year but has aggressively cut rates by 125 basis points in the current easing cycle.

The RBNZ has telegraphed its plan to cut rates by a half-point on Wednesday and we could see a limited response from the New Zealand dollar, since the decision has been priced in. Still, the US/New Zealand rate differential will widen and that could spell headwinds in the near term for the New Zealand dollar, which plunged 13% in the fourth quarter 2024 but has gained 1.9% since Jan 1.

What can we expect from the RBNZ after tomorrow’s anticipated rate cut? The RBNZ’s updated forecasts are expected to show the cash rate declining towards 3 percent, but in smaller increments of quarter-point cuts. This will depend on the strength of the economy and the direction of inflation. Another factor which could affect the rate path is the new US administration which has already started imposing tariffs.

New Zealand is vulnerable to US tariffs as the US is its second-largest trading partner, accounting for about 12% of New Zealand exports. Even if the US does not target New Zealand with tariffs, the trade war between the US and China has clouded the inflation outlook and is will likely hamper global growth.

NZD/USD Technical

- NZD/USD is putting pressure on support at 0.5691. Below, there is support at 0.5643

- 0.5781 and 0.5829 and the next resistance lines

Sunset Market Commentary

Markets

The focus of markets (and the international community) was on the talks in Riyadh between Russia and the US to end the war in Ukraine. The two parties agreed to appoint high-level teams to work ‘on a path to ending the conflict in Ukraine as soon as possible in a way that is enduring, sustainable, and acceptable to all sides’. For now, this brought little new for markets. Returning after the long weekend, US yields are rising between 2 bps (2-y) and 4.5 bps (30-y). Fed’s Waller indicated to leave rates unchanged until inflation moderates further (which he still expects). The NY empire manufacturing survey was stronger than expected (5.7 from -12.6, with also prices series jumping higher). EMU yields are taking a breather after yesterday’s rise/steepening on expectations of higher defense/fiscal expenditure. German yields are changing less than on bps across the curve. Despite ‘noisy/diffuse’ geopolitical and economic headlines of late, German ZEW investor confidence improved more than expected (expectations 26 from 10.3, 20.0 expected). ZEW comments that “Shortly before the day of the federal election, economic expectations have clearly improved in February. This rising optimism is probably due to hopes for a new German government capable of action. Also, after a period of absent demand, private consumption can be expected to gain momentum in the next six months’. European equities remain well bid, with the Eurostoxx50 touching a new record. The S&P 500 is also only a whisker away from record levels (+0.2%). Despite the risk-on, USD slightly outperforms with DXY returning to the 107 level. EUR/USD (1.045) is falling prey to profit taking as the 1.0533 YTD top serves as resistance for now.

The monthly UK eco update that will unfold this week, this morning started with a positive surprise. Labour data painted a better picture than signaled by survey evidence of late. The latter suggested a negative reaction of employers to higher social security contributions from the October budget. Still data were stronger than expected across the board, with the unemployment rate holding at 4.4% and January payrolls rising 21k vs a 30k decline expected. Maybe most important from a monetary policy point of view was (private sector) pay rising 6.3% (3M average Y/Y). This was no big surprise, not for markets and not for the BoE, but remains a reason for the BoE to hold a cautious approach on further policy easing. The immediate market reaction to the data was modest. UK Gilts underperform Bunds with yields rising between 3.5 bps (2-y) and 4.3 bps (30-y). Money markets currently only fully discount two additional 25 bps BoE cuts later this year, with less than 50% seen on a third step. In a public appearance today, BoE government Bailey are already looked forward to an expected uptick (to be published tomorrow) in the January inflation (expected to rise from 2.5% to 2.8%Y/Y). However, he tentatively downplayed this as mainly due to regulated prices rather than mirroring the underlying state of the economy. EUR/GBP tries to break the 0.83 big figure. For now sterling holds its recent gains, but no big follow-through gains yet.

News & Views

The governors of the Spanish, German, Italian and French central bank in a letter to the European Commission urged to simplify the wide array of rules for commercial lenders in “areas where the European framework is unduly complex and may create competitive distortions at international level, without any significant financial stability benefits.” While the letter comes as the US economy under president Trump is probably set for a broad-based wave of deregulation, the central banks said they are not calling for less strict rules as such, but only to streamline them and make them easier to comprehend and thus implement.

Canadian inflation in January printed at a consensus-matching 0.1% m/m and 1.9% y/y on a headline basis. The uptick from December’s 1.8% was largely due to energy (5.3% y/y) and was partially offset by a sales tax break for food and restaurant meals (-5.1% y/y). Core measures, however, quickened more than expected to an average of 2.7% compared to 2.55% in December. Combined with the strong shape of the labour market of late, it makes another rate cut by the Bank of Canada at the March 12 meeting increasingly unlikely. Market odds currently stand at 36% compared to 50% just yesterday. The BOC in January slowed down the pace of cuts from 50 bps to 25 bps, highlighted the cumulative amount of monetary easing done so far but didn’t offer specific guidance for what’s next. The BoC did warn for potential US tariffs to test the economy’s resilience. US president Trump has delayed a 25% levy from February to March 4. The Canadian dollar reacted muted with USD/CAD hovering around 1.42.

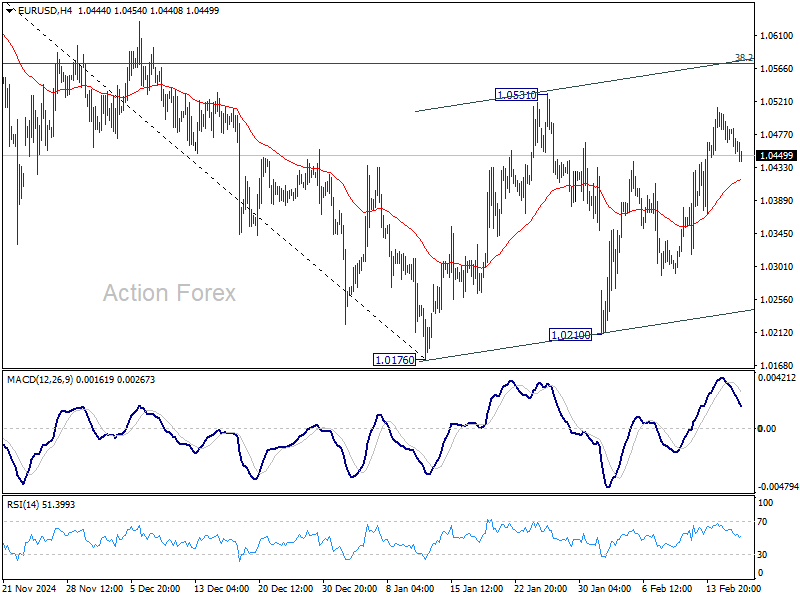

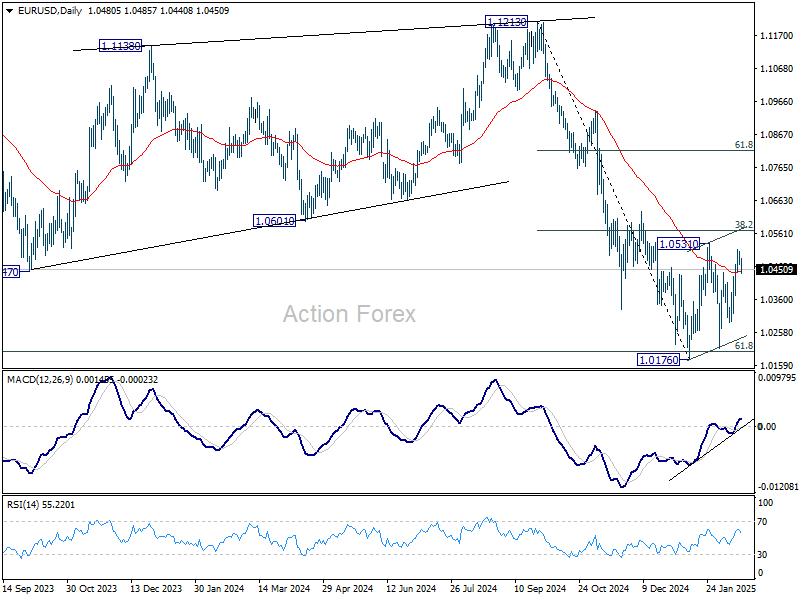

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0465; (P) 1.0486; (R1) 1.0505; More...

Intraday bias in EUR/USD remains neutral as consolidation from 1.0176 is still extending. Stronger rebound might be seen but outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

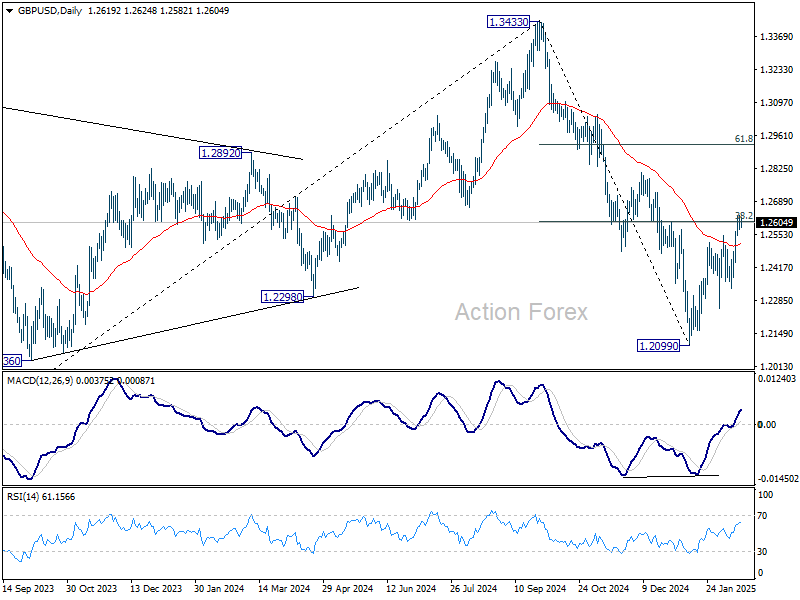

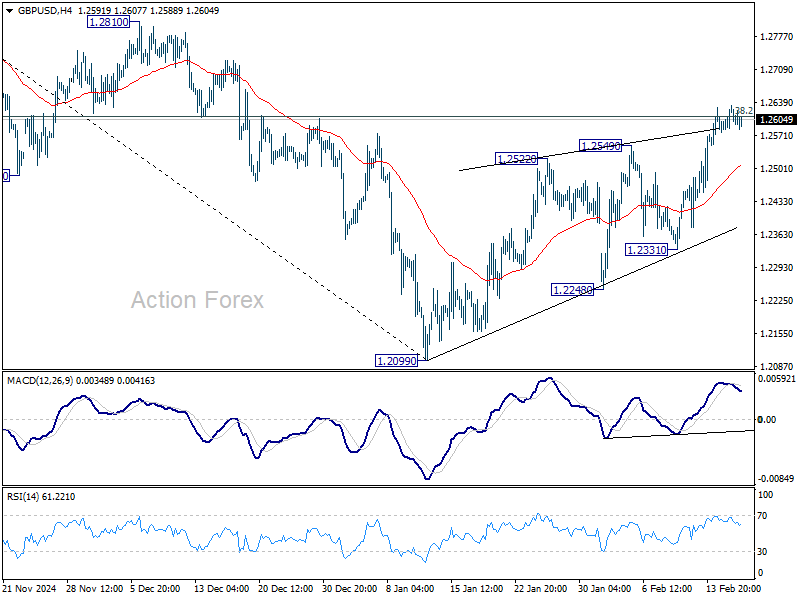

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2590; (P) 1.2613; (R1) 1.2648; More...

Intraday bias in GBP/USD stays neutral, and focus remains on 38.2% retracement of 1.3433 to 1.2099 at 1.2609. Rejection by this level will keep near term outlook bearish. Break of 1.2331 support will suggest that the rebound from 1.2099 has completed as a correction, and bring retest of 1.2099 low. However, firm break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.