Sample Category Title

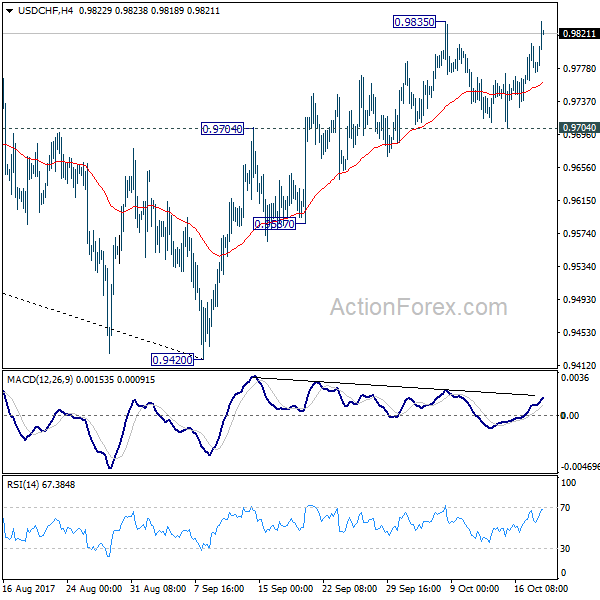

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9747; (P) 0.9778; (R1) 0.9814; More....

USD/CHF rises strongly today and focus is now back on 0.9835 resistance. Decisive break there will confirm resumption of rebound from 0.9420. In that case, USD/CHF should target 61.8% retracement of 1.0342 to 0.9420 at 0.9990 next. On the downside, break of 0.9704 support will argue that rebound from 0.9420 has completed. This will also mixed up the near term outlook and turn bias back to the downside for 0.9587 support.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

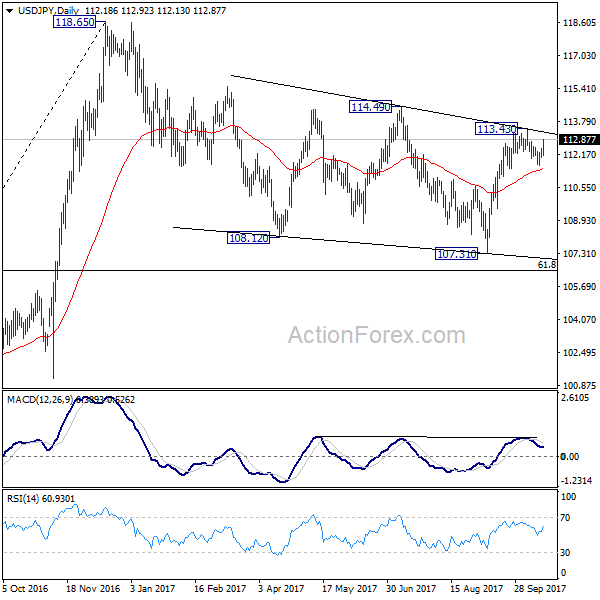

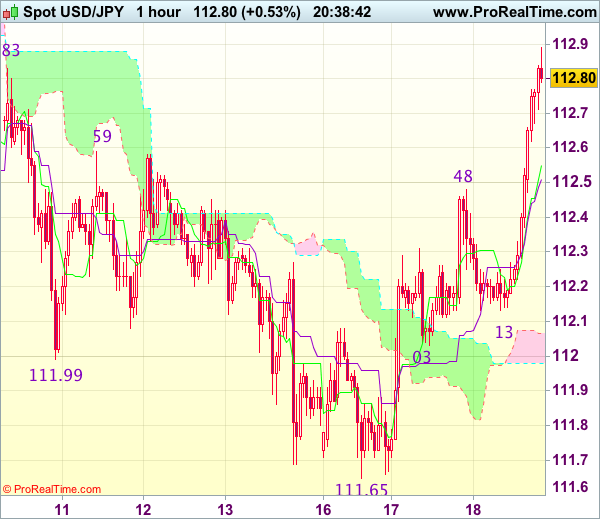

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.99; (P) 112.23; (R1) 112.43; More...

USD/JPY's strong rebound and break of 112.57 minor resistance suggests that pull back from 113.43 has completed at 111.64 already. And, rise from 107.31 is possibly resuming. More importantly, the development revives the case that correction from 118.65 has completed at 107.31. Intraday bias is now back on the upside for 113.43 first. Further break of 114.49 will confirm and pave the way to retest 118.65. However, break of 111.64 will mixed up the outlook again.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

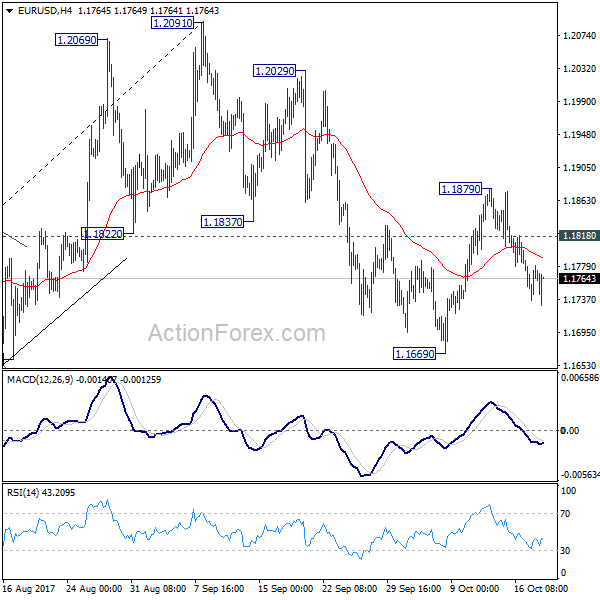

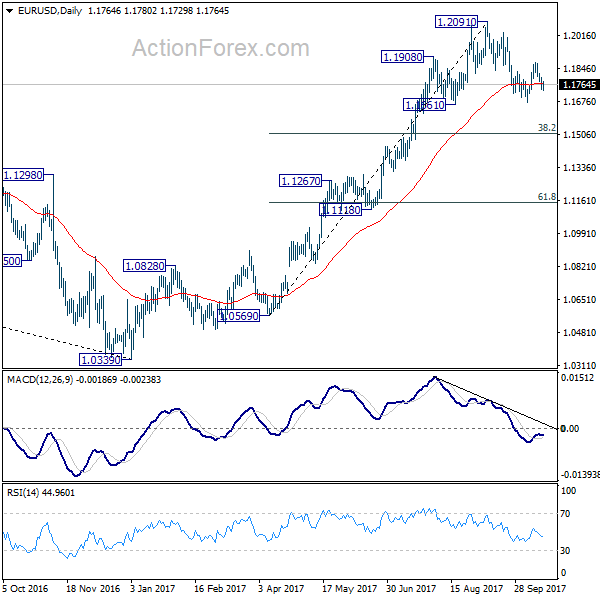

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1735; (P) 1.1767 (R1) 1.1798; More...

As long as 1.1818 minor resistance holds, deeper fall is expected in EUR/USD to 1.1669 support. Break there will confirm resumption of the whole corrective fall from 1.2091. In that case, EUR/USD will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510. Strong support is expected there to complete the correction. Nonetheless, above 1.1818 will turn bias back to the upside and extend the rebound from 1.1669 through 1.1879.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

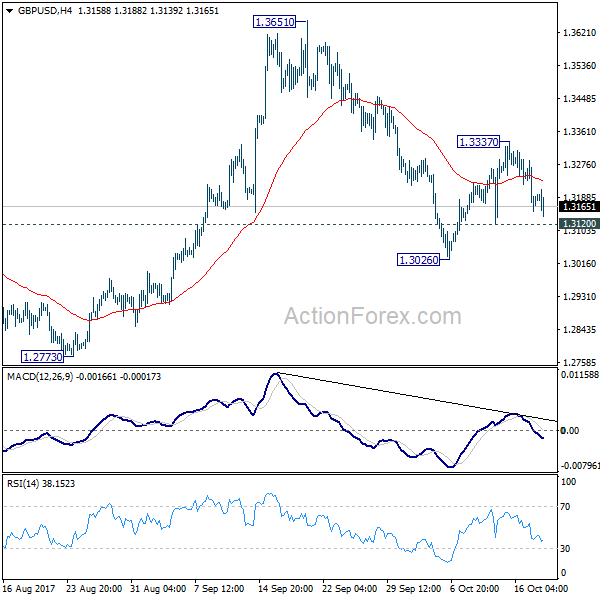

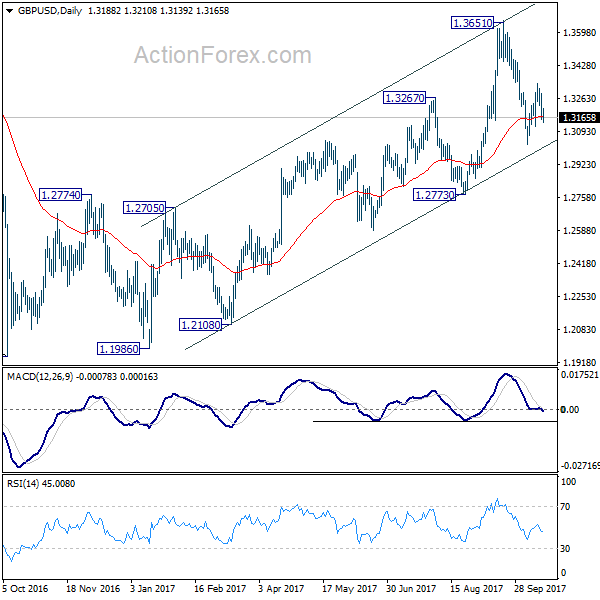

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3136; (P) 1.3211; (R1) 1.3269; More....

GBP/USD is holding above 1.3120 minor support and intraday bias remains neutral first. On the downside, break of 1.3120 will indicate that recovery from 1.3026 is completed at 1.3337. And fall from 1.3651 is resuming for 1.2773 support. That will revive that case that medium term rise from 1.1946 has completed at 1.3651. Meanwhile, above 1.3337 will bring retest of 1.3651 high instead.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll turn neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Strong Risk Appetite Sends Swiss Franc and Yen Lower, DAX Hit Record, DOW to Follow

Dollar trades generally higher today, except versus Canadian Dollar. But strength of the greenback is rather unconvincing against Euro, Aussie and even Sterling. The more decisive moves are found in USD/CHF and USD/JPY. That should be more likely due to strong risk appetite. German Dax hit new record high at 13094.76 earlier today and is maintaining most of the gains at the time of writing. US futures also point to higher open as DOW would extend recent record runs. Meanwhile, weaker than expected housing data from US also limits greenback's rally . Housing starts dropped to 1.13m in September, below expectation of 1.18m. Building permits also dropped to 1.22m, below expectation of 1.27m. From Canada, manufacturing shipments rose 1.6% mom in August.

Dollar strength on Taylor speculation far-fetched

The greenback is trading as the strongest one for the week and boosted by media report that US President Donald Trump was impressed by Stanford University Economic John Taylor at the Fed Chair candidate interview. Bets for Taylor to be the next Fed chair increased, making him one of the top three candidates alongside Jerome Powell and Kevin Warsh. Market reaction to the rise of Taylor was USD strength and an upward shift in the UST yield curve, hinging on hopes that this creator of the Taylor rule would accelerate the pace of rate hike if he has become the Fed' chief. We believe such expectation is a bit too far-fetched. More in Taylor Rule, Taylor Rules?

UK job data unlikely to derail BoE November hike

UK unemployment rate was unchanged at 4.3% in August, staying at 42 year low. Average weekly earnings rose 2.2% 3moy, above expectation of 2.1% 3moy. Claimant counts rose 1.7k in September, below expectation of 3.2k. Claimant count rate was unchanged at 2.3%. The set of data should have done little to change the chance of a November BoE rate hike. But wage growth was lagging behind CPI, which was at 3% in September, highest in more than five years. That will more likely than not to keep BoE's hands tied on more rate hikes in 2018.

ECB asset purchase program survived another legal challenge

ECB's asset purchase program survives another legal challenge today. Germany's Federal Constitutional Court rejected the request to stop Bundebanks from participation. The court said in a statement that "because of the high volume of purchases by the Bundesbank, disrupting bond purchases would endanger or even thwart the program's goal to raise inflation to about 2 percent." And, "granting the interim bid now would be more than just conserving the status quo, it would be identical with granting the lawsuit."

Chinese President Xi pledged to take center stage in the world

Chinese President Xi Jinping laid out his ambition to transform China by 2050, to become more "prosperous and beautiful." He hailed the economic progress under "socialism with Chinese characteristics". And said it presents as a "new choice for other countries". Xi also pledges to "take center stage in the world". On foreign policy, Xi emphasized that "no one should expect China to swallow anything that undermines its interests". On economy, he targets to move industries to "medium-high end" of the global value chain and foster a number of "world-class advanced manufacturing clusters". Regarding markets, Xi pledged to "improve the framework of regulation underpinned by monetary policy and macro-prudential policy, and see that interest rates and exchange rates become more market-based."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.99; (P) 112.23; (R1) 112.43; More...

USD/JPY's strong rebound and break of 112.57 minor resistance suggests that pull back from 113.43 has completed at 111.64 already. And, rise from 107.31 is possibly resuming. More importantly, the development revives the case that correction from 118.65 has completed at 107.31. Intraday bias is now back on the upside for 113.43 first. Further break of 114.49 will confirm and pave the way to retest 118.65. However, break of 111.64 will mixed up the outlook again.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Sep | 0.10% | -0.08% | ||

| 08:30 | GBP | Jobless Claims Change Sep | 1.7K | 3.2K | -2.8K | -0.2K |

| 08:30 | GBP | Claimant Count Rate Sep | 2.30% | 2.30% | ||

| 08:30 | GBP | ILO Unemployment Rate 3M Aug | 4.30% | 4.30% | 4.30% | |

| 08:30 | GBP | Average Weekly Earnings 3M/Y Aug | 2.20% | 2.10% | 2.10% | 2.20% |

| 12:30 | CAD | Manufacturing Shipments M/M Aug | 1.60% | -0.30% | -2.60% | |

| 12:30 | USD | Housing Starts Sep | 1.13M | 1.18M | 1.18M | |

| 12:30 | USD | Building Permits Sep | 1.22M | 1.25M | 1.27M | |

| 14:30 | USD | Crude Oil Inventories | -2.7M | |||

| 18:00 | USD | Federal Reserve Beige Book |

Trade Idea Update: USD/JPY – Buy at 112.50

USD/JPY - 112.81

Original strategy :

Buy at 112.30, Target: 113.30, Stop: 111.95

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.50, Target: 113.50, Stop: 112.15

Position : -

Target : -

Stop : -

As dollar has surged again after finding renewed buying interest at 112.13 and just broke above resistance at 112.83, adding credence to our view that low has been formed at 111.65 and consolidation with mild upside bias remains for the rise from 111.65 low to extend gain to 112.95-00, however, near term overbought condition should limit upside to 113.30 and resistance at 113.44 should hold on first testing.

In view of this, we are looking to buy dollar on pullback as previous resistance at 112.48 (now support) should contain downside and bring another rise later. Below 112.25-30 would risk test of support area at 112.03-13 but price should stay well above said low at 111.65, bring another rise later.

Taylor Rule, Taylor Rules?

Lacking other exciting news, the market was thrilled by the media report that US President Donald Trump was impressed by Stanford University Economic John Taylor at the Fed Chair candidate interview. Bets for Taylor to be the next Fed chair increased, making him one of the top three candidates alongside Jerome Powell and Kevin Warsh. Market reaction to the rise of Taylor was USD strength and an upward shift in the UST yield curve, hinging on hopes that this creator of the Taylor rule would accelerate the pace of rate hike if he has become the Fed' chief. We believe such expectation is a bit too far-fetched.

First, the Fed's monetary policy decision is made by a committee of 12 voting members. As such, it would be difficult for a more hawkish or dovish Chair to alter the final decision. Second, although the Taylor rule implies a much higher policy rate than then current one, the elements comprising the formula is not unchangeable. Indeed, Taylor last week suggested that "one can easily adjust the equilibrium interest rate in the rule". It is expected that his stance would be more aligned with the mainstream if he is appointed. Third, a hawkish Fed chair would be in conflict with Trump's economic policy which aims at boosting growth with deregulation and tax reform. Trump in his election campaign had reiterated a number of times his preference for a weak US dollar. Assuming the US economic developments continue as expected by the Fed, its monetary stance would be more or less unchanged, i.e. rate hike to remain gradual and data-dependent while balance sheet reduction would carry out as schedule, with whoever being the next chair.

Fed Chair Appointment

It is widely believed that Trump would announce his decision on the next Fed chair before he leaves for Asia on November 3. The market has identified five key candidates for the role, namely, Jerome Powell, Kevin Warsh, John Taylor, Gary Cohn and Janet Yellen. While the dovish-centre Powell remains the most likely candidate, bets for Warsh and Taylor have been rising of late. Both Warsh and Taylor are considered as in the hawkish camp. For the former, he criticized at the Hoover Institution Monetary Policy Conference in May about the Fed's balance sheet reduction strategy, noting that the "preferred sequencing of rate increases and balance sheet reductions differ markedly from what was agreed when we conceived QE in the 'war room' amid the crisis". Back in 2010, Warsh criticized the then-Fed chair Ben Bernanke's QE extension.

Talk is cheap. During his capacity as a FOMC governor from 2006 to 2011, Warsh voted largely in line with the majority in the majority. He had not dissented on any vote cut and QE decision during the period of GFC. He also voted for the second round of QE, despite his reservation.

Taylor Rule, Taylor Rules?

Taylor is believed to be the "most hawkish" candidate amongst the five. This also explains why the greenback and Treasury yields rose after reports suggesting that Trump has good impression on him.

Taylor's hawkish image is more driven by his eponymous monetary policy rule (Taylor Rule), which implies that the Fed funds rate should be much higher than the current rate. The Atlanta Fed website (https://www.frbatlanta.org/cqer/research/taylor-rule.aspx) has a simulated Taylor rule model for one to plug in different values to get various estimates of Fed fund rates. If the neutral rate is set at the traditional 2%, the Fed funds rate, using Taylor rule, would be 2.94%, compared 1.25% currently. However, if we set the neutral rate at -0.2%, one derived from the model developed by San Francisco Fed president John Williams and Thomas Laubach, the Fed funds rate would be around 0.74%. This illustrates that how one interprets the neutral rate, another elements in the Taylor rule, affect the outcome.

For John Taylor himself, his monetary stance may not be as hawkish as one has expected. In his speech titled Rules Versus Discretion: Assessing the Debate Over the Conduct of Monetary Policy at the Boston Fed conference last Friday, Taylor noted that "one can easily adjust the equilibrium interest rate in the rule". He added that the most important suggested change in policy rules in recent years is probably to "adjust the intercept to accommodate the lower estimate of the equilibrium real interest rate (R*)". He appears content with the situation that the FOMC members have recently adjusted the average estimate of the neutral by "at least one percentage point lower" than the original 2%.

Fed's Monetary Decision Marking

Unlike the RBNZ in which the government has unique power over the interest rate decision, the Fed's monetary decision is determined by the FOMC, a Committee consisting of 12 voting members: 7 members of the Board of Governors , the New York Fed president, and 4 of the remaining 11 Fed presidents, who serve one-year terms on a rotating basis. For the members in the Board of Governors, a full term is fourteen years with one term beginning every two years. A full term for the New York Fed president is five years. As such, the Committee turns over slowing. This avoids drastic changes in the monetary stance. There are also nonvoting fed presidents who attend the FOMC meetings, participate in the discussions, and contribute to the Committee's assessment of the economy and policy options. It would be quite impossible for the chair to override the monetary decision.

An important feature of Trumponomics is to stimulate US economy through deregulations and tax reform. He has also proposed improving the country's competitiveness on trade by a weak US dollar. It would be conflicting if the Fed chair he chooses turn out to be hawkish which would potentially send the currency higher.

We do not expect the next Fed chair to very much derail from the current monetary stance which seeks to increase the policy rate gradually and as the economic data justify. The balance sheet normalization process would also be largely in line with schedule.

Next EURUSD Down Leg Below 1.1730

The euro has continued to slip lower against the U.S dollar on Wednesday, with the EURUSD pair moving to a new weekly price-low of 1.1730. Continued fears over Catalonia and a strengthening U.S dollar are the main factors contributing to intraday euro weakness. The pair is currently trading around the 1.1748 level, as investors await the start of the U.S trading session.

A move below the 1.1730 support level is likely to trigger the next major move lower in the EURUSD pair. Below the 1.1730 level, sellers are likely to target the 1.1713 level, and the pairs 200-week moving average, at 1.1685.

If the EURUSD fails to push price below the 1.1730 level, buyers are likely move to test intraday buying demand above the 1.1750 level. Further resistance above 1.1750 is found at the 1.1780 and 1.1798 levels.

USDJPY Further Bullish Above 112.58

The U.S dollar has moved sharply higher against the Japanese Yen, hitting 112.76 during the European session, as the U.S dollar index gains strength across the board. The USDJPY pair is currently trading at the highs of the day, ahead of the release of key U.S housing data and the Federal Reserve's Beige Book.

The USDJPY pair is likely to continue to advance higher while trading above the key 112.58 technical level. Buyers are likely to target the 112.89 and 113.10 resistance levels. Further extended intraday technical resistance is found at 113.25 and 113.43.

Should the USDJPY pair start to decline below the 112.58 support level, intraday sellers are likely to push price-action back towards the 112.30 and 112.10 technical levels.

USD/CAD – Canadian Dollar Quiet Ahead Of Cdn. Manufacturing Sales

The Canadian dollar continues to have an uneventful week. In the Wednesday session, USD/CAD is trading at 1.2523, up 0.02% on the day. We could see some movement from the pair in the North American session, as Canada releases Manufacturing Sales. The markets are braced for a third straight decline, with an estimate of -0.1%. The US will release two key housing indicators. Building Permits is expected to slow to 1.25 million, and Housing Starts are forecast to remain unchanged at 1.18 million. On Thursday, the US releases unemployment claims and the Philly Fed Manufacturing Index.

With the Canadian economy performing well, could another rate hike be in the cards? The Bank of Canada surprised with a rate hike in September, but policymakers are concerned over tensions about NAFTA. Talks between Canada, the US and Mexico over re-negotiating NAFTA have floundered, raising the possibility that Donald Trump will scrap the agreement. The BoC would prefer not to raise rates until the NAFTA negotiations are settled. However, the Federal Reserve is widely expected to raise rates in December and the BoC will be under pressure to follow suit and protect the Canadian dollar.

With the Federal Reserve dropping strong hints that it will raise rates in December, the odds of a December hike are currently at a sizzling 91 percent. Just one month ago, the odds were 50-50 that the Fed would raise rates at the December meeting. Low inflation levels have been a key reason that the Fed has been reluctant to raise rates, but Fed Chair Janet Yellen and other policymakers have expressed optimism that inflation will move closer towards the Fed’s inflation target of 2 percent. The markets will be looking for some clues about the Fed’s rate plans, as FOMC members William Dudley and Robert Kaplan speak on Wednesday.