Sample Category Title

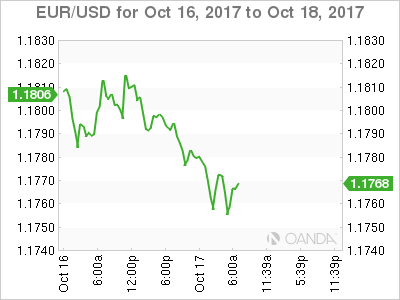

EURUSD Bearish Below 1.1780

The EURUSD has fallen below the 1.1780 support level, encouraging intraday selling in the pair. At present, the euro is trading around the 1.1760 level, as financial market concern grows over the worsening political situation in Catalonia, whilst the U.S dollar index continues to push higher.

The EURUD is expected to break below the 1.1750 support level as intraday selling interest accelerates. Once below the 1.1750 level, the euro is expected to test the 1.1739 and 1.1710 levels.

If the EURUSD can hold the 1.1750 support level, intraday buyers should then move the euro back towards the 1.1780 level, and the weekly pivot point, found at the 1.1807 level.

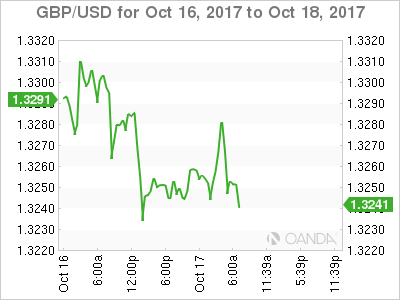

GBPUSD Bearish Below 1.3233

The British pound has fallen below its weekly pivot point against the U.S dollar, hitting 1.3200 after worse than expected UK PPI numbers. The GBPUSD pair currently trades at the lows of the day, as Bank of England Governor Mark Governor continues to speak in front of the UK Treasury Select Committee.

The GBPUSD pair is expected to remain bearish while trading below the key 1.3233 technical level. If price-action starts to decline further below the 1.3200 level, more selling can be seen towards 1.3190 and 1.3170.

If the pair can hold the 1.3200 support level, British pound buyers may start to push the pair back up towards the 1.3220 and 1.3333 and technical resistance level.

Canadian Dollar Edges Lower, Markets Eye Fed Policymakers

The Canadian dollar has posted slight losses in the Tuesday session. Currently, USD/CAD is trading at 1.2537, up 0.15% on the day. On the release front, there are no Canadian releases, and no major US indicators. On Wednesday, the focus will be on US housing data, with the release of Housing Starts and Building Permits.

The NAFTA pact is under attack from US President Trump, and that could spell trouble for the Canadian economy. Trump has declared that NAFTA has been terrible for the US and has vowed to renegotiate the deal. Negotiations between Canada, the US and Mexico over re-negotiating NAFTA have not gone well, and Trump has previously declared that he could scrap the deal and simply enter a new trade agreement with Canada. One of the key US demands that Canada is not happy with is a "sunset clause" which would require new negotiations every five years. The lack of progress in the talks has sent the Mexican peso lower, and if the unpredictable Trump decides to scrap the agreement, the Canadian dollar could lose up to 10 percent of its value, according to the Bank of Canada. The Bank surprised analysts with a rate hike in September, and the odds of another raise in rates is pegged at just 20 percent. BoC Governor Stephen Poloz has expressed concerns about the risks of the scrapping of NAFTA, and BoC policymakers would prefer not to raise rates until the NAFTA negotiations are settled. However, if the Federal Reserve raises rates in December, and the BoC does not follow suit, the Canadian dollar would likely lose ground.

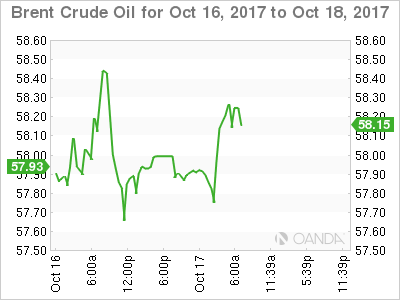

Oil prices continue to move higher, as fighting continues between Iraq and Kurdish forces. On Tuesday, the Iraqi army occupied the city of Kirkuk, which is located in an oil-rich region. Relations between Iraq and Kurdistan have deteriorated since the Kurds voted for independence in September, and the Iraqi offensive could disrupt oil shipments and raise oil prices, which would be bullish for the Canadian dollar.

EURGBP Remains Bearish As Recent Bounce Runs Out Of Steam

EURGBP has reversed back down again after finding resistance at a four-week high of 0.9032 last week. This top is just above the 50% retracement of the downleg from August’s 8-year high of 0.9306 to September’s 3-month low of 0.8745.

Momentum indicators are pointing to a neutral to negative bias in the short term with the RSI just below 50 and the stochastic oscillator deep in bearish territory. However, the stochastics have reached oversold area and the %K line is attempting a bullish cross with the %D line, suggesting an upside reversal is nearing.

Further losses should see the September low of 0.8745 acting as a major support as this is also where the 200-day moving average (MA) is currently converging. A drop below the 200-day MA would reinforce the bearish structure in the medium term and open the way towards the next key support level of 0.8580.

In the event of an upside reversal, the 38.2% Fibonacci retracement at 0.8960 could act as a barrier before being able to re-challenge the 50% Fibonacci retracement level around the 0.90 handle. A break above this level would shift the medium-term outlook to a more neutral one as it would take the pair above the 50-Day MA. Further gains would lead the way towards the 61.8% and 78.6% Fibonacci levels at 0.9090 and 0.9185 respectively.

However, for a resumption of the longer-term uptrend, which was halted in August, EURGBP would need to beat the 8-year high of 0.9306.

Taylor Law Supports Dollar

The 'mighty' U.S dollar has found some tentative support as investor speculation climbs on the back of the next Fed head being more 'hawkish.'

John Taylor, a candidate for Fed chair is known for a policy rule that would suggest higher interest rates, was said to have impressed President Trump in an interview last week. The President is to reportedly formally interview Fed Chair Yellen later this week.

Elsewhere, ongoing geopolitical risks (N. Korea, Spain's Catalan region and Brexit) has convinced many equity investors to consider taking a 'time-out.' Regional equity bourses are seeing mixed results as N. Korea warned that a nuclear war could 'break out any moment,' while in Europe, investors await the next move in the standoff over independence for Catalonia, while in the U.K Brexit talks could be headed for a breakdown.

Note: Bank of England (BoE) Governor Carney appears before the U.K Parliament's Treasury Committee for the first time since June's election this morning (06:15 am EDT).

A host of Fed speakers and the publication of the Beige Book this week may provide further clues about the U.S policy path – Philly Fed Harker today, and NY President Dudley and Dallas Fed Kaplan tomorrow.

1. Stocks pause atop lofty heights

In Japan, the Nikkei share average rallied for a 11th consecutive session as a stable yen (¥112.17) supported exporters, while expectations that Abe's ruling bloc will win the election this weekend continues to underpin sentiment. The Nikkei ended +0.4% higher, while the broader Topix was up +0.2%.

Note: A survey Monday showed that Japanese PM Abe's ruling coalition is on track for a big win in Sunday's general election.

Down-under, Australia's S&P/ASX 200 Index rose +0.7% and South Korea's Kospi index was up +0.2%.

In Hong Kong, stocks were little changed in quiet trading as investors wait for China's Communist Party congress to begin and Q3 Chinese economic data this week. The Hang Sang index was unchanged, while the China Enterprises Index lost -0.3%.

In China it was a similar situation, stocks ended little changed overnight as investors awaited economic data and a major leadership summit this week. The blue-chip CSI300 index was unchanged, while the Shanghai Composite Index lost -0.2%.

In Europe, regional bourses are trading slightly lower across the board as indices retreat from recent highs.

U.S indices closed Monday at another all time high, although volume continues to be light amid lack of volatility.

U.S stocks are set to open unchanged.

Indices: Stoxx600 -0.1% at 391.1, FTSE -0.2% at 7515, DAX -0.1% at 12996, CAC-40 -0.2% at 5354, IBEX-35 -0.4% at 10144, FTSE MIB -0.5% at 22317, SMI -0.2% at 9256, S&P 500 Futures flat.

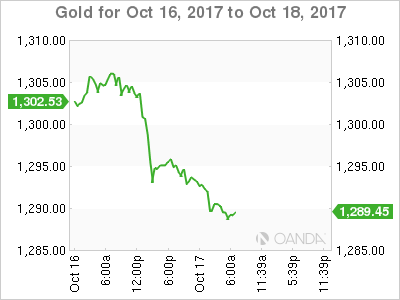

2. Oil rises as Iraq fighting shuts output in Kirkuk, gold lower

Crude prices rallied +1% Monday as Iraqi forces entered the oil-rich city of Kirkuk, seizing territory from Kurdish fighters and briefly cutting some crude output from OPEC's second-largest producer.

Note: Iraqi Kurdistan briefly shut down some +350k bpd of production from the major Bai Hassan and Avana oilfields due to security concerns.

Brent crude futures settled up +65c Monday, or +1.1% to +$57.82 per barrel while U.S crude ended up +42c, or +0.8% higher at +$51.87 per barrel.

Also supporting prices are renewed worries over U.S sanctions against Iran. President Trump on Friday refused to certify that Tehran was complying with the accord even though international inspectors say it is.

Note: During the previous round of international sanctions, roughly -1m bpd of Iranian oil was cut off.

Gold prices trade on the back foot, pressured by a firmer dollar, however, investor worries over geopolitical tensions in the Middle East and on the Korean peninsula is managing to keep these losses in check. Spot gold is down -0.4% at +$1,289.20 an ounce.

3. Sovereign yields back up

Reports that President Trump might pick John Taylor to lead the Fed after Janet Yellen's term ends next year has sent two-year Treasury yields to their highest in nine-years.

Taylor is an advocate of a rules-based approach to interest rate policy that would likely see official Fed rates much higher than at present – at least +3.5% according to some observers.

The back up in short-yields (U.S 2's +1.53%) has not been matched at the long-end. The yield on 10-year Treasuries gained +1bps to +2.31%.

In the U.K, inflation data this morning (see below) has bolstered the chances of the BoE's first interest rate hike in over a decade next month. U.K's 10-year yield has rallied +2 bps to +1.336%.

Elsewhere, in Germany, 10-year Bund yields have increased +1 bps to +0.38%, while Spain's 10-year yield decreased less than -1 bps to +1.578%.

4. Dollar finds tentative support

The EUR (€1.1783) has fallen to its lowest levels in a week overnight on reports that Fed chief candidate John Taylor made a good impression on Trump. Also providing pressure for the 'single unit' are reports that Spain is preparing to replace Catalan security officials. Outright, the EUR is down -0.3%, while against sterling, the unit is trading atop of its two-week lows (€0.8873).

The pound (£1.3247) continues to trade below the psychological £1.33 handle despite U.K Oct CPI coming in-line with expectations (see below) – the highest annual pace since Apr 2012, keeping t expectations that Governor Carney could raise BoE's interest rates in November.

5. UK inflation keeps BoE hike on track

Data this morning showed that British inflation rose to its highest level in more than five years last month and would suggest that the Bank of England (BoE) is on track to tighten rates next month.

The Office for National Statistics (ONS) said that consumer prices last month were +3.0% higher than a year ago.

Digging deeper, the rise is been driven largely by rising food prices and transport costs. Despite the U.K's economy slowing this year, the BoE has repeatedly signalled that interest rates are likely to rise.

Note: Rising inflation – driven largely by the pound's fall since the Brexit vote – is squeezing household incomes, causing broader economic growth to slow, as wages have failed to keep pace with the rising cost of living.

Market Update – European Session: UK Sept CPI Hits A 5 1/2 High

Notes/Observations

UK Sept CPI hits its highest annual pace since Apr 2012; keeps expectations that BOE could raise interest rates in November

Overnight

Asia:

RBA Oct Minutes: Any rate changes would be dependent on domestic economy; Appreciation in A$ expected to contribute to subdued pricing pressures

Japan Government Official: No discussion of FX at Economic Dialogue meetings between US and Japan officials. US express strong interest on bilateral trade deal with Japan and narrowing of US trade deficit. Japan told the US it should not focus just on trade deficit, Japan investment contributing to US job creation.

Moody’s: Japan’s credit strength remains robust (currently at A1 with a stable outlook)

Europe:

PM May and EU's Juncker joint statement following dinner meeting: Had broad and constructive exchanges in meeting on Brexit

Spain Economic Ministry 2018 budget plan for EU cut its 2018 GDP growth forecast from 2.6% to 2.3% citing political turmoil in Catalonia and a delay to approving next year’s budget

Americas:

President Trump to reportedly formally interview Fed Chair Yellen later this week about potentially staying on in her position

Economic Data

(EU) Sept EU27 New Car Registrations: -2.0% v +5.6% prior

(AT) Austria Sept CPI M/M: +1.0 v -0.1% prior; Y/Y: 2.4% v 2.1% prior

(IT) Italy Aug Total Trade Balance: €2.8B v €6.6B prior; Trade Balance EU: €0.2B v €2.0B prior

(UK) Sept CPI M/M: 0.3% v 0.3%e; Y/Y: 3.0% (highest since Apr 2012) v 3.0%e; CPI Core Y/Y: 2.7% v 2.7%e; CPIH Y/Y: 2.8% v 2.8%e

(UK) Sept RPI M/M: 0.1% v 0.3%e; Y/Y: 3.9% v 4.0%e, RPI-X (ex-mortgage interest payment) Y/Y: 4.1% v 4.2%e

(UK) Sept PPI Input M/M: 0.4% v 1.2%e; Y/Y: 8.4% v 8.2%e

(UK) Sept PPI Output M/M: 0.2% v 0.2%e; Y/Y:3.3% v 3.3%e

(UK) Sept PPI Output Core M/M: 0.0% v 0.1%e; Y/Y: 2.5% v 2.6%e

(UK) Aug House Price Index Y/Y: 5.0% v 5.4%e

(EU) Euro Zone Sept Final CPI Y/Y: 1.5% v 1.5%e; CPI Core Y/Y: 1.1% v 1.1%e

(DE) Germany Oct ZEW Current Situation Survey: 87.0 v 88.5e; Expectation Survey: 17.6 v 20.0e

(EU) Euro Zone Oct ZEW Expectations Survey: 26.7 v 31.7 prior

Fixed Income Issuance:

(IN) India sold INR110B vs. INR110B indicated in 3-month, 6-month and 12-month Bills

(ES) Spain Debt Agency (Tesoro) sold total €3.79B vs. €3.0-4.0B indicated range in 3-month and 9-month Bills

(ID) Indonesia sold total IDR22.5T in 3-month and 12-month Bills; 5-year, 10-year, 20-year and 30-year Bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 391.1, FTSE -0.2% at 7515, DAX -0.1% at 12996, CAC-40 -0.2% at 5354, IBEX-35 -0.4% at 10144, FTSE MIB -0.5% at 22317, SMI -0.2% at 9256, S&P 500 Futures flat]

Market Focal Points/Key Themes:

European Equities trade slightly lower across the board coming off earlier highs as Indices retreat from recent highs. US Indices closed at another all time high although volume continues to be light amid lack of volatility.

On the corporate front, French CAC components Danone, Casino and Remy Cointreau reported results which came ahead of consensus, while in the UK Internet fashion retailer ASOS trades higher after inline results and up beat 2018 outlook. Publisher Pearson trades higher after raising outlook whilst Merlin Entertainment trades sharply lower after guiding FY17 EBITDA below forecasts.

Looking ahead notable earners include Johnson and Johnson, Morgan Stanley and Goldman Sachs.

Equities

Consumer discretionary [Asos [ASC.UK] +1.6% (Earnings), Pearson [PSON.UK] +5.2% (Raises outlook), Merlin Ent [MERL.UK] -18% (Trading update, guidance light)]

Consumer Staples [Danone [BN.FR] +0.4% (Earnings), Casino [CO.FR] +1.1% (Earnings)]

Materials: [ Rio Tinto [RIO.UK] +0.5% (Q3 production)]

Industrials: [ Airbus [AIR.FR] +2.6% (C-Series partnership)]

Healthcare: [Sartorius Stedim [DIM.FR] -10% (Earnings, cuts outlook), Sartorius [SRT.DE] -6% (Earnings, cuts outlook)]

Real Estate: [Bellway [BWY.UK] +2.0% (Earnings)]

Speakers

ECB’s Constancio (Portugal): Needed to take macro-prudential tools much more seriously to avoid financial crisis. No general asset price over-valuation in Euro Area

ECB's Costa (Portugal): banks are now more capitalized than in 2007; financial sector not immune to risks

BOE Member Ramsden noted that saw signs that Brexit uncertainty could weigh on business sentiment. No signs of 2nd round effects of inflation on wages. Not in the MPC majority that sees a potential rate hike in coming months

Spain Budget Min Montoro: Catalonia crisis could have impact and could trigger an economic reverse so great that country would suffer a situation like the euro crisis at the end of 2011

Spain regional Catalan govt said to believe that dialogue cannot go forward following the recent jailings (**Note: On Oct 16th Spanish High Court: ordered detention of 2 Catalan separatist leaders under investigation for sedition)

Austria President Van Der Bellen: Have ask People’s Party (OVP) Kurz to form a gov't (as expected)

South Africa Central Bank (SARB)'s MMinele: CPI expectations were uncomfortably close to top of range; could not allow complacency to creep in

Turkey PM Yildirim reiterated govt stance that interest rates are too high given the economic conditions

India PM Advisor: RBI needed to cut rates by 75-100bps

Currencies

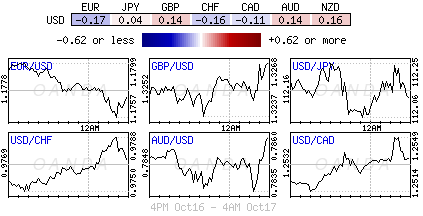

USD was firmer against most of the majors in the session with dealers citing a report that Fed chair candidate John Taylor (viewed as the most hawkish possibilities) made a favorable impression on Trump. EUR/USD was off by approx. 0.25% at 1.1765 just ahead of the NY morning. USD/JPY steady at 112.17

GBP/USD stayed below the 1.33 handle as UK Oct CPI came in-line with expectations. The 3.0% YoY reading was thehighest annual pace since Apr 2012 and kept expectations that BOE could raise interest rates in November

Fixed Income

Bund futures trade at 162.53 up 9 ticks as European stocks slide. Continued downside targets 161.53 while upside resistance stands initially at 162.75, followed by 163.51.

Gilt futures trade at 124.11 down 18 after UK September inflation matched estimates and hit a five-year high. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Tuesday’s liquidity report showed Monday’s excess liquidity fell to €1.812T from €1.820T and use of the marginal lending facility climbed to €160M from €118M.

Corporate issuance saw $2B come to market via 2 issuers, headlined by BPCE SA $1.25B 10-year senior non-preferred note. October issuance is at $49.8B

Looking Ahead:

(EU) EU Chief Negotiator Barnier to brief EU ministers

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (BE) ECB’s Praet (Beligium, chief economist) in Brussels

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (DE) Germany to sell €4.0B in 0% Sept 2019 Schatz

06:00 (IL) Israel Q2 Final GDP Y/Y: No est v 2.4% prelim

06:15 (UK) BOE Gov Carney in Parliament

06:30 (EU) ESM to sell €1.5B in 6-month bills; Avg Yield: % v -0.6245% prior; Bid-to-cover: x v 4.7x prior (Sept 19th 2017)

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia announces weekly OFZ bond auction

07:00 (BR) Brazil Aug IBGE Services Sector Volume Y/Y: -2.0%e v -3.2% prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (PL) Poland Sept Employment M/M: 0.1%e v 0.1% prior; Y/Y: 4.6%e v 4.6% prior

08:00 (PL) Poland Sept Average Gross wages M/M: -0.3%e v -0.2% prior; Y/Y: 6.2%e v 6.6% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Sept Import Price Index M/M: 0.6%e v 0.6% prior; Y/Y: 2.6%e v 2.1% prior

08:30 (US) Sept Export Price Index M/M: 0.6%e v 0.6% prior; Y/Y: No est v 2.3% prior

08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves

09:15 (US) Sept Industrial Production M/M: +0.2%e v -0.9% prior; Capacity Utilization: 76.2%e v 76.1% prior; Manufacturing Production: +0.1%e v -0.3% prior

09:30 (UK) BOE’s Brazier in Lisbon

10:00 (US) Oct NAHB Housing Market Index: 64e v 64 prior

10:00 (BR) Brazil to sell 2022, 2026 2035 and 2055 I/L Bonds

11:00 (CO) Colombia Aug Industrial Production Y/Y: No est v 6.2% prior

11:00 (CO) Colombia Aug Retail Sales Y/Y: No est v 3.1% prior

11:00 (CA) Canada to sell 0.75% Mar 2021 note

11:30 (US) Treasury to Sell 4-Week Bills

13:00 (US) Fed’s Harker (Voter, hawk)

15:30 (CA) Bank of Canada (BOC) Wilkins

16:00 (US) Aug Total Net TIC Flows: No est v -$7.3B prior; Net Long-Term Tic Flows: No est v $1.3B prior

16:30 (US) Weekly API Oil Inventories

(CO) Colombia Sept Consumer Confidence: -8.1e v -15.9 prior

Technical Outlook: USDCAD – Bulls Needs Sustained Break Above Daily Cloud To Resume

The USDCAD probes above daily cloud top 1.2537 (also Fibo 61.8% of 1.2597/1.2432 pullback) on Tuesday, in extension of Monday’s rally which showed strong rejection at cloud top.

The US dollar received support from President Trump’s comments about favoring more hawkish person to replace Fed Chief Yellen, while concerns about NAFTA talks success weigh on Loonie.

Setup of daily studies is bullish and supports further advance, but close above daily cloud is required to confirm and neutralize downside risk if near-term action stays capped by cloud top.

Bullish scenario sees final push towards key near-term barrier at 1.2597 (06 Oct high), break of which would signal continuation of larger uptrend from 1.2061 (08 Sep low).

Bulls could be delayed on repeated rejection at cloud top, while return and close below broken 10SMA (1.2502) would generate bearish signal.

Res: 1.2558, 1.2597, 1.2636, 1.2661

Sup: 1.2515, 1.2502, 1.2465, 1.2458

Technical Outlook: Copper Corrects Monday’s 4% Advance

Copper future contract for December delivery pulled back from fresh over three-year high at $3.2580 on Tuesday, as traders took profit after Monday's rally when copper advanced by 4% in the biggest one-day rally since Feb 10.

Fresh easing was also triggered by stronger dollar, with deeper dips signaled by daily RSI reversing from overbought territory and slow stochastic turning south, deeply in overbought zone.

Pullback is pressuring psychological $3.2000 support (also Fibo 38.2% of Monday's $3.1110/$3.2580 rally), which marks the first pivot ahead of previous high at $3.1770 (posted on Sep 5).

Correction could extend further if $3.1770 support gives way and could stretch to $3.11/12 zone (yesterday's low / Fibo 38.2% of $2.8930/$3.2580, 22 Sep / 16 Oct upleg).

Overall structure remains bullish and correction is expected to show the health of larger uptrend from Jan 2016 low at $1.9380.

Res: 3.2415, 3.2580, 3.2855, 3.2930

Sup: 3.2000, 3.1770, 3.1672, 3.1186

DAX Hugs 13,000 As Eurozone Inflation Remains Steady

The DAX is unchanged in the Tuesday session. Currently, the index is at 13,006.75, up 0.02% on the day. On the release front, German ZEW Economic Sentiment came in at 17.6 points, well short of the forecast of 20.1 points. Eurozone Final CPI remained unchanged at 1.5%, matching the forecast. On Wednesday, ECB President Mario Draghi will address an ECB conference in Frankfurt.

The German economy continues to impress, and the markets were looking for a surge in investor confidence in the ZEW Economic Sentiment report. That did not materialize, as the indicator improved slightly to 17.6 in October, but was well below expectations. The Eurozone ZEW Economic Sentiment softened to 26.7, well below the forecast of 34.2, and weaker than the previous reading of 31.7 points. Investors will likely focus on the German release, which marked a 4-month high, even though it missed expectations. On the inflation front, eurozone inflation remained stable at 1.5 percent. Inflation in the eurozone has moved significantly higher in 2017, but still remains shy of the ECB’s target of just below 2 percent. ECB President Mario Draghi has taken great pains to notify the markets that the ECB has no plans to raise interest rates in the near future, and the markets will be listening closely as he addresses an ECB conference on Wednesday.

The saga in Spain continues, as the Spanish and Catalan leaders play a dangerous game of cat-and-mouse. The central government has demanded that the Catalan leader, Carles Puigdemont, explicitly state whether he has declared independence. Madrid has extended a deadline for a reply until Thursday, and warned that if a clear answer was not forthcoming, it could trigger Article 155 of the Spanish constitution, which would allow the central government to disband the Catalan parliament and call elections or even set up a puppet government. Puigdemont has refused to be pinned down by Rajoy, and sent a two page letter to Spanish Prime Minister Mariano Rajoy, urging dialogue between the two leaders. However, Rajoy has insisted there will be no talks about independence, saying that the independence referendum, in which voters overwhelmingly voted in favor of independence, was illegal. The deepening crisis has led hundreds of companies to start leaving Catalonia, and the Standard and Poor’s rating agency has said that the region could face a recession if the situation is not resolved. Earlier this month, Spain’s economy minister said the uncertainty caused by the crisis had led to a freeze in investment projects in Catalonia. So far, the situation has not affected European stock markets, but that could change if the crisis takes a toll on the Spanish economy, the fourth largest in the eurozone.

Euro Edges Lower As German Economic Sentiment Falls Short

The euro has posted slight losses in the Tuesday session. Currently, EUR/USD is trading at 1.1762, down 0.28% on the day. On the release front, German ZEW Economic Sentiment came in at 17.6 points, well short of the forecast of 20.1 points. Eurozone Final CPI remained unchanged at 1.5%, matching the forecast. On Wednesday, ECB President Mario Draghi will address an ECB conference in Frankfurt, and the US releases Building Permits and Housing Starts.

With the German economy booming, the markets expected a surge in investor confidence in the ZEW Economic Sentiment report. That did not happen, as the indicator improved slightly to 17.6, but was well below expectations. The Eurozone ZEW Economic Sentiment softened to 26.7, well below the forecast of 34.2, and weaker than the previous reading of 31.7 points. Investors will likely focus on the German release, which marked a 4-month high, even though it missed expectations. On the inflation front, there were no surprises, as eurozone inflation remained stable at 1.5 percent. Inflation has moved significantly higher in 2017, but still remains shy of the ECB’s target of just below 2 percent. ECB President Mario Draghi has reiterated that the ECB will not raise interest rates in the near future, and the markets will be listening closely as he addresses an ECB conference on Wednesday.

The Spanish government has demanded that the Catalan leader, Carles Puigdemont, explicitly state whether he has declared independence. Madrid has extended a deadline for a reply until Thursday, and warned that if a clear answer was not forthcoming, it could trigger Article 155 of the Spanish constitution, which would allow the central government to disband the Catalan parliament and call elections or even set up a puppet government. Puigdemont continues to play a dangerous game of cat-and-mouse, and has refused to clarify if he proclaimed independence. Instead, Puigdemont sent a two page letter to Spanish Prime Minister Mariano Rajoy, urging dialogue between the two leaders. However, Rajoy has insisted there will be no talks about independence, saying that the independence referendum, in which voters overwhelmingly voted in favor of independence, was illegal. The deepening crisis has led hundreds of companies to start leaving Catalonia, and the Standard and Poor’s rating agency has said that the region could face a recession if the situation is not resolved. Earlier this month, Spain’s economy minister said the uncertainty caused by the crisis had led to a freeze in investment projects in Catalonia. So far, the situation has not affected the euro or European stock markets, but that could change if the crisis takes a toll on the Spanish economy, the fourth largest in the eurozone.