Sample Category Title

The US Dollar is Vulnerable, But It’s Temporarily

The US Dollar can't manage to continue growing, and the more attempts to rise it makes, the more doubts appear that it can really rise during this particular period of market fluctuations. The EUR/USD has clearly set a course for 1.20 and may resume falling only after reaching this level.

The statistics is against the USD so far. The numbers published last week, which were followed with insight, turned out to be weaker than expected and investors lost their interest (that was already very low) to the American currency. For example, the Retail Sales expanded by 1.6% m/m in September, which is quite good in comparison with the August reading of –0.1% m/m, but it's still less than the expected number of +1.7% m/m. The same can be told about the inflation in September. The CPI increased by 0.5% m/m after adding 0.4% in August. And that'd be okay, but investors expected +0.6% m/m. On top of that, the Core Inflation added only 0.1% m/m although it was expected to increase by 0.2% m/m.

Taken together, these two catalysts were able to make investors' attitude to the USD even more negative. The US Federal Reserve with the plan to sell assets on its balance sheet and the U.S. Department of the Treasury that was ready to increase the national debt were put on the back burner. Like it was already said, and it's still true, both of these plans will lead to the US Dollar strengthening. It's just a question of time.

There will be a lot of interesting statistical reports from the USA this week. In addition to that, Janet Yellen, the Chairwoman of the Federal Reserve, will speak on Friday. Speculations about candidates for her position died down for a while, but may revive at any moment.

Any information about possible activities of the US monetary authorities will support the Dollar regardless the market situation at that moment. One just have to wait, that's all.

The technical chart of the EUR/USD pair shows that the uptrend has transformed into the downtrend. We should also note that after breaking the main trend line, the price has fallen by the distance, which equals the width of the previous channel. If the instrument breaks the current support level, it may fall and reach 1.1550.

This chart shows the current descending movement in more details. The downtrend is clearly defined by the resistance and support levels. The sellers may worry that right now the price is moving close to the resistance level, because the pair may break it to the upside and grow to reach 1.2000, which is a psychologically-crucial level. However, if the "bears" push strong enough, the instrument may reverse and reach the support level at 1.1550.

GBPUSD Continues Falling Following Carney’s Speech

The price of EUR/USD continued to fall due to disappointing statistics from the ZEW Economic sentiment index. The index for Germany came in at 17.6 for October against the 20.1 forecast, while for the Eurozone it hit 26.7 versus the 34.2 forecasted. Growth in industrial production in the US of 0.3% in September against the 0.7% decline in the previous period gave a further downward push to the pair. Investors are waiting for tomorrow's speech by ECB President Mario Draghi where he may give some insights on the plans and timing of cuts to the asset purchasing program.

The British pound got a boost today from consumer inflation which grew to 3.0% in September compared to 2.9% in August. This increases the chance of an interest rate hike by the Bank of England happening sooner rather than later which is good news for the pound. Though an interest rate increase by 0.25% will only compensate the monetary easing from the previous year. However, the Bank of England's Governor, Mark Carney, didn't mention tightening monetary policy during his speech in parliament today. Volatility may remain high tomorrow due to the labour market data release in the UK.

The aussie dollar may see some action later today from the release of the MI leading index due out at 23:30 GMT. Earlier today the minutes of the Reserve Bank of Australia meeting were released with an optimistic forecast on the state of the Australian economy. AUD bulls' positive reaction however was short lived.

EUR/USD

The EUR/USD kept falling within the limits of the local descending channel and as a result is testing the support line at 1.1750. Breaking through 1.1750 may become a stimulus for continued price drops with the closest targets at 1.1700 and 1.1620. The growth potential is limited by the upper limit of the local descending channel.

GBP/USD

After some consolidation near 1.3250 the pound has shown a sharp descending move and is approaching the support level at 1.3150. Breaking through this mark is likely to stimulate the bears to pull the quotes down to the 1.3000-1.3050 range. On the other side, the RSI on the 15-minute chart is near the oversold zone which is the basis for a possible price rebound to 1.3250. Volatility is likely to remain high.

AUD/USD

The AUD/USD price resumed falling after some upward correction. The immediate goals in case of maintaining the current descending dynamics will be 0.7800 and 0.7740. If the quotes fix above the resistance at 0.7870 it may become a strong signal to buy with potentials to increase up to 0.8000 and above. Though today we're more likely to see a bearish sentiment.

Pound Dips Despite Inflation Climbing 3%

The British pound has lost ground in Tuesday trade. In the North American session, GBP/USD is trading at 1.3174, down 0.58% on the day. On the release front, British CPI edged up to 3.0 percent, matching the estimate. BoE Governor Mark Carney testified before the Treasury Select Committee in London. There are no major US indicators on the schedule. On Wednesday, the UK releases wage growth and unemployment data, and the US will publish Housing Starts and Building Permits.

British inflation continues to accelerate, as CPI, the primary gauge of consumer spending, showed that inflation in September was 3.0% higher than a year ago. This marked the fastest rise in inflation since April 2012. The continuing rise in inflation is primarily due to the weak British pound, which has dropped 12 percent since the Brexit vote in June 2016. The CPI release likely means that the Bank of England remains on track to raise interest rates at its November policy meeting. Inflation was on the mind of lawmakers on Tuesday, who pressed Carney when he testified before a parliamentary committee. Carney said that he expected inflation would peak in October or November, and that the bank had refrained from acting earlier to raise rates in order to lower inflation, saying that high inflation was a "trade-off" in order to hamper the economy.

The Brexit talks are at a deadlock, as the sides have made little progress after several rounds of negotiations. Prime Minister Theresa May is keen to talk trade with the Europeans, but the latter have conditioned trade talks on progress being reached on a number of issues, such as Britain's payment when it leaves the European Union, the status of the border with Northern Ireland and the jurisdiction of the European High Court on European citizens living in the UK. The two sides remain far apart on all of these issues, and each party has criticized the rigid positions of the other. The EU holds a summit on Thursday, and could announce that they won't talk trade with Britain until 2018. The lack of progress means that the possibility of a 'hard Brexit', in which Britain would leave with no deal being reached, is growing. BoE Governor Mark Carney acknowledged on Tuesday that the Bank has made contingency plans in case there is no agreement. However, British businesses are lobbying hard for an agreement, and want a 2-year interim period, such as a temporary customs union with the EU, in order to soften the blow of leaving the EU.

Trade Idea Wrap-up: USD/CHF – Buy at 0.9770

USD/CHF - 0.9800

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 0.9786

Kijun-Sen level : 0.9770

Ichimoku cloud top : 0.9747

Ichimoku cloud bottom : 0.9739

New strategy :

Buy at 0.9770, Target: 0.9870, Stop: 0.9735

Position : -

Target : -

Stop : -

As the greenback has surged again after brief pullback, adding credence to our view that low has possibly been formed at 0.9705 last week and consolidation with mild upside bias remains for gain to 0.9808 resistance but a firm break above there is needed to signal the fall from 0.9837 has ended instead, bring retest of this level, break there would confirm recent rise from 0.9421 low has resumed and extend headway to 0.9870 and possibly 0.9900.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as 0.9760-70 should limit downside. Only a break below support at 0.9730 would abort and signal the rebound from 0.9705 has ended, bring retest of this level. Once this support is penetrated, this would revive bearishness and extend the fall from 0.9837 to 0.9669-70 (61.8% Fibonacci retracement of 0.9565-0.9837 and previous support) but previous support at 0.9642 should remain intact.

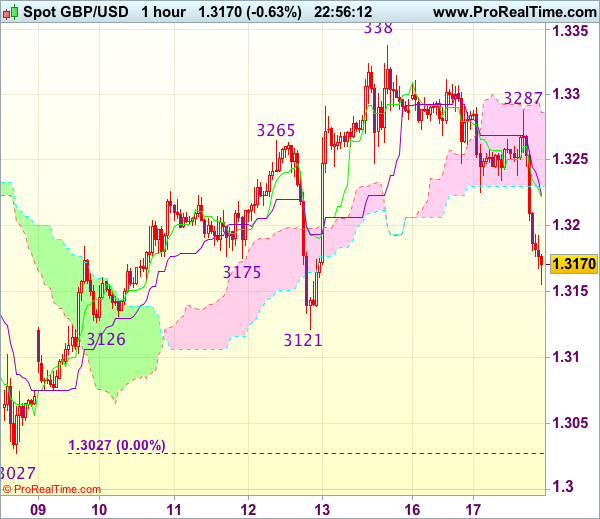

Trade Idea Wrap-up: GBP/USD – Sell at 1.3225

GBP/USD - 1.3173

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3221

Kijun-Sen level : 1.3223

Ichimoku cloud top : 1.3286

Ichimoku cloud bottom : 1.3230

Original strategy :

Sell at 1.3225, Target: 1.3125, Stop: 1.3260

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3225, Target: 1.3125, Stop: 1.3260

Position : -

Target : -

Stop : -

The British pound met renewed selling interest at 1.3287 and has dropped again today, signaling top has been formed at 1.3338 late last week and consolidation with downside bias is seen for this move to extend further weakness to 1.3150, then towards support at 1.3121, however, break of latter level is needed to retain bearishness and bring further subsequent decline to 1.3090-00.

In view of this, wee are looking to sell cable on recovery as the lower Kumo (now at 1.3230) should limit upside and bring another decline later. Above 1.3250-60 would risk another test of said intra-day resistance at 1.3287 but only break there would signal an intra-day low is formed instead, bring rebound to 1.3300 and possibly test of resistance at 1.3312.

Trade Idea Wrap-up: EUR/USD – Sell at 1.1800

EUR/USD - 1.1752

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1756

Kijun-Sen level : 1.1778

Ichimoku cloud top : 1.1828

Ichimoku cloud bottom : 1.1813

Original strategy :

Sell at 1.1800, Target: 1.1700, Stop: 1.1835

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1800, Target: 1.1700, Stop: 1.1835

Position : -

Target : -

Stop : -

As the single currency has fallen again after brief bounce to 1.1820 yesterday, suggesting top has possibly been formed at 1.1880 and the fall from there may extend weakness towards support at 1.1719, however, break there is needed to retain bearishness and signal the rebound from 1.1669 has ended, then further decline to 1.1700 would follow.

In view of this, we are looking to sell euro on recovery as 1.1800 should limit upside. Above 1.1820 would suggest low is formed instead, bring a stronger rebound to 1.1845-50 but price should falter below said resistance at 1.1880, bring another retreat later.

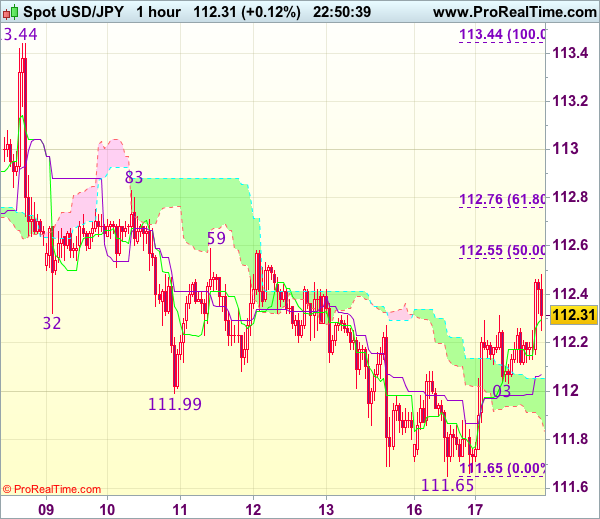

Trade Idea Wrap-up: USD/JPY – Buy at 112.05

USD/JPY - 112.30

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 112.30

Kijun-Sen level : 112.07

Ichimoku cloud top : 112.05

Ichimoku cloud bottom : 111.88

Original strategy :

Buy at 112.10, Target: 113.10, Stop: 111.75

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.05, Target: 113.05, Stop: 111.70

Position : -

Target : -

Stop : -

As dollar has surged again today after finding renewed buying interest at 112.03, adding credence to our view that low has been formed at 111.65 and consolidation with mild upside bias is seen for gain to 112.55-59 (50% Fibonacci retracement of 113.44-111.65 and previous resistance), however, break there is needed to signal the fall from 113.44 has ended, bring further gain to 113.00-10 but said resistance at 113.44 should hold from here due to near term overbought condition.

In view of this, we are looking to buy dollar on pullback as said support at 112.03 should limit downside and bring another rebound later. Below said support at 111.65 (yesterday’s low) would revive bearishness for the fall from 113.44 top to extend weakness to 111.47 support and later towards another previous support at 111.11 which is expected to remain intact.

UK Inflation Gives Way for Rate Hike; Pound Posts Short-Lived Gains on Dovish BOE Remarks

UK inflation in September rose to a 5 ½ -year high according to the Office for National Statistics, gaining one percentage point above the BOE's 2% target and igniting speculation that a rate hike could emerge in the BOE's November meeting. However, the pound could not sustain the uptick triggered by the data, giving away its gains, after the BOE chief and deputy governor held a dovish stance during parliamentary testimony.

Headline consumer prices matched expectations, increasing by 3.0% y/y in September but remaining close to August's mark of 2.9%. The growth in prices was mainly attributed to rising dairy and food prices as well as to the relatively weak currency. Excluding food and energy items, the CPI stood flat near a six-year high at 2.7%. On a monthly basis, the headline inflation fell from 0.6% to 0.3% as expected, while the core equivalent missed the forecast of 0.3%, declining from 0.6% to 0.2%.

Regarding producer prices, input costs came in higher than expected climbing steadily by 8.4% y/y (August's mark was revised upwards from 7.6% to 8.4%), while analysts had projected a growth of 8.2%. The cost of outputs sold by manufacturers came in line with expectations, edging down by 0.1 percentage points to 3.3% y/y.

With inflation strengthening above the BOE target and the BOE chief, Mark Carney, hinting last week that a rate hike would be appropriate "in the coming months", traders were pricing that a rate rise would likely be delivered in November when policymakers will gather to decide on monetary policy. However, the weakness in wage growth and economic activity could persuade rate-setters to maintain their accommodative policy as the fourth round of Brexit negotiations failed to agree on a transition period and the divorce bill, raising fears of a "no deal" Brexit.

Following the data release, Carney held a less hawkish speech in front of the Treasury committee at the Parliament, saying that the BOE'S target is to keep inflation at 2% and that "building a war chest in interest rate terms" to mitigate future shocks is "not appropriate or necessary given that policy can move quite nimbly if required". He also stated that the MPC committee expects inflation to peak above 3.0% in November or October, while asked about Brexit he replied that British Banks have worked more on a hard Brexit scenario under no transition period than EU banks have done.

Earlier, the BOE deputy governor, Dave Ramsden, admitted that he did not vote for a rate hike in September's policy meeting as earnings remain subdued despite growth in employment, while he also added that he would like more time before taking a decision on interest rates in November. The new MPC member, Silvana Tenreyo, claimed that she was not ready to support higher rates unless "inflation pressure builds in Britain's labour Market".

In the wake of the data, the pound immediately hit an intra-day high of $1.3286 but it soon tumbled to $1.3169 after BOE comments, being 0.60% down on the day. Euro/pound was 0.11% up at $0.8911.

Pound Tumbles on Dovish BoE Comments; Fed Chair Talk Drives Dollar Higher

Sterling took a tumble on Tuesday after Bank of England officials appeared more cautious than anticipated in supporting policy tightening even as UK inflation rose to a 5½-year high in September. The US dollar enjoyed a second day of solid gains as investors speculated that President Trump was considering appointing an inflation hawk as the next head of the US Federal Reserve. The euro meanwhile remained subdued as renewed political risks continued to weigh on the currency.

It was a busy session for European data, with UK inflation being the highlight. British consumer prices rose by an annual rate of 3.0% in September – up from the prior 2.9% and the highest since April 2012. The figure was in line with expectations and at the upper limit of the Bank of England's 1% band around its central target of 2%. Core inflation was unchanged at 2.7%, as expected, though the month-on-month rate rose by a smaller-than-forecast 0.2%.

The pound firmed to $1.3287 in the run up to the data but quickly lost momentum as BoE policymakers began appearing before the Treasury Select Committee in Parliament today. The Bank's newest Deputy Governor, Dave Ramsden, cast doubt about the need for higher interest rates, saying he wasn't part of the majority of MPC members at the August meeting who saw a case for a rate hike in the coming months. Another new MPC member, Silvana Tenreyro, said a premature rate increase could be "costly" but would vote for a rate hike if incoming data warrants it.

BoE Governor, Mark Carney, also surprised traders by giving only a cautious support for tighter policy. Carney said he would vote for a rate rise if the output gap continues to close in the coming months. But the lack of a stronger signal for a November move disappointed investors who have priced in a 0.25% hike at the next meeting.

Sterling plunged below the $1.32 level after the remarks, hitting a session low of $1.3165. The British currency briefly stabilized after the Brexit minister, David Davis, told Parliament the UK is not planning to walk away from the Brexit negotiations and urged EU leaders to approve accelerating the talks at the bloc's summit later this week.

Other data out of Europe today included the German ZEW business survey and the final reading of Eurozone CPI. Germany's ZEW economic sentiment index missed forecasts of 20.0 but still managed to improve from September's 17.0 to 17.6 in October. The current conditions gauge also missed estimates, falling to 87.0 in October from the prior 87.9. Analysts were expecting a figure of 89.0.

The euro slipped further after the data, touching a fresh one-week low of $1.1734 in afternoon European trade. There was little reaction to Eurozone September inflation numbers, which were left unrevised at 1.5% and 1.3% year-on-year for the headline and core rates respectively.

The greenback had a better session, with both dollar/yen and the dollar index posting gains. The dollar index stood 0.3% higher at 93.60 at the US open, while against the yen, the dollar traded around 112.30.

A report by Bloomberg that President Trump was impressed by Stanford University economist John Taylor at an interview last week led market participants to place him as the top contender for the next Fed chair. However, more important could be the outcome of Trump's meeting with current chair, Janet Yellen, on Thursday. If Taylor, who advocates higher rates, remains the favourite to take over the helm of the Fed in the coming days, the dollar could see further gains.

US bond yields have already been boosted by the prospect of a more hawkish Fed chair, with the 2-year yield on Treasury Notes jumping to a nine-year high of 1.554% today.

Further boosting the dollar today were positive data out of the US. Import prices rose by a bigger-than-expected 0.7% month-on-month in September, beating forecasts of 0.5%. Industrial production also came in above estimates, with output expanding by 0.3% m/m in September, versus forecasts of 0.2%. It compares with an upwardly revised -0.7% in August.

In other currencies, the Australian dollar remained in the red, extending its losses in European trading to hit a new intra-day low of $0.7822. Its kiwi counterpart also came under pressure from the stronger greenback despite stronger-than-expected inflation data out of New Zealand today. The kiwi fell to around $0.7150 in late session, having earlier touched $0.72. A 1% drop in dairy prices at the latest bi-weekly global dairy auction did not help the New Zealand currency either.

Major commodities also fell back, with oil prices unable to top yesterday's 2½-week highs, while copper gave way to profit taking after recent sharp gains. WTI oil was last trading at $51.94 a barrel and Brent crude at $58.10 a barrel, as ongoing fighting between Iraqi and Kurdish forces in Iraq's oil-rich Kurdistan region supported prices. Copper slid 1% to $3.19 per tonne, taking a respite after a 4% surge over the past week.

Gold declined for a second day, to around $1285 an ounce in late session, coming under pressure from the stronger dollar.

Tempest-Tossed: Industrial Production Notches Small Gain

The modest 0.3 percent gain in industrial production could have been larger had it not been for the quarter percentage point drag from Hurricanes Harvey and Irma.

Look In... to the Eye of the Storm

Do not "rush" to judgment on the modest gain in industrial production for September. Overall output increased 0.3 percent as the Fed estimated a quarter percentage point drag from the effects of hurricanes. Industrial production fell at a 1.5 percent annualized rate in the third quarter, but according to Fed estimates, this figure would have been an increase of at least 0.5 percent had it not been for the effects of the storms.

We had forecast a pullback in today's report for September industrial production. Our admittedly pessimistic view was informed by the experience around Hurricane Katrina in 2005. At that time, the Fed estimated Katrina shaved off 0.3 percentage points in August, then another 1.7 percentage points in September for a total of two percentage points over the two months. Fast forward to this cycle and the Fed already estimated a 0.75 percentage point drag from Harvey in August. There is also the matter of Hurricane Irma which followed Harvey roughly two weeks later. (We say "roughly" because both storms made landfall on multiple dates as they hovered along the coasts.) Similarly back in 2005, Katrina was followed to shore by Rita, but there were almost four weeks between the storms back then. The drags from the 2017 storms turned out to be only about half as much of a negative impact as we experienced 12 years ago.

Look Out... for the Force Without Form

In 2015, industrial production fell in 11 out of 12 months as a retrenchment in the energy sector weighed on mining output along with other factors like a (then) stronger dollar and weak global growth backdrop. In 2016, output fell only six out of 12 months as that rebalancing in the energy sector was still a factor, but the global backdrop was showing improvement as industrial production was regaining its footing. This year, there had been only one monthly slip (in January) before Harvey knocked industrial production into negative territory.

Looking into the remaining months of the year and considering the outlook for 2018, we look for industrial production to ramp-up modestly. The factors that weighed on growth in recent years have either reversed altogether or at least faded. The dollar's march higher has reversed this year, global growth has been firming and energy prices have broadly stabilized, which has lifted mining output again. On that basis our outlook is for 2.0 to 2.5 percent growth for industrial production in 2018.

Capacity utilization moved slightly higher and at 76.0 percent, it remains well-below its pre-recession peak. Among other factors, this excess slack could be an impediment to the Fed's elusive 2.0 percent price inflation target. We will delve deeper into the drivers of capacity utilization in a forthcoming special report later today.