Sample Category Title

Further GBPUSD Losses Expected Below 1.3200

The British pound continues to weaken against the U.S dollar, as Brexit negotiations remain deadlocked between the UK and the European Union. The pair is currently trading around the 1.3180 support level, after yesterday slipping to 1.3154. Traders now await the release of key unemployment and wage data from the United Kingdom economy.

Further GBPUSD selling pressure is expected while the pair trades below the key 1.3200 level. Intraday losses can be seen towards the 1.3154 and 1.3130 support level, with extended intraday support located at 1.3121 and 1.3080.

A sustained move above the 1.3200 level can lead to further intraday gains towards 1.3224 and 1.3233. Extended intraday resistance is located at the 1.3255 and 1.3280 levels.

British Pound Downtrend Intact Vs US Dollar

Key Highlights

- The British Pound recovered well from 1.3030, but faced strong offers near 1.3300 against the US Dollar.

- A key bearish trend line with current resistance at 1.3260 on the 4-hours chart of GBP/USD is acting as a barrier.

- The US Industrial Production in Sep 2017 posted a 0.3% rise, more than the +0.2% forecast.

- Today in the UK, the Claimant Count Change for Sep 2017 will be released, which is forecasted to register 1.0K.

GBPUSD Technical Analysis

The British Pound corrected sharply from the 1.3030 level against the US Dollar. However, the GBP/USD pair is struggling to settle above 1.3300 and remains at a risk of more declines.

The pair recently failed to break the 100 simple moving average near 1.3330 (4-hour, red) and started a downside move. It also failed near a key bearish trend line with current resistance at 1.3260 on the 4-hours chart.

Sellers succeeded in pushing the pair below the 50% Fib retracement level of the last wave from the 1.3027 low to 1.3337 high.

Therefore, there are chances of further losses in GBP/USD as long as the pair is below the 1.3300 resistance.

US Industrial Production

Recently in the US, the Industrial Production for Sep 2017 was released by the Board of Governors of the Federal Reserve. The forecast was slated for a 0.2% rise compared with the previous month.

The actual result was better the forecast, as there was an increase of 0.3% in the production in Sep 2017. It was way above the last revised decline of 0.7%.

The report stated:

For the third quarter as a whole, industrial production fell 1.5 percent at an annual rate; excluding the effects of the hurricanes, the index would have risen at least 1/2 percent. Manufacturing output edged up 0.1 percent in September but fell 2.2 percent at an annual rate in the third quarter.

The GBP/USD was pressured after the release and is currently at risk of more losses below 1.3240.

Economic Releases to Watch Today

- UK Claimant Count Change Sep 2017 – Forecast 1K, versus -2.8K previous.

- UK ILO Unemployment Rate August 2017 (3M) – Forecast 4.3%, versus 4.3% previous.

- UK Average Earnings Including Bonus August 2017 (3Mo/Year) – Forecast +2.1%, versus +2.1% previous.

- UK Average Earnings Excluding Bonus August 2017 (3Mo/Year) – Forecast +2.0%, versus +2.1% previous.

- US Housing Starts Sep 2017 (MoM) – Forecast 1.175M, versus 1.180M previous.

- US Building Permits Sep 2017 (MoM) – Forecast 1.25M, versus 1.30M previous.

Forex: UK Inflation At 5-Year High

The likelihood of a rise in UK interest rates, for the first time in a decade, gained momentum on Tuesday as UK CPI edged up from 2.9% to 3.0% – its highest level since April 2012. Bank of England Governor Mark Carney did nothing to dispel a rate hike as he gave evidence to the UK Treasury select committee where he stated that the fall in the value of GBP, since the Brexit vote last year, has resulted in higher prices paid for imported goods which will take up to three years to 'work its way through the economy'. With poor economic data, uncertainty over the Brexit process and a squeeze on real earnings the Bank of England's decision to hike rates is delicately balanced.

With raised tensions in the Middle East, the price of Oil rose on Tuesday as the markets are concerned that supply distribution could be disrupted. The API report out of the US showed a bigger than expected drawdown in US inventories which, when added to the fighting in Kirkuk, Iraq and the continued tensions between Iran and the US, helped push Oil prices higher. Official US fuel inventory will be released today by the EIA which may help push Oil prices higher if, as forecast, there is a significant drawdown.

China's President Xi Jinping delivered a keynote speech to the Communist Party congress in Beijing. The twice-a-decade congress is expected to cement the power of Xi who stated early on in his speech that the 'market will be allowed to play a decisive role in allocating resources'. 'Currently, conditions domestically and abroad are undergoing deep and complicated changes, our country is in an important period of strategic opportunity in its development,' he said in a calm, steady voice. 'The outlook is extremely bright; the challenges are also extremely grim.' The markets will be watching the congress meeting this week for any suggestion of whether Xi may be looking to appoint a successor to take over after his traditional second five-year term in office.

EURUSD is little changed in early Wednesday trading. Currently, EURUSD is trading around 1.1760.

USDJPY is trading close to Tuesday's close. Currently, USDJPY is trading around 112.30.

GBPUSD is currently trading near early session lows around 1.3182.

Gold is 0.12% higher in early trading. Currently, Gold is trading around $1,285.

WTI is 0.2% higher on Wednesday to currently trade around $52.32.

Major data releases for today:

At 09:10 BST, ECB President Mario Draghi is scheduled to present the opening speech at the ECB Conference 'Structural reforms in the euro area' in Frankfurt, Germany.

At 09:30 BST, UK National Statistics are scheduled to release Average Earnings including bonus (3Mo/Yr) for August. Consensus is calling for an unchanged 2.1%. The markets will be keen to see if UK average earnings are rising in line with inflation. If they are, we can expect the Bank of England to raise rates in the near future. If they are lagging inflation, then real earnings are lower and it may be difficult for the Central Bank to justify a rate hike.

At 13:00 BST, New York Federal Reserve Bank President William Dudley and Dallas Federal Reserve Bank President Robert Kaplan are scheduled to speak on New York & Texas (respectively) at the Centers of Growth breakfast conversation at Hearst, in New York.

At 13:30 BST, the Us Census Bureau, at the Department of Commerce, is scheduled to release Housing Starts Change for September. The previous poor release of -0.8% is expected to be improved upon with consensus suggesting a release of -0.5%. Whilst the data is still expected to be negative, the markets are aware that the recent Hurricanes are still impacting building in certain states.

At 15:30 BST, the US Energy Information Administration will release data for Crude Oil Stocks change for the week ending October 13. The consensus is calling for a drawdown of -4.750M compared to the previous draw of -2.747M. Expect volatility in Oil if the released number is significantly different from the consensus.

Currencies: Dollar Holds Cautiously Positive Bias

Sunrise Market Commentary

- Rates: No strong take on today's trading

Today's eco calendar contains US housing data and speeches by central bankers. The Bund's outperformance vs the US Note future is expected to last given dovish ECB rumours and European political risk, but we have no strong directional take for today's trading session. - Currencies: Dollar holds cautiously positive bias

The dollar slightly outperformed the euro and, to a lesser extent, the yen yesterday. Today's eco data are of second tier importance. Catalan uncertainty might remain a negative for the euro. Sterling didn't profit after UK inflation hit the 3%-mark as the Brexit stalemate weighs. Sterling traders look out for the UK labour market data today

The Sunrise Headlines

- US stock markets ended near opening levels with the Dow slightly outperforming and crossing the 23k mark intraday for the first time in its history. Asian bourses trade mixed overnight with China slightly outperforming.

- President Xi Jinping declared that China has “entered a new era” as he opened a landmark Communist party congress that will cement his status as a transformative leader alongside Deng Xiaoping and Mao Zedong.

- Philly Fed President Harker said the US labor market has "very little slack left." He sees one more rate increase in 2017 but the forecast could change if inflation doesn't pick up. He also expects three rate increases in 2018.

- Nafta talks are switching gears and slowing down as key obstacles emerge, with Canada and Mexico rejecting what they see as hard-line US proposals and negotiators exchanging their strongest public barbs yet.

- Oil prices extended gains with Brent crude above $58/barrel, lifted by a fall in US crude inventories and concerns that tensions in the Middle East could disrupt supplies.

- Two US senators reached a bipartisan agreement to shore up Obamacare for two years by reviving federal subsidies for health insurers that President Trump planned to scrap, and the president indicated his support for the plan.

- Today's eco calendar contains US Housing data and the UK labour market report. Several central bankers speak, including ECB Draghi. The US releases its Beige Book and Germany holds a 30-yr Bund auction

Currencies: Dollar Holds Cautiously Positive Bias

USD extends cautious rebound

The dollar continued the cautious uptrend that started Monday evening on headlines that chances of John Taylor becoming Fed chairman were rising. Catalonia moved temporary to the background as a driver for trading, but probably kept euro buyers on the side-lines. Higher than expected US import prices caused some further USD gains in the afternoon, but the rally petered out later. EUR/USD closed the session at 1.1766 (from 1. 1796). USD/JPY finished almost unchanged at 112.20.

Overnight, the focus in Asia is on the opening speech of Chinese President Xi Jinping at the Communist Party congress. However, there is no direct link to markets. Most Asian equity indices are trading marginally lower, with China outperforming. According to the foreign currency report of the US Treasury, no major trading partner is manipulation its currency. The assessment on the yuan was quite constructive. The US Treasury said that the yuan has recently moved in a direction that would help correct the bilateral trade imbalance with the US. USD/JPY is holding a very tight range in the 112.20/25 area. EUR/USD hovers around 1.1765.

There are no important eco data in the EMU today. US housing starts (-0.4% M/M) and building permits (-2.1%) are both expected to decline slightly. The data might be distorted by the hurricanes. Recent data from the sector were a bit diffuse and could even raise the question whether it is heading for a cooling down. Even so, we expect little impact on the dollar. The Fed will release the Beige Book preparing the November 1 policy meeting after the European close. Markets will look out for indications on price developments. There are again plenty of CB speakers including ECB's Praet and Draghi and Fed's Dudley and Kaplan. Markets will continue to look for clues on the ECB's APP. Markets considered recent indications/rumours as dovish. However, we don't expect the ECB policy makers to reveal important details. Technical considerations and global factors will continue to set the tone for USD trading. Catalonia remains a factor of uncertainty for the euro as Spain and the region are heading for a political confrontation. Earlier this week, we kept a neutral-to-tentatively negative bias for EUR/USD. We maintain this call. We remain cautious on USD/JPY. Recent price action was not convincing and event risk from whatever source might weight on the pair.

From a technical point of view, EUR/USD dropped below the 1.1823/ 1.2070 consolidation pattern, but no real test of the 1.1662 support occurred. Last week, the pair even returned (temporary?) above the 1.1823 previous range bottom, which was disappointing for EUR/USD bears. We maintain a cautious sell-on upticks bias. The pair needs to drop below 1.1670/62 support to really give comfort to EUR/USD bears. The USD/JPY momentum was constructive in September. The pair regained 110.67/95 (previous resistance), a short-term positive. The 114.49 correction top is the next important resistance. The rally clearly lost momentum last week. A break beyond 114.49 looks ever more difficult.

EUR/USD: continues gradual decline, but no important technical level within reach

EUR/GBP

Sterling rebound aborted

Sterling traded with a cautiously positive bias yesterday morning, ahead of the inflation data and the hearing of BoE governor Carney before Parliament. UK September inflation printed at 3.0% Y/Y, in line with expectations. Sterling reached an intraday high just after the inflation data. BoE Carney supported a rate hike, but stressed that the BoE is still facing the difficult balance between supporting growth and having inflation above target. His comments can be considered as an indication that any policy tightening will limited. Sterling more than reversed the initial gains. Cable tumbled one big figure and closed the day at 1.3190. EUR/GBP rebounded well north of 0.89 and closed at 0.8921.

UK labour market data will be published today. Consensus expects solid job growth (148k in the 3 months to August). Wage growth is expected at a very modest 2.1% Y/Y. Usually this report has market moving potential. However, we have the impression that a big surprise is needed. A limited BoE rate hike is discounted and the report probably won't change this scenario. So, the focus for sterling trading might return to Brexit going into tomorrow's EU summit. Recent price action suggests that sustained further sterling gains might face quite heavy headwinds as long as Brexit tensions remain as elevated as they are.

EUR/GBP staged a strong uptrend from April till late August to set a top at 0.9307. Rising UK inflation data and hawkish BoE comments reinforced a sterling rebound, but this rebound has run its course. EUR/GBP supports at 0.8743 and 0.8652 proved difficult to break. We look to buy EUR/GBP on dips. The recent rebound above 0.89 improved the ST technical picture of EUR/GBP, but for now there were no convincing follow-through gains. EUR/GBP 0.9026 is the 50% retracement of the recent countermove.

EUR/GBP: sterling rebound runs into resistance even as UK inflation reaches 3%.

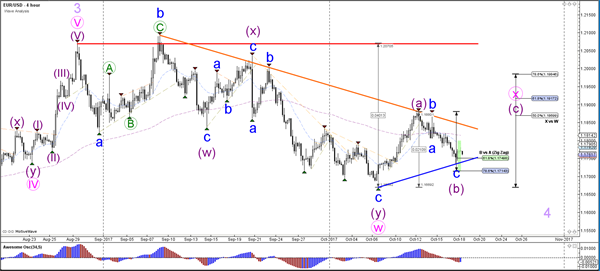

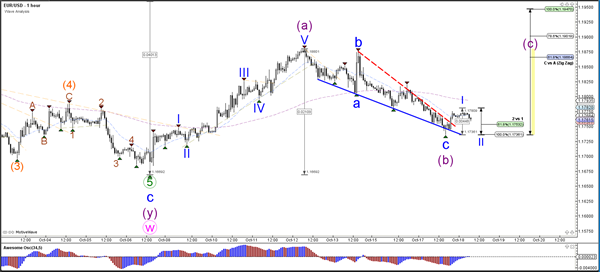

Daily Wave Analysis: EUR/USD Challenges Critical 61.8% Fibonacci Support Zone

Currency pair EUR/USD

The EUR/USD bounced at the 61.8% Fibonacci level of potential wave B (purple). A break above the resistance trend line (orange) would confirm a bullish breakout within wave C of wave X (pink). A break below the support trend line and 78.6% Fibonacci level makes a bullish ABC less likely and price will probably continue lower as part of wave 4 (light purple).

The EUR/USD broke above the falling wedge (dotted red) and could be building a wave 1-2 if price stays above the 100% Fibonacci level of wave 2 vs 1.

Currency pair GBP/USD

The GBP/USD offers two main scenarios where either a bearish ABC (green) or a wave 123 (green) is taking place. Price invalidates that wave 4 (orange) correction if price breaks above the resistance trend line (yellow). A break below the support trend line (blue) increases the chance of a bearish break within wave 5 (orange).

The GBP/USD broke below tow support trend lines (dotted blue) and fell towards the 50-61.8% Fibonacci levels. A bounce and break above resistance (yellow) could indicate a bullish structure whereas a bearish break could continue the wave 5 (orange).

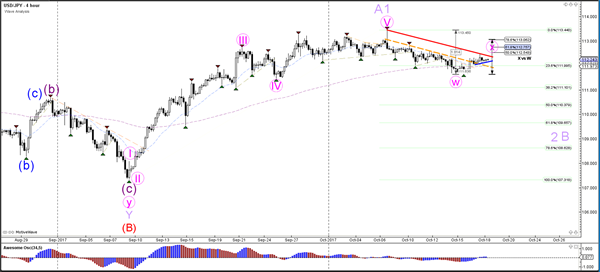

Currency pair USD/JPY

The USD/JPY could be building a larger WXY (pink) correction within wave 2 or B (purple).

The USD/JPY bullish break above the resistance trend line (dotted red) could be part of a bullish wave X (pink) correction.

German ZEW Expectations Came Out Higher At 17.6

Market movers today

In China, the 19th Congress of the Communist Party begins today, where the top leadership will see a big reshuffle. The Congress will reveal how much President Xi Jinping will st rengthen his power and is also likely to give a signal of a deepened reform focus.

In the UK, we are due to get the labour market report for August , which is likely to show no further reduct ion in the unemployment rate and unchanged wage growth and should hence not be a game changer for the Bank of England (BoE) members' view of t he economy ahead of the 2 November meet ing.

In Germany, coalition talks to form a ‘Jamaica' coalition of CDU/CSU, FDP and the Greens kicks off officially today but given large policy and ideological differences between the part ies, negot iat ions are expected to drag on and conclude only some t ime towards the end of this year.

Selected market news

Yesterday, final September euro area HICP figures confirmed the preliminary releases at 1.5% for headline and 1.1% for core inflation. In line with recent ECB communication, which point s t o a preference for a ‘lower for longer' scenario, we have changed our call and now expect the ECB to announce a QE extension by nine months at a pace of EUR30bn at the meet ing on 26 October.

Yesterday, German ZEW expectations came out higher at 17.6 in October (from 17.0 in September), in line with recent st rong readings in indust rial product ion and cont inued investor opt imism in the face of a robust eurozone growth out look, while the euro appreciat ion pace has abated somewhat . Current condit ions decreased slight ly to 87.0 in October from 87.9 in September, possibly due to some lingering uncertainty around German coalit ion building.

UK CPI inflation came out in line with expectations yesterday at 3.0% in September from 2.9% in August. Core inflation was unchanged at 2.7%. In line with market expectations, we expect the Bank of England to hike the Bank Rate by 25bp in November, which is current ly priced in with around an 85% probability in the UK money market .

According to Reuters Tankan monthly survey, there was strong confidence among Japanese manufacturers in October wi th sentiment at 31 versus 25 in September. The poll follows the bigger quarterly Bank of Japan survey from 2 October, which showed the most opt imist ic business out look for the manufacturing sector in a decade, and st rong export figures for Q3 so far.

US senators in both pol itical parties say that they have reached an agreement on fixes to stabi l ise Obamacare, according to Bloomberg. A deal has st ill to make it through both houses and be signed by President Donald Trump.

Elliott Wave View: AUDUSD

AUDUSD Elliott Wave structure suggests that the decline to 0.7731 on October 6th low ended Primary wave ((W)). From there, Primary wave ((X)) bounce is unfolding as a double three Elliott Wave structure. Rally to 0.7807 ended Intermediate wave (W) of ((X)) and pullback to 0.7815 ended Intermediate wave (X) of ((X)). A break above Intermediate wave (W) at 0.7815 will give more validity to this view. Until then, a double correction in Intermediate wave ((X)) is still possible. Near term, while pullbacks stay above 0.7815, but more importantly above 10/6 low at 0.7731, expect pair to extend higher.

AUDUSD 1 Hour Elliott Wave Chart

Double three ( 7 swings) is a common corrective pattern in Elliott wave’s theory. Another name for Double three is a 7-swing structure. It is a very reliable pattern that gives traders a good opportunity to trade with a well-defined level of risk and target areas. Below is the image of what what Elliott Wave Double Three looks like. It has labels of (W), (X), (Y) and an internal structure of 3-3-3. This means that all 3 legs has corrective sequences. Each (W) and (Y) is formed by 3 wave oscillations and has a structure of A, B, C or W, X, Y of smaller degrees.

GBP Steadies Ahead Of UK Jobs Data

- UK data likely to highlight tough job facing BoE policy makers;

- Draghi and Praet comments eyed as ECB plans to withdraw more stimulus;

- Dudley and Kaplan make appearances as speculation grows around Yellen’s replacement.

European markets are poised to open a little higher on Wednesday, as we await the latest labour market data from the UK and speeches from ECB and Federal Reserve policy makers.

The UK is a key focus for markets this week as traders try to determine whether or not the Bank of England will follow through on warnings that interest rates could rise at an upcoming meeting. Comments on Tuesday from Governor Mark Carney and two of his new colleagues on the MPC highlighted how close and tough the decision is, given the unfavourable economic outlook.

The September inflation data likely didn’t have much of an impact either way, with policy makers that were previously on the fence probably still perched up there now. With a hike next month now 76% priced in by markets according to Reuters, traders clearly need little convincing although I’m not convinced it’s that straightforward.

The labour market figures this morning will likely be closely monitored in the absence of any clear assistance from the CPI data. Once again though, the unemployment data is expected to paint one picture with the rate remaining at 4.3% while average earnings paints an entirely different one, as wages rise by only 2.1%. Negative earnings growth is one of the factors that is likely to weigh on the economy going forward and makes the BoE’s decision on interest rates all the more difficult.

Speeches from ECB President Mario Draghi and Chief Economist Peter Praet will also be closely followed today for hints at how the central bank will manage the process of reducing new asset purchases to zero over the next year or so. The ECB is expected to make an announcement next week, with the consensus reportedly favouring a €30 billion reduction until September, likely followed by a reduction to zero thereafter. Although given the cautious nature of the central bank, that is not something they will likely commit to or possibly even allude to even though the intent will be clear.

The Federal Reserve is never too far away from the spotlight, especially when President Donald Trump is interviewing candidates to succeed Janet Yellen when her term ends in February. The dollar has caught a bid in recent days following reports that Trump was impressed when interviewing John Taylor, who is seen as being more hawkish than Yellen. Who will replace Yellen, assuming her term isn’t extended will likely remain a hot topic and in the meantime, we will hear from a couple of her colleagues, Robert Kaplan and William Dudley, as the central bank prepares to raise rates one more time this year.

Market Update – Asian Session: Equities, FX Quiet Heading Into Earnings Season

Asia Summary

Asian equity markets opened the session mixed ahead of key events, including China's 19th Communist Party National Congress, which started today and the country's Q3 GDP data which is due tomorrow.

In Japan, the Nikkei and Topix indices opened slightly higher. If these indices are able to hold onto gains it would be the 12th and 8th straight rise, respectively. Tire manufacturer Bridgestone has gained over 1% after unveiling its medium term targets.

Japan's steel sector is broadly lower after outperforming in the prior session. Kobe Steel, Nippon Steel and JFE Steel have all declined by over 1.5%. In the retail space, Fast Retailing has gained over 1%. Shipbuilders in Japan are broadly lower amid reports that Nippon Yusen is facing delays regarding the replacement process for one of its cruise ships.

Iron-ore miner BHP has declined on the session, after affirming its FY18 production forecasts and reporting Q1 iron ore output that missed market expectations. The company said that production in the quarter was impacted by a fire that occurred at its Mt Whaleback screening plant in June. Amid the BHP report, iron ore miners Rio Tinto and Fortescue have traded slightly lower.

Australian infrastructure company, Lend Lease, has declined over 10% on its H1 guidance. Gaming company Crown Resorts has dropped over 5% amid whistleblower concerns. Meanwhile, supply-chain logistics firm Brambles has gained over 2%, after reporting 6% sales growth in Q1. Besides this, the company also noted a rebound in its US pallets business.

Some weakness has been seen in the South Korean chip sector. Samsung Electronics has declined on the session, while Hynix has traded lower by over 3% on above average volume. The latter is due to report earnings next Thursday on Oct 26th.

China's small-cap ChiNext index has opened the session higher, amid the start of the National Congress. According to an official from China's FX regulator (SAFE) the yuan exchange rate is expected to have a more stable foundation following this event. China's President Xi said the government will maintain overcapacity reductions and deleveraging efforts.

Looking ahead, China's Q3 GDP data is due to be released on tomorrow's session. According to one poll, y/y GDP is expected at 6.8%, even as PBoC Gov Zhou was quoted as saying H2 GDP growth was seen reaching 7%. China last had a y/y GDP reading of at least 7% in Q2 2015.

In terms of the ongoing New Zealand government coalition talks, First Party MP Patterson said his party was ‘getting close' to making a decision. Late yesterday, First Party Leader Peters said he wanted a decision before the end of the week.

The Aussie has seen some volatility ahead of the upcoming China growth figures and Thursday's release of the Sept employment change data.

Bank of Japan (BoJ) member Sakurai made comments in which he noted that the central bank's 2% inflation target will help stabilize FX rates, while the popularity of E-commerce is contributing to price competition among firms. In other central bank news, the Bank of Korea (BoK) is widely expected to leave rates unchanged at Thursday's policy meeting. However, according to a recent note by a tier 1 brokerage firm, the central bank could raise rates in 2018. The Bank of Korea last raised rates in 2011.

Fed's Harker, seen by some as a hawk, said he expected three rate increases in 2018. These comments are similar to recent remarks by Fed official Rosengren and echo what was seen in the most recent NY Fed primary dealer survey.

Meanwhile the US Treasury, in its Semi-annual Currency Report, removed Taiwan from its ‘watch list', but said Asian countries including China, Japan and South Korea should remain on its monitoring list. That being said, the Treasury concluded that no major trading was considered a currency manipulator.

Following the US equity close, IBM rose over 4% in the afterhours, despite reporting its 22nd straight quarter of declining revenues. In Q3, the tech giant's results exceeded market expectations and the company affirmed its FY earnings forecast. US companies due to report results on Wednesday include Alcoa, American Express, eBay and United Continental, among others.

Markets in Malaysia, Singapore and Sri Lanka are closed on today's session in observance of national holidays.

Key economic data

(AU) Australia Sept Westpac Leading Index m/m: +0.1% v -0.1% prior

Speakers and Press

Japan

(JP) Japan Trade Min Seko: Japan to offer $10B in financing for LNG projects

(JP) Bank of Japan (BOJ) member Sakurai: price moves are still weak and far from 2% target; important to continue with powerful easing under current framework

Korea

(KR) South Korea Finance Ministry Official: US putting S. Korea on currency monitoring list was expected; currency market movements should be market oriented

US Treasury Semi-annual currency report: No countries were named as currency ‘manipulators', China, Germany, Japan, South Korea and Switzerland were kept on the monitoring list. Taiwan was removed from the watch list.

China/Hong Kong

(CN) China President Xi: China will continue to grow at medium to high speed - work report at 19th National Congress

(CN) China FX Regulator SAFE: Expect yuan exchange rate to have more stable foundation after party congress

(CN) Yuan not likely to see sharp depreciation, reaffirms currency to be basically stable – China Securities Journal

(HK) According to Centaline Hong Kong 2017 homes sale may reach new record of HK$186.9B - HK press

(CN) Follow Up: China Total holding of US Treasuries: $1.20T v $1.17T prior (largest increase since July 2016, 7th consecutive purchase) - part of TIC Flows

Australia/New Zealand

(AU) According to MinEx Consulting Australia gold production to peak in 2021

US

(US) Fed's Harker (hawk, voter): Sees one more rate increase in 2017 and 3 in 2018 - financial press

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.1%, Hang Seng +0.0%; Shanghai Composite +0.3%; ASX200 +0.1%, Kospi -0.2%

Equity Futures: S&P500 +0.0%; Nasdaq100 +0.1%, Dax +0.1%; FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1781-1.1765; JPY 112.27-112.13; AUD 0.7858-0.7842;NZD 0.7178-0.7160

Dec Gold +0.3% at $1,289/oz; Nov Crude Oil +0.5% at $52.13/brl; Dec Copper +0.1% at $3.20/lb

(CN) China PBOC injects CNY300B in combined 7-day and 14-day reverse repos v CNY190B prior; injects net CNY270B

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.5991 V 6.5883 PRIOR

(CN) China MoF sells 2-yr bonds; avg yield 3.5619% v 3.58%e

(JP) Japan MoF sells ¥1.897T in 1-yr JGBS, avg yield -0.1687%; bid-to-cover 5.25x

FCG.NZ Bank of New Zealand cuts 2017-18 milk price forecast to NZ$6.30 from NZ$6.75/kg milksolids

(CN) China sells 5-yr bonds at 3.73% (highest yield since May 2014)

Equities notable movers

Australia/New Zealand

BHP.AU Reports Q1 Iron Ore Production (attributable basis) 55.6Mt v 58.6Mte v 57.6Mt y/y; -1%

LLC.AU Guides H1 Australia construction unit EBITDA lower y/y due to under performance of a small number of engineering projects; -9%

ADO.AU Receives Positive Assessment of Battery IP; +111%

PRT.AU Reports Q1 ad Rev -19.1% y/y; -15%

Japan

5713.JP Said to expand production of EV batteries - financial press; +4.1%

China/Hong Kong

1030.HK Privatization plan not approved; +6.8%

Aussie Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the AUD declined 0.08% against the USD and closed at 0.7842.

LME Copper prices declined 0.2% or $17.0/MT to $7046.0/MT. Aluminium prices declined 1.5% or $33.0/MT to $2111.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7852, with the AUD trading 0.13% higher against the USD from yesterday's close.

Overnight data indicated that Australia's Westpac leading index rebounded 0.08% on a monthly basis in September. In the prior month, the index had fallen by a revised 0.10%.

The pair is expected to find support at 0.7826, and a fall through could take it to the next support level of 0.7801. The pair is expected to find its first resistance at 0.7869, and a rise through could take it to the next resistance level of 0.7887.

Looking forward, traders would keep a close watch on Australia's unemployment rate data for September, slated to release overnight.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average