Sample Category Title

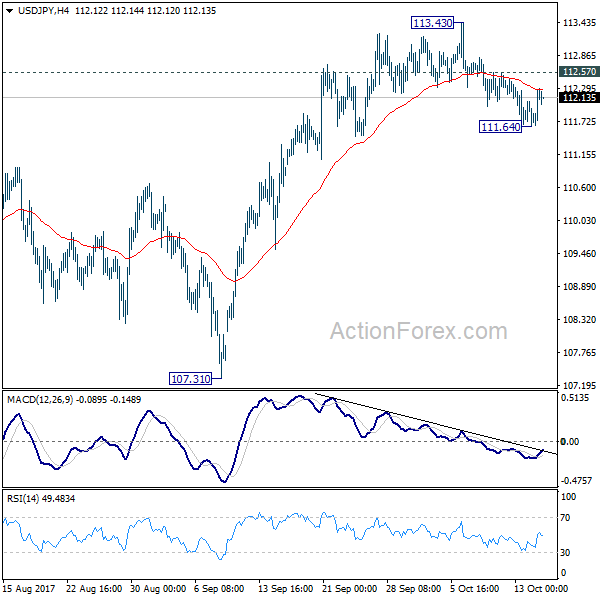

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.79; (P) 112.04; (R1) 112.42; More...

A temporary low is in place at 111.64 in USD/JPY and intraday bias is turned neutral first. Another decline is expected as long as 112.57 minor resistance holds. Below 111.64 will target 55 day EMA (now at 111.40) first. Sustained break there will target 107.31 and possibly below. Nonetheless, above 112.57 will bring retest of 113.43. Break there will resume whole rise from 107.31 for 114.49 key resistance.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

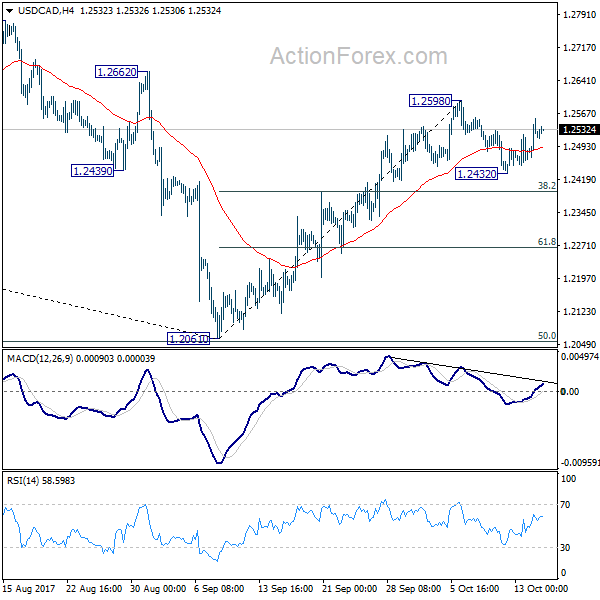

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2467; (P) 1.2512; (R1) 1.2563; More....

USD/CAD's recovery suggests that pull back from 1.2598 has completed at 1.2432 already. Intraday bias is turned back to retest 1.2598 first. Break will extend the rebound from 1.2061 to 1.2777 resistance next. In case the consolidation from 1.2598 extends with another fall, downside should be contained by 38.2% retracement of 1.2061 to 1.2598 at 1.2393 to bring rally resumption.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

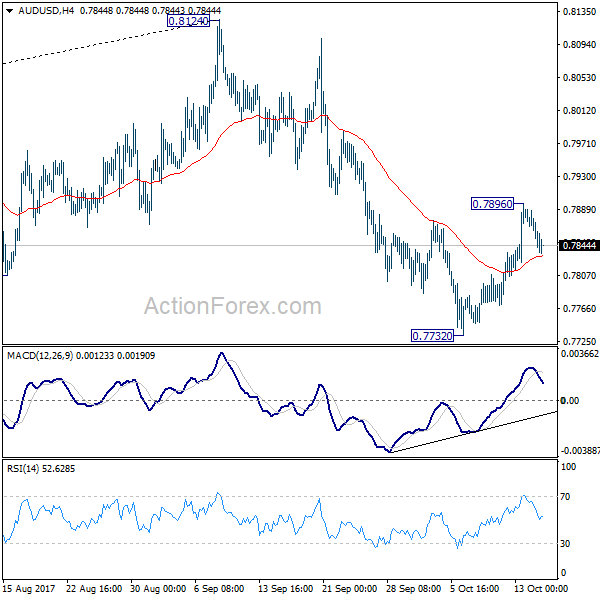

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7833; (P) 0.7861; (R1) 0.7879; More...

AUD/USD lost momentum after hitting 0.7896 and retreated. A temporary top was formed and intraday bias is turned neutral first. Another rise is mildly in favor for the moment. Break of 0.7896 will target a test on 0.8124 high. But we'd be cautious on strong resistance from there to limit upside and bring another fall to extend the corrective pattern. On the downside, break of 0.7732 will resume the decline from 0.8124 and target medium term fibonacci level at 0.7628 first.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will firm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

Australia Dollar Mildly Lower after RBA Minutes, British Pound Firm ahead of CPI

Dollar trades mildly higher this week even though momentum is relatively week. US equities extended the record runs, with DOW, S&P 500 and NASDAQ closing at new records overnight. Treasury yields also recovered mildly. But there is little support to the greenback yet. The forex markets are generally mixed in consolidative mode, except that some extra weakness is seen in Euro, due to political jitters. Meanwhile, Australia Dollar is trading a touch softer after RBA minutes. Sterling, on the other hand, is firm as markets await inflation data from UK.

RBA minutes give no sign of tightening soon

The minutes of RBA's October meeting showed that "the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time." The central bank acknowledged that "strengthening in global economic conditions had reduced some near-term risks to financial stability arising from rare or extreme events." But, it warned that "low interest rates and low financial market volatility had promoted financial risk-taking." Overall, there is practically no sign from RBA that indicates a rate hike soon. And considering sluggish wage growth that suggests plenty of spare capacity, RBA is no where near tightening. There are talks that RBA could stand pat throughout 2018.

NZ CPI beat expectations, but no change to RBNZ's stance

New Zealand CPI rose 0.5% qoq 1.9% yoy in Q3, up from prior 0.0% qoq 1.7% yoy, and beat expectation of 0.4% qoq 1.8% yoy. It's also well above RBNZ's own projection of 1.6% yoy. Still, it's believed that RBNZ won't change it's neutral stance on monetary policy. So far, there is little signs of overheating in the economy that points to higher inflation ahead. Instead, the economy could be entering a slowing phase.

Former EM Takenaka: Abe win will push the tide towards Kuroda

In Japan, former Economy Minister Heizo Takenaka hailed that BoJ Governor Haruhiko Kuroda has done an "excellent job" and "should continue" after his term expires next year. He pointed out that after Kuroda's massive stimulus policy, prices have stopped falling, and the economy is in better shape. And, according to Takenaka, a win for Prime Minister Shinzo Abe in the October 22 election will "of course push the tide" towards another term for Kuroda. He noted that "there is a sufficient amount of trust between the government and the BoJ for that to happen". Also, renewing Kuroda's term will raise expectations for appropriate policies but "a shift in personnel can change expectations at once".

May and Juncker agreed to accelerate Brexit negotiation

UK Prime Minister Theresa May and European Commission President Jean-Claude Juncker had a "constructive and friendly" dinner in Brussels yesterday. Coming out of the meeting, they said there was a "broad, constructive exchange on current European and global challenges". And in a joint statement regarding Brexit, they "reviewed the progress made in the Article 50 negotiations so far and agreed that these efforts should accelerate over the months to come." Separately, it's reported that despite brief objections by France and Germany, a revised draft circulated by European Council President Donald Tusk retains the option open for Brexit negotiations to move on to trade as soon as after December EU summit.

Looking ahead

UK inflation data will be the main focus of the day. CPI is expected to finally hit 3% mark in September, solidifying the case for a BoE rate hike in November. But it should be noted that, that rate hike would only bring interest rate back to pre-Brexit referendum level. And based on the current uncertainty around Brexit negotiations, there is little chance for BoE to start a tightening cycle. RPI and PPI will also be released from UK.

Elsewhere, German ZEW economy sentiment and Eurozone CPI final will be featured in European session. US will release import price index, industrial production and NAHB housing index later in the day.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7833; (P) 0.7861; (R1) 0.7879; More...

AUD/USD lost momentum after hitting 0.7896 and retreated. A temporary top was formed and intraday bias is turned neutral first. Another rise is mildly in favor for the moment. Break of 0.7896 will target a test on 0.8124 high. But we'd be cautious on strong resistance from there to limit upside and bring another fall to extend the corrective pattern. On the downside, break of 0.7732 will resume the decline from 0.8124 and target medium term fibonacci level at 0.7628 first.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will firm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q3 | 0.50% | 0.40% | 0.00% | |

| 0:30 | AUD | RBA Meeting Minutes Oct | ||||

| 8:30 | GBP | CPI M/M Sep | 0.30% | 0.60% | ||

| 8:30 | GBP | CPI Y/Y Sep | 3.00% | 2.90% | ||

| 8:30 | GBP | Core CPI Y/Y Sep | 2.70% | 2.70% | ||

| 8:30 | GBP | RPI M/M Sep | 0.30% | 0.70% | ||

| 8:30 | GBP | RPI Y/Y Sep | 4.00% | 3.90% | ||

| 8:30 | GBP | PPI Input M/M Sep | 1.20% | 1.60% | ||

| 8:30 | GBP | PPI Input Y/Y Sep | 8.20% | 7.60% | ||

| 8:30 | GBP | PPI Output M/M Sep | 0.20% | 0.40% | ||

| 8:30 | GBP | PPI Output Y/Y Sep | 3.30% | 3.40% | ||

| 8:30 | GBP | PPI Output Core M/M Sep | 0.10% | 0.20% | ||

| 8:30 | GBP | PPI Output Core Y/Y Sep | 2.60% | 2.50% | ||

| 8:30 | GBP | House Price Index Y/Y Aug | 5.40% | 5.10% | ||

| 9:00 | EUR | Eurozone CPI M/M Sep | 0.40% | 0.30% | ||

| 9:00 | EUR | Eurozone CPI Y/Y Sep F | 1.50% | 1.50% | ||

| 9:00 | EUR | Eurozone CPI - Core Y/Y Sep F | 1.10% | 1.10% | ||

| 9:00 | EUR | German ZEW (Economic Sentiment) Oct | 20 | 17 | ||

| 9:00 | EUR | German ZEW (Current Situation) Oct | 88.5 | 87.9 | ||

| 9:00 | EUR | Eurozone ZEW (Economic Sentiment) Oct | 34.2 | 31.7 | ||

| 12:30 | USD | Import Price Index M/M Sep | 0.60% | 0.60% | ||

| 13:15 | USD | Industrial Production Sep | 0.20% | -0.90% | ||

| 13:15 | USD | Capacity Utilization Sep | 76.20% | 76.10% | ||

| 14:00 | USD | NAHB Housing Market Index Oct | 64 | 64 | ||

| 20:00 | USD | Net Long-term TIC Flows (USD) Aug | 14.3B | 1.3B |

Market Morning Briefing: Dollar-Yen Looks Mixed/ Bullish

STOCKS

Overall global stock indices look bullish just now. While Dow could be poised for some more upmove in the coming sessions, Nikkei and Dax may possibly see a pause near current levels.

Dow (22956.96, +0.37%) is slowly rising and could move up towards 23000-23250 levels in the near term. Thereafter a small dip is possible towards current levels. Near term looks positive.

Dax (13003.70, +0.09%) has paused slightly just at the crucial resistance level and a sharp break above current levels is needed to initiate fresh bulls in the near to medium term. Else a corrective dip from here is possible, taking the index back towards 12800 levels.

Nikkei (21260.89, +0.03%) came off after testing 21400 on the upside. As mentioned yesterday, Nikkei looks overbought and a slight correction from here is preferred which could take the price down towards 21100 or lower. A failure to stop at 21400 (if seen) may take it higher to 21500/600 in the near term.

Shanghai (3372.73, -0.17%) has some scope of testing 3350/60 on the downside before re-attempting a rise towards 3410.

Nifty (10230.85, +0.62%) looks positive this week and could move up towards 10300/10 levels if the bulls continue to remain strong. Near term looks bullish.

COMMODITIES

Gold (1293.38) has come off as expected. While 1308 holds, the price could test 1280 before again rising back in the medium term.

Silver (17.20) is likely to test 17 before again bouncing back towards 17.35/40 again in the medium term. For now some sideways movement within 17.00-17.50 is preferred.

Brent (57.83) and WTI (51.81) are almost stable near levels seen yesterday. Both made an intra-day high yesterday to 58.47 and 52.37 respectively but came off to close at lower levels. There is some scope that the prices may move up in the near term towards 59 and 53 respectively.

Copper (3.2315) has moved up sharply to test immediate resistance levels seen on the line charts. A rejection from these levels looks possible in the next few sessions towards 3.15/10. Else a rise to 3.30/35 is likely before a sharp corrective fall is seen.

FOREX

Although we are bullish on the Euro (1.1780) in the longer term, with Support at 1.1730, we also notice possibilities of a Bear Shoulder-Head-Shoulder developing. A break/ close below 1.1700 could negate the bullish prospect.

We prefer bullishness on the Euro because the Dollar Index (93.35) may have Resistance between current levels and 93.50.

But, there are warning signs coming from Euro-Yen (132.05) which could be breaking its uptrend and from the German-US 10Yr Spread (-1.93%), which is trading below its earlier support trendline. Also, US yields have moved up (see Interest Rates below). So, we need to be careful about our current bullishness on the Euro.

Dollar-Yen (112.09) looks mixed/ bullish. The Pound (1.3258) has slipped a bit since yesterday and so has the Aussie (0.7850).

Dollar-Rupee (64.74/75) might start moving up soon, even though the NDF shows 64.70/74.

INTEREST RATES

Contrary to expectation, US Bond yields (5yr 1.96%, 10Yr 2.31% and 30Yr 2.82%) have moved up yesterday instead of coming down towards 1.81%, 2.21% and 2.72% respectively.

The US Yield Curve itself has flattened quite a bit, with a dramatic decline in the 10-5 Spread from 0.41% on 3rd Oct to 0.35% now. The 30-5 (0.87%) continues to be in a long-term downtrend that could potentially target 0.75%.

German Yields (5Yr -0.34% and 10Yr 0.37%) could have Supports here, but they seem to be rising slower than US yields.

In India too, we may see the Indo-US 10r Spread (4.4541%) come down.

EUR/JPY Taps Important Level Once Again

Remember the EUR/JPY retesting confluence of support setup that we were trading? Well we're back!

This is a prime example of what actually normally happens once a trend line breaks. We see sideways consolidation followed by price simply moving back in the direction of the original trend:

EUR/JPY Daily:

But it's the marked horizontal level that I really wanted to highlight this morning. By looking for confluence of support and backing up trend lines with solid horizontal levels, you're giving yourself that backstop. There is no subjectivity in a straight line and as you can see here, the level has been touched again basically to the pip.

So long as price is above the higher time frame zone that is also on that chart, these sorts of pullbacks should be looked at as possible buying opportunities.

Topsy Turvy Tuesday?

Topsy Turvy Tuesday?

Dealers have spent the last 24 hours digesting Friday's CPI fallout while keeping an eye on geopolitical risk amidst the deluge of Fed chair speculative headlines. As for the dollar, there was nothing earth-shattering within these idiosyncratic storylines usurping any broader USD trend. All in all, it made for a somewhat sleepy Monday in G-10

It's not wise getting too comfortable as tranquil Monday's tend to foreshadow a climatic tipping point and today's substantial economic diary could prove to be a real test of investor sentiment.

Also, it's worth keeping an eye on the expanding laundry list of geopolitical flashpoints. We're not only dealing with issues in the Korea Peninsula, but now an unpopular shooting war between Iraqi forces and the Peshmerga is full blown. With Turkey-US relations souring, and as the world is still trying to figure out what to do with ISIS, the Middle East looks like a powder keg waiting to explode.

Fed Chair debate

There's a growing buzz surrounding Stanford's Taylor who is suggested to be in Trump's good books, while the lack of impressive academic credential seems to be weighing negatively for former frontrunner Kevin Warsh. Also, Yellen is rumoured to be meeting with the president this week, and she is expected to be the last primary candidate interviewed for the job suggesting that decision time is near.

Euro

Traders continue to probe the EUR downside resolve after last weeks dovish Draghi comments and a slight rise in EU political risk in the wake of the surprising Austrian elections The EUR was primarily offered against the crosses with EURJPY looking suspectable to the bid tone on USDJPY.

Australian Dollar

The AUD was G-10 worst performer overnight despite the common signals suggesting otherwise. Metals ratcheted higher on very optimistic growth forecasts coming out of the Communist Party Summit. Also, yesterday's China Data supported regional risk, so the overnight AUD sell-off is a bit surprising. However, the reversals is likely more a case of traders taking profit ahead of the RBA Minutes based on their well-known dovish guidance

The British Pound

Brexit headlines continue to batter the Pound but with UK CPI report for September; and the testimonies of three key BoE members (Carney and for the first time, members Ramsden and Tenreyro) on tap, sterling traders will be buckling in for a bumpy ride. UK inflation is sitting just shy of the 3%, and if Septembers forecast to touch the elevated 3 % level, it will exert immense pressure on the BoE to begin the tightening cycle and should play positively for the Pound. Keep in mind; Carney has been extraordinarily Hawkish of late so his testimonies will also be a central focus for traders this afternoon.

Japanese Yen

The anticipated wave of dollar selling after last Friday's weak CPI failed to gain much traction below 111.75, and then USD bounced to 112.20 on Bloomberg headlines reiterating that Taylor is in Tumps good books. Thre remains an air of apprehension to sell dollar this week as traders are looking over their shoulder as hawkish Fed Chair headlines unfold.

Little to report ahead of the election this coming Sunday, where Abe continues to look strong. A substantial outcome for Abe should, in turn, mean a weaker JPY.

Chinese Yuan

Chinese data was robust but had a minor impact on currency markets. Unquestionably, the market is sitting tight while keeping eyes peeled and ears to the ground for any groundbreaking policy shift to come out of the Chinese Communist Pary Congress

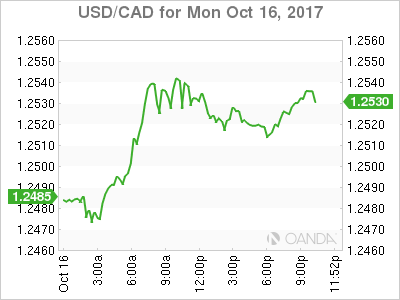

USD/CAD Canadian Dollar Lower As Growth Expectations Drop

The Canadian dollar depreciated on Monday after the release of the Bank of Canada (BoC) survey of managers. The Business Outlook Survey fell from 2.81 last quarter to 0.86. The anticipated slowdown in economic growth after it expanded at an accelerated growth was reflected in the reduced forecasts. The end result still points to a healthy economy, but not at the same pace that put the central bank into hiking rates twice.

The NAFTA negations have been anything but smooth sailing. The US trade delegation has been pushing for more America First clauses that have not been taken well by the Canada and Mexico delegations. The US tabled an idea a higher regional content for autos to be part of the free tariff access. Current North American content requirement is 62.5 percent and the US wants to increase that to 85 percent (with 50 percent of that being US content).

Negotiations have been tense after the US also proposed a five year term for the updated NAFTA, to which both Canada and Mexico had already objected. US and Mexican governments wanted to wrap up trade negotiations before the end of the year, but with the current pace of progress make this very unlikely.

The USD/CAD rose 0.47 percent since the Asian open. The currency pair is trading at 1.2528 as the US Empire State Manufacturing index posted a higher than expected figure. The survey of NY manufacturers was 30.2 on a 20.3 forecast. The combination of a softer BoC Business Outlook Survey in Canada and a stronger manufacturing indicator in the US further tipped the scales in favour of the US dollar.

NAFTA uncertainty has put the Bank of Canada (BoC) on alert as the loonie could lose up to 10 percent of its value if the Trump administration ends the agreement with no renegotiation. The central bank will meet next week, with 20 percent probability of a rate hike, but since the September rate hike and with a softer pace of growth a third rate hike in 2017 is still a long shot. Inflation and retail sales data later in the week will be more telling on what the BoC could do before the end of the year.

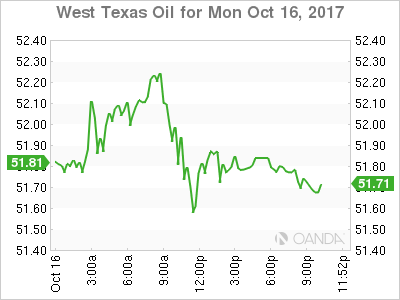

West Texas Intermediate prices have been volatile due to geopolitical events but seem to be attracted to the 51.80 level. The disruption of oil production from Kirkuk in Northen Iraq after the army seized the territory from Kurdish fighters drove prices to the $52.30. The situation is still ongoing, but for now prices remain stable below $52.

The comments from US President Donald Trump threatening to end the Iran nuclear had a positive effect on prices as lower output from oil pushed prices higher. The US congress has a 60 day period to decide if it reinstates the economic sanction to Iran.

Market events to watch this week:

Monday, October 16

5:45pm NZD CPI q/q

8:30pm AUD Monetary Policy Meeting Minutes

Tuesday, October 17

Tentative GBP BOE Gov Carney Speaks

4:30am GBP CPI y/y

Wednesday, October 18

4:30am GBP Average Earnings Index 3m/y

8:30am USD Building Permits

10:30am USD Crude Oil Inventories

8:30pm AUD Employment Change

10:00pm CNY GDP q/y

10:00pm CNY Industrial Production y/y

Thursday, October 19

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, October 20

8:30am CAD CPI m/m

8:30am CAD Core Retail Sales m/m

7:15pm USD Fed Chair Yellen Speaks

$1300 Gold Pauses After Strong Week

Gold prices are unchanged in the Monday session. Currently, the spot price for an ounce of gold is $1303.94, up 0.04% on the day. On the release front, there are no major releases out of the US. The Empire State Manufacturing Index soared to 30.2 points, easily beating the estimate of 20.3 points. This was the indicator's highest level since 2009.

Gold prices climbed 2.2 percent last week, as the metal closed on Friday above the symbolic $1300 level. The gold rally continued on Friday, as investors were disappointed that September CPI and Core CPI both missed their estimates. Low inflation levels continue to frustrate Fed policymakers, many who have predicted that a strong US economy and red-hot labor market will boost inflation levels. With inflation an important consideration in future rate decisions by the Federal Reserve, investors will be anxiously monitoring how Fed policymakers respond to September's soft inflation numbers. So far, the soft inflation numbers have not affected the odds of a December rate hike, as fed futures have currently priced a December hike at 91 percent.

The crisis over Catalan independence is at a deadlock, in if the situation escalates, nervous investors could dump euros in favor of safe assets such as gold. Last week, the Spanish government set a Monday deadline for Catalan President Carles Puigdemont to expressly state whether he had declared independence, and if so, Puigemont was given three more days to retract his proclamation. However, the Catalan President shirked away from a clear answer and let the first deadline pass, calling for more dialogue with Madrid. Prime Minister Mariano Rajoy has threatened to suspend the Catalan parliament and impose direct rule from Madrid, which could trigger a violent response. The crisis has led 500 companies to start leaving Catalonia, and the Standard and Poor's rating agency has said that the region could face a recession if the crisis continues.

Elliott Wave Trade Ideas Performance Update

4 positions were entered last week with total loss of 100 points and the positions are listed below.

9 Oct : EUR/GBP - Short at 0.8930, exited at 0.8970 (- 40 points)

10 Oct : EUR/JPY - Short at 132.40, exited at 133.00 (- 60 points)

13 Oct : GBP/USD - Short at 1.3315,

16 Oct : AUD/USD - Short at 0.7875,

| AUD EUR/JPY EUR/GBP CAD GBP GBPJPY

Jan - 15 -275 - 35 -120

Feb + 140 -17 - 40 +11

Mar - 20 +115 +132 - 19

Apr + 30 - 40 +120 + 45

May - 55 +100 - 6 -65 -60

Jun + 81 +150 - 10 +185 -120 +205

Jul - 40 - 60

Aug +155 +200 + 100 + 195 -45 - 50

Sep -50 + 165 + 5

Oct - 60 - 40 +200

Nov

Dec

Y-T-D + 371 + 8 +127 +823 -230 +285