Sample Category Title

Markets Muted To FOMC As Inflation Puzzles Officials

The FOMC meeting minutes released late yesterday showed a mixed outlook as policy makers were divided on interest rate hikes. While some officials preferred for rates to be hiked, others preferred to wait for more evidence.

Besides the FOMC minutes, Fed speak over the day included Evans who questioned whether more accommodative policy was required to boost inflation while on the other hand, George said that the Fed should continue with its gradual rate hikes.

On the economic front, data was relatively quiet. Looking ahead, the US producer prices index data will be released today. Estimates point to a 0.4% increase on the headline PPI while core PPI is expected to rise 0.2% on the month. ECB President Mario Draghi will be speaking today followed by FOMC members Powell and Brainard.

It Is All About Inflation

When the Federal Reserve met on 19-20 September, it announced the start of winding down the $4.5billion balance sheet and maintained plans for a thirdrate hike in 2017. The statement reflected confidence in economic activity, particularly the pickup in household spending and growth in business investments. DespiteHurricanes Harvey and Irma, the central bank was still confident that the U.S. economy would keep its momentum, and Janet Yellen sounded more hawkish than markets anticipated. This was all good news for the U.S. dollar, which rallied for three weeks after the meeting, appreciating 2.3% against a basket of currencies.

The primary concern was low inflation. Fed chair Janet Yellen, described it as something of a "mystery." When an institution that employs over 300 Ph.D. economists,not knowing whether low inflation is persistent or transitory, the risk of tightening monetary policy further might be a huge policy mistake if inflation does not return to normal levels. The Phillips curve model, which theorisesthat there should be a strong inverse relationship between unemployment and price inflation, is apparently not working;it is probably time for the Fed to abandon this theory, and find new models.

Yesterday's Fed minutes reflected such worries. Several members insisted that the decision of raising rates for the third time in 2017 should depend on economic data, which underscores their belief that inflation would move towards the Fed's 2% inflation target. The dollar bulls did not like the statement, despite expectations of a December rate hike remaining above 80%, according to CME's FedWatchTool. The Dollar Index continued to fall for the fifth day in a rowon Thursday, with overall declines of 1.5% from 6 October highs.

Given that inflation has become the most important economic metric impacting the dollar's direction, today's PPI and more importantly, tomorrow's CPI should be watched very closely. Any upside surprise would curb the dollar's fall; however, a disappointing figure would be an excuse to keep dragging the USD lower.

The Euro performed very well, climbing to the highest level in more than two weeks at 1.1878. After Carles Puigdemont suspended the process of Catalonia's independence, Spain's Prime Minister, Mariano Rajoy, has given him five days to say whether or not he has declared independence. Depending on the response, the government in Madrid could impose direct rule on Catalonia. I think the overall crisis in Spain is still underpriced, and if no agreement is reached in the next couple of days, the stability of the Eurozone as a whole would be at risk. Although economic fundamentals continue to support a stronger Euro, politics will play a significant role as to where the Euro heads next. ECB's Mario Draghi will participate in the annual meetings of the World Bank Group and the IMF in Washington today. Any new hintsof ECB's next move will move the single currency.

Despite no advances made in the Brexit negotiations, Sterling continued to trade higher against the dollar for the fourth consecutive day. Although Brexit will keep weighing on Sterling in the longer run, monetary policies seem to be the major driver for now. Expectations of BoE raising rates in the final quarter of 2017 remained high, thus narrowing monetary policy divergence within the Federal Reserve. I think in the next couple of days, Sterling will be driven by economic data rather than Brexit negotiations.

Forex: Fed Minutes: The Inflation Conundrum

USD broadly declined as the markets digested the release of last month’s FOMC meeting minutes. Many FOMC Members are still concerned with persistently low inflation, which is perplexing many as the US experiences a strong labour force, low unemployment, an increase in average hourly earnings and falling Jobless Claims, which should create inflationary pressure – but has had little effect to date. However, the minutes showed most policymakers believe another rate hike later this year “was likely to be warranted”, although they will be assessing upcoming inflation data in the months ahead.

EUR continued its recent strengthening trend on Wednesday after Spanish Prime Minister Rajoy did not suspend Catalan’s Government, although he could start the process that would lead to such a suspension. Reports suggest that Rajoy will need an explanation from Catalan President Puigdemont as to his recent comments about his “mandate for independence” and his appeal for discussions with Eurozone members before advancing the process. Rajoy could still decide to disband the Catalan Government and move power to Madrid. The markets took this as a positive sign for the Eurozone and, subsequently, bought EUR against its peers, even though there is uncertainty as to how these discussions could pan out.

EURUSD is nearly 0.2% higher in early Thursday trading. Currently, EURUSD is trading near the session high at 1.1877.

USDJPY is relatively unchanged overnight. USDJPY is currently trading around 112.40.

GBPUSD edged higher, on general USD weakness, to currently trade around 1.3260.

Gold is 0.25% higher in early Thursday trading. Currently, Gold is trading around $1,295.

WTI is little changed overnight, currently trading around $51.25pb.

Major data releases for today:

At 15:30 BST, the US Bureau of Labor Statistics, Department of Labor will release Producer Price Index excluding Food & Energy (MoM & YoY) for September. The Month-on-Month data is forecast to come in at 0.2% from the previous release of 0.1%. Year-on-Year is expected to remain the same at 2%. Producer Price Index (MoM) for September will also be released. Consensus is suggesting an increase to 0.4% from August’s reading of 0.2%. Such increases will add more likelihood for a rate hike in December by the Fed.

At 15:30 BST, the US Department of Labor will release Initial Jobless Claims for the week ending October 6th & Continuing Jobless Claims for the week ending September 29th. The resiliency of the US Labor Market has seen Initial claims forecast to come in at 251K (prev. 260K) with Continuing Claims forecast to be little changed at 1.935M (prev. 1.938M).

At 16:00 BST, the Chief Economist of the Bank of England, Andrew Haldane, is scheduled to speak as a panellist at the Rethinking Macro Policy Conference in Washington D.C.

At 17:30, FOMC Members Brainard and Powell are scheduled to speak. Brainard is a Panelist at the Rethinking Macro Policy Conference in Washington D.C, USA. Powell is scheduled to speak at the Institute for International Finance Spotlight on Emerging Markets also in Washington, D.C.

At 17:30 BST, ECB President Draghi is scheduled to speak at the Annual Meeting of the World Bank Group and the IMF in Washington, D.C.

At 18:00 BST, the US Energy Information Administration will release Crude Oil Stocks change for the week ending October 6th. Another drawdown is expected of -1.8M, which is significantly lower than the previous drawdown of -6.023M.

USD/JPY Still Heavy

Price is trading in the red on the short term and still tries to reach new lows. A further drop will be confirmed only after a valid breakdown below the 111.98 level. Technically, it should drop after the false breakout above the median line (ml) of the minor ascending pitchfork, but it was paused by the Nikkei’s rally.

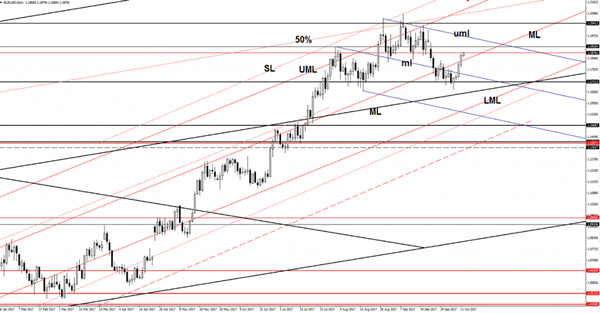

EUR/USD Euro On The Run

The EUR/USD increased and extended the upside momentum as the USD is weakened by the USDX’s massive drop. Price has managed to breakout above the median line (ML) of the ascending pitchfork and is almost to reach the 1.1910 next upside target. Technically, it should approach and reach also upper median line (uml) of the minor descending pitchfork. A valid breakout will announce a further increase, the next major target will be the 1.2041 horizontal obstacle.

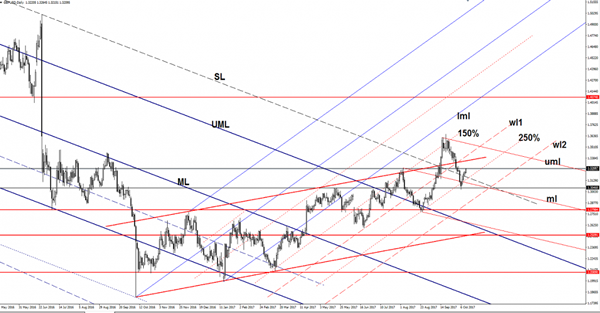

GBP/USD Throwback In Play

The GBP/USD rallies and tries to reach new highs on the short term. GBP has taken the lead again and appreciates versus all its rivals not only against the greenback. The dollar drops versus all its rivals as the USDX has touched new lows even if the FOMC Minutes have signaled a potential rate hike in December.

The USDX dropped much below the 93.00 psychological level and should drop much deeper in the upcoming days. USDX is still expected to approach the 92.49 static support, where he may find support again. Most likely the dollar index will develop an Inverse Head and Shoulders pattern on the Daily chart, which will signal a USD dominance in the upcoming weeks.

The USD is somehow expected to climb much higher in the upcoming weeks ahead of the December potential hike.

The GBP/USD is trading in the green and ignored the outside sliding parallel line. Price is challenging the 1.3268 static resistance and is expected to take this out as well and to approach the upside line of the ascending channel.

I've said in the previous reports that the perspective remains bullish on the short term as long as is trading within the ascending channel between the 150% and 250% Fibonacci lines. A retest of the 250% Fibonacci line will confirm an increase towards the upper median line (uml) of the minor descending pitchfork.

Currencies: EUR/USD Extends Comeback

Sunrise Market Commentary

- Rates: Consolidation phase to continue

The eco calendar remains rather dull today. The Spanish matter remains a factor of uncertainty. JP Morgan and Citigroup are the first big companies to report Q3 earnings and can influence intraday sentiment via stock markets. Central bank speakers are wildcards. We expect the consolidation/correction higher in core bonds to continue. - Currencies: EUR/USD extends comeback

EUR/USD continued the rebound from earlier this week. The move was due to overall dollar softness. Catalan developments hardly affect the single currency. US PPI data are expected to rise today. However, USD investors probably want a clear signal from tomorrow's key US data before changing tactics on the dollar

The Sunrise Headlines

- US stock markets ended up to 0.25% higher with main indices putting another record closing high in place. Risk sentiment in Asia remains positive overnight with indices 0.25%-0.5% higher.

- Most Federal Reserve officials believed at their September meeting that they would likely raise short-term interest rates again this year, but some cautioned the decision would hinge on whether inflation picks up.

- Spanish PM Rajoy gave the Catalan government eight days to drop an independence bid, failing which he would suspend the Catalonia's political autonomy and rule the region directly.

- A longer extension of the ECB's bond-buying programme may be more beneficial during periods of calm, chief economist Praet said, just weeks before the bank decides whether to extend stimulus.

- The Italian government won two confidence votes on a fiercely contested electoral law that is likely to penalise the anti-establishment 5-Star Movement in next year's national election.

- President Trump plans to sign an executive order to start the unwinding of the Affordable Care Act, paving the way for changes to health-insurance regulations by allowing the sale of less-comprehensive agencies health plans to expand.

- Today's eco calendar contains US PPI data, weekly jobless claims and EMU industrial production data. Italy and the US sell bonds and plenty of central bankers are scheduled to speak.

Currencies: EUR/USD Extends Comeback

EUR/USD extends rebound

The developments on Catalonia dominated the news headlines, but had little impact on the markets outside Spain. EUR/USD extended its gradual rebound. This was mostly USD softness. The Fed Minutes confirmed that most Fed members envisage an additional rate hike this yea, but low inflation remains a source of internal debate. The dollar lost marginal further ground after the report. USD/JPY closed the session little changed at 112.50. EUR/USD finished at 1.1859 (from 1.1808).

New record closing levels on WS also support equity gains in Asia overnight. However, the equity rally has no impact on core yields. The dollar doesn't receive additional interest rate support. USD/JPY even trades marginally softer at 112.34. EUR/USD regained the previous 1.1823 range bottom and trades around 1.1875. The Spanish/Catalan crisis entered a period of ‘distress' as the Catalan leaders have five days to clarify whether they declared independence. For now the political uncertainty doesn't weigh on the euro.

Today, EMU industrial production is expected to have grown strongly in August. Risks are on the upside, but the report is outdated. In the US, the initial claims are expected to decline further (to 252K) following the pop-up due to the hurricanes. US Producer prices are expected to have increased by 0.4% M/M and 2.6% Y/Y in September, following a more modest 0.2% and 2.4% Y/Y in August. Core PPI inflation is expected unchanged at 2% Y/Y. Markets are sensitive to inflation data, but price action may be modest as the more important CPI inflation will be released tomorrow. Global markets will also keep an eye at the first earnings reports from the first major US Banks (JP Morgan and Citigroup).

After a cautious comeback, the dollar is again losing ground this week. No news is apparently bad news for the dollar. USD investors want concrete news on the tax reform, on the economy and on the Fed's rate intentions. The absence of progress on these issues causes some 'by-default' USD selling. A higher PPI might be slightly USD supportive, but it won't be a trigger for a U-turn. For that, we probably have to wait for tomorrow's US retail sales and/or CPI. There will still be plenty of headlines on Catalonia, but we don't expect negative impact on the euro. The next important steps will probably occur next week. We look for tentative signs of a USD bottoming out ahead of tomorrow's US data. Even so, this week's price action is disappointing for USD bulls

From a technical point of view, EUR/USD dropped below the 1.1823/ 1.2070 consolidation pattern last week. The USD rebound developed very slowly. The 1.1662 support came on the radar, but no real test occurred. Yesterday, the pair even returned above the 1.1823 previous range bottom, which is disappointing for EUR/USD bears, but we wait for tomorrow's US data to amend our EUR/USD sell-on-upticks bias. The USD/JPY momentum was constructive of late, but for an important part due to yen weakness. USD sentiment recently improved though. USD/JPY regained 110.67/95 (previous resistance), a short-term positive. The 114.49 correction top is the next important resistance. The rally lost momentum last week. So a break beyond 114.49 is difficult.

EUR/USD returned north of the 1.1823 previous range bottom

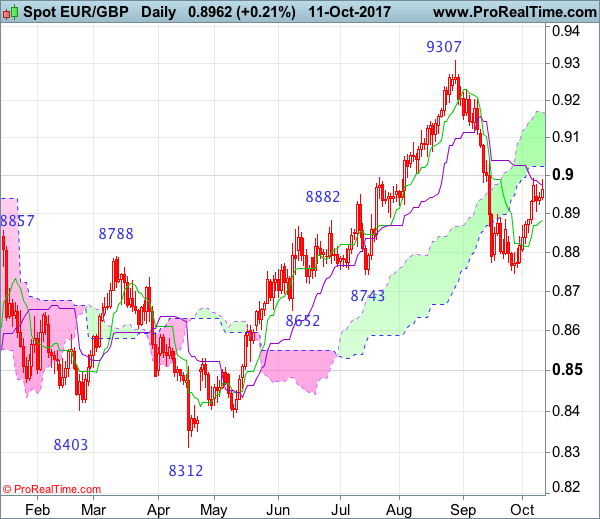

EUR/GBP

Sterling remains in consolidation modus

There were no important eco data in the UK yesterday. Sterling initially traded with a modest negative bias, especially against the euro. UK Chancellor of the Exchequer Hammond said he is considering to release more money to prepare for a ‘No deal Brexit' scenario if there aren't clear signs of progress by early 2018. There was no reaction of sterling to the Hammond comments. However, they illustrate that the clock is ticking against the UK and that UK companies desperately need progress and clarity on the Brexit process. EUR/GBP closed the session at 0.8970, nearing the recent correction top. Cable finally closed the session marginally higher at 1.322, but this was mostly due to USD weakness.

The RICS House price data were marginally stronger than expected this morning. There are no other important eco data in the UK today. BoE chief economist Haldane gives a speech in Washington late this evening. We don't expect him to bring high profile news on monetary policy. There's still no trigger for a clear directional move in EUR/GBP. The pair might continue to drift sideways in the 0.89 big figure, awaiting new eco or other news.

EUR/GBP staged a strong uptrend since April to set a top at 0.9307 late August. UK price data and hawkish BoE comments reinforced a sterling rebound. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of euro strength and sterling softness to persist. The prospect of (limited) withdrawal of BoE stimulus triggered a good sterling countermove, but this rebound has run its course. EUR/GBP supports at 0.8743 and 0.8652 are difficult to break. We look to buy EUR/GBP on dips. Last week's rebound above the 0.89 area improved the ST technical picture of EUR/GBP. EUR/GBP 0.9026 is the 50% retracement of the recent countermove

EUR/GBP rebound slows, but holds north of 0.89

Swedish Inflation Is In Focus Today

Market movers today

Swedish inflation is in focus today. We expect a new high in y/y terms (2.5% y/y for CPIF), though we expect the y/y rate to moderate in coming months. A relatively high print is probably expected at this point , and rates in the short end of Swedish curves have traded up in anticipation. In Norway, the budget for 2018 is revealed (see next page).

On the global front , the euro area is due to release industrial production for August . Following a st rong German print for August , we should expect a decent increase. If confirmed, it will point to another robust quarter for euro area growth.

In the US, PPI and initial jobless claims are due for release. The Fed's Brainard (vot er, dovish) and Powell (voter, neut ral) are due to speak today.

With respect to Brexit, the fifth negotiation round concludes today with a joint press conference. As the EU leaders at the EU summit later next week are likely to conclude there has not been ‘sufficient progress' to begin discussing the future relationship, more negotiations are needed in November and early December.

Selected market news

In our view, there was nothing new of great importance in the FOMC minutes, as we already know the different positions among the FOMC members . This also explains why markets did not react to the minutes. It remains our base case that the Fed will hike in December, as the core voting FOMC members put more weight on labour market data than current inflation data, although we agree with the dovish camp that low inflation may not be temporary due to low inflation expectations. Also, there was no news on what level the Fed targets for its balance sheet , as the Fed is likely to want to keep its flexibility, adjusting the target along the way. ‘Quant it ative tightening' is new to the Fed, so it is unlikely to see any benefits from precommitting. For more see FOMC minutes: Core members still want to hike in December, 11 October 2017.

Trump is set to meet with John Taylor (professor at Stanford University and the man behind the so-called " T aylor rule") lat er this week about the Fed chair, see Bloomberg, 11 October 2017. Taylor has indicated previously that he thinks the Fed funds rate is too low and that he wants a more rule-based approach to monetary policy. Trump has said previously that he will make an announcement on his nominat ion for Fed change in a couple of weeks.

President Trump has also said he will soon make an announcement on an Iranian deal. The US is pushing for condemning Iran but allies are pushing back and defending the nuclear deal, see Washington Post, 11 October 2017.

Yesterday in Spain, Prime Minister Mariano Rajoy gave Catalan leader Carles Puigdemont five days to clarify whether he has declared independence from Spain while threatening with article 155, which would suspend the authority of the Catalonian local government. Today is a national holiday in Spain and Rajoy is due to at tend a military parade in Madrid alongside King Felip VI.

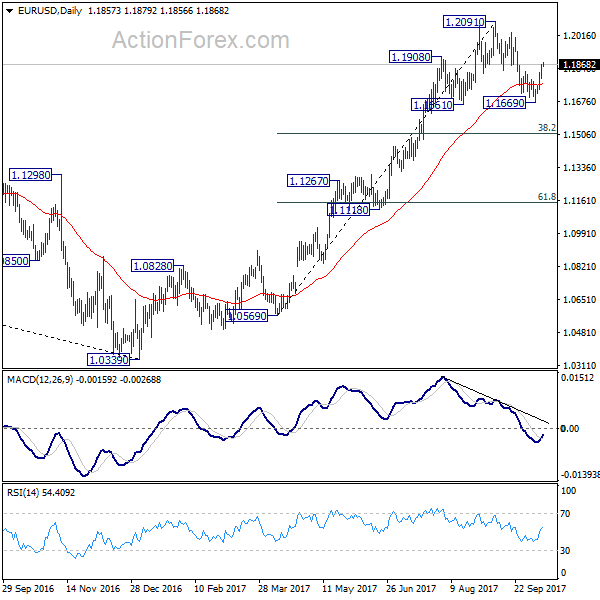

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1813; (P) 1.1841 (R1) 1.1888; More...

Intraday bias in EUR/USD remains on the upside for the moment. Pull back from 1.2091 should have completed at 1.1669, ahead of 1.1661 support. Further rise should be seen to retest 1.2091 high. We'll be cautious on strong resistance from there to bring another fall to extend the consolidation. On the downside, below 1.1794 minor support will turn bias back to the downside and could extend the correction from 1.2091 through 1.1669.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

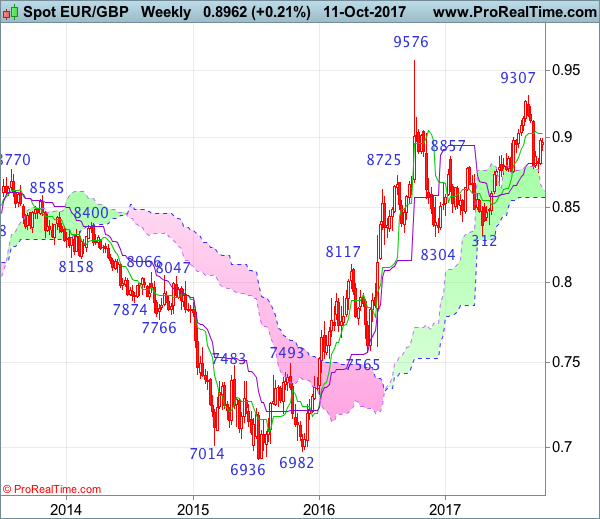

EUR/GBP Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: N/A

• Time of formation: N/A

• Trend bias: Near term up

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 29 Aug 2017

• Trend bias: Down

EURGBP – 0.8962

As the single currency found good support at 0.8746 late last month and has rebounded, suggesting the decline from 0.9307 has ended there and consolidation with mild upside bias is seen for retracement of this move to the lower Kumo (now at 0.9025), then 0.9045-50, however, reckon upside would be limited to 0.9110-15 and as top has been formed at 0.9307, reckon upside would be limited to 0.9150 and price should falter below 0.9203, bring another leg of corrective decline later this month.

On the downside, whilst pullback to 0.8900-10 cannot be ruled out, reckon the Tenkan-Sen (now at 0.8882) would limit downside and 0.8820-25 should hold and bring another rebound later. A daily close below 0.8020-25 would suggest the rebound from 0.8746 has ended and bring weakness to 0.8790-00, then towards this recent low later. Looking ahead, only break of 0.8746 would signal the fall from 0.9307 top has resumed and extend weakness towards 0.8690-95 (61.8% Fibonacci retracement of 0.8312-0.9307) but previous support at 0.8652 would hold.

Recommendation: Stand aside for this week.

On the weekly chart, despite falling marginally to 0.8746 (a doji star was formed), last week’s rebound formed a white candlestick, suggesting at least the first leg of decline from 0.9307 top has ended there, hence consolidation with mild upside bias is seen for gain to the Tenkan-Sen (now at 0.9027) and then 0.9050, however, if our view that top has been formed at 0.9307 is correct, upside would be limited to 0.9120-25 and price should falter well below 0.9203, bring another leg of decline later this month.

On the downside, expect pullback to be limited to 0.8900 and 0.8840-45 should hold, bring another rebound later. Only a drop below last week’s low at 0.8801 would suggest the rebound from 0.8746 has ended and bring retest of this level, break there would signal another leg of corrective decline from 0.9307 top is underway and bring retracement of early upmove to 0.8690-95 (61.8% Fibonacci retracement of 0.8312-0.9307) and possibly support at 0.8562, however, reckon downside would be limited to the lower Kumo (now at 0.8571) and previous resistance at 0.8531 should turn into support and contain euro’s downside.