Sample Category Title

DAX Edges Higher on Sharp German Mfg. PMI

The DAX index has started the week with slight gains. In the Monday session, DAX is trading at 12,863.25, up 0.27% on the day. On the release front, German Final Manufacturing PMI improved to 60.6, matching the forecast. In the Eurozone, Final Manufacturing PMI improved to 58.1, just shy of the estimate of 58.2 points. On Tuesday, the eurozone releases the Producer Price Index, which is expected to edge up to 0.1%.

There was drama and violence in the Spain on the weekend, as Catalonia, one of the richest regions in Spain held a referendum on independence. However, the vote was marked by street battles and widespread violence between voters and police. The national government banned the referendum, and police used tear gas and rubber bullets in against defiant voters, causing over 800 casualties. Catalonian officials claimed that 90 percent of voters had voted for independence. The Catalan regional government is holding an emergency meeting on Monday to discuss what steps it will take regarding independence, setting up the stage for a full-blown constitutional crisis with Madrid. Although, the drama in Spain is not expected to have a serious impact on the eurozone nervous investors reacted to the news on Monday by selling euros in favor of the dollar and Swiss franc.

The eurozone economy continues to hum in 2017, and the manufacturing sector has rebounded, thanks to a stronger global economy which continues to show strong demand for European products. German and Eurozone Final Manufacturing PMIs both improved in September, with the German indicator recording its strongest reading since April 2011. The labor market also has been improving. The eurozone unemployment rate remained at 9.1%, just below the estimate of 9.0%. Better economic conditions have led to louder calls for the ECB to tighten its monetary policy, particularly from Germany, where officials feel that that the robust economy needs tighter policy. However, the ECB must take into account those member countries that are lagging behind Germany, and ECB President Mario Draghi reiterated last week that the ECB had not made any plans to taper its asset purchase program. On Wednesday, Germany and the eurozone release Services PMIs, with both indicators expected to show expansion.

Euro’s Catalan Woes

Monday October 2: Five things the markets are talking about

The 'mighty' U.S dollar remains bid along with Treasury yields as investors contemplate the markets outlook for U.S tax cuts as well as the chances of a new, and potentially less 'dovish' Fed Chief.

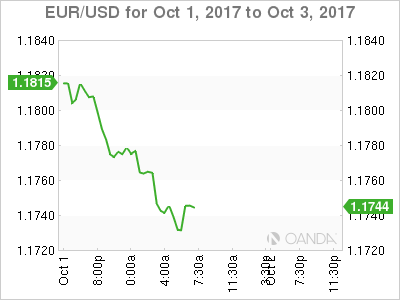

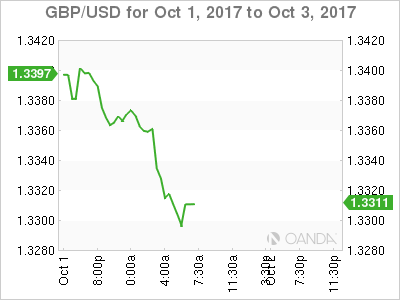

In currencies, the EUR (€1.1741) has retreated in the wake of a controversial vote for independence in the Spanish region of Catalonia. The region is now on track towards a declaration of independence – results showed that +90% of voters backed independence (with a turnout of +2.3M), while GBP (£1.3310) trades under pressure ahead of this week's U.K Conservative Party's annual conference where there could be challenges to PM Theresa May's leadership.

Elsewhere, this week, there will be a number of central bank policy announcements – the Reserve Bank of Australia (RBA), the Reserve Bank of India (RBI) and the European Central Bank (ECB).

No change is expected down-under, while slow growth in India and muted inflation would suggest a cut from the RBI, while forward guidance is looked for from the ECB regarding QE.

Manufacturing PMI's for September are due for most of the world's major economies – the U.S ISM measure comes this morning at 10:00 am ETD.

In North America, Canada and the U.S will round off this busy week with their respective employment reports on Friday.

1. Global stocks mixed results

Asian equity markets opened higher after stronger China PMI over the weekend and a cut by the People's Bank of China (PBoC) to their reserve requirement ratio (RRR).

Note: China (closed all week), Hong Kong, India and South Korean markets closed for holidays so liquidity remained light.

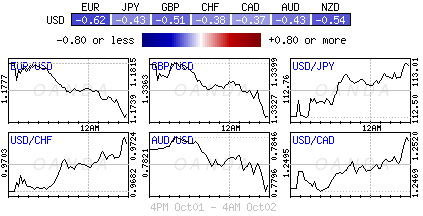

In Japan, the Nikkei rose to a 25-month high, +0.2%, as the yen (¥112.78) weakened outright following 'hawkish' rhetoric from the Fed. Ongoing N. Korea concerns continue to cap the index. The broader Topix index dropped -0.1%.

Down-under, Australia's S&P/ASX 200 Index gained +0.8%, with resources companies climbing on optimism China's growth slowdown will be modest.

In Europe, the Spanish Ibex trades lower after Catalan referendum. Catalonia says they are on track towards declaration of independence. The referendum has lead to a constitutional crisis in Spain and is beginning to spread jitters to peripheral markets.

U.S stocks are set to open in the 'black' (+0.1%).

Indices: Stoxx50 +0.2% at 3,591, FTSE +0.5% at 7,407, DAX +0.3% at 12,871, CAC-40 flat at 5,330, IBEX-35 -1.2% at 10,261, FTSE MIB -0.1% at 22,682, SMI +0.4% at 9,194, S&P 500 Futures +0.1%

2. Oil slips after Q3 rally, gold lower

Oil trades under pressure as an increase in U.S drilling and higher OPEC output has put the brakes on a rally that recorded its biggest Q3 gain in 13-years.

Last week, U.S energy companies' added oilrigs for the first week in seven, while Iraq announced its exports increased slightly in September.

Brent crude is down -12c at +$56.67 a barrel – it recorded a Q3 gain of around +20%, the biggest Q3 increase since 2004 and traded as high as $59.49 last week. U.S. crude (WTI) is down -17c at +$51.50. The benchmark posted its strongest quarterly gain since Q2 2016.

Note: Signs that a three-year supply glut is easing helped by a production cut deal by OPEC and non-OPEC members, have driven the 'Black gold's' rally.

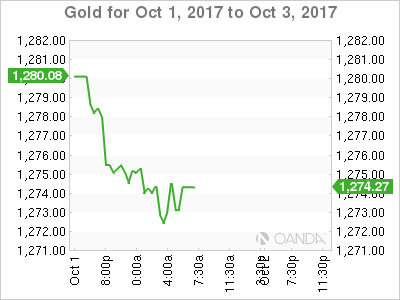

Overnight, gold slipped to its lowest in nearly two-months as the U.S dollar rallied and global equities gained, while growing expectations for a Fed interest rate hike in December also added to pressure. Spot gold is down -0.4% at +$1,273.60 an ounce.

3. U.S yields rally

Firming expectations that the Fed will hike rates in December coupled with domestic data pointing to steady growth in the U.S and talk of a potentially more hawkish successor to Fed Chair Janet Yellen is helping to push U.S yields higher.

Ten-year yields are trading atop of +2.37%; it's highest yield since mid-July, which has also pushed the dollar +0.5% higher against a basket of currencies.

Note: Speculation that President Trump could choose former Fed Governor Kevin Warsh, who is considered more 'hawkish' than Yellen, to replace her as head of the Fed.

Elsewhere, Germany's 10-year Bund yield gained +2 bps to +0.48%, the highest in two-months. In the U.K, 10-year Gilt yield has advanced +2 bps to +1.39%, the highest in eight-months.

Note: Spanish 10-year government bond yields rallied as much as +7 bps to +1.69%, taking the gap between them and German benchmarks close to its widest in nearly four-months.

3. EUR's Catalan Woes

The EUR (€1.1742) trades under pressure after the Spanish Catalan independence referendum, in which an overwhelming majority voted to separate from Spain.

Note: The ballots represented only about +40% of eligible voters in the region.

Expect the pound to be fuelled by political mongering. In Manchester U.K this week, the Conservative Party's annual conference is taking place and its expected to be awash with rumors of potential challenges to PM May's leadership. Also investors should expect some fierce arguments about the shape that Brexit should take.

5. U.K manufacturing PMI below forecasts

The purchasing managers' index on U.K. manufacturing activity falls to 55.9 in September, from 56.7 in August, below the consensus forecast for 56.4.

IHS Markit, which compiles the survey, said production and new orders rose at above long-run average rates, but cost inflationary pressures 'surged higher.”

'Although it looks as if the sector made solid progress through the Q3, the growth slowdown in September is a further sign that momentum is being lost across the broader U.K. economy,” said Rob Dobson, director at IHS Markit.

The U.K. economy has slowed markedly this year as inflation, which accelerated sharply after sterling's steep post-Brexit depreciation, began to outpace wages and squeeze the ever-important U.K consumer.

Busy US Data Weeks Kicks Off With PMIs

.

NFP Headlines Big Data Week

It promises to be another very busy week in the markets, with particular focus falling on the economic data, the most notable will come on Friday in the form of the US jobs report.

We'll also get a few notable releases on Monday, with the official and ISM manufacturing PMIs being released alongside construction spending figures. Federal Reserve policy maker and FOMC voter Robert Kaplan is also scheduled to appear today and is one of a number of officials due to speak this week.

Chaos as Catalans Vote For Independence

The illegal Catalonia independence referendum went broadly as expected over the weekend as voters turned out and clashed with Spanish police, who had been tasked with stopping the vote taking place. While hundreds of people were injured in the clashes, a large number of people managed to cast their vote and it's claimed that 90% of those that did voted for independence.

While the vote isn't legally binding, traders are clearly a little concerned about the impact that the vote, not to mention how the situation was handled by the Spanish authorities. The IBEX is the worst performing major index in Europe on Monday, down more than 1%, while the euro is also suffering in the aftermath of the vote, down more than half a percent against the dollar.

Sterling Slips After PMI as Conservative Party Conference Gets Underway

There's been a flurry of economic data releases already today, with manufacturing PMIs being released for countries throughout Europe. The data was broadly in line with expectations, with the Italian reading missing slightly and the Spanish coming in a little above. The UK manufacturing PMI slipped a little more than expected, dropping from 56.7 to 55.9, further weighing on the pound this morning.

Sterling is coming under a little pressure as the Conservative party conference gets underway in Manchester. Concerns about division within the party on both the Brexit strategy and Theresa May's position as leader continue to paint the picture of instability within the Conservatives, following what was a disastrous election campaign that saw them unnecessarily concede their majority. We're likely to hear plenty of murmurings over the coming days and there'll be particular focus on speeches from May and Boris Johnson who has repeatedly undermined her on Brexit and is clearly vying for her position.

Euro Starts Week Lower After Catalonian Chaos

The euro has lost ground in the Monday session. Currently, EUR/USD is trading at 1.1734, down 0.69% on the day. On the release front, German Final Manufacturing PMI improved to 60.6, matching the forecast. In the Eurozone, Final Manufacturing PMI improved to 58.1, just shy of the estimate of 58.2 points. In the US, the focus is also on manufacturing data, led by ISM Manufacturing PMI, which is expected to slow to 57.9 points.

The weekend referendum in Catalonia, one of the richest regions in Spain, descended into street battles and widespread violence between voters and police. The national government banned the referendum, and police used tear gas and rubber bullets in against defiant voters, causing hundreds of casualties. Catalonian officials claimed that 90 percent of voters had voted for independence, setting up a constitutional crisis with Madrid. Although, the drama in Spain is not expected to have a serious impact on the eurozone nervous investors reacted to the news on Monday by selling their euros in favor of the dollar and Swiss franc.

The eurozone economy continues to hum in 2017, and the manufacturing sector has rebounded, thanks to a stronger global economy which continues to show strong demand for European products. German and Eurozone Final Manufacturing PMIs both improved in September, with the German indicator recording its strongest reading since April 2011. The labor market also has been improving. The eurozone unemployment rate remained at 9.1%, just below the estimate of 9.0%. Better economic conditions have led to louder calls for the ECB to tighten its monetary policy, particularly from Germany, where officials feel that that the robust economy needs tighter policy. However, the ECB must take into account those member countries that are lagging behind Germany, and ECB President Mario Draghi reiterated last week that the ECB had not made any plans to taper its asset purchase program.

The US dollar gained some ground last week from an unexpected source – President Donald Trump. Trump has all but given up on his health care proposal, as the plan lacks enough support from Republican lawmakers. Next on the Trump Express is tax reform, which was a key campaign plank. Last week, Trump proposed a major overhaul of the US tax code, which includes reducing the corporate tax rate from 35 percent to 20 percent, as well as a 25 percent tax rate for small businesses, such as partnerships. Like other Trump proposals, the tax plan was sketchy on details, including how the tax plan would be paid for. With Democrats and some Republicans wary of Trump’s tax agenda, it’s likely his that tax reform proposal will face a stiff battle in Congress. Still, the markets like the idea of lower taxes, and the US dollar posted back-to-back weekly gains.

Technical Outlook: Brent OIl : Extended Bears Crack Important Support At $56.00

Brent Oil extends pullback from last week and remains in steep descend for the fifth straight day. Fresh bearish extension on Monday cracked important support at $56.00 (Fibo 38.2% of $50.47/$59.48 upleg).

Rising 20SMA (currently at $55.72) is reinforcing support zone, where bears may take a breather on oversold slow stochastic.

However, south-heading daily RSI shows a plenty of room at the downside and signals further easing on firm break below $56.00/$55.72 triggers, which would expose support at $54.97 (daily Kijun-sen / 50% retracement.

Initial resistance lies at $56.74 (session high) and extended upticks should remain below broken daily Tenkan-sen at $57.36.

Res: 56.74, 57.00, 57.36, 57.72

Sup: 55.98, 55.72, 55.25, 54.97

CRUDE OIL Holding Above $50

Crude oil is consolidating above the $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance found at 52.43 (26/09/2017) has been broken. Expected to show another leg higher.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Breaking Support At 16.58

Silver has reversed and has broken uptrend channel by breaking support implied by its lower bound. Strong resistance is given at 18.65 (17/04/2017 high) while support found at 16.58 (15/08/2017 high) has been broken. Expected to show further bearish move.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

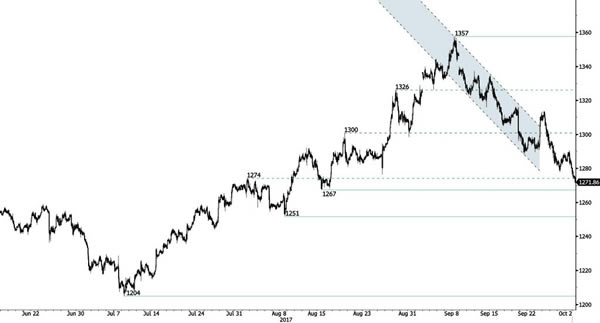

GOLD Continued Decline

Gold continues to go down. Hourly support is given at 1267 (15/08/2017 low). Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show further bearish move.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Bullish Breakout

Bitcoin has strongly increased over the weekend. Strong support is given at 2975 (22/08/2017 low). Sell walls around $4000 have been broken. Key resistance can be located at 4921 (01/09/2017 high). The road is wide open for further increase.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Breaking Uptrend Channel

EUR/CHF is breaking within uptrend channel. Yet, we need more downside pressures. Strong resistance is now given at 1.1623 (22/09/2017 high). Expected to show further short-term weakness.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).