Sample Category Title

Summary 9/25 – 9/29

Monday, Sep 25, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Sep 26, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Sep 27, 2017

[php_everywhere] [/php_everywhere]

Thursday, Sep 28, 2017

[php_everywhere] [/php_everywhere]

Friday, Sep 29, 2017

[php_everywhere] [/php_everywhere].

The Weekly Bottom Line: We’ve Got To Admit Its Getting Better

U.S. Highlights

- Finally, midway through 2017 global growth is looking better than it was a few months ago. Our latest Global Outlook discusses how the optimism that has been missing for several years has finally returned.

- With stronger global growth comes tighter monetary policy. This week the Fed formally took the next step of starting to reduce the size of its balance sheet.

- The Fed also reaffirmed that it expects to hike rates again this year. Our U.S. Outlook looks solid over the next two years, despite the hit from the devastating hurricanes. Reduced economic slack should lead to higher inflation, consistent with a gradual pace of rate hikes over the next two years.

Canadian Highlights

- The data flow this week remained broadly consistent with our updated view that the Canadian economy is likely to maintain above-trend growth in the third quarter.

- On balance, wholesale activity for July provided some upside risk to our outlook for third quarter growth, while retail and manufacturing sales volumes were less supportive. On the price side, headline and underlying measures of inflation rose slightly in August, suggesting that prices may have finally stabilized after a soft spell.

- Overall, we anticipate that the persistence of above-trend economic growth will likely motivate the Bank of Canada to push up rates by another 25 bps before the end of the year.

U.S. - We've Got To Admit Its Getting Better

In recent years, economic growth forecasts have suffered from serial disappointment. Economic outlooks have typically been downgraded part way through the year, but not so this time. Our latest Global Outlook discusses how a broadening and strengthening of expansions in advanced and emerging economies has helped restore a sense of optimism in the global economy that has been missing for several years.

Global growth is on track to average 3.5% this year, and over the next two years. Highly accommodative monetary policy has done its job in sowing the seeds for self-sustaining economic growth across a number of regions. Now, with economic slack being absorbed at a faster clip, central banks are increasingly scaling back that stimulus. In the Euro Area, real GDP growth of 2.4% in the first half of the year was faster than expected, and nearly double the economy's estimate of trend growth. As a result, the European Central Bank looks set to announce an end to its asset purchases at its upcoming meeting in October.

The Federal Reserve is further along in reducing monetary stimulus, with four rate hikes under its belt. This week it formally announced that it will start reducing the size of its $4.4 trillion balance sheet in October. The pace will be very gradual, with the monthly runoff amounting to 0.2% of its balance sheet. The process was already laid out clearly in June, and as such there was little reaction in the longer end of the curve.

Markets paid greater attention to the Fed's message on future rate hikes, and how that may have changed given the softness in inflation this year. Yellen acknowledged that not all of the weakness in inflation can be chalked up to transitory factors (as we discussed in our latest forecast). However, interest rate projections for the near-term were left unchanged. The median expectation of Fed members is for one more hike this year and three hikes in 2018. Confirmation that the Fed hasn't lost its faith in the Phillips curve did produce an upward move in shorter-term yields. And, the odds on a rate hike in December have shifted from a coin flip to being roughly two-thirds priced in.

The Committee also indicated that recent hurricanes are likely to impact inflation and economic activity in the near term, disrupting it first and then boosting it thereafter as rebuilding begins. However, the storms are "unlikely to materially alter the course of the national economy over the medium term." As such, we expect the Fed to see through any of the volatility in the data over the coming months, with the storms unlikely to prevent the Fed from potentially raising rates at their December meeting – particularly if inflation data firms as we expect.

Overall, the U.S. economy is expected to continue its "Steady-Eddie" performance of slightly better than 2% growth over the next few years. Upside and downside risks to this outlook remain: either from a fiscal boost from Washington or from delayed capital spending due to policy uncertainty on taxes or NAFTA renegotiation.

Canada - A Little More Sizzle Before the Fizzle

The data flow this week remained broadly consistent with our view that the Canadian economy is set to expand at a robust, above-trend pace in the third quarter.

Consumer spending thus far has been very robust, supported by past gains in wealth and job growth. Retail sales have performed particularly well, with volumes rising every month this year through June. Given this hot streak it should come as no surprise that consumers took a break in July. This morning's retail data showed improvement in sales driven by higher prices, as volumes fell 0.2% on a month-on-month basis. Overall, the data is broadly consistent with our view that Canadian households are likely to scale back spending in the second half of the year as higher interest rates start to bite and housing activity moderates.

Other activity data this week were mixed, but the upside risk to growth from wholesale trade edges out any downside from manufacturing sales. On the latter, manufacturing sales for July were disappointing as volumes fell 1.4% and growth in prior months was revised down. However, some of the weakness in the month may be due to an unusually long retooling-related shutdown of vehicle assembly plants in the month, suggesting a possible rebound in August as plants come back on line. But, with forward-looking indicators down in the month, it looks as if the Canadian manufacturing sector could cool a bit in the third quarter.

More positively, Canadian wholesalers recorded a 2.1% jump in volumes in July, the largest monthly increase yet this year. Strong sales by building material and supplies distributors, machinery and equipment suppliers, and clothing distributors helped drive the advance. Overall, this uptick in wholesale activity presents a material upside risk to our 2.3% tracking of third quarter GDP growth (Chart 1).

All told, the Canadian economy is on pace to expand at an above-trend pace of about 2.5% in the third quarter. This remains broadly consistent with our updated outlook published mid-week, which anticipates a slowdown in activity in the second half after the sizzling pace.

On the price side of things, CPI data for August remained broadly supportive of our outlook (Chart 2). Headline and underlying inflation measures all ticked up in the month, providing some justification for the two 25 bp rate hikes in the span of six weeks by the Bank of Canada. Looking ahead, the rapid appreciation of the loonie is likely to shave about 0.3 percentage points off of quarterly price growth by the start of next year. However, the Bank of Canada is likely to look through this weakness, deeming it as largely another temporary factor acting to keep price pressures subdued. Instead, as highlighted in Deputy Governor Tim Lane's speech this week, the Bank will remain focused on how the Canadian economy adapts to higher interest rates and a higher dollar. Overall, we anticipate that the persistence of above-trend economic growth will likely motivate the Bank of Canada to push up rates by another 25 bps before the end of the year.

U.S.: Upcoming Key Economic Releases

U.S. Personal Income & Spending - August

Release Date: September 29, 2017

Previous Result: Income 0.4% m/m, Spending 0.3% m/m

TD Forecast: Income 0.2% m/m, Spending 0.1% m/m

Consensus: 0.2% m/m, Spending 0.1% m/m

Headline PCE inflation is expected to firm to 1.5% in August, reflecting a 0.3% rise in prices on the month. Driving the August pickup are energy prices, led by higher gasoline prices amid the Hurricane Harvey disruption. In line with the CPI report, we expect the core (ex food & energy) index to post a 0.2% m/m increase, its first since February. Unrounded, however, the monthly gain should be more modest than its CPI counterpart due to different weightings for housing and medical care in particular. As a result, we expect core PCE inflation to be unchanged at 1.4% y/y. However, this should mark the bottom of the cycle, barring disappointment in future readings. Overall, the return to a healthier 0.2% m/m rise in the core PCE should comfort the Fed's inflation outlook in offering an early sign that transitory effects are fading and underlying strength is building.

Nominal PCE (personal spending) is expected to rise 0.1% in August, relatively weak again reflecting the Harvey impact that dented motor vehicle sales in particular. The gain would be consistent with Q3 real PCE tracking just below a 2.0% pace, a downgrade from our earlier estimates primarily due to the hurricane impacts. With the impacts expected to unwind by Q4, the Fed will look through this as a one-off shock. We also expect a 0.2% increase in August personal income, based on the weaker than expected 0.1% rise in average hourly earnings.

Canada: Upcoming Key Economic Releases

Canadian Real GDP - July

Release Date: September 29, 2017

Previous Result: 0.3% m/m

TD Forecast: 0.1% m/m

Consensus: N/A

A sizeable drag from the manufacturing industry will constrain GDP growth to 0.1% m/m in July. Real manufacturing sales fell due to extended shutdowns at Canadian auto plants, but the transitory nature implies a rebound in August. Outside of auto production, the performance of the goods sector should be relatively mixed. Energy output could see further gains due to increased production at the Syncrude upgrader facility, which had been operating at a reduced capacity following an explosion earlier this year, but we see downside risks to residential construction. Services should be fairly mixed as the ongoing slowdown in housing and a modest decline in real retail sales will offset a surge in wholesale sales. Our forecast for a 0.1% gain in July is consistent with Q2 growth in the mid-2% range, which is still above estimates from the July MPR even though it represents a significant slowdown from Q2.

Weekly Market Outlook: Inflation Key To EURUSD

- Inflation Key To EURUSD - Peter Rosenstreich

- Investors To Focus On ECB Amid Boring FOMC - Arnaud Masset

- Bank Of Japan Still On The Accommodative Side - Yann Quelenn

- Online Gaming

FX Market - Inflation Key To EURUSD

EU inflation data will be critical for the near-term EURUSD direction. Last week the Fed took another significant step towards policy normalization by announcing the start of balance sheet reduction in October. In addition, despite lacking a upwards trend in inflation data Fed members indicated that a December hike, then three more 25bp increase in 2018 was the base senario. The net result was a marginal and short lived USD rally. For EURUSD traders the Fed played their hand, so the next move will be the ECBs.

Strong improvement in EU growth outlook, led by domestic consumption, and improving backdrop for inflation has encouraged ECB policy makers to suggest the removal of emergence measures. However, further evidence that inflation trajectory will continue would provide the basic justification for a reduction in asset purchases. The most recent print of August core inflation was 1.2% y/y, above expectations. Yet the rise has not been broad-based, depending primary on the tourism trade in southern nations. Spillover from the summer holiday season into September is not expected while the strong Euro probably damped demand for industrial goods. We anticipate that September core inflation will stall at 1.2% y/y (1.2% y/y exp). However, consumer spending, supported by the strong gain in labour markets, is expected to drive the September headline read to 1.6% y/y from 1.5% (1.5% y/y exp).

The initial reaction to an unchanged core inflation read will likely be disappointment with traders unwinding speculative Euro longs. However, the sentiment around the EU is positive, supported by Merkel winning a historic 4th term as German chancellor and UK "Brexit Bill" concessions. In addition, on a technicality, the ECB will have to reduce its bond purchased in 2018 since they are restricted to hold no more than 33% of nations sovereign debt (German debt will be first to hit that threshold). In the US, traders are sceptical of the Fed optimistic forecast, while in the EU, traders have accepted that the next move for Draghi will be tighter policy. We view any dip in EURUSD as an opportunity to reload EURUSD longs.

Economics - Investors To Focus On ECB Amid Boring FOMC

As widely expected, the FOMC triggered the process to reduce the size of its $4.5tn balance sheet. Although the normalization process will start in October, which could be seen as a bit rushed, the pace of disinvestment will be very slow and has already been well telegraphed as described in the Addendum to the Policy Normalization Principles and Plans released in June.

As a first step, the Federal Reserve will reinvest principal payments it receives from maturing Treasury securities only if it exceed $6 billion per month, then this "cap" will be increased by $6bn every three months until it reaches $30bn a month. Regarding principal payments from agency debt and mortgage-backed securities, the process is the same except that the initial "cap" is set at $4bn a month, while the "cap" will increase by $4bn every three month until it reaches $20bn a month.

The reaction of investors was quite mixed as the US dollar was unable to maintain its gains and returned slowly towards its pre-FOMC meeting levels. Initially, high quality commodity currencies such as the CAD, NZD and AUD experienced a more acute sell-off, mostly due to the substantial proportion of long speculative position in those currencies against the USD. However, by Friday afternoon, even the Japanese yen retraced against the greenback with USD/JPY easing towards 112.

It must be noted that all in all, it wasn't a hawkish meeting with both the statement and Yellen's speech being cautious, especially about the inflation forecast. Speaking of which, the Fed revised downwardly its inflation forecast. Now, FOMC members don't expect core inflation to reach the 2% target percent until 2019. However, the growth forecast was moderately revised to the upside as the real GDP growth forecast has been lifted to 2.4% for 2017 compared to 2.2% previously. Finally, Fed officials cut the forecast for the official rate down to 2.8% in the long-term from 3%, suggesting a stabilisation of the economy.

Considering the market's reaction, with both the greenback and US treasury yields reversing quickly Thursday's gains, it appears that investors are not too quick to believe the Fed will increase interest rate according to the announced pace. In addition, according to the Fed Funds Futures, the probability that the Fed raises rates in December barely reached 63% on Friday. Therefore, there is no rush to take long USD position, especially knowing that the ECB is on the cusp to scale down significantly it quantitative easing programme.

Economics - Bank Of Japan Still On The Accommodative Side

Last Thursday night, the Bank of Japan has announced after an 8-1 vote that its benchmark interest rate will remain on hold at -0.1%. It is certain that the Bank of Japan was also closely looking towards the Fed which had its meeting few hours earlier. Indeed, the US central bank has announced a reduction of its balance sheet which is providing some relief to the USDJP which has surged above 112 and is now consolidating around this level.

The BoJ stands ready to continue its all-in monetary policy by buying assets at around yen 80 trillion a year in order to maintain the 10-year Japanese Government Bonds at its 0% target. This can definitely not end well. We recall that the Japanese debt-to-GDP ratio is above 230% and deflation threat is still very important. On top of that some BoJ members believe that the inflation target of 2% is too high for the current monetary policy which is, in definite, not loose enough. This is something that we need to underline, in particular since the Bank of Japan has recently postponed its deadline for reaching the inflation target for six consecutive times.

It is nonetheless important to note that the overall economic fundamentals are improving with Japan recording a positive growth period of around a decade. Q2 GDP came at 0.6% q/q. A strengthening domestic demand and the recent boost in Japanese exports are the main reasons for this continuous period of growth.

Globally, markets are pricing in the end of the US Quantitative Easing, at least further tightening. The big unknown is how will react the global bond markets as higher yields would likely trigger a sell-off which can be massive as free money kept flowing into this market during the last decade. Against the backdrop of the US balance sheet reduction, we consider that the USDJPY is set to appreciate towards 114 within the short-term.

Themes Trading - Online Gaming

Much ground has been covered since the first video game consoles of the early 1970s, which offered only 2D games in black and white with no sound. Since then, the video games industry has grown exponentially as computer technology has advanced. Nowadays, blockbuster video games enjoy massive budgets, easily surpassing those of Hollywood movies: budgets in excess of $100 million are not uncommon. According to ESAF (the Entertainment Software Association Foundation), over the last five years total consumer spending on the video games industry in the US grew by an average of $1.38 billion a year to reach $30.4 billion in 2016. Video game content accounts for more than 80% of this amount, putting video game makers in a strong position to take advantage of this trend. Moreover, the fastest growth is in social network gaming, mobile apps and online gaming, which together account for over 65% of total revenue.

The video games industry is evolving faster than any other, constantly adapting to the latest technological breakthrough. The industry has already embarked on its latest transformation. However, it is not too late to be part of it. We built this theme with the aim of offering exposure to the entire video games market, from traditional physical media distribution and console builders to new market entrants. We have overweighted the fastest-growing part of the industry: companies active in "Online Gaming" certificate is now trading live: https://www.swissquote.ch/url/investment-ideas/themes-trading

Week Ahead Geopolitics Dampen Dollar Rally

North Korea, Brexit and German elections distract from Hawkish Fed

The US dollar is higher against major pairs at the end of trading on September 22. The NZD and the EUR are the main exceptions with elections in the next 48 hours in both regions. Parliamentary elections will begin in New Zealand on Friday, September 22. The ruling party is making a comeback in the polls and has given the Kiwi a boost, but the Labour party could still come up with a shock upset. German elections appear to be a more predictable affair with Angela Merkel's party the likely to come up on top, but with the rise of the far-right and the need for a partner for a grand coalition the number of seats of other parties will be of utmost importance.

Japanese Prime Minister Shinzo Abe is expected to call a snap election next week. Rising support as the result of the situation in North Korea has emboldened Abe to call for elections in October. The move is intended to weaken opponents, but like in the United Kingdom the move is a gamble that can backfire with a new national party offering the biggest threat. His major objective seems to be achieving a majority with the aim of reforming the constitution.

Economic data release will play a part during the week of September 24 to 29 but since no major release will be published it will be a minor role. In the United States The Consumer Board will release its Consumer confidence index on Tuesday, September 26 at 10:00 am EDT. US durable goods and Crude oil inventories will be published on Wednesday, September 27. The Final GDP estimate will be released on Thursday, September 28 at 8:30 am EDT with a forecasted 3.1 percent.

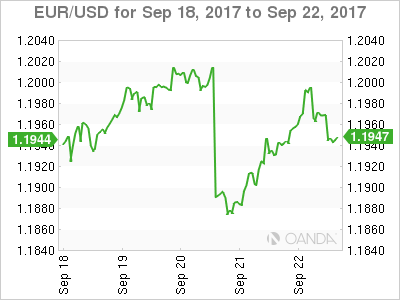

The EUR/USD gained 0.057 on in the last five days. The single pair is trading at 1.1945 after strong purchasing managers index in Europe beat expectations managing to stop the US dollar that the Fed economic projections had sparked in the middle of the week. The pair also got a boost from rumours that the United Kingdom would seek a softer Brexit alternative, although there was not a clear mention of that during Theresa May's speech on Friday. A softer Brexit scenario and the German elections expected to bring little in the way of surprise brought the single currency slightly higher to end the week.

Germany is expected to reelect Angela Merkel's party the Christian Democratic Union (CDU) during the Sunday, September 24 election. The main question still unanswered is who will make up the coalition needed to form a government. The Social Democratic Party (SPD) is anticipated to come in second, but is said to want to avoid a repeat of the current grand coalition. Germany has not proven immune to the rise of populism with the rise of the Alternative for Germany (AfD), the far-right party is expected to grab as much as 10 percent of the vote. The party formed in 2013 has gained support by preaching an anti-immigrant message and is could end up being the third largest party and in some scenarios could be the opposition to Merkel's CDU led grand coalition. Exit polls will be quick to announce the results, but the coalition forming process could last weeks but knowing the allocation of the votes will be instrumental in adding stability to the market.

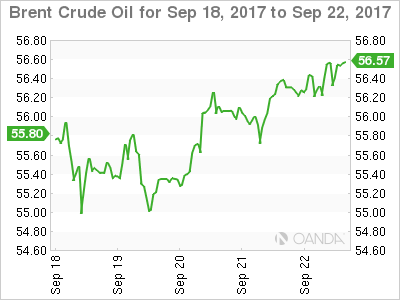

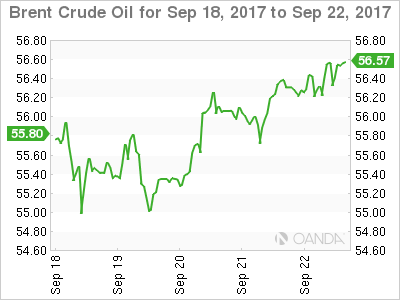

Oil rose 1.76 percent this week. The price of Brent is trading at $56.54 very near weekly highs. Oil prices ended the week with gains after the Organization of the Petroleum Exporting Countries (OPEC) and other major producers met in Vienna to discuss the current production cut agreement. While no big decision was announced OPEC members had been supportive of extending the deal beyond the March 2018 end. Russia's Energy Minister was more pragmatic and offered no clues other than its too early to discuss a decision. With US production disrupted by tropical storms and the OPEC and other producers reducing their output oil prices have risen.

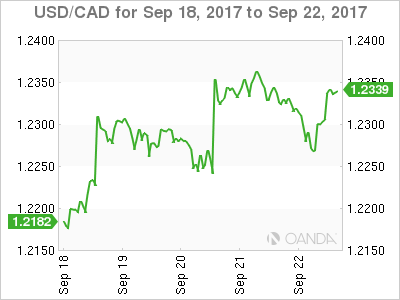

The USD/CAD gained 1.204 percent this week. The currency pair is trading at 1.2344 after Canadian data put a stop to the loonie rally. Canadian inflation underperformed in July rising by only 1.4 percent and retail sales rose by 0.4 percent but a decline in the volume of goods sold is a cause for content. The Canadian dollar appreciated versus the US dollar in early September when the Bank of Canada (BoC) hiked rates earlier than expected. The Canadian benchmark is now 1.00 percent, the same level as back in 2015 before current BoC governor made two pro-active rate cuts ahead of a forecasted fall in oil prices.

The market was originally expecting a rate hike in October, and with the September rate move and mixed data the probabilities are down to 38 percent. What is keeping the odds high is the fact that the Canadian economy surprised with a 4.5 percent annual growth in the second quarter. The US dollar got some support from the Fed on Wednesday when the central bank as anticipated announced the beginning of its balance sheet reduction plans. The hawkish economic projections published at the same time put downward pressure on the loonie as the interest rate divergence will could still favour the US dollar with a December rate hike above 70 percent probability.

Gold lost 2.01 percent in the last five days. The precious metal is trading at $1,295.11 after touching highs of $1,322.02 earlier in the week. Gold managed to score a daily gain on Friday, but could not reverse the downward trend triggered by the U.S. Federal Reserve economic projections showing another rate hike still on the table for this year. The Fed has hiked twice already with the Fed funds rate sitting at a 100 to 125 basis points range. The FedWatch tool developed by the CME shows a 71.4 percent probability of a rate hike at the end of the Fed's December meeting.

North Korean tension has kept Gold bid as a war or worlds could trigger a real armed response. The move in the yellow metal this week shows the market is more focused on rates than geopolitics, but as always that could be subject to change if there is an escalation in hostilities.

Market events to watch this week:

Sunday, September 24

- All Day EUR German Federal Elections

Tuesday, September 26

- 10:00am USD CB Consumer Confidence

Wednesday, September 27

- 8:30am USD Core Durable Goods Orders m/m

- 10:30am USD Crude Oil Inventories

- 4:00pm NZD Official Cash Rate

- 4:00pm NZD RBNZ Rate Statement

Thursday, September 28

- 8:30am USD Final GDP q/q

- 8:30am USD Unemployment Claims

Friday, September 29

- 4:30am GBP Current Account

- 8:30am CAD GDP m/m

*All times EDT

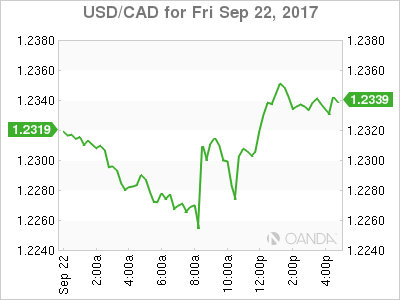

Canadian Dollar Flat Ahead of Geopolitical Weekend Risk

The Canadian dollar was flat on Friday as the US dollar rally triggered by the hawkish economic projections published on Wednesday by the Fed were offset by rising risk concerns about North Korea. Canadian data was mixed on Friday putting in question a third rate hike in 2017.

Canadian inflation underperformed in July rising by only 1.4 percent and retail sales rose by 0.4 percent but a decline in the volume of goods sold is a cause for content. The Canadian dollar appreciated versus the US dollar in early September when the Bank of Canada (BoC) hiked rates earlier than expected. The Canadian benchmark is now 1.00 percent, the same level as back in 2015 before current BoC governor made two pro-active rate cuts ahead of a forecasted fall in oil prices.

The market was originally expecting a rate hike in October, and with the September rate move and mixed data the probabilities are down to 38 percent. What is keeping the odds high is the fact that the Canadian economy surprised with a 4.5 percent annual growth in the second quarter. The US dollar got some support from the Fed on Wednesday when the central bank as anticipated announced the beginning of its balance sheet reduction plans. The hawkish economic projections published at the same time put downward pressure on the loonie as the interest rate divergence will could still favour the US dollar with a December rate hike above 70 percent probability.

Oil rose 1.76 percent this week. The price of Brent is trading at $56.54 very near weekly highs. Oil prices ended the week with gains after the Organization of the Petroleum Exporting Countries (OPEC) and other major producers met in Vienna to discuss the current production cut agreement. While no big decision was announced OPEC members had been supportive of extending the deal beyond the March 2018 end. Russia's Energy Minister was more pragmatic and offered no clues other than its too early to discuss a decision. With US production disrupted by tropical storms and the OPEC and other producers reducing their output oil prices have risen.

Gold lost 2.01 percent in the last five days. The precious metal is trading at $1,295.11 after touching highs of $1,322.02 earlier in the week. Gold managed to score a daily gain on Friday, but could not reverse the downward trend triggered by the U.S. Federal Reserve economic projections showing another rate hike still on the table for this year. The Fed has hiked twice already with the Fed funds rate sitting at a 100 to 125 basis points range. The FedWatch tool developed by the CME shows a 71.4 percent probability of a rate hike at the end of the Fed's December meeting.

North Korean tension has kept Gold bid as a war or worlds could trigger a real armed response. The move in the yellow metal this week shows the market is more focused on rates than geopolitics, but as always that could be subject to change if there is an escalation in hostilities.

Market events to watch this week:

Sunday, September 24

- All Day EUR German Federal Elections

Tuesday, September 26

- 10:00am USD CB Consumer Confidence

Wednesday, September 27

- 8:30am USD Core Durable Goods Orders m/m

- 10:30am USD Crude Oil Inventories

- 4:00pm NZD Official Cash Rate

- 4:00pm NZD RBNZ Rate Statement

Thursday, September 28

- 8:30am USD Final GDP q/q

- 8:30am USD Unemployment Claims

Friday, September 29

- 4:30am GBP Current Account

- 8:30am CAD GDP m/m

*All times EDT

Weekly Market Outlook: Elections in Germany & New Zealand, RBNZ Meeting, Key Data in Focus

Next week's market movers

- In Germany, voters will elect their new Chancellor. On the vote, we see the case for a relief bounce in European assets if Merkel is the winner as anticipated, though any major reaction may only occur towards the end of October, when the coalition-making process begins.

- New Zealand will hold its General Election as well. A victory by the incumbent National Party could support the Kiwi, whereas a potential Labor win could weigh on the currency, we think.

- The RBNZ is expected to stand pat. We don't expect any major change in language, given the lack of developments since the latest meeting.

- We also get key economic data from Germany, the Eurozone, Japan, and the US.

Important events start earlier next week, as on Saturday, New Zealand will hold its General election. Most opinion polls suggest a very tight race between the incumbent National Party and the Labor party. Judging from how the Kiwi has reacted to opinion polls so far, a victory by the National Party would probably prove beneficial for the currency, whereas a potential win for the Labor Party could weigh on NZD. We believe this is the case mainly to the different stances these two main parties hold on trade policy. The Nationals largely represent the status quo and advocate continued free trade. On the other hand, Labor officials have noted in the past that they are open to renegotiating trade deals such as the Trans-Pacific Partnership (TPP). Considering how heavily reliant New Zealand is on international trade, such a renegotiation could potentially hurt exporting firms and thereby, slow down the economy.

Subsequently on Sunday, Germany will hold its own Federal Election. Unlike the bloc's recent elections in the Netherlands and France, this battle appears to be more traditional in nature, with the two main parties holding very similar views on key issues. According to almost every opinion poll, another victory by incumbent Chancellor Merkel is perceived as certain. As such, we believe that the market reaction on the actual vote may be relatively limited, with risks tilted towards a small relief bounce in the euro and European stocks in case Merkel wins as expected.

We believe that any major market reaction in the aforementioned asset classes may result from who Merkel chooses to align herself with, something that will become clearer towards the end of October. The political alliance she forms could determine whether much-needed EU reforms will materialize, such as the creation of a position for an EU Finance Minister, a shared euro-budget, and further banking sector integration. All of these would likely be seen as steps towards the creation of a fiscal union in Europe that would accommodate the monetary one. In our view, any signs that such positive reforms may be looming could lead investors to fundamentally re-evaluate European assets, and by extension, the euro itself.

Turning back to Germany, a continuation of the "Grand coalition" between Merkel's CDU with the SPD, Germany's second largest party, is likely to be the most market-friendly outcome, considering the SPD's pro-EU stance. This could spell further good news for the common currency, and quite possibly for major European equity indices. On the other hand, a coalition that does not include the SPD, but for example includes the FDP that is against the aforementioned EU reforms, could be perceived as a negative for European markets and the euro, we think.

On Monday and Tuesday, we have no major events or indicators on the economic agenda. Market participants may still be digesting the outcomes of the aforementioned elections.

On Wednesday, during the early Asian morning, the RBNZ will announce its policy decision. At its latest gathering, the Bank acknowledged that CPI inflation softened in Q2, but noted that it is still within the target range. Importantly, officials kept the timing of their first planned rate hike unchanged for Q1 2020, while they expressed discomfort about the up-until- then strength of the Kiwi. On top of that, in the aftermath of the decision, Governor Wheeler said that the option of FX intervention is always open. Since that gathering, we did not get much in terms of economic developments. The only point worth mentioning is that the Bank's 2-year inflation expectations for Q3 slid somewhat. This combined with the fact that the Kiwi is trading more or less at the same levels it was trading back then make us believe that the Bank is likely to remain on hold once again and make very few changes to its language.

As for the Bank's first rate increase, according to New Zealand's OIS, the market continues to anticipate that to happen in Q3 2018, much earlier than the Bank's own forecasts. Another round of concerns over the exchange rate, especially more intervention warnings, could convince the market to push back its hike expectations. Having said all these, the gathering is scheduled just a few days after the nation's elections. Given that the forthcoming direction of the Kiwi may be primarily determined by the election outcome, we think the Bank's gathering may attract less attention than otherwise.

Turning to the economic indicators, in the US, durable goods orders for August are coming out. The consensus is for the headline orders to have rebounded after falling sharply in July, while the core rate is forecast to have declined. The core forecast is supported by the nation's ISM manufacturing PMI for the month, where the New Orders sub-index ticked down. The strong rebound in US civilian aircraft orders, on the other hand, supports the case for a rise in the headline rate. On balance, the market may place more emphasis on a potential decline in the core rate.

On Thursday, Germany's preliminary CPI for September is due out, one day ahead of Eurozone's print. The forecast is for the CPI rate to have ticked up, and to be exactly in line with the ECB's mandate of below, but close to 2%. The forecast is supported by the nation's preliminary Markit composite PMI for the month, which showed another strong rise in prices charged for goods and services. An acceleration in German inflation could raise speculation for a similar reaction in the bloc's overall print.

Finally on Friday, during the Asian day, Japan's CPIs for August are due for release. Without a forecast available, we see the case for both the headline rate and the core rates to have risen. We base our view on the nation's forward-looking Tokyo CPIs for August, where both the headline and the core rates rose. Even though something like that would probably be further encouraging news for BoJ policymakers, we maintain our view that as long as inflation remains so far away from the 2% inflation target, the Bank is unlikely to alter its QQE with yield-curve control framework. Under this framework, the BoJ has committed not only to achieving 2%, but to actually overshoot it.

During the European morning, Eurozone's preliminary CPI data for September are coming out, though no forecast is available yet for either the headline or core rates. We see the case for both rates to have risen somewhat further, something that we base on the bloc's preliminary composite PMI for September, which showed selling price inflation reaching its highest rate since April. Further uptick in these rates would probably be pleasant news for ECB policymakers, who are set to provide some clear details about the future of QE at their upcoming October meeting. Moving forward, we think that market focus will be on whether the Bank will proceed with a "dovish tapering", whereby it begins to reduce its monthly purchases without setting a clear roadmap for ending the programme completely.

From the US, we get personal income and spending, as well as the core PCE price index, all for August. Getting the ball rolling with income and spending, both of these rates are forecast to have declined from the previous month. The income forecast is supported by the slowdown in the nation's average hourly earnings for the month, while the decline in retail sales suggests that the spending rate may even turn negative. Turning to the core PCE index, in the absence of a forecast, we see the case for the rate to have remained unchanged. We base our view on the core CPI rate for the month, which held steady at +1.7% yoy.