Sample Category Title

GBP Awaits PM May’s Brexit Speech

The US dollar was seen giving back the gains a day after the FOMC meeting. EURUSD managed to recover as the currency pair regained the 1.19 handle.

On the economic front, the Bank of Japan left interest rates and QE unchanged signaling that it could still maintain its easy monetary policy. This led to some weakening in the Japanese yen across the board. The ECB President Mario Draghi gave a speech yesterday but refrained from making any references to monetary policy or the euro's exchange rate.

Looking ahead an important day for the British pound as the Prime Minister, Theresa May will be giving a speech on Brexit to the UK Parliament. Investors are expecting that the UK will be moving towards a softer Brexit. However, the risks are balanced, and the GBP could be seen trading volatile today. ECB President Mario Draghi is also expected to speak later in the day.

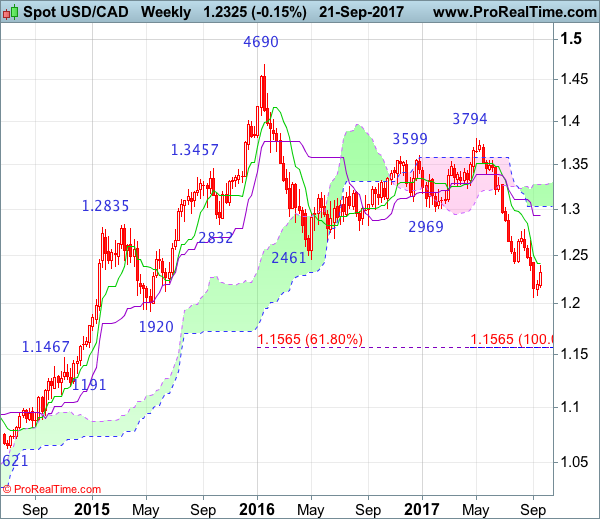

USDCAD In Downtrend Since May, Near-Term Risk To The Downside

USDCAD maintains a bearish market structure on the daily chart. The pair is clearly in a downtrend and making lower peaks and lower lows since the high of 1.3793 on May 5. The market paused a corrective move from the more than 2-year low of 1.2061 and is putting in a top at 1.2390.

USDCAD will likely remain under pressure as long as it trades below key resistance at 1.2400. The recent upside momentum from the bounce off 1.2061 on September 8 has run out of steam, as indicated by the RSI oscillator which has stopped rising.

The near-term risk is to the downside, with scope for a re-test of the 1.2061 low. This level is expected to provide support but should it fail to hold, then USDCAD will resume its downtrend to target the next major low at 1.1919.

Should prices turn back up and rise above the 1.2390-1.2400 resistance zone, the downside pressure would ease and open the way for a move towards next resistance areas at the previous highs of 1.2662 and 1.2777. But only a move above 1.3000 is likely to indicate that the longer-term downtrend has ended.

The underlying bias suggests that the bearish move from May is still in progress. The negatively aligned moving averages are supporting this view, as the 50-day MA is below the 200-day MA following a bearish crossover on July 13. The near-term bias is also bearish.

Can US Dollar Remain In Uptrend Vs Japanese Yen?

Key Highlights

- The US Dollar traded higher this week and moved above 111.50 against the Japanese Yen.

- There is a crucial ascending channel forming with support at 111.70 on the 4-hours chart of USD/JPY.

- US Initial Jobless Claims for the week ending 16th Sep 2017 decreased from the last revised reading of 282K to 259K.

- The US Manufacturing PMI preliminary reading (Sep 2017) will be released today, which is forecasted to increase from 52.8 to 53.0.

USDJPY Technical Analysis

The US Dollar remains in an uptrend and is currently positioned well above the 111.00 support against the Japanese Yen. However, the USD/JPY pair recently struggled to settle above 112.70 and is correcting lower.

Looking at the 4-hours chart of USD/JPY, there is a crucial ascending channel forming with support at 111.70. During the recent drop, the pair broke the 50% Fib retracement level of the last wave from the 111.09 low to 112.71 high.

However, the decline was prevented by the 111.60 support. The pair is once again moving north, but lacking momentum to break 112.20.

To sum up, the pair must stay above 111.70-111.60 to remain in the bullish trend.

US Initial Jobless Claims

Recently in the US, the Initial Jobless Claims figure for the week ending 16th Sep 2017 was released by the US Department of Labor. The forecast was slated for a rise from the last reading of 284K to 300K.

However, the actual result was well above the forecast, as there was a decline in claims to 259K. The last reading was also revised down to 282K. The 4-week moving average now stands at 268,750, which is around 6,000 more than the previous week’s revised average from 263,250 to 262,750.

The report added that:

The advance number for seasonally adjusted insured unemployment during the week ending September 9 was 1,980,000, an increase of 44,000 from the previous week’s revised level.

The result was positive, and might continue to support USD/JPY above the 11.70-50 levels in the near term.

Economic Releases to Watch Today

US Manufacturing PMI for Sep 2017 (Preliminary) – Forecast 53.0, versus 52.8 previous.

US Services PMI for Sep 2017 (Preliminary) – Forecast 55.9, versus 56.0 previous.

Canadian Retail Sales July 2017 (MoM) – Forecast 0.1%, versus +0.1% previous.

Canadian Retail Sales ex Autos July 2017 (MoM) – Forecast +0.4%, versus +0.7% previous.

Canadian Consumer Price Index August 2017 (MoM) – Forecast +0.2%, versus 0% previous.

Canadian Consumer Price Index August 2017 (YoY) – Forecast +1.5%, versus +1.2% previous.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4871; (P) 1.4967; (R1) 1.5145; More....

With break of 1.5031 resistance, intraday bias is turned to the upside for 1.5173/5226 resistance zone first. Break will resume medium term rally from 1.3624. On the downside, below 1.4791 will turn bias to the downside and extend the fall from 1.5173 to retest 1.4421 support.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

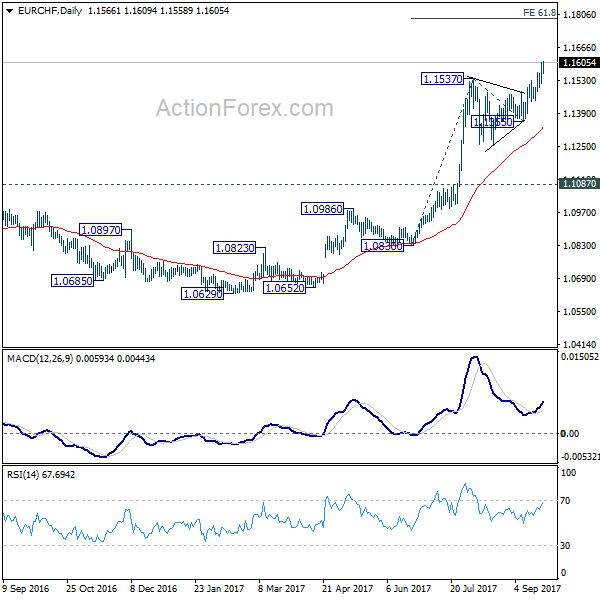

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1537; (P) 1.1571; (R1) 1.1622; More... .

Intraday bias in EUR/CHF remains on the upside for the moment. Current rally is expected to target 61.8% projection of 1.0830 to 1.1537 from 1.1355 at 1.1792 next. On the downside, below 1.1511 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

War Of Words Escalates

It did not take long for North Korea to react to President Trump's recent address to the United Nations General Assembly. Kim Jong-un had responded with a personal statement where he said he was considering retaliating at the “highest level' following Trump's warning that the US would “totally destroy

North Korea' if Washington was forced to defend itself or its allies. This comment was subsequently followed up by comments from North Korea's Foreign Minister, Ri Yong-ho, who said “Pyongyang could respond to Trump's recent threat of military action by testing a powerful nuclear weapon in the Pacific'. Ri Yong-ho told reporters in New York that “It could be the most powerful detonation of an H-bomb in the Pacific. We have no idea about what actions could be taken as it will be ordered by leader Kim Jong-un.' Needless to say, these comments have caused a degree of risk off in the markets with safe-havens benefitting.

Initial Jobless Claims released by the US Department of Labor on Thursday showed those claiming benefits unexpectedly declined 23,000, to a seasonally adjusted 259,000 for the week ended Sept. 16. A Labor Department official commented that “Harvey and Irma affected claims for Texas and Florida'. With Hurricane Maria causing havoc in Puerto Rico, weather is likely to affect near-term claims data and likely hurt job growth in September.

The markets were surprised at the news on Thursday that, the last of the 3 major ratings agencies, Standard & Poors Global Ratings, cut China's sovereign credit rating for the first time since 1999, based on the risks from China's soaring debt, and revised its outlook to stable from negative. China's sovereign rating was cut by one step, to A+ from AA-. This is the second downgrade by a major rating company this year, which suggests concern that China is struggling to maintain a balance between economic growth and improving its financial sector. China had yet to respond to this latest downgrade, but the markets will be wary following the last downgrade which China was strong to refute.

EURUSD gained 0.45% on Thursday trading, as high as 1.19535, and the upward momentum has continued in early trading with EURUSD currently trading around 1.1965.

USDJPY strengthened up to 112.712 on Thursday but weakened in early Friday trading as the markets move into safe-havens following the latest comments from North Korea. Currently, USDJPY is trading around 111.95.

GBPUSD gained nearly 0.7% on Thursday, trading up to 1.35863. Currently, GBPUSD has given up some of those gains to trade around 1.3565.

Gold continued its slide against USD, losing nearly 1% on Thursday, before retracing higher as the markets take a risk-off sentiment into the weekend. Gold is currently trading around $1,296.50.

WTI continues to strengthen and currently trades around $50.75pb, although the markets will be keenly watching the OPEC meeting for any extensions to the current output limits.

Major economic data releases for today:

At 09:00 BST, ECB President Mario Draghi is scheduled to provide a keynote speech at Henry Grattan Lecture Invitation, organized by Trinity College (School of Social Sciences and Philosophy) in Dublin, Ireland.

Sometime between 09:00 BST & 11:00 BST, UK Prime Minister Theresa May is scheduled to speak in Florence, Italy. Mrs. May is expected to give fresh details about the future relationship she wants with the EU.

Currencies: Risk-Off Blocks Post-Fed USD Comeback

Sunrise Market Commentary

- Rates: Profit taking on short positions ahead of the weekend?

North Korea threatened to detonate an H-bomb in the Pacific. Risk aversion reigns in Asia and will dominate at the start of European trading, offering investors the opportunity to take some profit on short positions in the German Bund and US Note future. Central bank speakers (both ECB and Fed) are wildcards. - Currencies: Risk-off blocks post-Fed USD comeback

Yesterday, the dollar failed to extend the gains recorded after the Fed decision on Wednesday. Overnight, sentiment turned risk-off on North Korea, weighing on the dollar. The dollar currently suffers more from a decline in core yields than the yen and even the euro. Sterling traders look out for the Brexit speech of UK PM May.

The Sunrise Headlines

- A slight risk-off tone swept through markets, with the yen and gold drifting higher, and Treasury yields nudging down. Asian equities and US equity futures are all in the red. Tensions on North Korea are the main reason.

- US president Trump ramps up pressure on North Korea. He ordered fresh sanctions on individuals, companies and banks doing business with the country. Kim Jong Un may consider testing a hydrogen bomb, Yonhap reported.

- Brent's premium to WTI hit the widest since August 2015 as OPEC meets in Vienna. There's mixed signals on whether they'll discuss deeper or longer cuts. Russia said it's too early to talk specifics. Brent trades close to $57.30 key level.

- The UK will pay into the EU until 2020 (€20B or more), Theresa May will say in a landmark speech in Florence, a person familiar said. The BBC reported May will seek a transition of 2 years and go for a bespoke trade arrangement.

- Mario Draghi said the ECB isn't in the business of raising rates just to tame local bubbles. If financial and business cycles diverge, imbalances can arise even when inflation is muted, but "monetary policy is not the right instrument" to correct the situation, he said

- Poland's central bank may consider a "small hike" in early 2018 to offset inflationary and wage pressures, MPC Gatnar told Reuters. MPC Minutes showed a majority expects stable interest rates in the coming quarters.

- Today, beside the increased geopolitical tensions with North-Korea, attention goes to the US & EMU PMI business confidence and to Fed & ECB speakers. OPEC meets in Vienna.

Currencies: Risk-Off Blocks Post-Fed USD Comeback

Risk-off to block any post Fed-USD comeback

Yesterday, the dollar failed to build on Wednesday’s post-Fed gains. This was a disappointment for USD bulls. Investors clearly didn’t buy into the Fed’s “hawkish” stance on policy normalisation. The US yield rally also fell apart. Strong US eco data didn’t support further USD gains. EUR/USD finished the day at 1.1941 (from 1.1892). USD/JPY was more resilient. The pair hovered in a tight range close to the recent top and at 112.48.

Overnight, risk sentiment soured in Asia. Press reports said that North Korea might retaliate on Trump’s speech and trade measures, testing a hydrogen bomb in the pacific (see headlines). The renewed geopolitical tensions caused a modest risk-off repositioning. Asian equity indices show losses, bonds gain and the Yen outperforms. USD/JPY declined from the mid 112 area to the 111.84 area. The dollar is also losing slightly against the euro (EUR/USD currently at 1.1960). Even post-Fed, the dollar remains most vulnerable to a decline in core yields.

Today, the US & EMU September PMI’s will be published. Both are expected to show only minor changes compared to August. US manufacturing PMI is expected slightly higher (53). The weaker dollar hadn’t yet a substantial impact. The US nonmanufacturing PMI confidence has gone steadily up in the past months and consolidation is expected (55.7). The EMU manufacturing PMI reached a cyclical high in August at 57.4 despite a stronger euro. Consensus expect a minor decline to 57.2. The EMU Services PMI is expected marginal higher at 54.8 (from 54.7). We see risks on the upside of consensus for the latest measure. After the Fed meeting, any USD reaction to good US data would be interesting, but the US PMI is no strong market mover. There are also plenty of ECB members scheduled to speak, including Draghi, Coueré and Constancio. The discussions on the fate of the APP programme in 2018 are ongoing. However, tensions on North Korea probably will dominate trading. Of late, the risk-off reaction to geopolitical tensions was mostly modest and short-lived. However, investors will probably refrain from picking-up risky assets ahead of the weekend. This lingering risk-off feeling is mostly negative for the dollar; in the first place for USD/JPY, but to a lesser extend also for EUR/USD.

From a technical point of view EUR/USD hovers in a consolidation pattern between 1.1823 and 1.2070. It was disappointing for EUR/USD bears that last week’s correction didn’t reach the range bottom. More confirmation is needed that the bottoming out process in US yields and in the dollar might be the start of more sustained USD gains (against the euro). In case of a break, next support in EUR/USD comes in at 1.1774 and 1.1662

The day-to-day momentum in USD/JPY is (was?) more constructive. The yen traded weak across the board and the dollar might be in better shape post-Fed. USD/JPY regained the 110.67/95 previous resistance. This a short-term positive. If current event risk on north Korea is again temporary in nature, the yen might remain in the defensive. The 114. 49 correction top is the next important reference.

EUR/USD: dollar fails to extend gains post-Fed. North Korea risk-off is also no help

EUR/GBP

Sterling well bid going into May’s Brexit speech

Yesterday, sterling initially stabilized after Wednesday’s strong performance. UK August public finance results were better than expected but played no role. Sterling found again a stronger bid late in Europe. We didn’t see any specific reason. A further repositioning ahead of May’s Brexit speech was probably in play. EUR/GBP finished the session at 0.8792. Cable closed the day at 1.3580. The recent highs against the euro and the dollar are again within reach

Today, the CBI trends orders will be published. However the focus will be on the Brexit speech of UK PM May. PM May is expected to sound a bit more conciliatory on key issues as the Brexit bill and will aim for a transition period. Question is whether these ‘concessions’ will be enough to unlock the stalemate at the next round of formal negotiations. A more constructive environment might be slightly sterling supportive. However, we don’t expect today’s speech to clear the horizon in a profound way. EUR/GBP is again close to the recent lows. A break could cause some extension of the recent GBP-comeback.

EUR/GBP made an impressive uptrend since April and set a MT top at 0.9307 late August. The euro was strong and UK price data were soft enough to keep the BoE side-lined. Recent UK price data amended this story and the reversal of sterling was reinforced by hawkish BoE comments. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of relative euro strength and sterling softness to persist. However, the prospect of (limited) withdrawal of BOE stimulus put a solid floor for sterling ST term. We look how far the current correction has to go. EUR/GBP is nearing support at 0.8743 and 0.8652, which we consider difficult to break. We start looking to buy EUR/GBP on dips.

EUR/GBP: near recent lows going into May’s Brexit speech

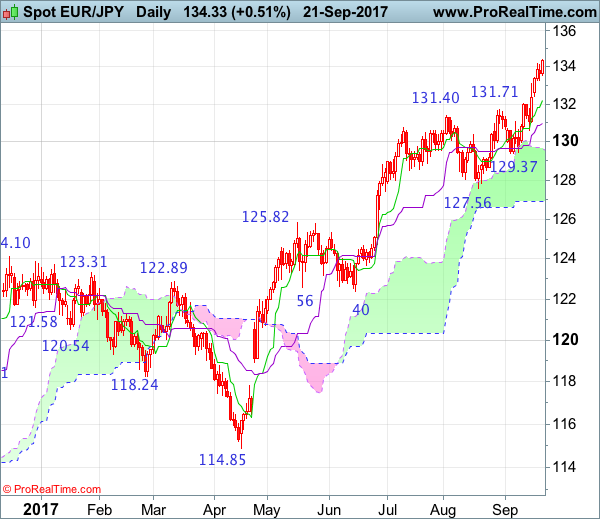

EUR/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Window

• Time of formation: 24 April 2017

• Trend bias: Up

Daily

• Last Candlesticks pattern: Hammer

• Time of formation: 18 May 2017

• Trend bias: Up

EUR/JPY – 134.00

The single currency has continued moving higher throughout this week after breaking above previous resistance at 132.01, adding credence to our bullish view that recent upmove is still in progress and may extend further gain to 134.55-60, then 135.00, however, near term overbought condition should limit upside to 136.00-10 and reckon 136.90-00 would hold from here, price should falter well below 138.45-50 (1.618 times extension of 109.49-124.10 measuring from 114.85), risk from there has increased for a much-needed correction to take place next month.

On the downside, whilst initial pullback to 133.65-70 cannot be ruled out, reckon support at 133.26 would limit downside and bring another rise later. Below previous resistance at 133.09 would bring correction to 132.35-40 and then test of the Tenkan-Sen (now at 132.06) but only a daily close below this level would suggest a temporary top is possibly formed, bring retracement of recent rise to 131.40-50 and possibly towards the Kijun-Sen (now at 130.87) but previous support at 130.62 should remain intact.

Recommendation: Buy at 132.50 for 135.00 with stop below 131.50.

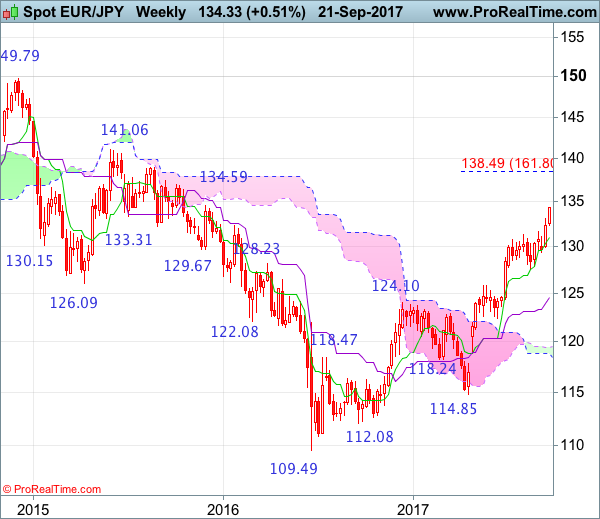

On the weekly chart, after last week’s rally to 133.09, the single currency has moved higher again this week and another white candlestick looks set to be formed, adding credence to our bullish view that the erratic upmove from 109.49 (2016 low) is still in progress for gain to indicated upside target at 134.40 (61.8% Fibonacci retracement of entire fall from 149.79-109.49), then 135.00, however, reckon upside would be limited to 136.00-10 and 136.95-00 should hold, price should fatter below 138.45-50 (1.618 times extension of 109.49-124.10 measuring from 114.85), bring retreat later.

On the downside, expect pullback to be limited to 132.38 support and bring another rise to aforesaid upside targets. Below said support would bring minor correction to 131.90-00, then 131.40-50 but a weekly close below the Tenkan-Sen (now at 130.87) is needed to suggest a temporary top is possibly formed, bring test of 130.62 support, only a drop below this level would add credence to this view and signal retracement of recent upmove has commenced for further decline to 128.90-00, then towards 128.00-10 but previous support at 127.56 should remain intact.

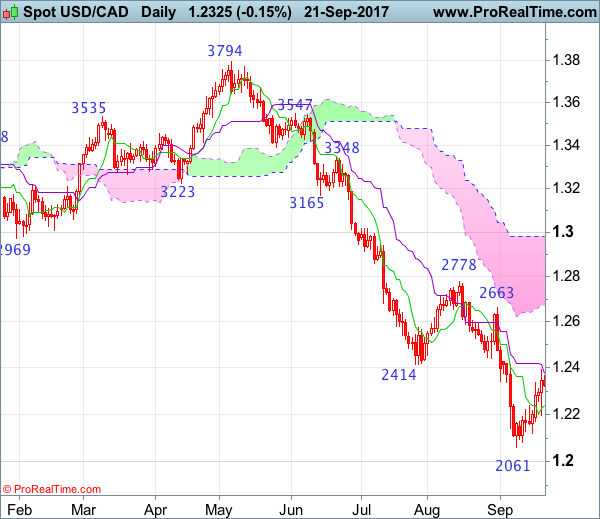

USD/CAD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting doji

• Time of formation: 01 May 2017

• Trend bias: Sideway

Daily

• Last Candlesticks pattern: Bearish engulfing

• Time of formation: 5 May 2017

• Trend bias: Down

USD/CAD – 1.2300

As the greenback found support at 1.2197 and has rebounded again, suggesting further consolidation above recent low at 1.2061 would be seen and near term upside risk remains for the corrective rise from there to bring retracement of recent decline, hence gain to 1.2415 resistance and then test of previous support at 1.2441, above latter level would bring a stronger rebound to 1.2500 and then 1.2520-25, however, near term overbought condition should prevent sharp move beyond 1.2560-70 and price should falter well below resistance at 1.2663, bring retreat later.

On the downside, expect pullback to be limited to 1.2270 and the Tenkan-Sen (now at 1.2237) should hold, bring another rebound later. A daily close below said support at 1.2197 would suggest the rebound from 1.2061 has ended, bring further fall to 1.2140-50, then test of support at 1.2121 but break of latter level is needed to signal recent decline has resumed and bring retest of 1.2061. Looking ahead, below 1.2061would extend downtrend to psychological level at 1.2000, having said that, loss of momentum should prevent sharp fall below 1.1920-25 (61.8% projection) and 1.1900 should hold.

Recommendation: Take profit on our short position entered at 1.2340 and stand aside for this week.

On the weekly chart, this week’s rebound looks set to form another white candlestick and further consolidation above this month’s low at 1.2061 would take place and another corrective bounce to 1.2414-20 (previous support and current level of the Tenkan-Sen) cannot be ruled out, however, reckon upside would be limited to 1.2500 and 1.2600 should hold. Only a weekly close above resistance at 1.2663 is needed to signal a temporary low has been formed at 1.2061, bring retracement of recent decline towards resistance at 1.2778 which is likely to hold from here.

On the downside, whilst pullback to 1.2270 cannot be ruled out, reckon 1.2220-30 would hold and bring another rebound, below this week’s low at 1.2171 would suggest the rebound from 1.2061 has ended, bring test of 1.2121, break there would signal decline from 1.3794 top has resumed for retest of 1.2061, break there would extend weakness towards psychological support at 1.2000, however, reckon downside would be limited to 1.1920-25 (61.8% projection of 1.3794-1.2414 measuring from 1.2778) and reckon 1.1840-50 would hold from here, price should stay above 1.1750-60, bring rebound later.

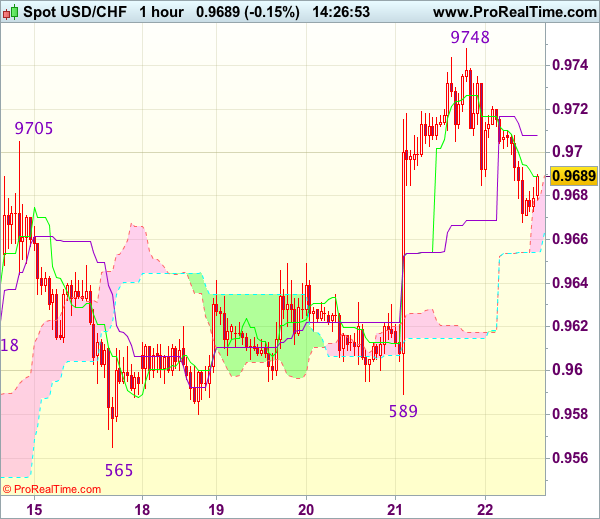

Trade Idea : USD/CHF – Stand aside

USD/CHF - 0.9683

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9689

Kijun-Sen level : 0.9708

Ichimoku cloud top : 0.9678

Ichimoku cloud bottom : 0.9654

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback retreated after rising to 0.9748 earlier this week and consolidation below this level would be seen and pullback towards the lower Kumo (now at 0.9654) cannot be ruled out, however, reckon previous minor resistance at 0.9630 would limit downside and price should stay well above indicated support at 0.9589, bring rebound later.

On the upside, whilst recovery to the Kijun-Sen (now at 0.9708) cannot be ruled out, reckon upside would be limited to 0.9720-25 and said resistance at 0.9748 should hold, bring retreat later. In the event dollar is able to penetrate said resistance at 0.9748, this would revive bullishness and extend recent rise from 0.9421 low to 0.9761-66 (50% Fibonacci retracement of 1.0100-0.9421 and previous resistance), then another previous resistance at 0.9773. As near term outlook is still mixed, would be prudent to stand aside for now.