Sample Category Title

USD/CAD Minor Retreat May Appear

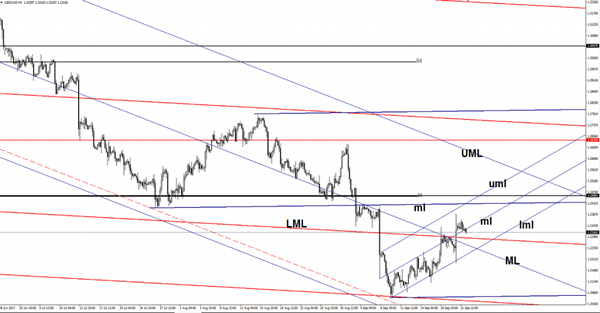

USD/CAD drops after another failure to reach the upper median line (uml) of the minor ascending pitchfork. A retest of the median line (ml) will signal a drop towards the lower median line (lml) of the same minor ascending pitchfork.

Support can be found at the lower median line (LML) of the red descending pitchfork and at the median line (ML) of the blue descending pitchfork.

NZD/USD Throwback?

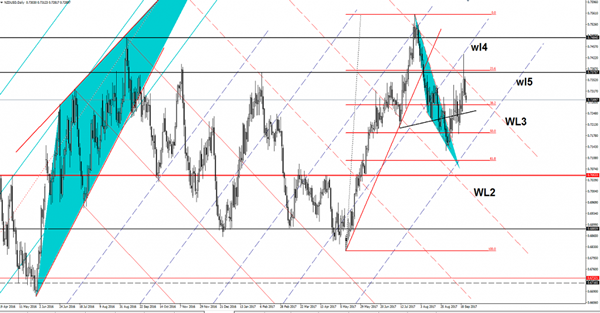

The NZD/USD drops further and should hit the 38.2% retracement level, which represents a very important static support. Remains to see if will break this or will bounce back and will try once again to take out the major dynamic resistance from the third warning line (WL3). Will drop much deeper if will stay trapped below the third warning line (WL3).

USD/JPY Rejected By Confluence Area

The currency pair has dropped sharply in the morning and seems poised to start a corrective phase. The Yen has taken the lead again as the Nikkie stock index plunges after the impressive rally. Technically, the currency pair maintains a bullish perspective, despite a minor retreat.

USD/JPY moves in range on the short term, so we’ll have a clear direction once will escape from this extended sideways movement. The Japanese currency could dominate the currency market in the upcoming days as the JP225 could come to retest the 20058 former horizontal resistance. I’ve said in the last reports that the index is expected to retreat a little after the upside momentum.

Surprisingly or not, the USD is losing ground versus all its rivals even if the United States data have come in better on Thursday.

Price is still trapped within the extended sideways movement, it was expected to climb towards the 23.6% retracement level, but has fond strong resistance at the confluence formed between the median line (ml) of the minor ascending pitchfork with the first warning line (wl1). USD/JPY was rejected by the mentioned confluence and now will hit the 38.2% retracement level. Could come down to retest the third warning line (WL3) to validate this dynamic support (resistance turned into support).

A further Nikkei retreat will send the rate towards the 250% Fibonacci line and towards the lower median line (lml) of the minor ascending pitchfork.

U.K. Prime Minister Theresa May’s Speech In Focus

Euro Soars Higher After Draghi's Comments. The mood was a bit cheerier in the European markets, with ECB head Draghi declaring that the financial sector no longer poses a threat to the economy. The bullish sentiment around the Eurozone currency is going strong, suggesting it has some more room to rally.

Aussie Tumbled Across the Board After Governor Lowe's Speech. The Australian dollar bears painted the forex town red on Thursday as the commodity currency was weighed down by the RBA's shaky tightening bias, the credit rating downgrade on China, and the sharp drop in gold prices.

Kiwi Slips to 72.81 US Cents as Fed's Rate Hike. The New Zealand dollar fell as the US Federal Reserve signals on balance sheet unwinding and interest rate hikes outweighed gains made earlier in the week after a poll showing the National Party in the lead ahead of tomorrow's vote.

Traders Looking Forward to How Prime Minister May's Speech Might Turn Out. All eyes and ears are on U.K. Prime Minister Theresa May as she prepares to deliver her Brexit speech in Florence today. She is expected to propose a two-year transition period for both parties to hash things out, during which the U.K. can retain access to the single market even after the official split happens on March 2019.

Gold Falls on Dec Rate Hike Expectations. Gold fell in reaction to a rising US dollar, losing over 1% and falling back under the $1,300 level after the Fed signaled it was on track to raise US interest rates again in December. The metal is highly sensitive to rising US rates, which boost the cost of holding non-yielding bullion relative to other assets.

Oil Prices Steady Ahead of OPEC Meeting on Supply Cut Extension. Oil prices held steady in early Asian trade on Friday as the market waited to see whether major oil producers would extend supply cuts beyond March at a meeting in Vienna later in the day.

Watch Out Today for:

09:00 am GMT: EUR ECB President Draghi's Speech

GBP UK Prime Minister Theresa May speech

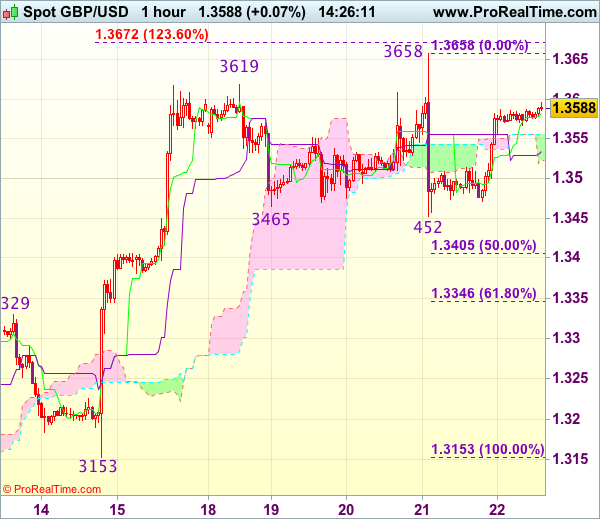

Trade Idea : GBP/USD – Stand aside

GBP/USD - 1.3565

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.3580

Kijun-Sen level : 1.3534

Ichimoku cloud top : 1.3555

Ichimoku cloud bottom : 1.3523

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although cable has retreated after edging higher to 1.3596 and consolidation with mild downside bias is seen for weakness towards the Kijun-Sen (now at 1.3534), below 1.3500 is needed to revive near term bearishness and signal the rebound from 1.3452 has ended, bring further fall to 1.3470, then test of said support. Looking ahead, only a drop below 1.3452 would add credence to our view that top has been formed at 1.3658 earlier this week, bring retracement of recent rise to 1.3400-05 (50% Fibonacci retracement of 1.3153-1.3658).

On the upside, above 1.3600 would extend gain to 1.3620-25, however, still reckon said this week’s high at 1.3658 would hold from here, bring retreat later. Only a break above said resistance at 1.3658 would signal recent upmove has resumed and extend gain to 1.3690-00 later. As near term outlook is still mixed, would be prudent to stand aside for now.

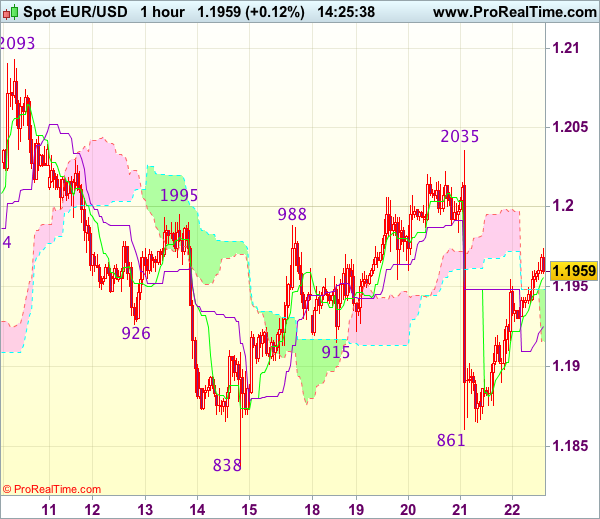

Trade Idea : EUR/USD – Hold short entered at 1.1970

EUR/USD - 1.1965

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.1956

Kijun-Sen level : 1.1925

Ichimoku cloud top : 1.1948

Ichimoku cloud bottom : 1.1916

Original strategy :

Sold at 1.1970, Target: 1.1870, Stop: 1.2005

Position : - Short at 1.1970

Target : - 1.1870

Stop : - 1.2005

New strategy :

Hold short entered at 1.1970, Target: 1.1870, Stop: 1.2005

Position : - Short at 1.1970

Target : - 1.1870

Stop : - 1.2005

As the single currency found good support at 1.1861 and has staged a strong rebound, suggesting consolidation above this level would be seen, however, as long as 1.2000 holds, mild downside bias remains for another decline, below 1.1915-20 would bring test of 1.1885-90 but break of latter level is needed to signal the rebound from 1.1861 has ended, bring another fall to this level, then retest of previous support at 1.1838 which is likely to hold on first testing.

In view of this, we are holding on to our short position entered at 1.1970. Above 1.2000 would dampen our bearishness and risk test of this week’s high at 1.2035 but only break there would shift risk back to upside and extend the rebound from 1.1838 to 1.2060-70 first.

PMI Figures Released In Germany, France And The Euro Area

Market movers today

Markets will keep a close eye on Theresa May's speech on Brexit in Florence this afternoon, where she will outline the details of the UK's negotiating stance after the UK formally leaves the EU at the end of March 2019. Yesterday, parts of May's speech was already leaked and among other things it was confirmed that May will propose a two-year transition period after Brexit takes effect, see Bloomberg for more.

Today, we have a busy data calendar, not least with PMI figures released in Germany, France and the euro area. We expect euro area manufacturing PMI to remain strong, but moderate slight ly to 57.2 in September, as the euro appreciation is bound to drag on export orders eventually, despite activity so far remaining strong. We look for a similar decline in the Service PMI due to weaker signals from the new orders component in the last reading, and forecast service PMI at 54.2 in September.

The market will also have plenty of ECB speeches to digest as Mario Draghi, Benoît Coeuré and Vítor Constâncio are all scheduled to speak.

In the US, Markit PMI manufacturing is due to be released, which we estimate will show a further increase given the recent large disparity between ISM manufacturing and Markit PMI manufacturing (58.8 versus 52.8). Again, however, numbers might be somewhat skewed due to the impact of the recent hurricanes.

Selected market news

Risk sentiment took a small hit yesterday as tensions with North Korea increased again. Equit ies as well as bond yields declined and the JPY st rengthened.

The North Korean leader responded to US President Donald Trump's speech in UN where Trump threatened to dest roy North Korea totally. Kim Jong-un called T rump ‘mentally deranged' in a rare statement rare directly from the North Korean leader , and vowed to make Trump pay dearly. He said Trump's comment s had confirmed his nuclear programme was the ‘correct path' and also st at ed t hat ‘we will consider with seriousness the exercising of a corresponding, highest level of hard-line count ermeasure in hist ory', see South China Morning Post. Kim's foreign minister said t o report ers t hat t hese measures could include t esting a hydrogen bomb in the pacific. Yesterday, Trump announced new financial sanctions targeting North Korea. Trump also said that Chinese President Xi Jinping had ordered Chinese banks to cease conduct ing business with North Korean entities. Trump praised Xi, calling t he move ‘very bold' and ‘somewhat unexpected'.

Yesterday, the US Philadelphia Fed manufacturing index pointed to continued strength in US manufacturing. The index increased from 18.9 in August to 23.8 in September (consensus 17.1). Details showed a decent rise in the orders index as well.

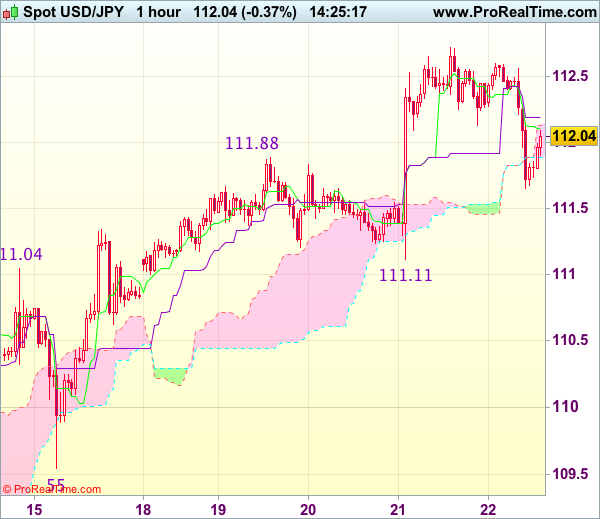

Trade Idea : USD/JPY – Hold long entered at 111.70

USD/JPY - 112.02

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 112.11

Kijun-Sen level : 112.19

Ichimoku cloud top : 112.13

Ichimoku cloud bottom : 111.88

Original strategy :

Bought at 111.70, Target: 112.70, Stop: 111.35

Position : - Long at 111.70

Target : - 112.70

Stop : - 111.35

New strategy :

Hold long entered at 111.70, Target: 112.70, Stop: 111.60

Position : - Long at 111.70

Target : - 112.70

Stop : - 111.60

Although the greenback retreated after rising to 112.72 yesterday and consolidation below said resistance would be seen initially, reckon 111.65 would contained downside and bring another rise later towards said resistance but only break there would confirm recent upmove has resumed and extend further gain to 112.90-00, then towards 113.25-30 (1.236 times projection of 107.32-111.04 measuring from 109.55), having said that, previous chart resistance at 113.58 would hold from here, bring retreat later.

In view of this, we are holding on to our long position entered at 111.70. Below said support at 111.65 would risk weakness to 111.40-45 but break there is needed to signal a temporary top has been formed at 112.72, bring retracement of recent rise towards support at 111.11 first.

Market Update – Asian Session: North Korea Rhetoric Again Weighs

Asia Summary

Asian equity markets opened mixed, in line with Thursday’s NY trading session. Rio Tinto opened higher by over 1%, after announcing an additional $2.5B stock buyback. Shares of Taiwan’s HTC have risen over 9% following the transaction with Google.

On the geopolitical front, President Trump announced an executive order for additional US sanctions on North Korea, which may include shipping and trade networks. North Korea later responded and said it would consider the ‘highest level of countermeasure.’

Later, a South Korean press report (citing North Korea’s Foreign Minister) suggesting that North Korea could conduct an H-bomb test has since weighed on markets.

Amid the North Korea headline, AUD/JPY has declined over 0.4%. Also, China’s metals, including iron ore, have traded lower by over 2%, following reports that the Shanghai Metals Exchange raised trading fees.

South Korean steelmakers have traded sharply lower (Posco -4.1%) amid press speculation that the US could increase tariffs.

In corporate issuance, China Postal Savings Bank announced plans to issue $7.25B in perpetual preference shares in order to strengthen additional Tier 1 capital. On the sovereign front, S&P downgraded Hong Kong from AAA, while China criticized its own recent downgrade by the ratings agency.

S&P also issued its Banking Industry Country Risk Assessment (BIRCA) on Japan, in which it revised the trend for the country’s economic risk to stable from negative. It also revised the view of the trend for banking industry risk to negative from stable.

Looking ahead, comments are expected out of ECB (Draghi, Coeure, Constancio) and Fed officials (Williams, Kaplan)

In US corporate news, there has been press speculation that Hewlett Packard Enterprise is said to be planning to cut ~5,000 jobs, which equals about 10% of its total workforce.

Speakers and Press

China

(HK) S&P downgrades Hong Kong sovereign rating to AA+ from AAA (follows recent downgrade of China); Outlook revised to Stable from Negative; cites potential for spillover risks.

(CN) China MOF: S&P sovereign rating cut of China is 'wrong decision'; The ratings agency's inclusion of local government debt financing vehicles into local government debt does not have legal foundation.

(CN) S&P Tan: Says local government financing vehicles (LGFVs) still a key source of China credit growth.

Other

(KR) North Korea countermeasure may mean H-bomb test in Pacific - South Korean Press; Cites North Korea Foreign Minister.

(KR) North Korea leader Kim Jong Un: President Trump's UN speech was rude nonsense, he is mentally unstable; Trump should select his words prudently; Says to mull highest level of countermeasure.

(JP) S&P publishes latest Banking Industry Country Risk Assessment (BIRCA) on Japan; revised 'trend for Japan's economic risk to stable from negative'; revised view of trend for banking industry risk to negative from stable

(JP) Japan Defense Min: North Korea Foreign Min comments about hydrogen bomb test in Pacific Ocean are 'absolutely unacceptable'; Says North Korea Foreign Minister remarks are personal, but should take them seriously.

(JP) Japan Chief Cabinet Spokesman Suga: Plans to hold extraordinary Diet session on Sept 28th

(JP) Japan Finance Min Aso: Government has not decided to delay budget balancing; not yet sure if 2020 primary surplus target can be hit

(JP) Japan Economic Revitalization Min Motegi: Maintains primary balance surplus target; will reassess target in next years mid-term review

(JP) Japan PM Abe to speak to press on Monday afternoon – US financial press

(KR) US Dept of Commerce said to have included South Korea on list for sanctions of steel imports - South Korea Press; The report says an announcement could come at the end Sept.

Asian Equity Indices/Futures (00:30ET)

Nikkei -0.3%, Hang Seng -0.9%, Shanghai Composite -0.5%, ASX200 +0.3%, Kospi -0.7%

Equity Futures: S&P500 -0.3% ; Nasdaq -0.5% , Dax -0.2% , FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1938-1.1959; JPY 111.66-112.56; AUD 0.7909-0.7934; NZD 0.7282-0.7313

Aug Gold +0.5% at 1,300/oz; Aug Crude Oil +0.1% at $50.62/brl; Sept Copper -0.9% at $2.911/lb

GLD SPDR Gold Trust ETF daily holdings up 6.21 tons to 852.2 tons

(CN) China PBOC sets yuan reference rate at 6.5861 v 6.5867 prior

(CN) PBOC OMO: To inject CNY120B in 7 and 28-day reverse repos v injected CNY60B in 7 and 28-day reverse repo prior; Weekly net injection CNY450B v CNY260B injection prior

(AU) Australia sells A$800M in 2.25% May 2028 bonds, avg yield 2.8368, bid to cover: 3.7X

Equities notable movers

Australia

Seven West Media, SWM.AU Did not reach merger agreement with Prime Media; +1.7%

Tatts Group, TTS.AU Received gambling regulatory approvals for planned merger with Tabcorp ; +2.7%

Hong Kong/China

Logan Property Holdings, 3380.HK Denied that it was planning share placement ; -7%

US markets on close: Dow -0.2%, S&P500 -0.3%, Nasdaq -0.5%, Russell flat

Best Sector in S&P500: Industrials +0.3%

Worst Sector in S&P500: Consumer Staples -1%

At the close: VIX 9.67 (-0.11pts); Treasuries: 2-yr 1.44% (flat), 10-yr 2.278% (flat), 30-yr 2.805% (-2bps)

US Market Summary

US equity markets drifted lower despite some better than expected data in the August Leading Indicators and the September Philly Fed. Heads of state continued consultations in NY and President Trump emerged with an announcement that the US, Japan and South Korea would further tighten sanctions on the regime in Pyongyang. WTI crude managed to rally off of early lows to close up 0.1%, while natural gas tanked 4.3% after the EIA posted a larger than expected build in gas inventories. Bond yields continued to creep higher, with the 10-year stretching above 2.8%.

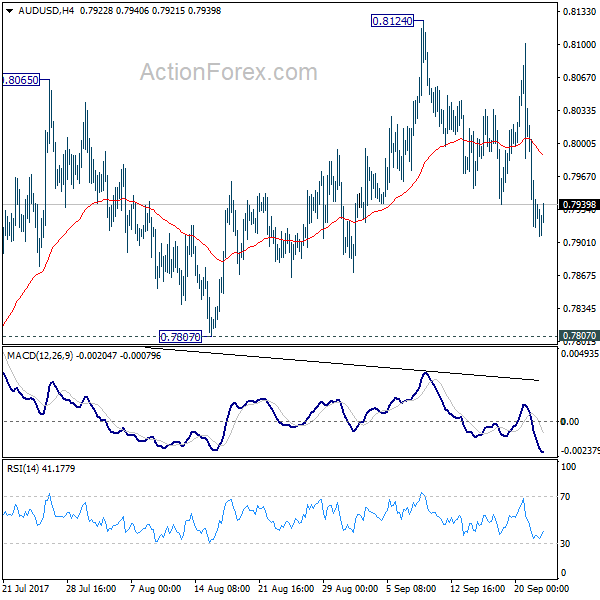

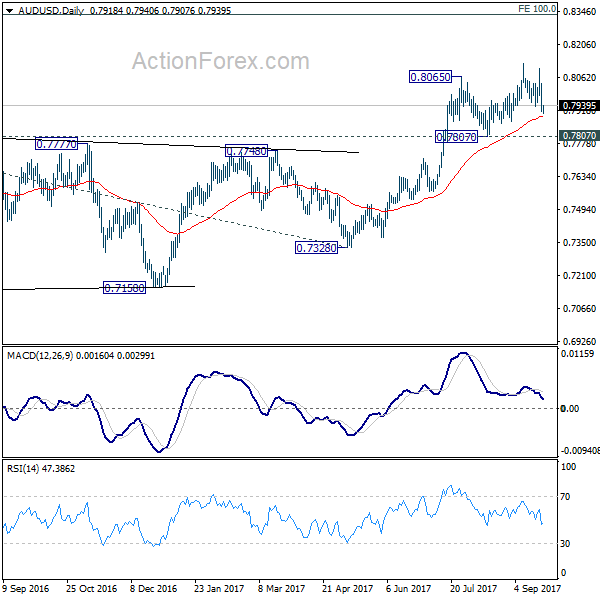

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7888; (P) 0.7961; (R1) 0.8007; More...

At this point, AUD/USD is still bounded in range of 0.7807/8124. Intraday bias remains neutral for more consolidative trading. Deeper fall cannot be ruled out. But still, with 0.7807 support intact, near term outlook stays bearish and another rise is expected. Break of 0.8124 will turn bias to the upside and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335 next. However, considering bearish divergence condition in 4 hour MACD, firm break of 0.7807 will indicate near term reversal and turn bias back to the downside for 0.7328 key support.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8090) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7807 support is needed to to be the first sign of completion of the rebound. Otherwise, further rise is now in favor.