Sample Category Title

Technical Outlook: WTI Oil – Fresh Bullish Acceleration Looks For Final Break Above $50.48 Top

WTI oil price is back above $50 on Tuesday and looking for retest of last week's new high at $50.48 (the highest since 25 May).

Upside attempts in past three days were repeatedly rejected (Bullish candle with long upper shadow on 14 Sep and two long-legged Dojis on Fri / Mon) suggesting that bull-leg from $46.99 (11 Sep trough) might be running out of steam.

Sustained break higher is needed to signal extension of the bull-leg from $46.99 which is also the third wave of five-wave sequence from $47.57 (31 Aug low) towards its 100% Fibonacci expansion at $50.83.

Bullish technical studies and positive sentiment are supportive for further upside, but markets are eyeing for further signals from US crude stocks reports (API is releasing its report late today and EIA on Wednesday) with both reports showing build in oil inventories in past two weeks.

Meeting between OPEC members and other oil producers is scheduled on Friday and is in focus as oil producers are expected to talk about possible extension of oil production cap.

Broken 200SMA now offers solid support at $49.57, followed by lows of Monday / last Thursday at $49.14, reinforced by rising 10SMA.

Res: 50.48, 50.83, 51.00, 51.74

Sup: 50.00, 49.77, 49.57, 49.14

Technical Outlook: USDCAD – Corrective Rally Shows Initial Signs Of Stall

The USDCAD pair holds in red on Tuesday with upside attempts being limited at 1.2300 barrier. Fresh easing comes after Monday’s comments by

BOC Deputy Governor Lane, who said that BOC will pay close attention to the respond of the economy to strong Canadian dollar and higher interest rates.

Lane’s remarks resulted in lowered probability of rate hike in October, which fell to 38% from 44% before the statement.

CAD hit the lowest level in two weeks against the greenback in immediate reaction, but loonie’s losses look short-lived so far.

Correction of the downleg from 1.2662 to 1.2061 probed above its 38.2% retracement at 1.2290 but failed to close above it on Monday, after hitting high at 1.2337, where rally was capped by falling 20SMA.

Technical studies remain in strong bearish setup and keep focus at the downside. Current corrective action should be ideally capped at current levels, with return below 10SMA (1.2185) to confirm lower top and shift near-term focus lower.

Conversely, renewed strength above 20SMA (1.2334) would risk further upside extension. Next key barriers lay at 1.2419/32 (daily Kijun-sen / Fibo 61.8% of

1.2662/1.2061) and break here would signal extended corrective action.

Res: 1.2300, 1.2337, 1.2361, 1.2419

Sup: 1.2261, 1.2232, 1.2186, 1.2166

Market Update – European Session: German ZEW Recovers From Recent Uncertainty Aided By Improving Growth

Notes/Observations

German economic expectations rebound in Sept aided by solid Q2 GDP growth and no uncertainty expected in the upcoming German Federal elections

Overnight

Asia:

China Foreign Min Wang: Reiterates view that North Korea nuclear issue must be resolved peacefully with talks. To strictly follow UN resolutions and assume its international obligations

US Defense Sec Mattis: there are military options that exist for North Korea that would not put Seoul at grave risk. Discussed reintroduction of nuclear weapons to Korean Peninsula with S. Korean counterpart

Europe:

BOE Gov Carney reiterated MPC view that some BOE tightening may be needed in coming months spare capacity was being absorbed a bit faster rate than anticipated; rate hikes will be limited and gradual

PM May said to convene special Brexit cabinet meeting in order to bind Foreign Sec Johnson to her vision of Brexit before her key speech in Florence on Friday, Sept 22nd

Americas:

Bank of Canada's (BOC) Lane: Paying close attention to impact of stronger CAD currency. Each decision is a live decision. Rates are still quite low to what we feel is a neutral level for rates

Trade Rep Lighthizer: China's broad effort to subsidize its industries is a threat to the world trading system; WTO has been unable to handle China's threat to trade under current rules

Economic data

(EU) Euro Zone July Current Account (Seasonally Adj): €25.1B v €22.8B prior; Current Account NSA: €32.5B v €29.8B prior

(IT) Italy July Current Account: €8.6B v €5.3B prior

(DE) Germany Sept ZEW Current Situation Survey: 87.9 v 86.2Be; Expectation Survey: 17.0v 12.0e

Fixed Income Issuance:

(ID) Indonesia sold total IDR17.5T in 3-month and 9-month Bills; 5-year,10-year,20-year and 30-year Bonds

(ES) Spain Debt Agency (Tesoro) sold total €2.95B vs. €2.5-3.5B indicated range in 3-month and 9-month Bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 381.7, FTSE +0.2% at 7268, DAX -0.1% at 12547, CAC-40 flat at 5229, IBEX-35 +0.4% at 10383, FTSE MIB flat at 22367, SMI +0.1% at 9060, S&P 500 Futures flat]

Market Focal Points/Key Themes: European Indices trade mostly higher across the board in range bound trade as Indices remain muted ahead of tomorrow's FOMC rate decision. The FTSE trades higher as the Sterling continues to give back some ground after the large gains seen of late. On the corporate front Ocado is one of the leading decliners after posting Q3 results while Fingerprint cards continues to see weakness after guiding Q3 Revenues yesterday. M&A activity continues to be in Focus with BASF acquiring Solvay's Polyamides business for €1.6B, whilst Eurofins Scientific acquired EAG Laboratories for $780M in cash meanwhile Haldex trades lower in Sweden after Knorr-Bremse withdrew their bid. Looking ahead to the US morning notable earners include Autozone, Apogee and Yingli Green ENergy.

Equities

Consumer discretionary [Ocado [OCDO.UK] -4.3% (Earnings), Hugo Boss [BOSS.DE] -2.8% (Analyst downgrade), Intertrust [INTER.NL] -3.5% (CFO steps down)] -Consumer Staples [Eurofins [ERF.FR] +5.2% (Acquistion)]

Industrials: [Haldex [HLDX.SE] -3% (Knorr Bremse withdraws offer)]

Technology: [FIngerprint Cards [FINGB.SE] -11% (Follow through, Analyst downgrade)]

Telecom: [Kinepolis [KIN.BE] +6% (Acquisition)]

Healthcare:[Solvay [SOLB.BE] -1.4% (Divests Polyamides business to BASF)]

Speakers

France Fin Min Le Maire: 2018 budget will be fair and support the economy; Govt likely to cut spending by €16B in 2018. Lowered the2017 budget deficit to GDP ratio from 3.0% to 2.9% and 2018 budget deficit to GDP ratio to 2.6% (prior govt estimate was 2.7%)

France Finance Ministry 2018 Budget Statement (official release): Planned budget deficit to GDP of 2.6% and net tax cut of €10B

Spain Fin Min de Guindos: Govt to approve 2018 budget on Friday, Sept 22nd

German ZEW Economists noted that the improved morale was due to solid Q2 GDP growth, rise in bank lending and investment by both govt and private companies. Saw no uncertainty expected in upcoming German elections and concerns over stronger Euro currency have faded

Bank of Korea (BOK) Aug Minutes noted that one member saw its current monetary policy as accommodative but needed to change stance. Timing is important in reducing monetary easing; 2% CPI meant bigger need to reduce easing

Japan PM Abe to hold press conference on Monday, Sept 25th (**Note: Reports circulated that Abe would call a snap election as soon as Sept 25th to take advantage of the uptick in approval ratings and the disarray in the main opposition party)

Iraq Oil Min Al-Luaibi: Current oil production cuts are going fine; prices and global markets are improving. Iraq and other oil producers seek an additional 1% in production cuts but no decision made.

Currencies

USD/JPY edged towards the 112 level on speculation that PM Abe would soon call a snap election t to take advantage of the uptick in approval ratings and the disarray in the main opposition party. The weaker yen currency amid expectations that victory for the ruling coalition would mean continuation of current BOJ policies

GBP/USD was back below the 1.35 level after hitting key technical resistance at 1.36. PM May reportedly to convene special Brexit cabinet meeting in order to bind Foreign Sec Johnson to her vision of Brexit before her key speech in Florence on Friday, Sept 22nd.

EUR/USD locked in recent range just under the 1.20 level. Better German ZEW data kept the tailwinds behind the Euro while concerns over its recent strength seemed to have faded

Fixed Income

Bund futures trade at 161.13 up 7 ticks as markets await the Fed Meeting and ECB speakers. Continued downside targets 161.03 while upside resistance stands initially at 162.07, followed by 163.27.

Gilt futures trade at 125.59 up 17 ticks as more banks predict a November BOE hike. Continued downside eyeing 124.91. Upside targets 127.90 then 128.24.

Monday's liquidity report showed Friday's excess liquidity fell to €1.7652T from €1.7655T and use of the marginal lending facility fell to €102M from €109M.

Corporate issuance saw $5.5B come to market via 8 issuers headlined by Bunge Limited Finance Corp $1B 2-part senior unsecured note offering and Expedia $1B 10-year senior unsecured note offering

Looking Ahead

(FI) Finland's Government meeting on 2018 Budget

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

05:30 (UK) DMO to sell 1.5% Conventional July 2047 Gilts

06:00 (IL) Israel July Manufacturing Production M/M: No est v 1.9% prior

06:00 (IL) Israel Aug Unemployment Rate: No est v 4.1% prior

06:30 (EU) ESM to sell 6-Month Bills

07:45 (US) Weekly Goldman Economist Chain Store Sales

07:45 (UK) BOE Financial Policy Committee (FPC) Kohn

08:00 (HU) Hungary Central Bank (NBH) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.90%

8:00 (PL) Poland Aug Sold Industrial Output M/M: +3.2%e v -8.5% prior; Y/Y: 5.9% e v 6.2% prior, Construction Output Y/Y: 24.0%e v 19.8% prior

08:00 (PL) Poland Aug Retail Sales M/M: 0.7%e v 0.6% prior; Y/Y: 7.1%e v 7.1% prior, Real Retail Sales Y/Y: 6.7%e v 6.8% prior

08:00 (PL) Poland Aug PPI M/M: 0.4%e v 0.3% prior; Y/Y: 2.9%e v 2.2% prior

08:30 (US) Aug Housing Starts: 1.174Me v 1.16M prior; Building Permits: 1.22Me v1.230M prior (revised from 1.223M)

08:30 (US) Q2 Current Account: -$116.0Be v -$116.8B prior

08:30 (US) Aug Import Price Index M/M: 0.4%e v 0.1% prior; Y/Y: 2.2%e v 1.5% prior; Import Price Index ex Petroleum M/M: 0.2%e v 0.0% prior

08:30 (US) Aug Export Price Index M/M: 0.2%e v 0.4% prior; Y/Y: No est v 0.8% prior

08:30 (CA) Canada July Manufacturing Sales M/M: -1.9%e v -1.8% prior

08:55 (US) Weekly Redbook Sales - 09:00 (BE) Belgium Sept Consumer Confidence: No est v 2 prior

09:00 (EU) Weekly ECB Forex Reserves

09:00 (RU) Russia Aug Unemployment Rate: 5.1%e v 5.1% prior, Real Disposable Income: 0.0%e v -0.9% prior, Real Wages Y/Y: 3.8%e v 4.6% prior

09:00 (RU) Russia Aug Real Retail Sales M/M: 3.1%e v 3.8% prior; Y/Y: 1.1%e v 1.0% prior

09:00 (HU) Hungary Central Bank Gov Matolcsy post rate decision statement

09:00 (RU) Russia announces weekly OFZ bond auction

09:50 (UK) BOE to buy £1.125B in in APF Gilt purchase operation (over 15 years)

11:00 (BR) Brazil to sell I/L 2022, 2026, 2035 and 2055 Bonds

11:30 (US) Treasury to sell 4-Week Bills

16:30 (US) Weekly API Oil Inventories

CRUDE OIL Consolidating Around 50

Crude oil is pausing around the $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance found at 50.43 (31/07/2017) has been broken. Expected to show another leg higher.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Breaking Uptrend Channel

Silver has reversed and has broken uptrend channel by breaking support implied by its lower bound. Strong resistance is given at 18.65 (17/04/2017 high) while support can be found at 16.58 (15/08/2017 high). Expected to show further bearish move.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

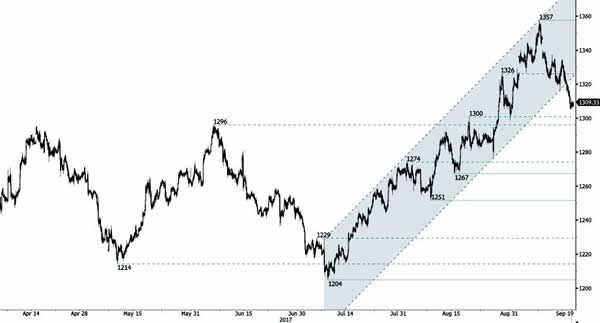

GOLD Weakening

Gold is trading lower and has exited uptrend channel. Hourly support given at 1315 (14/09/2017 low) has been broken. Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show further bearish move.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Bouncing Sharply

Bitcoin has taken a dive after strong interest over the summer. The digital currency has set up a new support at 2975 (22/08/2017 low). Key resistance can be located at 4921 (01/09/2017 high). The road is wide open for further shortterm decline.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Monitoring Resistance At 1.1538

EUR/CHF's buying pressures are going up and the pair has broken resistance area between 1.1356 and 1.1472. The pair is now monitoring resistance at 1.1538 (04/08/2017 high).

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Strong Decline

EUR/GBP is trading lower. However, as long as prices remain below the resistance at 0.9176 (declining trendline), the short-term technical structure is biased to the downside. Hourly support is given at 0.8982 (12/09/2017). Strong resistance lies at 0.9306 (29/07/2017 high).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Bouncing On Lower Bound Of Uptrend Channel

AUD/USD is bouncing higher below 0.8000. Hourly resistance is given at 0.8125 (08/09/2017 high). Hourly support below 0.7950 (former uptrend channel). Expected to further weaken.

In the long-term, the trend is largely negative since 2011. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.