Sample Category Title

Before & After the Hurricanes

Hurricanes will get the bulk of the blame but the latest data showed growth was slowing before Harvey and Irma. A big week ahead: Trump's UN speech on Tuesday; Fed decision & Yellen presser on Wednesday; PM Theresa May's EU speech on Friday and German Elections on Sunday. A new Premium note has been added to further our existing index trade.

A cascade of growth downgrades followed US retail sales and industrial production numbers on Friday. Retail sales fell 0.2% compared to +0.1% expected in August. The control group, which excludes autos, gas and building supplies was down 0.2% compared to +0.2% expected. In addition, July sales were revised lower.

It wasn't just consumers with bad news. August industrial production fell 0.9% compared to +0.1% expected in the worst monthly decline in five years. The Fed said Harvey reduced output by 0.75 pp so it's not as bad as it looks, but it's undoubtedly a poor reading. How poor? The NY Fed and Atlanta Fed GDP trackers were both lowered by 0.8 pp for Q3 while Q4 estimates were trimmed as well.

The market took the weak data in stride in a sign that it views Harvey as the culprit. That may be a hint on how buoyant the dollar will be in the week ahead as the market prepares for details of Trump's tax plan at the end of the month.

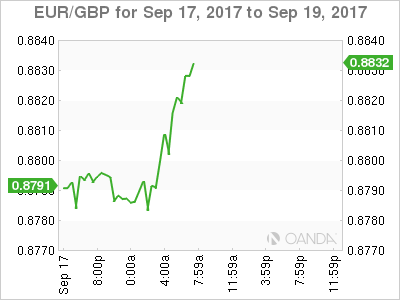

What was unambiguous was pound strength as cable finished the week just under 1.36. The OIS market is pricing in a 65% chance of a BOE hike on Nov 2 and 73% before year-end. What makes that probability even higher is that Carney's credibility can't afford another misstep.

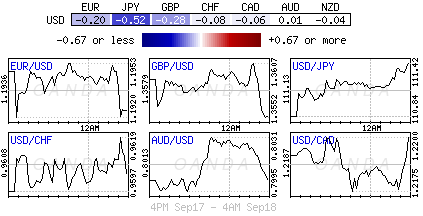

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

- EUR +86K vs +96K prior

- GBP -46K vs -54K prior

- JPY -57K vs -74K prior

- CHF -2K vs -2K prior

- CAD +50K vs +54K prior

- AUD +60K vs +65K prior

- NZD +12K vs +15K prior

Those sterling shorts are suddenly rather vulnerable and no doubt many covered since the Bank of England decision. Watch out for Carney's speech today at 11 am EST (4 pm London). Euro shorts were pared after last week hitting the most-extreme since May 2011.

Market Update – Asian Session: Quiet Start To Week

Notes/Observations

ECB sees inflation rate below 1% in early 2018 citing a statistical quirk

Overnight

Asia:

Japan PM Abe: To decide on dissolving Diet and election after current US visit (**Note: Earlier reports circulated that PM Abe was considering snap election as soon as Oct)

UN Sec Council statement (from Friday) condemned 'highly provocative' North Korean missile launch

US Ambassador to UN Haley: UN Security Council may run out of options with regard to North Korea. Iran, Syria and North Korea will be major focus at UN Gen Assembly next week

US Sec of State Tillerson: increasingly aggressive North Korean threatens the region and endangers the world

North Korea said to be aiming to establish "military equilibrium" with US; "will make the US rulers dare not talk about military option"

Europe:

ECB's Praet (Belgium): Reiterates Council view that euro zone still needs substantial stimulus to get back to the near 2% inflation target; will also respond if inflation were to get too high

ECB reportedly estimates 2018 QE reinvestment average at €15B/month (**Reminder: current QE program of €60B/month in bond purchases is expected to be wound down during 2018)

Bank for International Settlements (BIS) Quarterly Review: Strong outlook with low inflation spurs risk-taking

Forza Italia party chief Berlusconi (former PM) lays policy priorities in marking a formal return to Italy's political stage

Foreign Sec Johnson laid out his vision for Brexit; believes it can still deliver £350M a week extra for the NHS (**Note: Various cabinet colleagues accuse Johnson of "backseat driving" on Brexit)

UK Interior Sec Rudd: Johnson was not starting a leadership bid by setting out his plans for Brexit in a newspaper article, adding that his intervention was "absolutely fine"

Sovereign rating actions from Friday:

S&P raised Portugal sovereign rating to investment grade, raises one notch to BBB- from BB+; outlook Stable

Moody's raised Ireland's sovereign rating to A2 from A3; outlook revised to Stable from Positive

S&P affirmed Cyprus sovereign rating at BB+; outlook revised to Positive from Stable

S&P affirmed Russia sovereign rating at BB+; outlook Positive

S&P affirmed Austria and Finland sovereign ratings at AA+; outlook Stable

Economic data

(AT) Austria Aug CPI M/M: -0.1% v -0.3% prior; Y/Y: 2.1% v 2.0% prior

(CZ) Czech Aug PPI Industrial M/M: 0.2% v 0.1%e; Y/Y: 1.4% v 1.3%e

(HK) Hong Kong Aug Unemployment Rate: 3.1% v 3.1%e

(EU) Euro Zone Aug CPI M/M: 0.3% v 0.3%e; Y/Y (final reading): 1.5% v 1.5%e; CPI Core (final reading) Y/Y: 1.2% v 1.2%e

Fixed Income Issuance:

(NO) Norway sold total NOK6.0B vs. NOK6.0B indicated in 12-month Bills; Avg Yield 0.39% v 0.41% prior; Bid-to-cover x v 2.42x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.5% at 382.5, FTSE +0.3% at 7235, DAX +0.6% at 12591, CAC-40 +0.4% at 5235, IBEX-35 +0.7% at 10391, FTSE MIB +0.7% at 22381, SMI +0.4% at 9061, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices start the week of on the front foot continuing the momentum from the end of last week, with the dollar reach an 8 week high against the yen ahead of the FOMC rate decision mid week. On the corporate front Fingerprint cards continue to fall after guiding Q3 Rev short of expectations, whilst Ryanair trades lower after cancelling over 150 flights after 'Messing up' Pilot holidays. Elsewhere Petra Diamonds trade sharply lower after prelim results, whilst in the healthcare space Thrombogenics trade higher after regaining rights to JETREA.

Equities

Consumer discretionary [(Ryanair [RYA.UK] -3.4% (Flight cancellations)]

Materials: [Petra diamonds [PDL.UK] -8.6% (Prelim FY17 results)]

Financials: [Esure [ESUR.UK] +6.8% (Controlling shareholder mulling sale), Hiscox [HSX.UK] -2% (Hurricane Harvey claims estimates)]

Technology: [Fingerprint Cards -22% (FINGB.SE] -21% (Q3 guidance)]

Telecom: [Nokia [NOKIA.FI] +1.2% (Received decision in patent license arbitration with LG Elec)]

Healthcare: [Thrombogenics [THR.BE] +17.5% (Regains global rights to JETREA (ocriplasmin))]

Energy: [Seabird Exploration [SBX.NO] -59% (Private placement)]

Speakers

ECB noted that base effect seen affecting inflation in coming quarters. Combined impact of base effects from the energy and unprocessed food HICP components will lower headline inflation in the first quarter of 2018, but raise it in the following quarter. September staff projections foresaw a V-shaped path for headline inflation

ECB's Hansson (Estonia): ECB steps could involve new refinancing operations, reworked guidance and more details on reinvestments

France Budget Min Darmanin: 2017 GDP growth seen at 1.7% vs. 1.5% official govt target

Spain Fin Min de Guindos: No market impact from any instability resulting in Catalonia region. Companies were leaving Catalonia due to high taxes. Unemployment is falling faster than govt projections as domestic economy was growing over 3%

Italy Fin Min Podoan: Domestic banks efficiency has improved due to govt measures; NPLs were falling at a faster rate. Pubic backstop and deposit insurance is needed for EU banking union

Greece PM Tsipras: Optimistic to see above target primary surplus in 2017. Country needed to complete 3rd bailout review asap despite technical and political difficulties. Aiming to complete prior actions by November

China PBOC Adviser Sheng Songcheng: Now is not the time to change the CNY currency (Yuan) regime

China PBoC said to be working on draft proposal for foreign access to financial sector

China FX Regulator SAFE reiterated view that CNY currency (Yuan) exchange rate was stable even with recent FX appreciation

Currencies

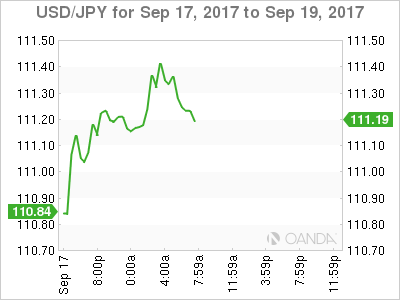

USD/JPY was at a 2-month high with the pair above 111.30 ahead of the NY Morning. Dealers were eyeing the upcoming FOMC policy meeting mid-week meeting for clues on whether interest rates could rise again by year-end

EUR/USD was little changed at 1.1940 area with dealers seeing little impetus for movement before Wednesday's Fed policy meeting

Yields on 10-year Portuguese government bonds drop faster than their euro zone counterparts early Monday after the sovereign's upgrade to BBB-, an investment-grade rating, by S&P after the close Friday

Fixed Income

Bund futures trade little changed at 161.37 as investors await a number of speeches by European and U.K. central bankers this week, as well as the US Federal Reserve's meeting. Continued downside targets 161.03 while upside resistance stands initially at 162.07, followed by 163.27.

Gilt futures trade at 125.42 up 12 ticks with little in the way of UK economic data, Gilts will take their lead from the performance of core European government bonds.. Continued downside eyeing 124.91. Upside targets 127.90 then 128.24.

Monday's liquidity report showed Friday's excess liquidity fell to €1.7655T from €1.7660T and use of the marginal lending facility fell to €109M from €115M.

Corporate issuance saw $42.8B last week via 66 tranches, bringing YTD issuance to above $1.03T. For the week ahead analysts forecast around $25B to come to market. In Euro denominated issuance ~€35B came to market via 39 issuers and 49 tranches

Looking Ahead

(UR) Ukraine Q2 Final GDP Q/Q: 0.6%e v 0.6%prelim; Y/Y: 2.4%e v 2.4%

05:30 (BE) Belgium Debt Agency (BDA) to sell €3.5B in 2024, 2027 and 2034 OLO Bonds

05:30 (NL) Netherlands Debt Agency (DSTA) to sell €2.0-4.0B in 3-Month and 6-month Bills

06:00 (PT) Portugal Aug PPI M/M: No est v -0.3% prior; Y/Y: No est v 2.2% prior

06:45 (US) Daily Libor Fixing - 07:00 (IN) India announces details of upcoming bond sale (held on Fridays)

07:00 (BR) Brazil Sept IGP-M Inflation (2nd Preview): 0.4%e v 0.3% prior

07:25 (BR) Brazil Central Bank Weekly Economists Survey

08:00 (PL) Poland Aug Employment M/M: 0.1%e v 0.3% prior; Y/Y: 4.6%e v 4.5% prior

08:00 (PL) Poland Aug Average Gross Wages M/M: -1.1%e v -0.1% prior; Y/Y: 5.7%e v 4.9% prior

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada July Int'l Securities Transactions (CAD): No est v -0.9B prior

08:30 (CH) Swiss Government question time in Parliament

09:00 (FR) France Debt Agency (AFT) to sell combined €4.0-5.2B in 3-month, 6-month and 12-month Bills

09:30 (EU) ECB announces Covered-Bond Purchases - 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

09:50 (UK) BOE to buy £1.125B in in APF Gilt purchase operation (3-7 years)

10:00 (US) Sept NAHB Housing Market Index: 67e v 68 prior

10:30 (DE) ECB's Lautenschlaeger (Germany) in Basel

11:00 (UK) BOE Gov Carney at IMF in Washington DC

11:00 (CO) Colombia July Trade Balance: -$0.6Be v -$0.1B prior

11:30 (US) Treasury to sell 3-month and 6-month bills

14:15 (DE) SPD's Schulz takes questions at Televised Town-Hall Event in Luebeck

14:15 (CA) Bank of Canada (BOC) Dep Gov Lane

16:00 (US) July Total Net TIC flows: No est v $7.7B prior; Net Long-Term Tic Flows: No est v $34.4B prior

16:00 (US) Weekly Crop Progress Report

Dollar To Remain Contained Ahead Of Fed Decision

September 18: Five things the markets are talking about

This is a busy week both on the central bank and parliamentary election front.

Among the G7, the Bank of Japan (Thursday) and the Fed (Wednesday) hold policy meetings this week, as to does Norway’s Norges Bank (Thursday).

The BoJ is expected to leave its policy unchanged and probably will not reveal when it will unwind stimulus, but could signal determination to keep the yield curve under control.

However, for the Fed, expectations are uncertain. Recent hurricane activity is expected to cloud the outlook for the Fed – intensifying the problem is the delay in the collection and publication of official data. Expectations are for revisions going forward. Interest rates are expected to remain on hold, while the market assigns a +50% probability of a December rate increase. Many anticipate the FOMC to begin reducing the Fed’s balance sheet.

In the U.K, Brexit strategy is in focus as PM May prepares to outline her revised approach this Friday, while in Germany, the final days of the federal parliamentary campaign will play out before next Sunday’s vote (Sept. 24). Down-under, New Zealand goes to the polls this Saturday (Sept. 23).

1. Stocks given the green light

The bullish sentiment that stoked more records stateside on Friday has carried through into the new week, with both European and Asian rallying across the board.

In Japan capital markets were shut for respect-for-the-aged day.

In Hong Kong, equities jumped to the highest a 27-month overnight, as regional bourses hit decade highs, while stronger-than-expected Chinese loan data aided sentiment. The Hang Seng index rose +1.3%, while the China Enterprises Index gained +1.2%.

Down-under, and Australia’s S&P 200 was up +0.5% at the close, while in S. Korea, the Kospi index climbed +1.4%.

In China, equities were boosted by stronger domestic data that added to views that economic growth is holding up and by the loosening of margin requirements on stock index futures trading. The blue-chip CSI300 index rose +0.3%, while the Shanghai Composite Index also added +0.3%.

In Europe, regional bourses all start the week on the front foot, continuing Friday’s momentum as the U.S dollar reaches a two-month high outright against the yen (¥111.40).

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx600 +0.5% at 382.5, FTSE +0.3% at 7235, DAX +0.6% at 12591, CAC-40 +0.4% at 5235, IBEX-35 +0.7% at 10391, FTSE MIB +0.7% at 22381, SMI +0.4% at 9061, S&P 500 Futures +0.2%

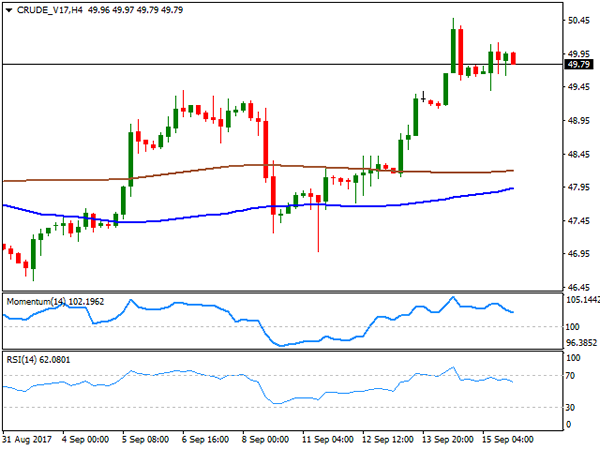

2. Oil bid on rising refinery demand, falling rig count, and gold lower

Ahead of the U.S open, crude oil prices remain better bid, trading atop of multi-month highs as the number of U.S rigs drilling for new production fell and refineries continued to restart after getting knocked out by Hurricane Harvey.

Brent crude futures are at +$55.91 a barrel, up +29c, straddling their five-month high print touched last Thursday, while U.S West Texas Intermediate (WTI) crude is trading up +41c, or +0.8%, at +$50.30, near their three-month high print also reached last Thursday.

Note: Oil refineries across the Gulf of Mexico and the Caribbean are also restarting after being shut due to hurricanes Harvey and Irma.

Also supporting crude prices is the number of rigs drilling for oil in the U.S fell sharply last week. Friday’s Baker Hughes report revealed that U.S energy firms cut seven oilrigs in the week to Sept. 15, bringing the total to 749, the fewest since June.

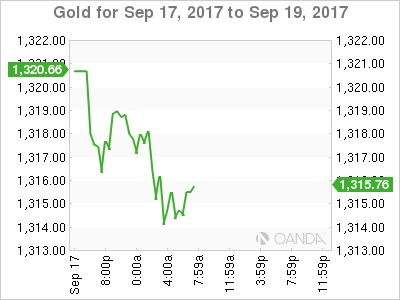

In the Euro session, gold has slipped to its lowest level in a fortnight as the dollar and stocks rally, while prospects of U.S monetary policy tightening ahead of a Fed meeting is also weighing on the metal. The ‘yellow’ metal is down -0.3% at +$1,315.36 an ounce.

3. Sovereign yields rise

This week, the main event will be the Federal Open Market Committee (FOMC) meeting, starting tomorrow and concluding with Wednesday’s press conference (02:30 pm EDT).

U.S policy makers are expected to take another step towards policy “normalisation,” but will it be this week? It’s not a slam-dunk, as persistently subdued global inflation, despite a pick-up in growth, remains somewhat of an impediment to tightening monetary policy. As such, the market is not wholly convinced that the Fed will move on rates again this year, with a December change put at less than a +50% probability.

The yield on 10-year Treasuries has backed up +1 bps to +2.21%, the highest yield in almost four-weeks. In Germany, the 10-year Bund yield has gained less than +1 bps to +0.44%, the highest in more than a month, while Britain’s 10-year Gilt yield has climbed less than +1 bps to +1.31% – the highest print in more than 10-weeks.

4. Dollar to remain contained ahead of Fed decision

Last week’s positive U.S inflation surprise was not sufficient to convince the market of a noteworthy continuation of the Fed rate hike cycle. Investor focus now shifts to the Fed directly.

The U.S dollar is unlikely to move much before Wednesday’s Fed announcement as is usual in the run-up to these meetings. With rates expected to remain on hold should not mean much for the dollar unless there is a ‘hawkish’ signal from this week’s Fed meet.

Ahead of the open, the dollar is a tad firmer across the board. EUR/USD at €1.1931 is down -0.16%, USD/JPY is up +0.5% at ¥111.40, while GBP/USD down 0.3% at £1.3554.

Note: Sterling is down after rallying on Thursday and Friday as caution sets in before a speech by BoE Governor Mark Carney at 10:00 am EDT.

Note: JPY outright is trading atop of its two-month lows as investors are shaking off risk fears of political threats, but also because there is a public holiday in Japan, which means less liquidity in the market.

5. Euro annual inflation up to +1.5%

Data this morning from Eurostat showed that Euro area (monetary union of 19 members) annual inflation was +1.5% in August 2017, up from +1.3% in July 2017. In August 2016 the rate was +0.2%.

European Union (28 member states) annual inflation was +1.7% in August 2017, up from +1.5% in July. A year earlier the rate was +0.3%.

Note: ECB President Draghi indicated earlier this month that the bank would outline plans next month to scale down its +€2.3T bond-buying program (QE).

Euro Continues To Drift As Eurozone CPI Matches Forecast

The euro ended the week quietly, and the lack of activity continues in the Monday session. Currently, the pair is trading at 1.1941, up 0.27% on the day. On the release front, Eurozone Final CPI improved to 1.5%, matching the forecast. There are no major US events on the schedule. On Tuesday, Germany releases ZEW Economic Sentiment and the US publishes Building Permits and Housing Starts.

Eurozone economic conditions have been solid in 2017, but inflation levels have been stubbornly low. This has complicated the ECB’s plans to reduce its quantitative easing scheme (QE), although ECB President Mario Draghi has said that the ECB will announce its plans to reduce QE at the October policy meeting. QE is scheduled to end in December, and policymakers will have to balance opposing interests as to what happens next. Germany, with its robust economy, would like to remove stimulus entirely, while less affluent eurozone members want to retain an accommodative monetary policy. We’re likely to see some compromise, in which stimulus is extended into 2018, but will be tapered from its current level of EUR 60 billion/month.

Germany head for the polls on September 24, and Angela Merkel is widely expected to win her fourth term as prime minister. French President Emmanuel Macron, a staunch supporter of a unified Europe, is hoping to work with Merkel and reform the eurozone. Macron’s proposal includes a eurozone finance minister who would be in charge of a eurozone budget. Macron’s call for greater cooperation is linked to Britain’s exit from the EU, which could lead to divisions among the remaining 27 members in the bloc. However, the French ambitious plan will need Germany’s support before it can become a reality. Will Germany embrace the idea? Angela Merkel’s has indicated that she is open to the idea, but Jean-Claude Juckner, head of the European Commission, came out against the plan last week. Juckner said he favored a finance minister for the EU but was against a separate eurozone budget and finance minister. Even if the plan is not adopted, we can expect a Macron-Merkel alliance to take steps which will strengthen Franco-German ties and further unify the eurozone.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1933

The recent rise has been capped at 1.2000 interim resistance, but the pullback is corrective in nature, so my intraday outlook is positive, for a spike towards 1.2070 area. Crucial on the downside is 1.1830 and only a break through that area will challenge 1.1660 and 1.1480.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2000 | 1.2160 | 1.1900 | 1.1830 |

| 1.2070 | 1.2500 | 1.1830 | 1.1660 |

USD/JPY

Current level - 111.31

The uptrend has been renewed, heading towards 112.80 hurdle. Initial support lies at 110.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.00 | 111.00 | 110.30 | 108.12 |

| 112.80 | 112.80 | 109.20 | 107.30 |

GBP/USD

Current level - 1.3550

The acceleration of the uptrend led to test of 1.3635 resistance area and current pullback should be considered corrective, preceding another leg towards 1.3830 area. Key support is projected at 1.3440.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3635 | 1.3635 | 1.3530 | 1.3340 |

| 1.3830 | 1.3830 | 1.3440 | 1.3150 |

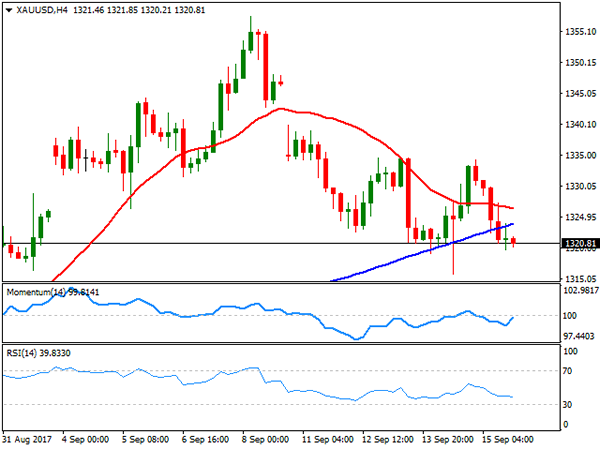

Technical Outlook: SPOT GOLD – Bears May Extend To Fibo 38.2% Support At $1300

Spot Gold remains in red at the beginning of the week with extended weakness probing below strong supports at $1317 (bull-channel support line / Fibo 38.2% of $1251/$1357 upleg.

Fresh bears hit session low at $1312 (daily Kijun-sen) which may act as temporary footstep for near-term consolidation, signaled by oversold slow stochastic on daily chart.

Upside attempts are expected to be limited (broken 20SMA at $1319 to ideally cap) before bears resume.

Close below bull-channel support line will initial bearish signal, while close below daily Kijun-sen is needed to confirm bearish continuation, which could extend to $1300 (Fibo 38.2% of $1204/$1357 ascend).

Alternative scenario requires firm break above last week's tops at $1334, reinforced by south-turning daily Tenkan-sen, to turn near-term bias higher.

Res: 1319, 1327, 1331, 1340

Sup: 1312, 1304, 1300, 1292

FOMC To Focus On Data | Three Reasons For Sterling Strength | ECB Ready

Rift in hard and soft economy data

Sterling Bullish Due to Three Main Reasons

ECB Ready

Rift in hard and soft economy data

- Retail sales below forecast and downward revision

- Industrial production underwhelming

- Empire state and Michigan guiding you towards a ditch

The rift continues between the soft data and hard data over in the US. Last week, we have seen more evidence of this in the economic numbers and it is about time for the Fed to start paying attention to this. They are going to embark on the process of unwinding their balance sheet and at the same time continue their glide path to normalise the interest rate.

The hard economic numbers have been coming in underwhelming since April. Last week's industrial and retail sales number reminded the markets of the same message. If you look at the Empire State Manufacturing and the university of Michigan Consumer Sentiment numbers, it tells you that the soft data is navigating investors towards a ditch. What is important to keep in mind is that your hard data is something which is the engine that drives the economic growth.

Fed's Plan For Four More Interest Rate Hikes To Face Serious Headwinds

- The economic growth is going to remain sluggish

- Catastrophes caused from the hurricanes are becoming prominent in the economic data; the US factory output declined in August due to the curtailing of the refinery operations and chemical production

- The US consumer sentiment dipped as investors have shown their anxieties growing due to the hurricane

- The Atlanta Fed's GDPNow index has reduced its economic growth target for the third quarter from 2.29% to s.s25%

- The New York Fed's GDP forecast has taken the same route, and he expect the GDP to grow at 1.34% a much lower number from the previous reading of 0.3%

Sterling Bullish Due to Three Main Reasons

- The BoE may increase interest rate; the dovish voters are turning hawkish- November meeting could be a live meeting

- The Dollar weakness is a factor

- The Sterling weakness improved trade balance and has hence an effect on the economy

The critical aspect due to which we do not support the strength in the sterling is that the Brexit negotiations are heavily ignored. We have literally no progress and the negotiations process is chocking itself.

The weakness in the consumer spending is largely being ignored. The wage growth is abate and rising inflation is making consumers to tighten their belt even further which is a recipe for a disaster.

ECB Ready

The ECB is expected to make an announcement this week about reinvesting an average of 15 billion euros a month from maturing debt holdings. This would have a twofold impact; firstly, it would soften the blow on the Eurozone's economic growth when the ECB will start its monetary policy tapering process. And finally, it would send a clear signal for the euro traders that the tapering process is going to become reality now and that could see more upward movement for the euro-dollar pair.

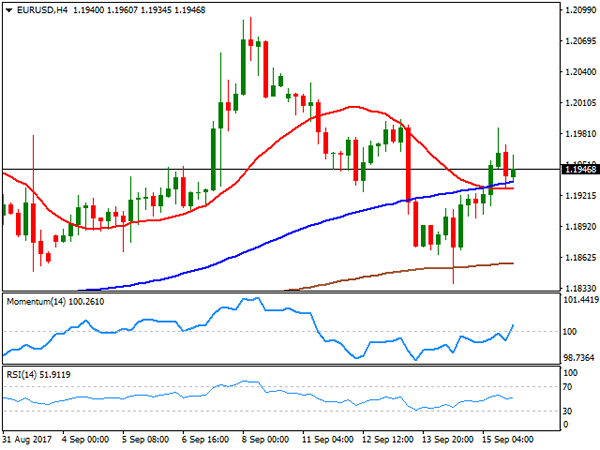

Technical Outlook: EURUSD – N/T Action Remains Between Daily Kijun-Sen / Tenkan-Sen Boundaries

The Euro ticked higher on Monday after inflation in the Eurozone hit the highest in four month.

Annualized CPI came at 1.5% in Aug, meeting the forecast while m/m release came at 0.3%, along with forecast but well above previous month's -0.5% release.

The pair remains entrenched between daily Kijun-sen (1.1877) and daily Tenkan-sen line (1.1964) which was dented on Friday but without clear break higher.

Today's price action is so far holding between 20SMA (1.1914) and 10SMA (1.1949), looking for initial signal on break of either boundary.

However, break of either wider range boundaries (Tenkan-sen / Kijun-sen) would provide clearer direction signals.

Studies on daily chart remain bullishly aligned but reversal signal is generating on weekly chart as overbought RSI is turning.

Violation of daily Kijun-sen (1.1877) and rising weekly 10SMA (1.1850) would be seen as firmer signal of deeper correction.

Alternatively, lift above daily Tenkan-sen (1.1964) and psychological 1.2000 barrier would generate stronger bullish signal.

Res: 1.1949, 1.1964, 1.2000, 1.2029

Sup: 1.1914, 1.1877, 1.1850, 1.1837

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

Despite advancing for a second consecutive day on Friday, the EUR/USD pair closed the week in the red at 1.1946. Friday's advance was backed by soft US data, as August Retail Sales fell by 0.2% from a month earlier, which additionally suffered downside revisions. In the same month, Industrial Production fell by 0.9% while Capacity Utilization edged lower, to 76.1%. The pair eased from Friday's high at the end of the day, as the Michigan consumer sentiment index for September beat expectations, coming in at 95.3, still below August reading of 96.8.

All through the week, attempts to regain the 1.2000 level failed, rather on upward exhaustion than on self dollar's strength. The greenback can't find its way higher, although some light have appeared at the end of the tunnel, as mid-week, the Trump administration hinted it will start working on the tax reform before the month end. Wall Street rallied to record highs on the news, but the dollar remained subdued. Anyway, the market is now focused on the upcoming Fed's monetary policy decision this Wednesday. The Central Bank is expected to keep rates unchanged, but also to announce details on their plan to reduce the balance sheet. Additionally, the dot-plot will give some hints on how policymakers are positioned towards next rate hikes.

The pair consolidated near 2017 highs for a second consecutive week, settling above a bullish 20 DMA in the daily chart, and with technical indicators having regained the upside, limiting the risk of a deeper correction ahead that anyway will depend on market's reaction to Fed's decision. A long term ascendant trend line coming from April this year stands for this Monday around 1.1825, whilst August 31st low comes at 1.1822, making of the region a key support for the upcoming days, as below it, the pair could extend its slide down to 1.1667, the low set on August 17th. Short term, the 4 hours chart shows that the price has managed to recover above its 20 and 100 SMAs that anyway converge within a tight range, around 1.1910, whilst technical indicators have reentered positive territory by the end of the week, but lack enough momentum to support a new leg north.

Support levels: 1.1920 1.1860 1.1825

Resistance levels: 1.1965 1.2000 1.2045

USD/JPY

The USD/JPY pair had a rough week, but closed at its highest since late July, at 110.82, quickly reverting a slide down to 109.54 late Thursday, the result of another missile test from North Korea which spurred demand for safe-haven assets. However, the market is paying less attention to this kind of events lately, and the pair quickly recovered its previous upward strength. Also, the negative sentiment was offset by US Treasury yields which traded steady around their previous daily closes. The yield on the benchmark 10-year Treasury note stood at 2.20%, while the yield on the 30-year Treasury bond ticked lower to 2.77% from previous 2.78%. The pair posted a 7-week high on Friday of 111.33, but the daily chart shows that it was unable to sustain gains beyond the 100 DMA, settling around it. Furthermore, the same chart shows that the 200 DMA comes at 111.50, the level to break for a following bullish extension. The daily Momentum heads nowhere around its 100 level, but the RSI aims higher around 57, leaning the scale towards the upside. In the 4 hours chart, technical indicators present clear bearish divergences form price action, posting lower lows as the price advances since mid week, but still above their mid-lines, which limits the case for a steeper downward move. The 100 SMA in this last time frame aims modestly higher, still below the 200 SMA, both over 100 pips below the current level.

Support levels: 110.25 109.70 109.35

Resistance levels: 111. 05 111.50 111.90

GBP/USD

The GBP/USD pair surged to its highest since the Brexit vote back in June last year, hitting 1.3615 and settling not far below it, as hawkish surprises kept coming from MPC members. Following BOE monetary policy announcements on Thursday, in which most policymakers agreed that some withdrawal of monetary stimulus is likely to be appropriate over the coming months, MPC Vlieghe, a well-known dove said on Friday that a rate hike is possible for the coming months, and that more than one hike could be needed. The pair soared with the news, accumulating roughly 470 pips in the last two days of the week, and remained bid after disappointing US macroeconomic figures. Further gains seem likely now that the market is pricing in a rate hike for November, but a downward correction, or at least some consolidation could be expected at the beginning of the week. Technically, daily indicators maintain their strong bullish momentum, despite being in overbought territory, whilst the 20 DMA turned sharply north far below the current level, all of which supports an expected continuation. In the 4 hours chart, technical indicators also head higher within extreme overbought territory as the price develops well above a bullish 20 SMA, this last some 250 pips below the current level.

Support levels: 1.3560 1.3525 1.3480

Resistance levels: 1.3615 1.3650 1.3690

GOLD

Spot gold posted its lowest settlement for this September on Friday, closing at $1,320.81 a troy ounce, sharply down for the week, undermined by increasing demand for riskier assets, as Wall Street rallied to record highs. Gold prices spiked late Thursday on news North Korea performed another missile test that landed in the Japanese sea, but changed course after London's opening. One reason of gold's decline is the upcoming Fed meeting, as despite chances of a rate hike are pretty much null, market expects a hawkish bias through definitions on the reduction of the balance sheet. Technically, the daily chart shows that the price settled slightly below a bullish 20 SMA, whilst technical indicators head sharply lower, dangerously close to their mid-lines, suggesting a bearish extension could be seen on a break below 1.1315,72, the weekly low and the immediate support. In the 4 hours chart, the price settled below its 20 and 100 SMAs, whilst technical indicators hold within bearish territory, also favoring a new leg lower ahead.

Support levels: 1,315.70 1,308.10 1,298.90

Resistance levels: 1,323.95 1,330.40 1,337.80

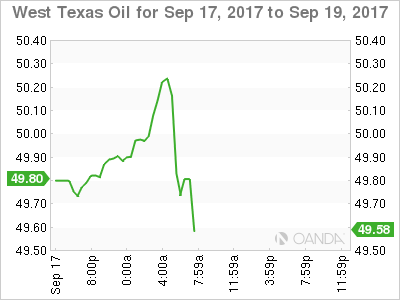

WTI CRUDE OIL

West Texas Intermediate crude futures ended Friday at $49.79 a barrel marginally higher on the day, but sharply up for the week, on a series of positive market news. Mid week, the International Energy Agency said that oil's glut was shrinking amid strong demand from Europe and the US, coupled with production declines from OPEC. Additionally, the OPEC's forecast indicated an expected increase in demand for 2018. On Friday, the US Baker Hughes report added to the bullish case, after reporting that active rigs drilling for oil fell by 7 the past week, down to 749 from previous 756. The commodity failed to regain the 50.00 mark earlier on the week, but seems poised to rally beyond it, given that in the daily chart, the price held firmly above its 100 and 200 SMAs, whilst technical indicators maintain their upward strength within positive territory. Shorter term, and according to the 4 hours chart, oil may correct lower, as technical indicators are retreating from overbought levels, whilst despite far below the current level, moving averages remain horizontal. In the case of further gains, WTI has a critical resistance around 52.00, and advances up to this last could trigger some strong profit taking, pushing prices down towards the 45.00 price zone.

Support levels: 49.40 48.80 48.25

Resistance levels: 49.90 50.50 51.20

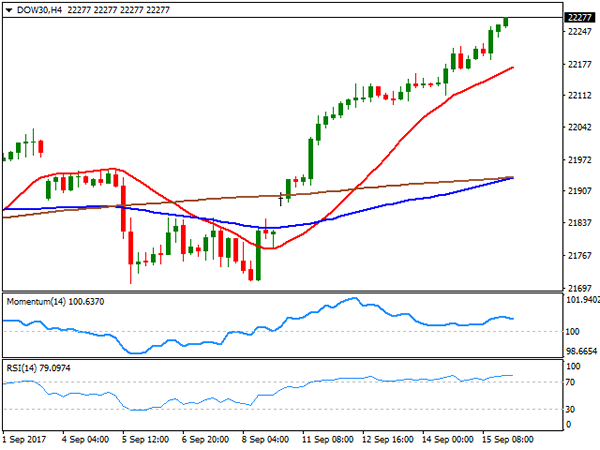

DJIA

US major indexes closed with gains and at record highs on Friday, backed by solid earnings reports and hopes that the so-long promised US tax reform stands around the corner. The tech sector was the best performer on Friday, with the three major indexes ending the week up over 1.0%. On Friday, the DJIA added 64 points to 22,268.34, the Nasdaq Composite gained 0.30% to 6,448.47, while the S&P advanced 4 points, to 2,500.23. Boeing was the best performer within the DJIA, up 1.54%, while General Electric led decliners with a 1.36% loss. The daily chart shows that technical indicators resumed their advances after a short-lived period of consolidation, entering overbought territory as the index moves further above all of its moving averages, supporting further gains ahead. In the 4 hours chart, technical indicators present modest bearish divergences, with the RSI consolidating around 79 and the Momentum within positive territory, despite the index keeps posting higher highs, a first sign of warning over a possible downward corrective movement, whilst the benchmark remains far above all of its moving averages, with the 20 SMA providing an immediate support at 22,172.

Support levels: 22,236 22,196 22,162

Resistance levels: 22,300 22,345 22,390

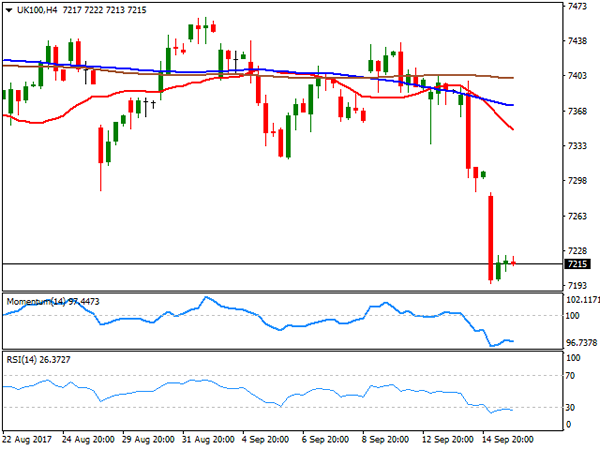

FTSE100

FTSE 100's decline continued on Friday, with the index finishing the week at levels last seen in April, down on Friday 79 points or 1.10%, to 7,215.47. Strength in the Pound, which rallied to its highest since the Brexit referendum outcome late June 2016, weighed on the index, as most companies listed make the most of their gains abroad. Only 17 members managed to gain ground, led by Imperial Brands that added 2.05%, and followed by ITV which gained 1.41%. Carnival, on the other hand, was the worst performer, down 6.22%, followed by Provident Financial that shed 4.28%. The index heads into the next weekly opening with a strong bearish momentum according to technical readings in the daily chart, as technical indicators maintain their sharp bearish slopes, nearing oversold territory, whilst the 20 DMA is finally detaching from the 100 DMA, both anyway far above the current level. In the 4 hours chart, technical readings also favor a new leg lower ahead, as technical indicators resumed their declines within oversold territory, and after a limited upward corrective movement, whilst the index has settled far below all of its moving averages.

Support levels: 7,197 7,158 7,120

Resistance levels: 7,225 7,264 7,301

DAX

The German DAX lost 21 points to 12,518.81 on Friday, as European indexes were dragged lower by a plummeting FTSE which suffered from a wild Pound's appreciation. Nevertheless, the index ended the week with strong gains, as risk sentiment receded at the beginning of the week, whilst hopes the US government will finally focus on the growth agenda sent Wall Street to record highs. Within the DAX, Continental was the best performer, up 1.43%, followed by Daimler that added 0.72%. Bayer led decliners, shedding 1.51%, followed by Deutsche Bank that lost 1.04%. The index achieved most of its gains at the beginning of the week, spending the second half of it consolidating, maintaining its bullish stance daily basis, as it settled above all of its moving averages, whilst technical indicators held well above their mid-lines, although with limited upward strength. In the 4 hours chart, the index hovers around a bullish 20 SMA, whilst the Momentum indicator is aiming to recover around neutral territory, and the RSI indicator turns marginally higher around 66, all of which favors a new leg higher on a break above 12,567 the weekly high.

Support levels: 12,489 12,443 12,401

Resistance levels: 12,567 12,603 12,646

Technical Outlook: US Oil – Fresh Bulls Eye Last Week’s Peak At $50.48

WTI oil price regained traction on Monday after Friday's trading was shaped in Doji candle and returned above $50 barrier. Fresh bulls are establishing above weekly cloud top ($49.87) which was dented last week but failed to close above the cloud and eye last week's high at $50.48 (the highest since 25 May). Long weekly bullish candle (oil price rallied near 5% last week) underpins, along with firmly bullish daily techs. Eventual close above cracked Fibo 61.8% retracement of $55.01/$42.04 ($50.06) former top of 01 Aug at $50.41, would generate stronger bullish signal for resumption of recovery leg from $42.04 (1 June low) towards next barrier at $51.98 (25 May peak). Psychological $50 level now acts as initial support, followed by broken 200SMA ($49.57) which is expected to keep the downside protected.

Res: 50.41, 50.48, 50.77, 51.00

Sup: 50.00, 49.57, 49.00, 48.73