Sample Category Title

GBPUSD Intraday Analysis

GBPUSD (1.3203): The British pound posted declines yesterday as price action rallied to a fresh one-year high at 1.3328. We now expect the declines to continue further although GBPUSD could be seen posting a modest test towards 1.3236 level to establish resistance. The downside bias increases on a potential break down below 1.3160 support level. Below this level, GBPUSD comes at a risk of a strong decline towards the lower support at 1.2980 - 1.2961. Today's BoE meeting could be the main event that will influence the cable.

EURUSD Intraday Analysis

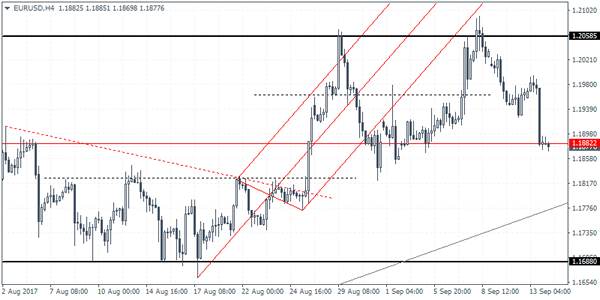

EURUSD (1.1877): The EURUSD extended declines yesterday as price action fell to the lower support level of 1.1882. The decline invalidates the cup and handle pattern that was being anticipated. Still, price action remains trading flat at the current levels with resistance at 1.1962 likely to be tested in the near term. This sideways range could signal a possible near-term breakout. Above 1.1962, EURUSD could once again aim for the next big level of 1.2058, while to the downside, a break down below 1.18822 could signal a move towards the next main support that comes in at 1.1688.

GBP Falls On Weaker Wage Growth, BoE Meeting Coming Up Today

The British pound's strong rally saw prices rising to a fresh one-year high, but the gains were capped as the latest jobs data showed that wage growth increased just 2.1% on the year. Compared to the 2.9% increase in inflation, the soft pace of wage growth kept the GBP in check. Investors shrugged off the unemployment rate which fell further to 4.3%.

Elsewhere, the US producer price index data showed a modest increase of 0.2% on the headline and 0.1% on core PPI, which was slightly better than the previous month. The US dollar was seen recovering on the back of the PPI data and easing global tensions.

Looking ahead, the SNB and the BoE meetings are the big-ticket events today. Both central banks are expected to hold monetary policy steady. For the BoE, traders will be looking to the forward guidance from the central bank.

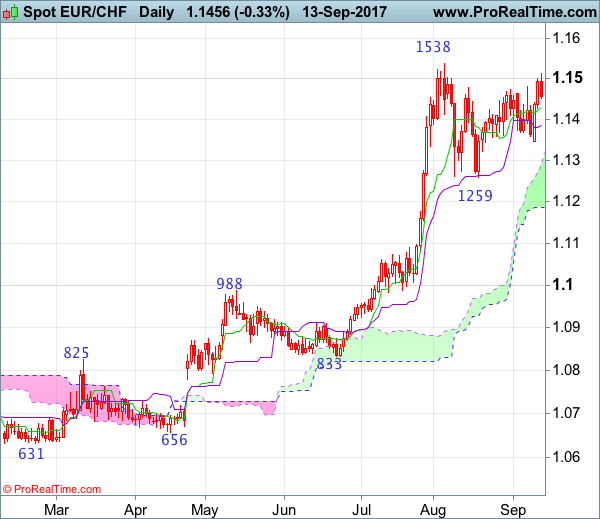

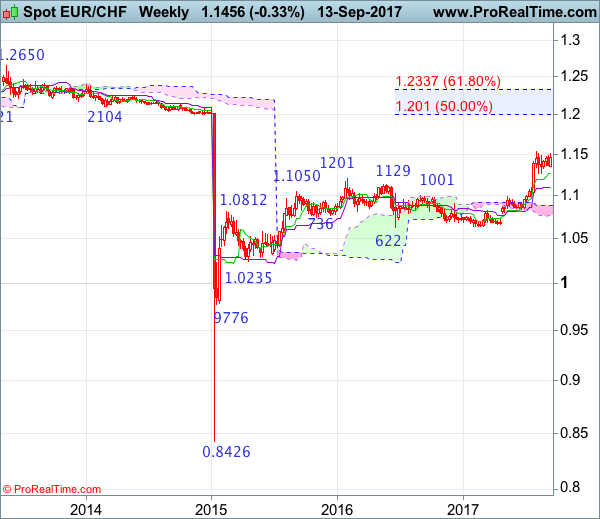

EUR/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 24 Jul 2017

• Trend bias: Up

Daily

• Last Candlesticks pattern: Morning doji

• Time of formation: 25 Jul 2017

• Trend bias: Up

EUR/CHF – 1.1467

As the single currency has rebounded again after finding support at 1.1350, bullishness remains for another rise towards resistance at 1.1538, however, break there is needed to confirm recent upmove has resumed and extend headway to 1.1600-10, having said that, further sharp move beyond 1.1700 should not be repeated and price should falter below 1.1770-80, risk from there is seen for a retreat to take place later this month.

On the downside, expect pullback to be limited to the Tenkan-Sen (now at 1.1429) and the Kijun-Sen (now at 1.1386) should remain intact, bring another rise to aforesaid upside targets. Below support at 1.1350 would defer and risk test of 1.1320-25, break there would suggest the rebound from 1.1259 has ended instead, bring retest of this level, below there would extend the corrective fall from 1.1538 top for retracement of recent upmove to 1.1185 (50% Fibonacci retracement of 1.0833-1.1538), however, sharp fall below 1.1100-05 (61.8% Fibonacci retracement) should not be repeated and 1.1050 would hold, bring rebound later.

Recommendation: Hold long entered at 1.1355 for 1.1555 with stop below 1.1350.

On the weekly chart, this week’s rebound after finding renewed buying interest at 1.1350, retaining our bullishness for recent upmove to resume after consolidation, above resistance at 1.1538 would confirm recent upmove has resumed and extend the major rise from 0.8426 low for headway to 1.1590-00, then towards 1.1700-10 but overbought condition should prevent sharp move beyond 1.1800 and reckon 1.1900-10 would hold from here, risk from there has increased for a retreat to take place later.

On the downside, expect pullback to be limited to 1.1400 and said support at 1.1350 should hold, bring another rise later. Below 1.1320-25 would risk test of 1.1259-63 (said support and current level of the Tenkan-Sen), a weekly close below there would shift near term risk to the downside and suggest a temporary top is formed instead, bring retracement of recent rise to 1.1100-05 (61.8% Fibonacci retracement of 1.0833-1.1538), then test of the Kijun-Sen (now at 1.1097) but reckon support at 1.0987 would remain intact.

What To Expect From The BoE?

Today's Bank of England Monetary Policy Committee (MPC) announcement is the main event of the week. While it is highly unlikely that we willsee an immediate interest rate hike, or a reduction in quantitative easing, the markets' biggest question following the rise in inflation, is whether the central bank will finally provide signals of tightening monetary policy.

On 3 August, when the BoE last met, the MPC voted by a majority of 6-2 to maintain rates at 0.25%. They also expected inflation to peak around 3% in October, which is where we almost stand now. BoE Governor Mark Carney suggested that markets are underestimating how soon interest rates will rise. However, investors are still unconvinced that an interest rate hike will come anytime soon, primarily because BoE's Chief Economist Andy Haldane did not vote in favour of this during the last meeting, despite sending signals of his readiness to vote for a hike;that is why his call today will be of great importance.

Economic data since the last meeting has been somewhat mixed. The weak sterling continued to support the manufacturing sector, with IHSMarkit'sPurchasing Manager Index rising to 56.9, a four-month high, suggesting that manufacturing remained healthy despite Brexit uncertainty. The service sector however, which dominates the U.K.'s economy and contributes around 80% of the total GDP, slowed to53.2 in August, down from 53.8 the previous month. More importantly, consumer spending remained weak despite the uptick in August, as higher prices and lower disposable income continued to affectU.K. consumers.

The brightest spot in the economy has been unemployment levels, which fell to a new 42-year low of 4.3%, news that was warmly welcomed by the MPC. However, low wages remain the BoE's and other central banks biggest conundrum. With inflation hitting 2.9%, real wages remained in negative territory and there's no clear indication whether it will pick up soon.

Mixed signals from the economy will provide ammunition to both hawks and doves, but traders need to know who will score more points today. If Andy Haldane sways to the minority of dissenters and votes for an immediate rate hike, it would signal that interest rates will go higher by the end of year, and GBPUSD will likely shoot above yesterday's high of 1.3328. However, if only two MPC members dissent, and inflation isgiven little attention, we may see Sterling slide back towards 1.30-1.31 range.

(SNB) Swiss National Bank Leaves Expansionary Monetary Policy Unchanged

The Swiss National Bank (SNB) is maintaining its expansionary monetary policy, with the aim of stabilising price developments and supporting economic activity. Interest on sight deposits at the SNB is to remain at –0.75% and the target range for the three-month Libor is unchanged at between –1.25% and –0.25%. The SNB will remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration.

Since the last monetary policy assessment, the Swiss franc has weakened against the euro and appreciated against the dollar. Overall, this development is helping to reduce, to some extent, the significant overvaluation of the currency. The Swiss franc nevertheless remains highly valued, and the situation on the foreign exchange market is still fragile. The negative interest rate and the SNB's willingness to intervene in the foreign exchange market as necessary therefore remain essential in order to reduce the attractiveness of Swiss franc investments and thus ease pressure on the currency.

Owing to the exchange rate situation, the conditional inflation forecast has been revised upwards slightly compared to June. For the current year, the forecast has risen marginally to 0.4%, from 0.3% in the previous quarter. For 2018, too, the SNB anticipates an inflation rate of 0.4%, compared to 0.3% last quarter. For 2019, it now expects inflation of 1.1%, compared to 1.0% last quarter. The conditional inflation forecast is based on the assumption that the three-month Libor remains at –0.75% over the entire forecast horizon.

The past few months have seen further improvements in the international environment. The global economy exhibited strong, broad-based growth in the second quarter. In the advanced economies, GDP continued to expand above potential, in some cases exceeding expectations. One exception was the UK, where uncertainty over Brexit is weighing on growth. In the emerging economies, too, economic activity was positive overall. In its baseline scenario, the SNB continues to anticipate favourable developments in the global economy for the quarters ahead.

Despite the improved situation in the real economy, inflation has so far remained modest in most advanced economies. Against this backdrop, leading central banks are likely to maintain their expansionary monetary policy and embark only gradually on a normalisation path.

The positive baseline scenario for the global economy continues to be subject to risks. In particular, geopolitical factors and uncertainty regarding the future course of monetary policy at leading central banks could cloud the outlook.

In Switzerland, an analysis of the available economic indicators suggests that the moderate recovery is continuing. The Swiss economy is benefiting from the consolidation of global economic activity. Renewed momentum in goods exports is supporting industrial activity. Capacity utilisation is thus on the rise and companies are also becoming increasingly willing to invest. The situation on the labour market is gradually improving.

The recovery is less evident in the quarterly GDP estimates. Owing to weak GDP momentum in late 2016/early 2017, the current year is likely to see growth of just under 1.0%. At its monetary policy assessment in June, the SNB was still expecting growth of roughly 1.5%. The lower forecast is attributable to the weak GDP figures for the previous quarters.

Overall, imbalances on the mortgage and real estate markets persist. While growth in mortgage lending remained relatively low in the second quarter, risks in the residential investment property segment increased. In addition, following a period of stabilisation, prices in the owner-occupied residential property segment rose again slightly. The SNB will continue to monitor developments on these markets closely, and will regularly reassess the need for an adjustment of the countercyclical capital buffer.

UK Unemployment At 42 Year Low

UK unemployment fell to its lowest level since 1975, data on Wednesday revealed. Unemployment fell by 75K, bringing the unemployment rate down to 4.3% (from 4.4%). Wage growth was unchanged from the previous release at 2.1%, but recent inflation data of 2.9% shows wage growth is clearly not keeping up. A strong labour force is helping UK growth but the specter of a rate hike, to keep inflation near to the Bank of England’s 2% target, has the markets concerned, although many do not see an increase until well into 2018.

A plethora of data was released from China on Thursday, showing weaker than expected numbers. Year-on-Year data showed Chinese retail sales at 10.1% (forecast 10.5%), Industrial Production at 6% (forecast 6.6%) and fixed asset investment at 7.8% (forecast 6.6%). Whilst the released data missed forecasts they still indicate a strong economy that is helping global demand.

In the US, Speaker of the House, Ryan, stated on Wednesday that a plan for tax reform would be released by the Republicans in the week of September 25th. An overhaul in the US Tax system is desperately needed by the Trump Administration as they have struggled to implement any of their planned initiatives. The markets will now be focusing on several interest rate decisions in Europe and inflation data from the US today.

EURUSD moved lower, following a 0.7% drop on Wednesday. Currently, EURUSD is trading around 1.1875.

USDJPY is little changed in early trading. Currently, USDJPY is trading around 110.45.

GBPUSD suffered as sluggish wage growth data were blamed for a fall in value of GBP against USD. Currently, GBPUSD is trading around 1.3205.

Gold was little changed overnight, currently trading around $1,322.

WTI moved higher on Wednesday, following the EIA report that global oil demand is at its highest level since 2015. Currently, WTI is trading around $49.60.

Major economic data releases for today:

At 08:30, the Swiss National Bank will release their Interest Rate Decision. Rates are not expected to change form the existing 0.75%, but the markets will pay attention to the tone of the announcement for clues as to when policy may soften.

At 12:00, the Bank of England will release their Interest Rate Decision. With recent increases in UK inflation, the markets will be looking for clues as to the timetable for future rate hikes in the minutes that will also be released. Consensus calls for there to be no change in rates today.

At 13:30 BST, the US Bureau of Labor Statistics will release US CPI & CPI Exc. Food & Energy (YoY) for August. CPI exc. Food & Energy is forecast to come in at 1.6% (prev. 1.7%), whilst CPI is forecast to come in at 1.8% (prev. 1.7%). The impact of the recent Hurricanes & the resulting recent gasoline price hikes may result in a distorted release. Markets are likely to see USD volatility regardless of the data released.

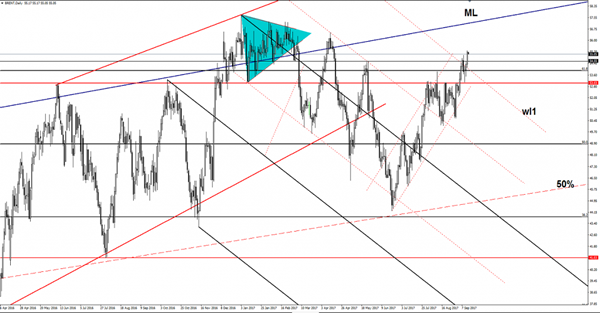

Gold Slips Lower

The yellow metal drops further on the short term and closed the former gap up. Is under selling pressure on the short term as the USD has managed to increase versus all its rivals. A further USDX increase will send the Gold towards the $1307 per ounce, where we have an important static support. Support can be found at the warning line (WL1) as well.

Brent Oil Further Increase Confirmed

The price has rallied in the last two sessions and have managed to breakout above the warning line (wl1) of the major descending pitchfork. Brent jumped above the 54.96 previous high as well and confirms a further increase. It should climb towards the $57 per barrel in the upcoming period, even if we’ll have a minor decrease because the price could make a minor consolidation here.

We have a major upside target at the median line (ML) of the major ascending pitchfork. Technically, it was expected to approach the median line (ML) after the failure to reach and retest the 50% Fibonacci line.

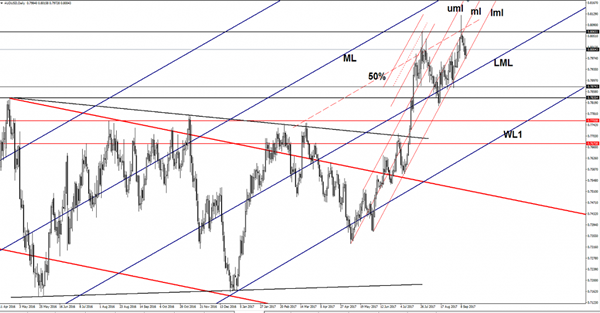

AUD/USD Throwback

The AUD/USD increased significantly in the morning and recovered a little after the yesterday’s impressive drop. Is trading in the green right now after the rejection from a dynamic support level. The rebound could be only temporary if the USDX will resume the yesterday’s bullish momentum.

AUD/USD maintains a bullish perspective on the short term because is still trapped in the green zone. However, the rate showed some exhaustion signs on the Daily chart, but we still need a confirmation that will start another leg lower.

The AUD/USD increased somehow surprisingly today as the Australian data have come in mixed, while the Chinese figures have disappointed. The Australian Employment Change surged from 29.3K to 54.2K, beating the 17.5K estimate, while the Unemployment Rate remains steady at 5.6%. The MI Inflation Expectations rose by 3.2%, less versus the 4.2% growth in the former reading period.

The Aussie ignored the Chinese Industrial Production release, the indicator increased only by 6.0%, less versus the 6.6% estimate.

Price was rejected by the lower median line (lml) of the minor ascending pitchfork and now tries to climb higher again. Personally, I’m expecting to see a further drop on this pair, a valid breakdown below the lower median line (lml) of the ascending pitchfork will open the door for more declines in the upcoming period.

A major drop will be validated after a breakdown and a retest of the lower median line (LML) of the major ascending pitchfork.